HJBC/iStock Editorial via Getty Images

Investment thesis

I started covering Société BIC (OTCPK:BICEF) (OTCPK:BICEY) in December 2020 as impacts from self-imposed restrictions to stop the spread of the coronavirus worldwide, as well as operating weakness due to lack of enough product innovation and diversification over the years, caused a 70% share price decline from all-time highs reached in 2015. Furthermore, the global projected decline in smoking rates and the digitalization of school material and office tasks suggested that the trend would continue to be negative as long as the company did not adapt to these changes. I updated the situation in September 2023 as it seemed like the management was finally taking the necessary steps to get back on the growth path, but the share price was still 60% below all-time highs as inflationary pressures were having a significant impact on EBIT margins while recessionary concerns fueled investors’ pessimism.

In both articles, I explained the reasons why I believed that the share price decline represented a good opportunity for long-term dividend investors with enough patience to wait for the company’s picture to improve, and in this article, I am going to break down the results of Q3 2023 and explain why I do think that these results continue to reflect positive results from the efforts carried out in since 2020 under the Horizon Plan.

Since 2020, the company has expanded its total addressable markets thanks to recent acquisitions and product innovation, and profit margins have continued to improve in recent quarters. Throughout this time, the company has remained highly profitable, which has allowed it to maintain an exceptionally robust and debt-free balance sheet. Therefore, I consider this a good time for any dividend growth investor with a long-term horizon interested in geographically diversifying their portfolio as the share price remains depressed.

A brief overview of the company

Société BIC is a French manufacturer of disposable consumer products focused on stationery supplies, lighters, razor blades, and more recently products for the design of temporary tattoos. The company was founded in 1945 and its market cap currently stands at €2.75 billion, so its size is large but not immense as it fits in the low range of the mid-cap category. Also, the company enjoys a highly diversified global presence as 43% of revenues were generated in North America in 2022, 29% in Europe, 17% in Latin America, 6% in the Middle East and Africa, and 5% in Asia and Oceania.

BIC BodyMark (Eu.bic.com/en-gb/beauty/bodymark)

The company’s operations are divided into three main business segments: Blade Excellence, Flame for Life, and Human Expression. Under the Flame for Life segment, which provided 39% of revenues in 2022, the company manufactures lighters for all kinds of use cases. Under the Human Expression segment, which generated 38% of revenues in 2022, it manufactures office and school supplies, creative expression products (including temporary tattoos), and digital stationery including tablets and digital pens, among others. Lastly, under the Blade Excellence segment, which generated 22% of overall sales in 2022, the company manufactures shavers, as well as blades and handles for other brands.

The company is currently investing in the development of higher-value products to ensure steady revenue streams in the long term and achieve improved margins, which include the diversification of the use cases of their lighters beyond tobacco, improved shavers for more sensitive skins, and the company’s introduction to the temporary tattoo market.

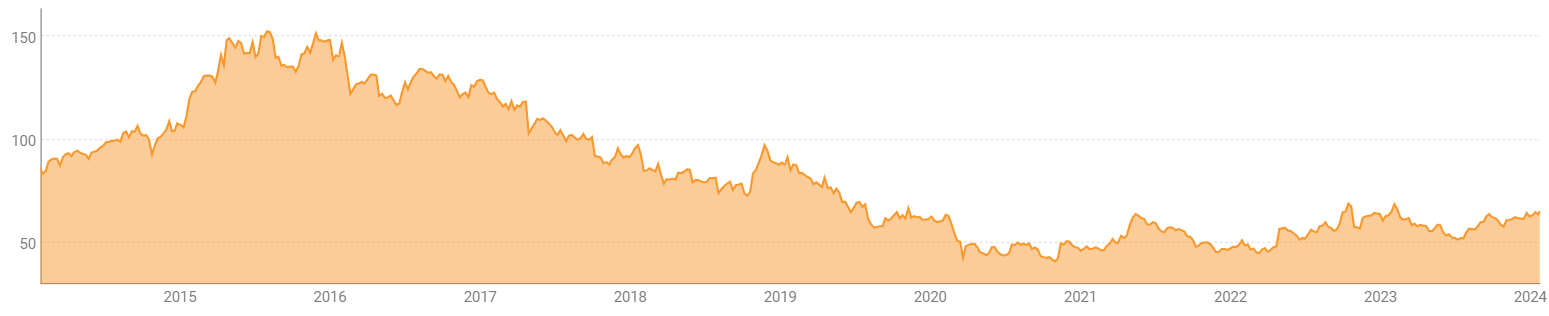

BIC Share price (Investors.bic.com/en-us/calendar-and-share/stock-market-prices)

