Wirestock

Introduction

I wanted to look into Skechers (NYSE:SKX) since I haven’t covered the company in over half a year, so I wanted to see how it has performed over the last year. It also has earnings coming up at the end of April, which begs the question if it would be the right time to start or to add to a position before the report. The company has performed well over the year, and my long thesis is more than intact, however, there may be softness coming in this report which may present an even better entry point if you like the company long-term, therefore, I am assigning a hold rating until we see what the report gives us.

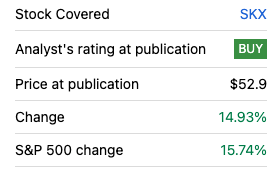

Since the first time I covered the company, the shares have advanced around 15%, which matched the S&P500 Index (SPY). In that article, I argued the company has a lot of potential to expand its DTC segment and the wholesale segment is still strong. What I did not foresee was the Wholesale business becoming much weaker and DTC becoming the largest revenue generator, but overall my buy rating held up well as I believed in the DTC segment doing well, which would lead to higher margins in the end.

Stock Performance since the first article (SA)

Briefly on Performance

As of FY23, which ended 31st of December ’23, and was published on February 28th ´24, the company had around $1.26B in cash and short-term investments against $242m in long-term debt. That is not a bad position to be in. The liquidity that the company has can easily cover all of the outstanding debt, while the company’s EBIT can easily cover annual interest expenses on debt too as its interest coverage ratio stood at around 35x. For reference, many analysts consider an interest coverage ratio of 2x to be sufficient, so it is safe to say the company is at no risk of insolvency and has no liquidity issues. Now, let’s look at other important metrics and how these have progressed throughout 2023. Starting with margins.

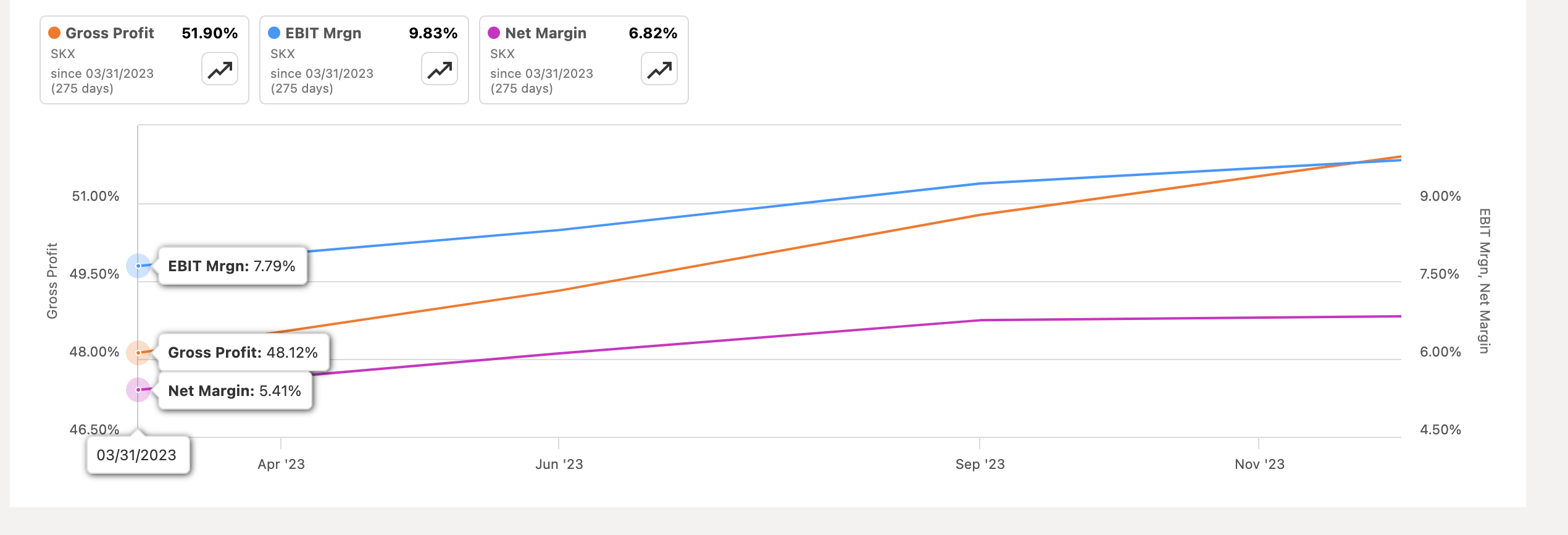

Retail businesses are known to have thin margins, so I am quite impressed that over the past year, SKX managed to improve margins across the board. The improvements can be attributed to the amazing growth of its Direct-to-consumer segment, which saw around 20% growth in the year, an increase in average selling price from product and channel mix, and savings on freight costs.

