RHJ

Overview

My recommendation for The Simply Good Foods Company (NASDAQ:SMPL) stock is a buy rating. SMPL products are well positioned to take advantage of several industry tailwinds, such as food away from home consumption, growing snack consumption, and growing health awareness. Layering on top of these trends are SMPL turnaround efforts for the Atkins brands and Quest’s growing awareness marketing campaign. All these should drive top-line growth, which is positive for margin expansion as SMPL sees fixed-cost leverage from its G&A expenses.

Business

SMPL is a packaged food company focused primarily on nutritious snacking. Its two primary brands are Quest and Atkins, and the business mainly sells to the North American consumer base (97% of revenue from North America). Atkins was the first brand that the company started selling (a SPAC acquired Atkins brands in 2017), and Quest came into the picture later on in 2019. The Atkins brand sells protein-rich nutrition with a low-carb and low-sugar profile for people seeking to manage weight, while Quest sells protein-rich foods with limited carbs and sugar, mainly for athletes. Collectively, the main driver of growth has been volume over the past few years (average 11% between FY18 and FY22) until FY23, where volume turned negative and price/mix became the main growth driver. Since 2017, SMPL has grown revenue from ~$400 million to $1.2 billion over the trailing 12 months [TTM], and this is done by improving EBIT margin from 15.4% in FY17 to ~17% in TTM. After the Quest acquisition, which pushed SMPL’s balance sheet to a leverage of >5x net debt to EBITDA, SMPL has done a great job of deleveraging the balance sheet, exiting 1Q24 with a net debt position of ~$190 million, or less than 1x net debt to EBITDA.

Growth supported by industry tailwinds

SMPL is well-positioned to benefit from several industry tailwinds, such as food away from home consumption, growing health awareness, and snacking.

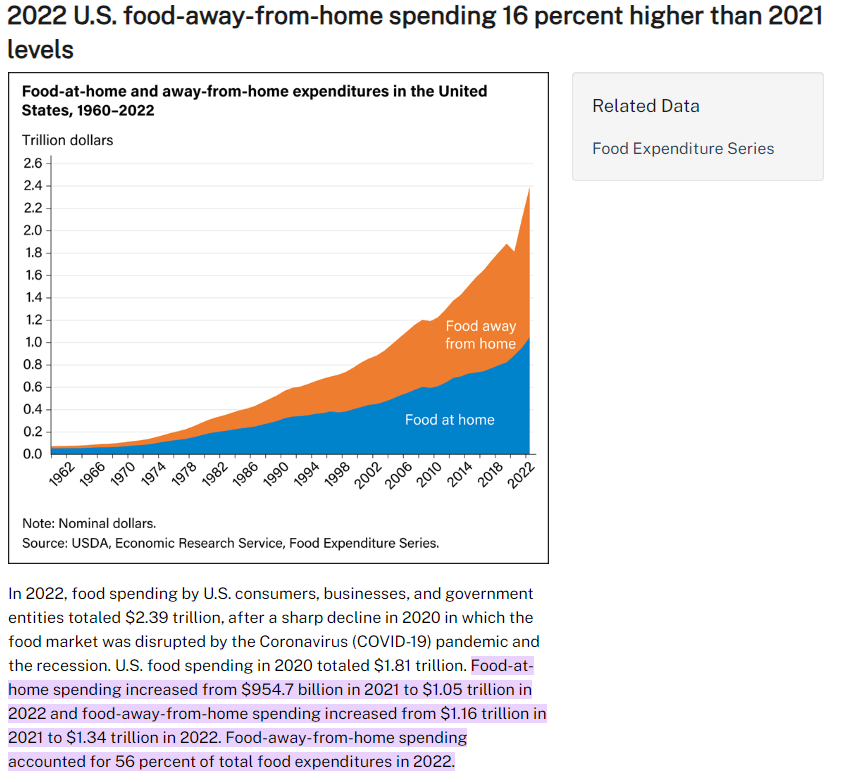

USDA

In the US, food away from home has grown significantly over the years, with a big surge in recent years now accounting for over 50% of total food expenditure. From a growth perspective, historical growth has been around the mid-single-digit percentage range. Layering on top of this trend is the growing consumption of snacks, which is expected to grow faster than overall food spending. Just by looking at these two drivers, SMPL products fit the bill exactly. SMPL products are filling, convenient to consume, and easy to travel with their small size. The last industry tailwind is consumers growing attention to health. This is in favor of SMPL as well because its products are protein-rich foods with limited carbs and sugar, making them an ideal choice for snacking. Furthermore, I also believe that SMPL’s product offering can benefit from the changing behavior among people on these drugs, including a shift to smaller portions, a focus on weight management, and a mix shift in people’s diets towards more protein and away from high-fat and high-sugar foods. Management has also specifically called out their intention to capitalize on this opportunity. They have conducted research over the last several months to understand how people on the drugs are eating and are planning on rolling out targeted communications, brand messages, and offers to potential customers on GLP-1 medications or interested in starting. My take is that most GLP-1 users will eventually stop taking the medication because of the high cost and reduced effectiveness after reaching a certain body weight, and SMPL is well-positioned to take advantage of this trend as I see it as the perfect companion for consumers in weight management (after they stop taking GLP-1).