Currently, shares are trading at €64.75, which represents a 59.24% decline from all-time highs of €158.84 in August 2015 but a 3.02% increase since the last article I wrote, with which the price of the shares has moved very little after the Q3 2023 results despite them showing significant margin expansion and reflecting ongoing efforts continue contributing to revenue growth.

Revenues remain high and are expected to continue increasing in 2024

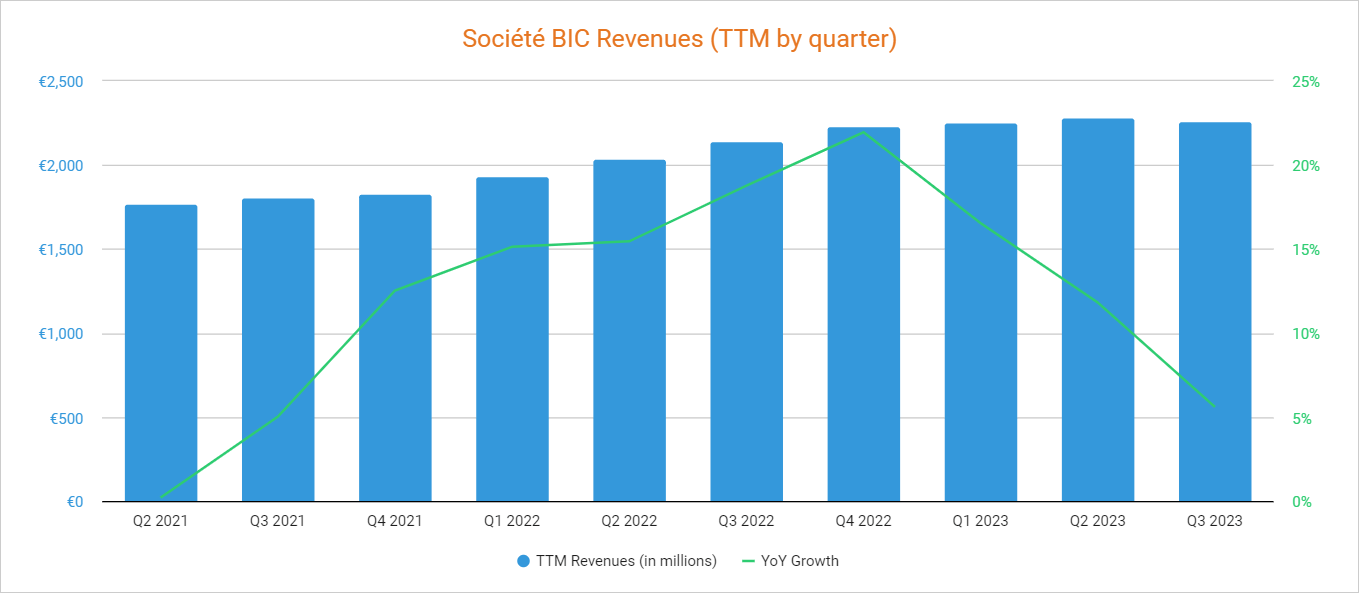

The company suffered a steady revenue decline in the 2015-2020 period, with the largest drop experienced in 2020 as a result of the coronavirus pandemic, leaving a total 27.38% decline compared to 2015. Despite this, everything began to improve with the reopening of the global economy in 2021 with an increase of 12.53% compared to 2020 and another increase of 21.95% in 2022, boosted by price raises and acquisitions. As for 2023, revenues increased by 4.46% year over year in Q1 and by 4.38% year over year in Q2.

