PM Images

Overview

While my portfolio is already heavy-weighted with BDCs (business development companies), I continue to get pulled in by the appeal of these high yielding opportunities. TSLX has a solid performance history and juicy high yield of 8.6%. Sixth Street Specialty Lending (NYSE:TSLX) operates as a business development company, offering a diverse range of financial services. The firm specializes in providing various types of loans, including senior secured loans such as first-lien and second-lien, along with unsecured loans, and investments in corporate bonds and equity securities.

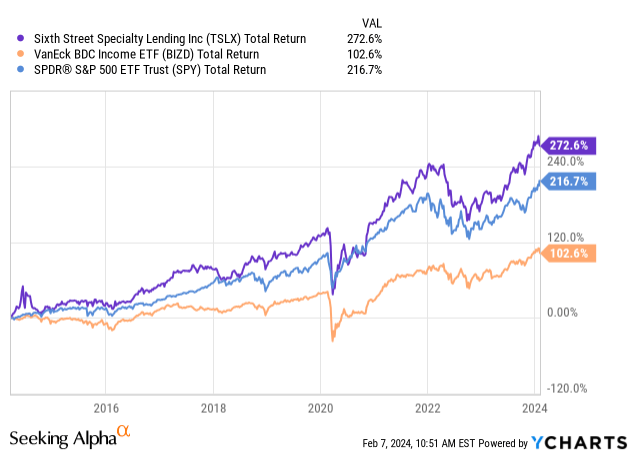

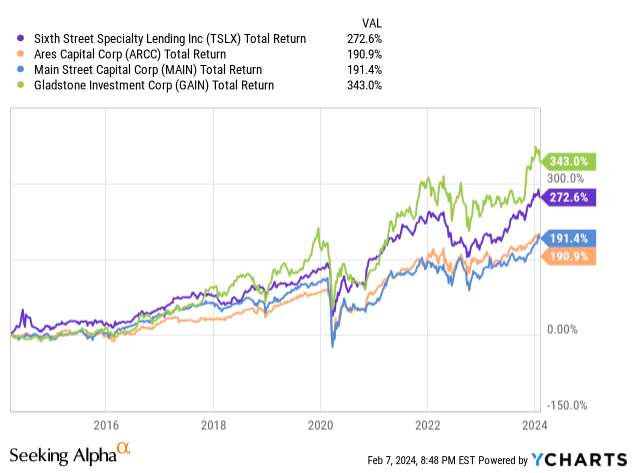

Comparing the performance against the VanEck BDC Income ETF (BIZD), we can see TSLX outperforms in total return. Amazingly, TSLX also outperforms the S&P 500 (SPY) in total return over the last ten-year period. I think this outperformance not only shows the quality in strategy and management of this BDC, but I also think there is a possibility of continued outperformance due to the higher interest rate environment going forward.

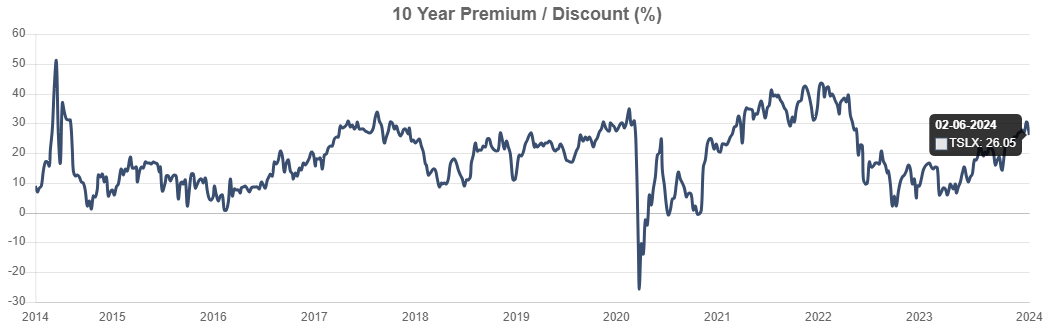

The price of TSLX is currently trading at a premium to NAV by 26%. While I’d ideally like to initiate a position while shares are trading at a discount to NAV, it’s unlikely that we will ever get that opportunity. Shares have only briefly traded at a discount to NAV one time over the last 3-year period. While I have complete faith in management’s ability to continue growing the distribution while simultaneously providing supplementals, I would prefer to nail a much better entry.

