nadla/iStock via Getty Images

Snowflake (NYSE:SNOW) has experienced extraordinary growth at the topline since going public in 2020 with no end to growth in sight. As the renaissance for AI and advanced data analytics continues to take form, Snowflake’s data hosting and analytics platform will be central for advancements in business intelligence. The ultimate outcome for Snowflake will be determined by which direction companies choose to host and analyze their data, whether it be on-prem or in the cloud. Through scale comes the risk of slowing growth and I believe Snowflake may experience slower growth in eFY25 as the firm reaches a more mature growth stage. SNOW is also significantly overvalued at 25.45x trailing sales, well above their nearest competitor MongoDB (MDB) at 17.58x. I provide SNOW a SELL recommendation with a price target of $148.16/share at 17.5x eFY25 revenue.

Operations

Corporate Reports

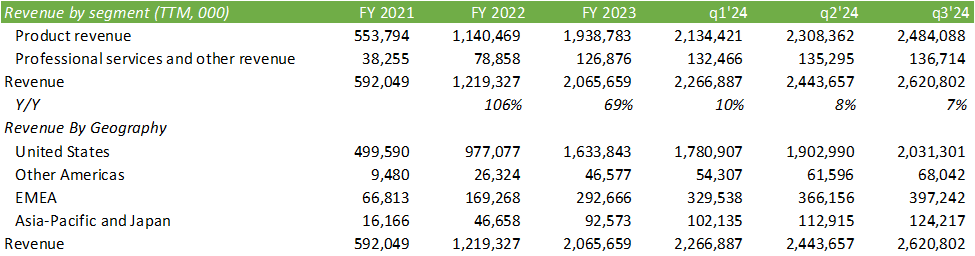

Considering Snowflake’s operations, revenue generation appears to be growing closer to a more mature growth rate on a TTM basis, experiencing a sequential slowdown quarter-to-quarter. Though this isn’t necessarily a negative trend, I believe that it may suggest that the “land” phase is nearing completion and now it is time for the firm to focus on the “expand” aspect. The firm has grown its customer base to include 647 of the Forbes Global 2000 customers and has 436 customers with a TTM $1mm spend. During the quarter, Snowflake added 4 customers with over $5mm in spend and 2 with over $10mm. The firm’s RPOs now stands at $3.7b, 57% of which will be recognized in the next 12 months.

Snowflake also has an additional avenue to garner government contracts with their recent FedRAMP authorization. This will allow the firm’s software to be used with federal agencies as they have cleared their stringent GRC requirement. This could be trekking into Palantir (PLTR) territory with government-related contracts in their own respect, or be utilized simultaneously.

Considering the company’s progression from aggregating data in 2014, to connecting and scaling data on the cloud in 2018, and bringing analytics into the mix in 2022, I believe the firm is beginning to near industry saturation on their platform and needs to emphasize the business intelligence component to remain both relevant and cost effective. Though Snowflake is still far from reaching its full implementation potential, I believe that the high-flying growth phase is beginning to wind down and I believe management’s focus on margins suggests that they may see this as well.

Management guided a 37% increase in product revenue for eFY24, reaching $2.65b, with q4’24 product revenue in the range of $716-721mm. Adding in professional services revenue, I anticipate Snowflake to achieve 2,788mm for eFY24. Though not yet at the scale to be an independent reportable segment, management mentioned that Snowpark grew by 47% sequentially. Snowpark is their unstructured data analytics platform that can be used for LLM/AI-related applications.

Corporate Reports

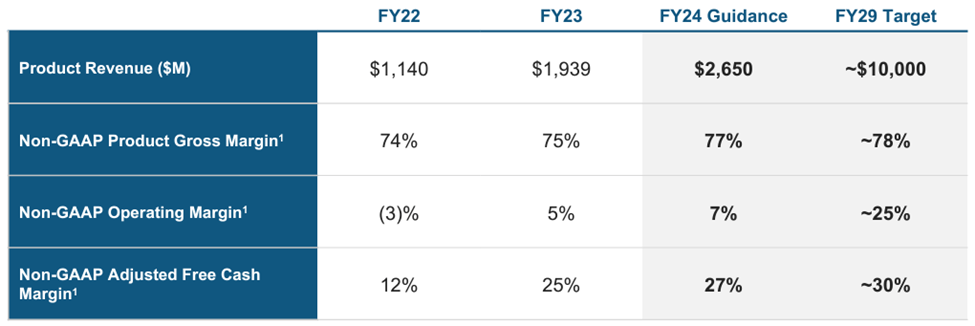

Using management’s guidance, we can walk through their operations at 7% adjusted operating income and 77% adjusted gross margin for eFY24. This will give us $195mm and $2,147mm for adjusted operating income and adjusted gross margin. This would lead adjusted operating income for q4’24 to have a 20% margin at $152mm, a significant improvement from any previous quarter.