Societe BIC TTM Revenues (Seeking Alpha)

Despite this, revenues decreased by 3.41% year over year in Q3 2023, and although this result represents a decrease of 12.21% quarter over quarter, this is mostly attributable to the company’s seasonality as Q2 is typically the strongest quarter of every year, so the recent drop must be analyzed through a year over year comparison. In this regard, it’s important to note that revenues actually grew by 7.2% year over year if calculated on a constant currency basis, and the management has maintained its expectations of closing 2023 with sales growth in the 5% to 7% range. Furthermore, 2024 is also expected to deliver ~5% revenue growth, which would confirm the break of the negative trend experienced in the 2015-2020 period, although this should not move the needle if it is not accompanied by further EBIT margin improvements. Still, the global temporary tattoo market is expected to grow at a CAGR of ~9% in the 2023-2030 period, which should contribute to long-term growth for the company beyond 2024.

In short, the company reported trailing twelve months’ revenues of €2.26 billion in Q3 2023, which is slightly above the €2.24 billion reported in 2015. Still, significant headwinds continue to be a challenge as inflationary pressures are causing a deterioration in the purchasing power of many families around the world, which has pushed them to extend the use of the company’s products or even switch to cheaper brands or private labels. Also, these same pressures continue to negatively impact margins, albeit to a lesser extent, at a time marked by strong pricing pressures from other manufacturers.

EBIT margins keep improving and the company is highly profitable

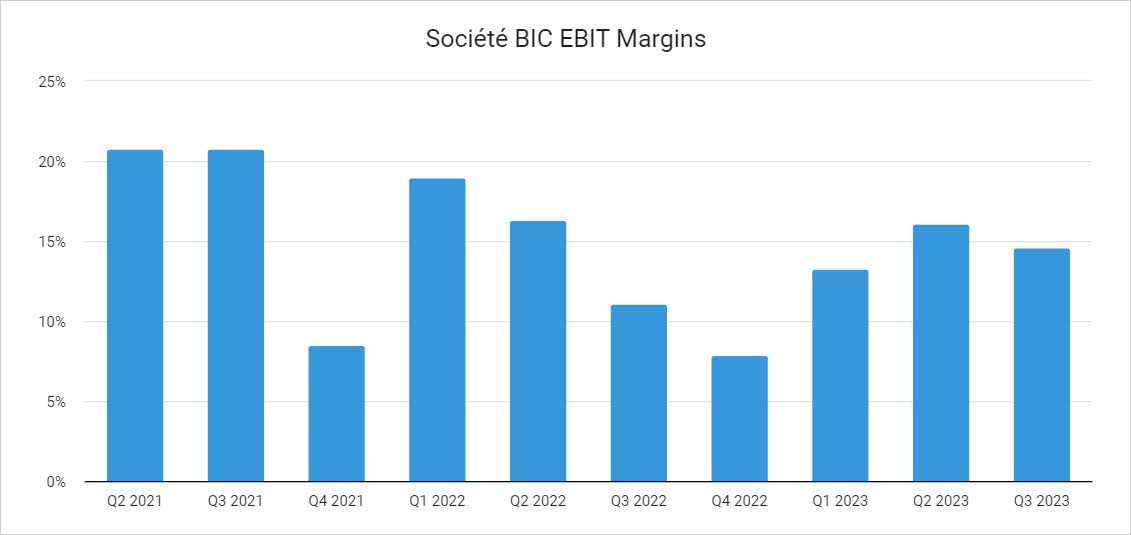

Although trailing twelve months’ revenues show that the company recovered lost revenues since 2015, this has not been enough to fully recover profit margins as higher raw material and electricity costs, unfavorable foreign exchange rates, higher OpEx, and marketing efforts to boost BIC EZ Reach sales in Europe continue to negatively impact EBIT margins.

Before 2019, the company used to enjoy EBIT margins that danced around 20%, but these have deteriorated in recent quarters as trailing twelve months’ EBIT margins stood at 12.90% in Q3 2023. Still, EBIT margins of 14.6% during the quarter represented a significant improvement from the 11.1% reported in the same quarter of 2022 boosted by manufacturing efficiencies, lower raw material prices, and more favorable forex. In this sense, it seems that EBIT margins continue to improve, which is a very positive sign.