Margins (SA)

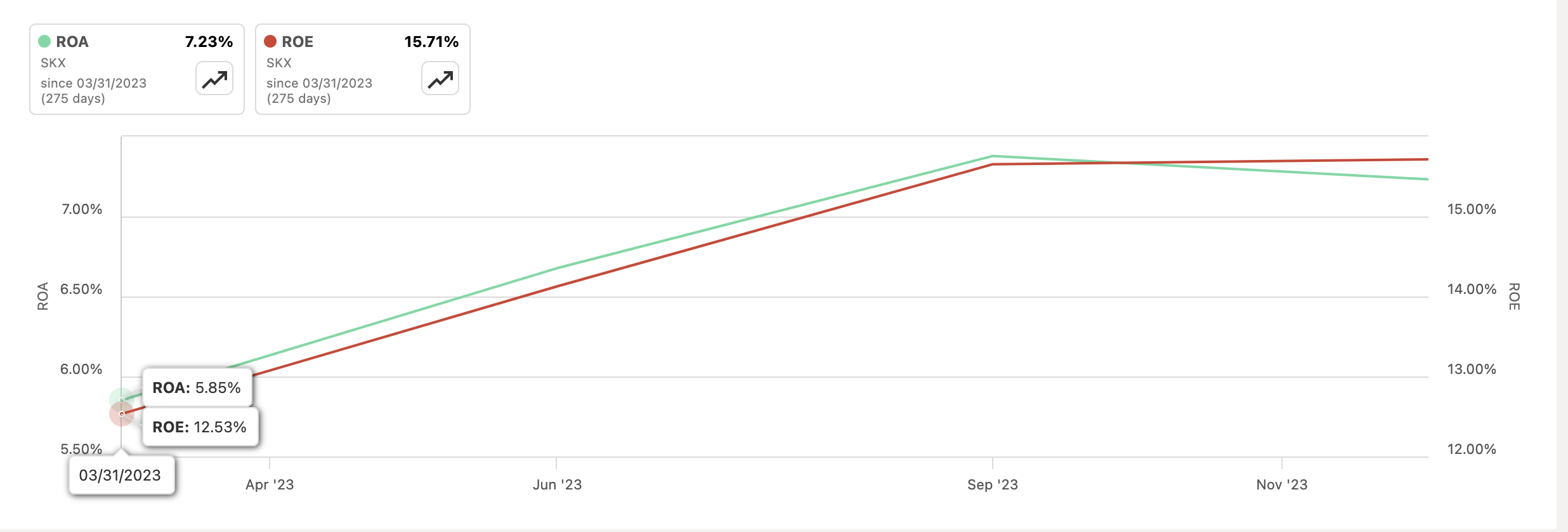

With improvements to the bottom line, come improvements to overall efficiency and profitability metrics like ROA and ROE. These have seen a steady increase over the year just like margins, with a slight plateau in the last two quarters. Does this mean that the company may not be able to improve its efficiency going forward? We need to see a couple of more quarters to come to that conclusion as right now there is not enough evidence to support that.