The GLP-1 drugs are a significant tailwind for both businesses. And over the past three months, we conducted a lot of proprietary research with consumers on the drugs to understand the impact they were having. from: 4Q2023 earnings call

Asset light model allows for more marketing spend

All of SMPL’s products are made by contract manufacturers and then sent to a single third-party distribution center. Ingredients, packaging, and production scheduling are all handled by the contract manufacturers, while SMPL pays them for the finished goods using a tolling charge that is agreed upon and based on the quantity of items produced. While the downside is that SMPL does not have end-to-end control over production (e.g., it might face insufficient capacity during a demand surge), I think this strategy has enough positives to justify adopting it. For one, this model limits the company’s capex and manufacturing overhead, which means SMPL has a lot of spare capacity (cash) to invest in other growth initiatives, mainly marketing. In a typical manufacturing business, I’d say that end-to-end governance of the manufacturing and production processes is extremely important. However, for SMPL, which is a consumer-facing product, marketing and branding are a lot more important because it is tough to differentiate itself against peers (more products are similar to each other). As such, how SMPL positions each product and communicates the right branding message to consumers is the key to winning market share. In order to facilitate this, a lot of marketing spending is required. To put things into perspective, SMPL spent ~11% of its revenue on marketing, which is almost the entire OPEX of Bellring Brands (OPEX is 13% of revenue), but both companies have similar EBITDA margins of 20%. This also suggests that room for margin expansion is huge, as SMPL G&A accounts for 9% of revenue, which is too high when compared to BRBR. As it scales, G&A as a percentage of revenue should taper, given that they are largely fixed costs (it has been coming down from 11% to 9% in FY23).

Atkins brand turnaround on track while Quest builds awareness

One of the issues that has plagued SMPL performance recently is the turnaround in the Atkins brand. Encouragingly, the progress is well on track, despite Atkins retail takeaway continuing to fall in 1Q24. I think the market has already anticipated this, given that the turnaround action plan is still in its early stages. The focus should be on the steps management has taken to drive a turnaround, including recent innovations like Baked Bars and Break Bar and a new ad campaign with plans to lean into advertising merchandising for the New Year, New You season in 2Q24. Again, this supports the positive aspect of SMPL’s asset-light model, as it has a lot of flexibility to invest in marketing without hurting margins.

On the other hand, Quest continues to show positive traction, as retail takeout grew 19% in 1Q24. Quest success in acquiring new customers (19% growth is balanced across the existing customer base and new customers) is a good precedent for Atkins brands turnaround, I believe, as it shows that management is well aware of how to craft the right message to attract the right group of audience members. Quest should continue to see positive growth as management announced a new advertising campaign for Quest beginning in February to build consumer awareness..

Valuation and risk

Author’s valuation model

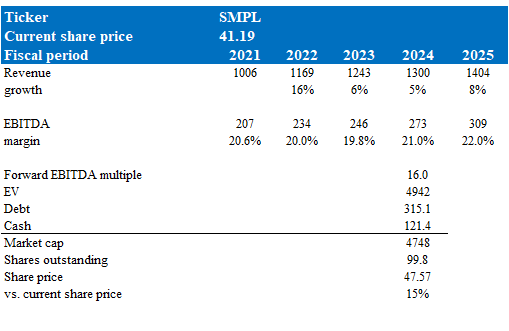

According to my model, SMPL is valued at $47.57 in FY24, representing a 15% increase. This target price is based on my growth forecast of management-guided 5% growth in FY24, followed by an acceleration to high single-digits in FY25, reflecting the US snack industry growth rate. I believe my FY25 growth assumption is conservative, as SMPL should be able to capture share as it turns around the Atkins brand and Quest gains more awareness. As I discussed above, I believe SMPL has plenty of room for margin to expand as it leverages the fixed cost of its G&A expenses. A similar trend can be seen in Bellring Brands, where OPEX as a percentage of sales continued to decline over the years, from 18% in FY18 to 14% in FY23. As SMPL growth recovers to high single-digits and margins expand, I think the market will naturally value this company on a normalized basis—its historical average multiple. SMPL historically trades at 16x forward EBITDA, and it should trade at that level.

The investment risk is that SMPL might not be able to turn around the Atkins brand as well as I expected, either due to bad messaging or a bad product. While I did mention that SMPL success in the Quest brand is a good precedent, there are no guarantees that management will not misexecute.

Summary

I recommend a buy rating for SMPL based on the company’s favorable positioning to capitalize on industry tailwinds, including the surge in food away from home consumption, increasing health awareness, and growing snacking trends. Internal efforts to turnaround the Atkins brand and the expanding awareness marketing campaign for Quest are also growth drivers for SMPL. As top line grows, I expect margin expansion through fixed-cost leverage (mainly through G&A expenses). Notably, SMPLY asset-light model allows for increased marketing spend, crucial for consumer-facing differentiation.

Q2 2024 Earnings Call Transcript")