Société BIC EBIT Margins (Financial reports)

This improvement shows how pricing actions and manufacturing efficiency initiatives are progressively offsetting current headwinds, but pricing pressures from competitors in the United States remain a challenge. Currently, the trailing twelve months’ EBIT margin stands at 12.90%, which suggests that the company continues to be highly competitive as the sector median is significantly below at 9.84%. Still, investors remain concerned as revenues from its most profitable segment, Flame For Life, only increased by 3.9% year over year in Q3 at constant currencies compared to the overall 7.2% increase, which shows a significant slowdown while its adjusted EBIT margin of 34.1% is significantly higher than that of the rest of segments (7.5% in Human Expression and 18.7% in Blade Excellence). Still, the global pocket lighter is expected to grow at a CAGR of ~3% in the 2023-2032 period, so I would not expect the segment to lose strength in the foreseeable future.

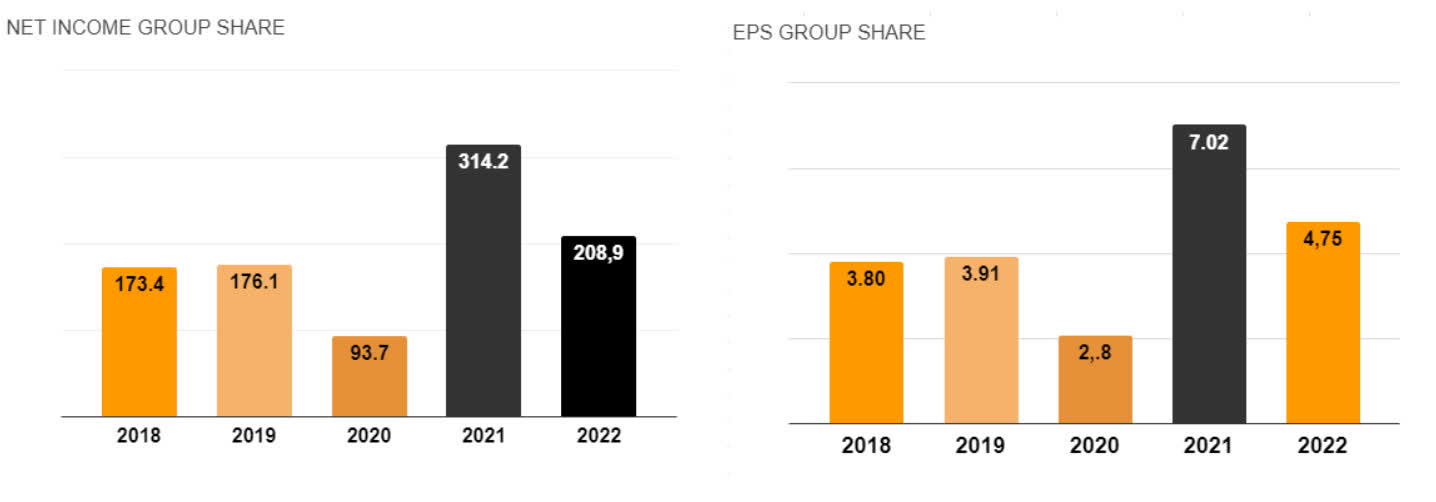

Regarding the current situation, the last quarter shows that the efforts carried out since 2020, as well as the recent relaxation of headwinds experienced in 2022, are having a positive impact on profit margins as the company reported a net income of €59.8 million in Q3 2023 compared to €46.8 million in the same quarter of 2022, and EPS of €1.39 compared to €1.06.

BIC 2018-2022 Net income and EPS (Investors.bic.com/en-us/strategy-and-governance/key-figures)

In this regard, the company is highly profitable and profit margins continue to improve. In addition, it has a very robust balance sheet that should allow it to continue navigating the current headwinds while continuing with the Horizon Plan, which is expected to bring new products in 2024 and 2025 and, possibly, new acquisitions to continue increasing the total addressable market.