ROA and ROE (SA)

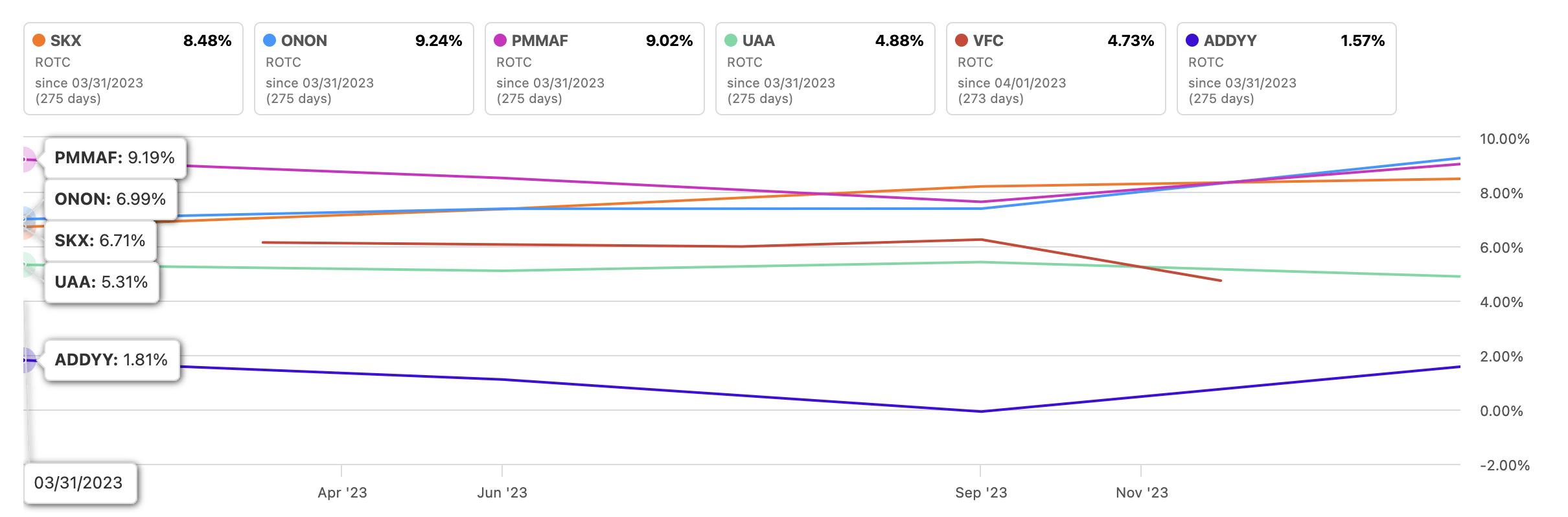

In terms of competitive advantage, the company’s ROTC is up there with the best of them and ranks third out of the small sample I’ve collected that kind of matched SKX’s size.

ROTC vs Peers (SA)