Corporate Reports

At this level, it would appear that management is seeking to improve margins going forward. Using these figures, we can work through their reported GAAP and equate stock-based compensation to be in the ballpark of $122mm for eq4’24, or $984mm for eFY24 and account for 28% of OPEX+COGS vs. the historical rate of 30%.

Corporate Reports

Considering management’s long-term expectations, these figures should improve as non-GAAP operating margins approach 25% by 2029.

Corporate Reports

Though this target is perfectly achievable, I do believe that it may be challenging for Snowflake to grow revenue by 2.6x eFY24 levels without aggressive M&A. I do believe that larger firms with internal resources will opt to leverage their on-prem data lakes as opposed to utilizing cloud platforms to save on costs, which will be further discussed in the macro section. Regarding cost reduction, utilizing Snowflake’s platform for performance optimization may lead to reduced IT spending, so this could really go either way. One of the benefits of using Snowflake’s platform vs. an on-prem database is scalability. Having the convenience of expanding storage at the click of a button can save a firm tremendously in time and hardware costs. Security can also be a major factor in utilizing Snowflake’s platform in which liability for a breach can be mitigated, saving the firm from challenges raised by the new SEC reporting rule.

Working through their cash flow statement, Snowflake’s deferred revenue appears to be experiencing more outflow than inflow with deferred revenue in decline from its high watermark in FY22. Though judging by their revenue growth, that may only suggest consumers are opting to pay as you go as opposed to committing to longer-term agreements. It may also be an indicator of fewer organizations purchasing long-term platform agreements and opting to use their data on-prem, as management at Intel (INTC) would suggest (further discussed in my macro analysis).

Corporate Reports

Stock-based compensation accounts for a major proportion of adjustments made in the cash flow statement. Though stock-based compensation is technically a non-cash operating expense, the company buying back and issuing shares may make one think otherwise. Given that stock-based compensation accounts for 30% of operating costs, I don’t believe it to be prudent to discount this factor when valuing the firm.

Macro

The biggest question to ask when approaching Snowflake is whether companies will elect to store and analyze their data in the cloud or in their data center on-prem. Considering Nvidia’s (NVDA) approach in working with the hyperscalers, one would insinuate that companies would choose cloud over on-prem. On the opposite end, Intel anticipates that consumers will choose to host and analyze their data on-prem. Though this is a very subjective question on which to discern, I believe for the purposes of scalability of larger data models, organizations will opt to host their own data to control more of the costs. As alluded to in my article covering Intel, IT spending in 2024 will grow but will more heavily focus on cost-savings initiatives and organizational optimization.

Valuation & Shareholder Value

Corporate Reports

Management has a $2b share repurchase program as authorized February 2023 and has repurchased 4mm shares as of q3’24 for an aggregate price of $591.7mm with $1.4mm remaining. Management guided that diluted shares outstanding for q4’24 will be 360mm, about 30mm additional shares from the current level. With the additional dilution at the current market cap, shares should reprice to $185/share.

Looking at shareholders, institutional investors net sold SNOW shares in the last quarter, per Atom.Finance.

atom.finance

Significant insider sales took place in the last quarter with Frank Slootman, CEO, selling 651,306 shares since September 28, 2023, Christopher Degnan, Chief Revenue Officer, selling 125,474 shares since December 14, 2023, and Christian Kleinerman, SVP of Product, selling 5,224 shares since November 14, 2023.

Looking at valuing SNOW, peer comps price SNOW at a significant premium with its closest public peer, MongoDB (MDB) trading at 17.58x sales. Using 17.50x eFY24 sales, we can come up with a price target of $148.16/share. Considering the firm’s slowdown in revenue growth and the decline in deferred revenue, I find it difficult for Snowflake to achieve their goal for $10b in revenue for FY29. I provide SNOW a SELL rating with a price target of $148.16/share.

Corporate Reports

Considering their tactical price performance, $148/share sits at their hypothetical pricing floor and matches with the 0.382 retracement. The alternative would be that SNOW experiences a significant revenue beat and guides a strong q1’25, which can result in shares reaching up towards $230/share. I believe the downside risks outweigh the upside and I also believe management selling significant amounts of shares might be a signal in that direction.

TradingView

Q2 2024 Earnings Call Transcript")