The balance sheet is very strong as the company is debt-free

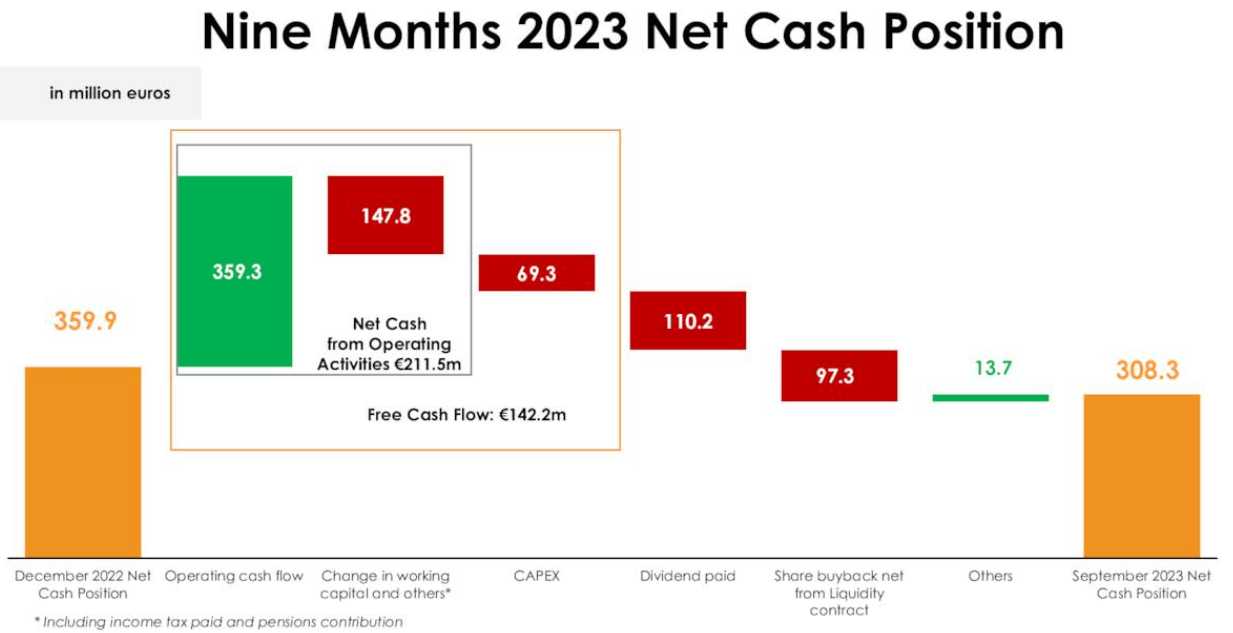

The company enjoys a debt-free balance sheet and held €308.3 million in its net cash position at the end of Q3 2023, which represented a €51.6 million decline year-to-date. Still, this decline is mostly attributable to aggressive share buybacks of €97.3 million during the same period, negative changes in working capital and others of €147.8 million, and higher CAPEX of €69 million (compared to €57.4 million in the same period of 2022). Additionally, it must be taken into account that annual dividends paid of €110.2 million took place within these first 9 months, and Q4 won’t be affected by it as no dividends are paid in Q4.

BIC YTD Cash position (Q3 2023 Results presentation)

This shows the company’s high profitability and suggests that cash from operations should be more robust in the coming quarters due to increased working capital, so the annual dividend of €2.56 per share is, in my opinion, highly safe and even gives the management some margin to continue increasing it in the coming years.