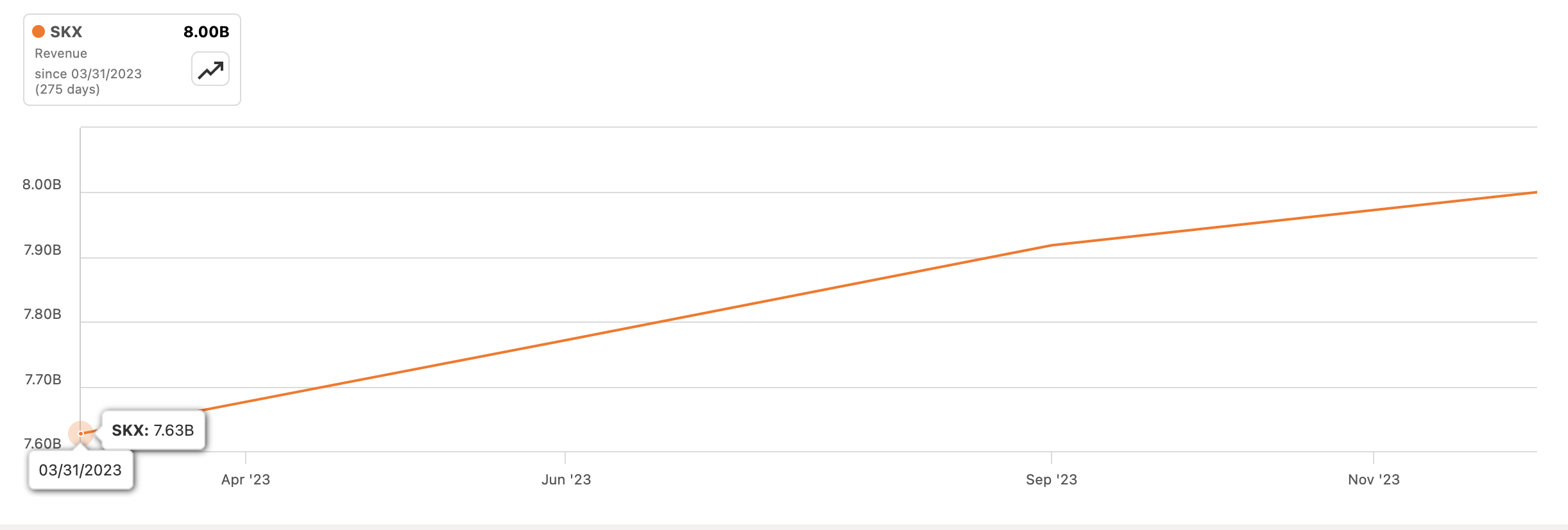

In terms of revenues, it has been on a steady upward trajectory throughout the year, although it is nothing outstanding, steady growth is better than a declining or stagnating one.

Revenue (SA)

Overall, it looks like it was a decent year for the company. It became much more profitable and efficient and on top of that it maintained steady growth in its top line. I would have taken either one of them as positive, but if we can get the two to trend up it’s even better.

What to expect from upcoming earnings

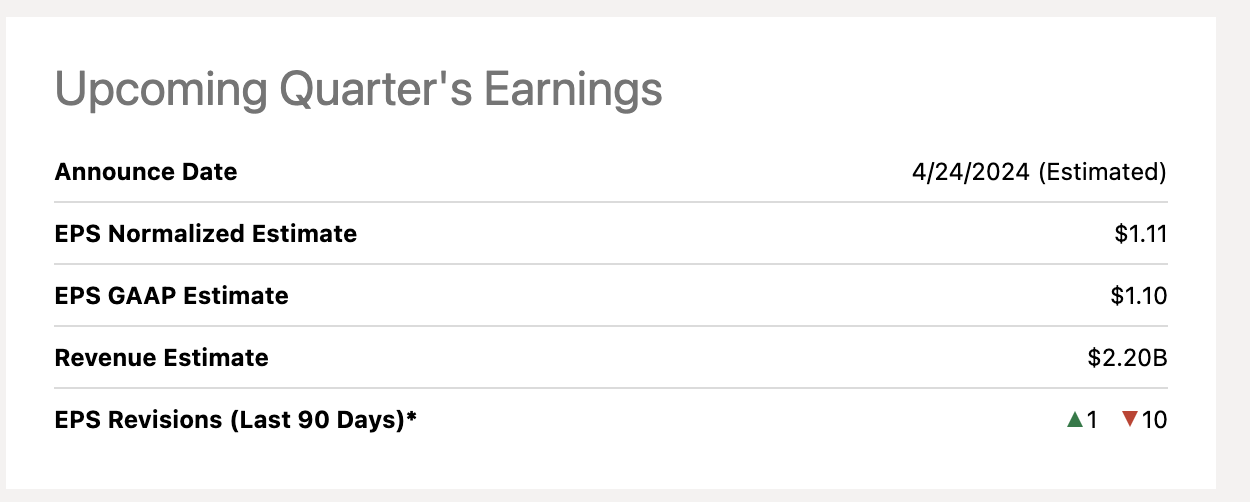

Analysts are estimating the company will do about $1.10, and $1.11 of GAAP and non-GAAP EPS. I do like it when both items are almost identical, and no accounting magic is happening to inflate the company’s value. Analysts are also expecting the company to make around $2.20B in revenue, which is around 12% growth sequentially and around 10% y/y, which is a decent growth still. There have been 10 downward revisions and only 1 upward revision in the last 90 days, so bear that in mind. In the last 2 quarters, the company missed revenue estimates while beating on EPS, so coupled with those downward revisions, we may see another miss.

On the yearly estimates, analysts are expecting the company to make around $8.79B and $3.93 of EPS.

The company expects to make anywhere between $2.175B to $2.225B, which is $2.2B at the midpoint and in line with estimates, and between $1.05 to $1.10 of EPS, which is slightly below analysts’ estimates at the midpoint for the upcoming quarter. For the year, the company expects to make $8.7B at the midpoint of revenues.