Strategy

The company targets investments across multiple sectors including business services, software & technology, healthcare, energy, consumer & retail, and more. Its primary focus is on financing and lending to middle-market companies primarily operating in the United States. These companies typically have market caps ranging from $50 million to over $1 billion, and EBITDA between $10 million and $250 million.

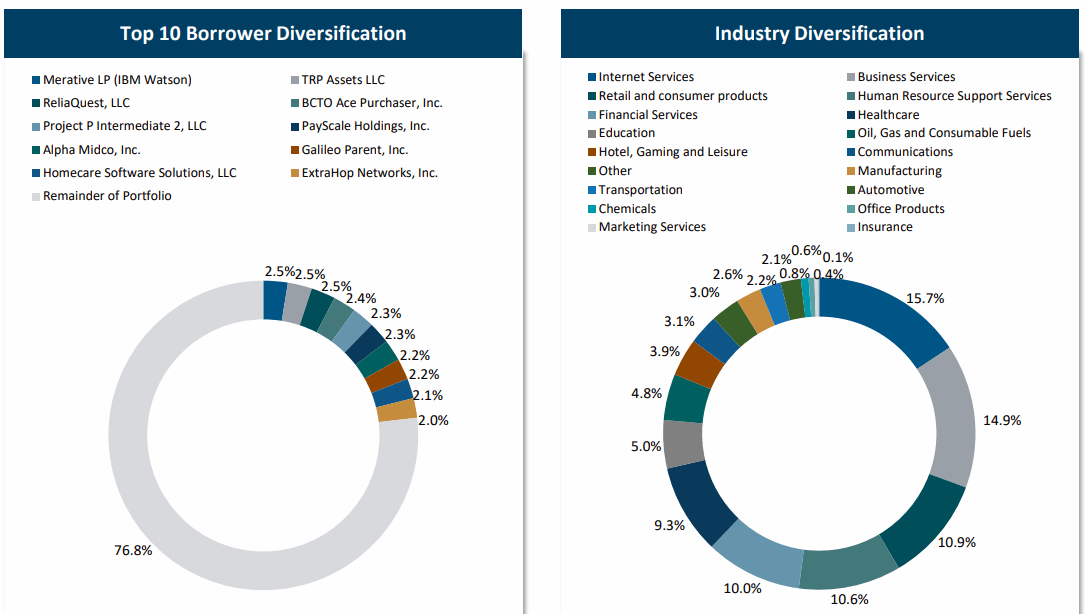

TSLX’s portfolio is diversified in sector with most industries accounting for less than 10% of the total. The leading portfolio makeup is comprised of Internet Services at 15.7%, Business Services at 14.9%, and Retail & Consumer products at 10.9%. Notably, none of the top borrowers account for more than 2.5% of the total value.

TSLX Investor Presentation

Approximately 91% of the loans in their portfolio are floating-rate, which means their interest rates adjust periodically based on market rates. This structure offers protection against interest rate fluctuations. Not only does it offer protection from changing rates, but it also means that TSLX is able to benefit from the higher interest rate environment that we are experiencing. These investments are predominantly structured as first-lien positions, providing a seniority advantage in the event of borrower default.

Next, approximately 82% of the debt investments in the portfolio come with call protection. Call protection is in place as a safeguard that works by restricting the issuer’s ability to redeem or call back the debt securities before a specified date or at least a certain premium. The entire strategy being utilized, not only offers the potential for attractive returns, but also serves as a defensive mechanism against rate changes and early redemption of investments.

Lastly, TSLX borrowed $300M through unsecured notes that will be due in August of 2028. These notes carry an annual interest rate of 6.95%. The money from these notes was used to pay off existing debts under the Revolving Credit Facility.