The dividend is safe

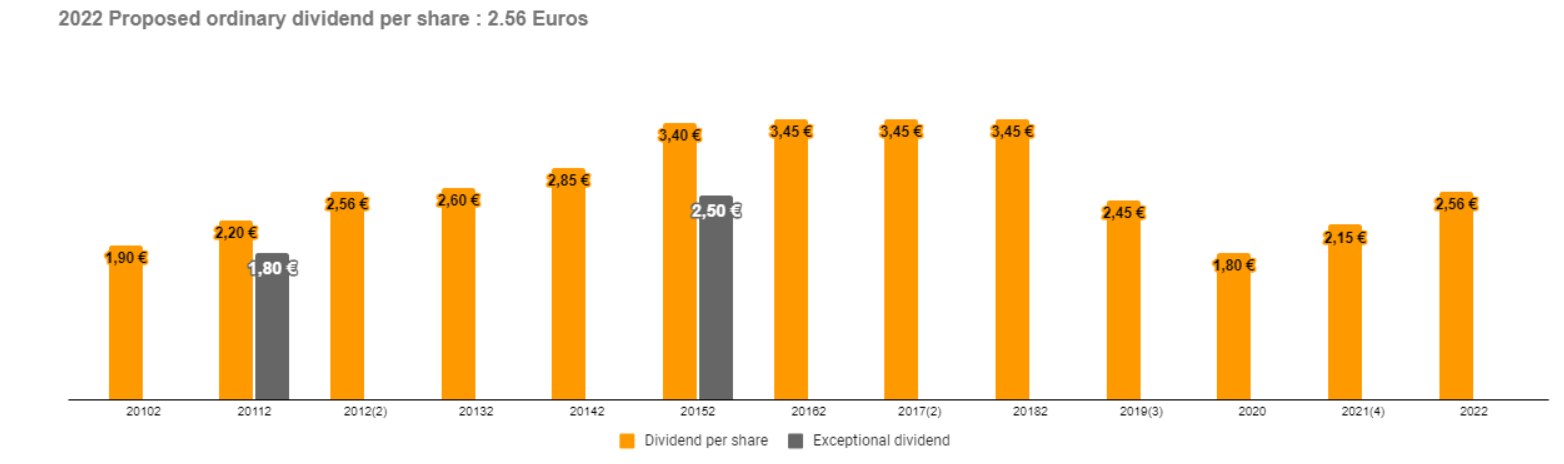

After increasing by 1.47% in 2016 to €3.45 per share, the proposed annual dividend remained frozen in 2017 and 2018 until the management decided to cut it by 28.98% in 2019 and by a further 26.53% in 2020 to preserve as much cash as possible amidst the deterioration of cash from operations. Since then, the dividend has increased by 19.44% in 2021 and by a further 19.07% in 2022 to €2.56.

Societe BIC Dividends per share (Investors.bic.com/en-us/strategy-and-governance/key-figures)

This dividend is still 25.80% lower compared to the €3.45 proposed in 2016, 2017, and 2018, while the current dividend yield is 3.95% due to the share price decline experienced in recent years. Furthermore, the dividend yield on cost would stand at 5.33% if the company restored the 2018 dividend in full. In this sense, the dividend has a lot of upside potential in the coming years as the cash payout ratio has historically been low as you can see in the table below.

| Year | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 | 2022 |

| Cash from operations (in millions) | €349.0 | €367.1 | €298.7 | €380.6 | €303.9 | €317.2 | €357.6 | €280.6 | €300.0 |

| Dividends paid (in millions) | €122.4 | €134.8 | €277.0 | €161.0 | €157.8 | €155.2 | €110.2 | €80.9 | €94.7 |

| Cash payout ratio | 35.07% | 36.72% | 92.74% | 42.30% | 51.92% | 48.93% | 30.82% | 28.83% | 31.57% |

In this regard, a negative change of -€51.6 million in the net cash position in the first 9 months of 2023 reflects that the company is still capable of comfortably covering its dividend considering unusually high share buybacks of €97.3 million and a negative impact of €147.8 million due to changes in working capital and others, pending the Q4 results in which no dividend will be paid. Furthermore, the non-existence of debt means that no interest expenses need to be covered at the end of each period, which offers a significant competitive advantage to the company and significant safety to investors.