Seeking Alpha

Comments on the Outlook

As of writing this update, a couple of major brands reported their numbers, specifically Nike (NKE) and Lululemon (LULU). Nike saw a beat on both numbers but the share price is down after hours by around 6%, which means that many investors didn’t like the slow growth across the board as net income was down 5%. It didn’t look like a very bad report in my opinion so I think it will see a rebound, however, for LULU it’s a different story. The company’s shares are down 10% after hours due to guiding below analysts’ consensus for the year. The report for Q4 itself was decent in my opinion. Gross margins came in much higher than a year ago, with some operating margin improvements and a beat on EPS. But as it always is with these reports, the important thing from them is the guidance, so taking these two as examples of what might happen to SKX, I wouldn’t be surprised if we see a beat on numbers, but we get a weak guidance which will drive down its share price.

I would like to see how its DTC segment is faring so far. The company has said that the segment is finally making up more than 50% of total sales. I would like to see this strength continue and make up even more of the total sales number in the future, as wholesale seems to be on the decline.

DTC and online stores should be the main priority in my opinion as that will continue to drive efficiency and profitability further, and with the continuation of opening new stores, that is exactly what the company is doing. This way I wouldn’t be surprised if we see further margin expansion over the next couple of years.

Is the company going to see similar faith as the aforementioned companies? We’ll just have to wait and see but I think over time, the company will achieve even higher efficiency and profitability.

Valuation

It has been quite a while since I modeled the company last, and a lot has changed since then, so I went ahead and updated my assumptions and other economic indicators since then. For revenues, I decided to go with around 7% CAGR over the next decade, which is half its 10-year average of 14.4% and around 6% lower than its 3-year average. This way I am getting more margin for error, which will act as a higher margin of safety. Furthermore, I am also modeling a more optimistic case, and a more conservative one, to give myself a range of possible outcomes. Below are those estimates, with their respective CAGRs.

Revenue Assumptions (Author)

For margins and EPS, I decided to go slightly lower than what the analysts are estimating, to give myself even more room for error. I think it is always better to be more pessimistic about the company’s prospects than too positive. That way if the company is still cheap with such conservative estimates, you know you’re getting a good deal and will sleep well at night knowing that you didn’t overpay for a company. Below are those estimates.

Margins and EPS Assumptions (Author)

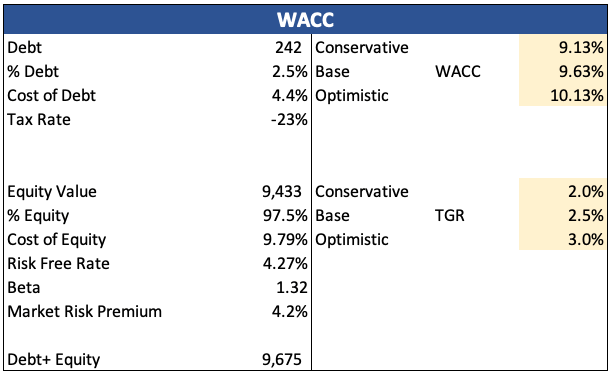

For the DCF valuation, I went with the company’s WACC of around 9.6% as my discount rate, as it is close to what I usually use, which is 10%. I am also using a 2.5% terminal growth rate for my base case. You can see my inputs for the WACC calculation below.

WACC Calculation (Author)

Additionally, to give myself even more room for error, I am adding a 20% discount to the final intrinsic value calculation, just to make sure I beat the share price down and get as much of a cushion as I can. With that said, the company’s intrinsic value is around $65 a share, which means it is trading at a slight discount to its fair value.

Intrinsic Value (Author)

Closing Comments

So, why am I recommending holding off for now? It is a little short-sighted of me but if you are already not invested in the company, I would wait for the next report, as I believe we may see some soft guidance from them in the short run, which may present an even better entry point.

My long-term thesis is still intact as I believe the company will be much more profitable in a few years than now, but since the earnings are coming up, I wouldn’t be in a hurry to enter now. If you already have a position, it would be wise to wait for the next report also and add on any substantial weakness in the short run.

I think the management is doing the right thing by prioritizing DTC, which will turn to higher profitability and the steady growth that we have seen in the past will remain.

Q2 2024 Earnings Call Transcript")