Well-Covered Dividend

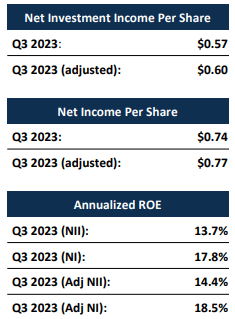

As of the latest earnings report, the NII (net investment income) per share of $0.57 comfortably covered the dividend of $0.46/share. The amount of money earned per share from investments and income includes about $0.03 per share for expenses related to capital gains incentive fees. Excluding these fees, the company’s adjusted net investment income was $52.3 million, or $0.60 per share.

The company’s strong performance in net investment income in the third quarter shows that its portfolio continues to earn well. This income was boosted by higher interest rates, which led to better returns on the investments. As rates are expected to be higher on average, it’s likely these we continue to see increased levels of profitability and even some supplemental distributions.

TSLX Q3 Press Release

The current dividend yield of 8.6% sits slightly above the 5-year dividend average of 8.05%. The last dividend raise that was announced was in February of 2023 and was a slight 2% bump. Now that it’s almost been a full year, I anticipate a dividend raise to be announced again sometime soon. The dividend has an average growth rate of 3.36% over the last 5-year period but this is great considering the yield is already above 8%.

Valuation

CEF Data

TSLX’s price has consistently traded at a high premium to NAV over the last few years. The highest premium the price point reached was a whopping 44% while the lowest discount to NAV was only -0.86%. The average premium over the last 3-year period is 23.84%. The current premium is slightly over this average at 26.05% which means TSLX is traded at about a fair valuation.

The consistent premium may indicate confidence in management and the portfolio’s history of consistent returns. I would personally prefer to get in at a lower premium level since rates are expected to be cut several times this year. Though TSLX is likely to remain profitable, I do think we’ll see the price retract a bit when the first set of cuts finally do take place. During the last Fed meeting, rates were left unchanged despite original projections of a cut happening in the first quarter of the year.

As a point of reference, some other high quality BDCs have consistently traded at a premium to NAV. While each of these peers have different portfolio strategies, I think it would be helpful to reference the average 3-year premium here versus some of the other top quality BDCs.

- Ares Capital (ARCC): Average Premium of 5.93%

- Gladstone Investment (GAIN): Average Premium of 8.52%

- Main Street Capital (MAIN): Average Premium of 59.34%

Risk

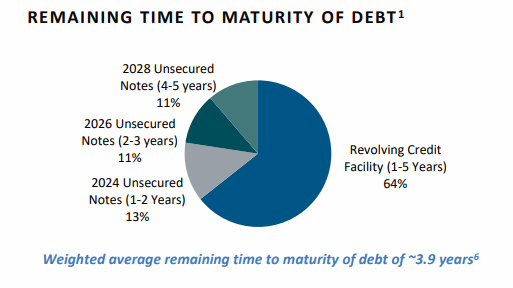

The largest percentage of the portfolio of debt is comprised of revolving credit at 64% and 2024 unsecured notes at 13%. Revolving credit provides borrowers with access to a predetermined amount of funds and offers flexibility in terms of borrowing and repayment. Borrowers can draw funds up to a specified limit and repay any portion of the borrowed amount, typically on a monthly basis. The unused portion of the credit line remains available for future borrowing, hence the name revolving.

TSLX Q3 Investor Presentation

Unlike term loans with fixed maturity dates, revolving credit facilities can be called in by lenders. This could lead to disruptions in liquidity and financing, affecting TSLX’s ability to fund its operations or make additional investments. This would impact NII and overall profitability and can have an effect on the growth of the dividend.

Takeaway

Sixth Street Specialty Lending stands out with its solid performance history and an enticing high yield of 8.6%. TSLX operates as a BDC, providing diverse financial services, specializing in various types of loans and investments. Its performance surpasses that of comparable indices like the VanEck BDC Income ETF and even outperforms the S&P 500 over the last decade.

However, TSLX’s premium trading price to NAV poses a challenge for new investors seeking entry. The majority of TSLX’s debt portfolio consists of revolving credit facilities, which exposes the company to risks such as disruptions in liquidity and financing due to potential lender calls. Despite these risks, TSLX’s well-covered dividend and diversified portfolio, coupled with its ability to navigate the current interest rate environment, makes it a good choice for investors looking to increase their dividend income.

Q2 2024 Earnings Call Transcript")