Share buybacks remain in force

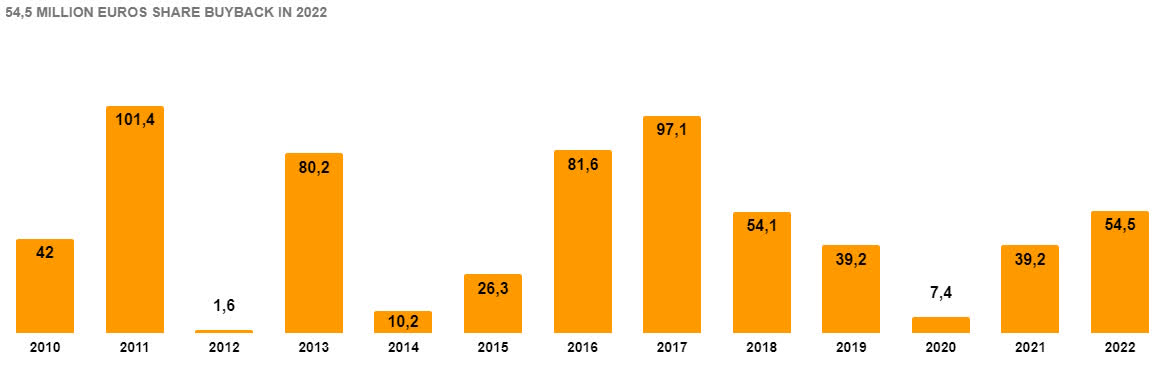

The company has a long tradition of buying back shares as a way to reward long-term investors as the total number of shares outstanding decreased by 13.72% from Q3 2013 to Q3 2023. This means that each share represents a growing portion of the company as the results are distributed among fewer shares, which progressively improves per-share metrics.

BIC Share Buybacks (Investors.bic.com/en-us/strategy-and-governance/key-figures)

Furthermore, the company already repurchased €97.3 million worth of shares in 2023 still pending Q4 results, which means that share buybacks are still in force. For this reason, investors could expect their position to slowly grow (in terms of the size of the company that each share represents) over the years, which should positively contribute to their total return in the long term. Also, fewer outstanding shares should make way for future dividend raises as the dividend is distributed among fewer and fewer shares as time passes.

Risks worth mentioning

In the long term, I consider BIC’s risk profile to be quite low because, after all, it is a highly profitable company with a long tradition of manufacturing essential products that enjoys a very robust balance sheet and no debt. Despite that, there are certain risks that I would like to highlight.

- Recent interest rate hikes could trigger a global recession, which could have a direct impact on the company’s operations as consumers could extend the use of BIC’s products before replacing them to save money or even move to cheaper brands.

- The global pocket lighter market is expected to show very moderate growth in the coming years, which means the company must provide added value to its products from other business segments to achieve and maintain the profitability enjoyed during the years before the coronavirus pandemic. In this regard, the challenges are not few and the company could report lower EBIT margins compared to the past for a very long time if it loses market share in the lighter industry.

- Profit margins could contract again if inflationary pressures intensify again, and this could also have a further impact on consumers’ purchasing power.

- The dividend could grow at lower rates from now on. It is important to remember that the dividend growth experienced in 2021 and 2022 came, in part, because the company cautiously cut the dividend in 2019 and 2020 due to operating weaknesses and the coronavirus pandemic, so it could be expected that dividend growth will moderate as it approaches the €3.45 proposed in 2016, 2017 and 2018. Still, the dividend yield on cost of €3.45 per share would be 5.33% at the current share price, so the dividend upside potential is high.

- The pace of share buybacks could be slowed if EBIT margins and sales do not continue to improve or if new headwinds are added to the current context as the management could decide to preserve cash to navigate temporary headwinds.

Conclusion

When the results of the third quarter of 2023 were published, 2.5 years had passed since the Horizon plan was launched, and there are still 2.5 more years left until its completion. Since then, operations have improved significantly and sales have surpassed (albeit barely) 2015 levels, breaking the negative trend of recent years. The third quarter of 2023 is no exception as revenues remained robust, and EBIT margins have continued to expand. Furthermore, the company continues to enjoy an exceptionally strong balance sheet as the dividend is fully covered with relative ease.

The fact that the slowdown in sales growth is more notable in the most profitable segment continues to worry investors, and the share price remains 59% below the all-time high as a consequence as it could take many years until margins fully recover. But despite this pessimism, I believe that long-term dividend growth investors interested in providing some geographic diversification to their portfolio could take advantage of the low share prices as the long-term dividend yield on cost potential is high. In fact, the current 3.95% yield is already quite generous, in my opinion, not only because of the upside potential but also because the cash payout ratio has been historically low.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")