d3sign/Moment via Getty Images

Summary

In our initial report on Simon (NYSE:SPG), we gave it a Hold. Following a generally positive Q4 earnings report, we raised our price target and upgraded it to a bullish Hold. While Simon is now trading at a moderate discount to our NAV estimate, we require a more substantial margin of safety before moving to a Buy. We also reevaluate the Series J preferred stock, and maintain our Sell rating given the ~3.4% YTC, which is lower than the entire US treasury yield curve and most 3-year CDs.

Earnings Update

Simon reported Q4 ’23 earnings on February 4. The results were a mixed bag, but net positive in our view.

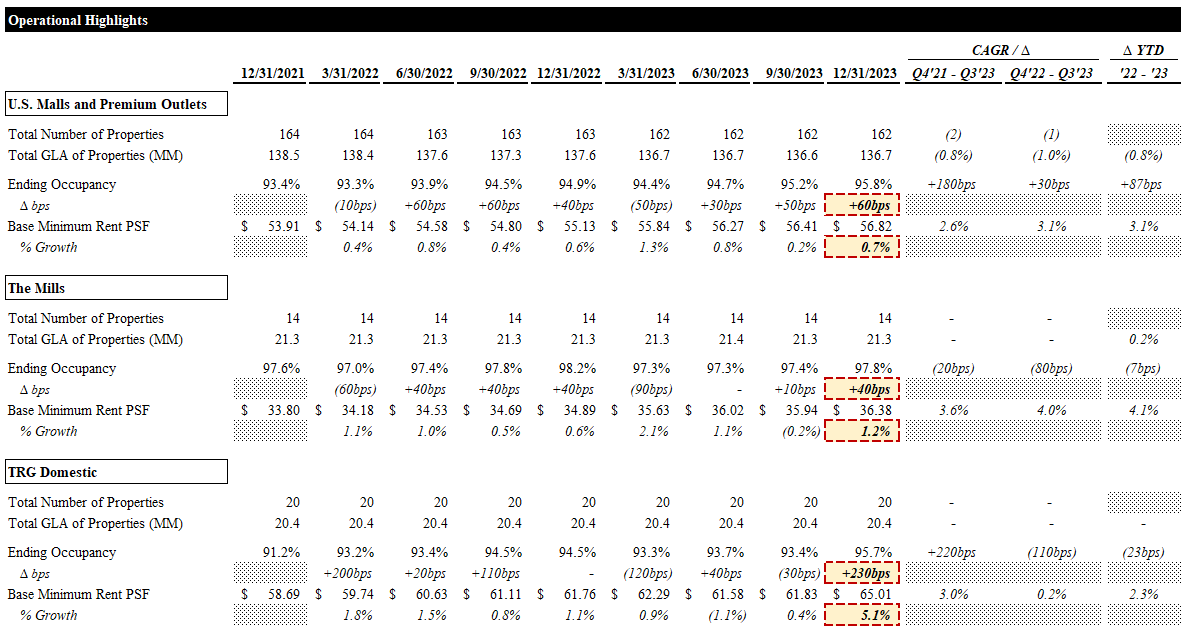

FFO per share beat consensus by ~$0.05, adjusted for the unanticipated ~$0.31 gain from the partial monetization of its stake in ABG (n.b., now ~10% from ~12%). However, ’24 FFO guidance missed consensus by ~2%, seemingly from volatility in non-real estate earnings (n.b., real estate FFO is expected to improve modestly YoY). Positive leasing momentum helped drive occupancy growth across the portfolio (n.b., +60bps in US Malls and Premium Outlets, +40bps at Mills, and +230bps at TRG Domestic). It finished the quarter with ~$11Bn of liquidity, including ~$2.8Bn of cash, which should continue to support opportunistic investments (e.g., mixed-use developments), redevelopments and buybacks (n.b., repurchased ~$140MM in ’23).

Operational Highlights (Empyrean; SPG)

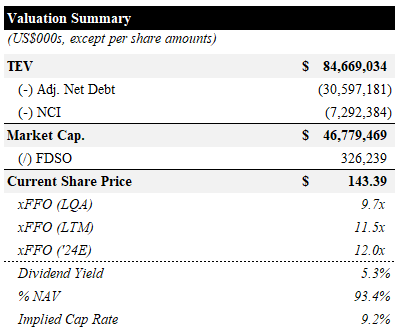

Simon is now trading for ~9.7x LQA FFO and ~11.5x LTM FFO. Its guidance for full year ’24 implies ~12.0x NTM FFO. Its yield remains materially similar to our initial report at ~5.3%. Our NAV estimate, discussed below, improved and now implies a ~7% discount (n.b., ~9% implied cap rate).

Valuation Summary (Empyrean; SPG)

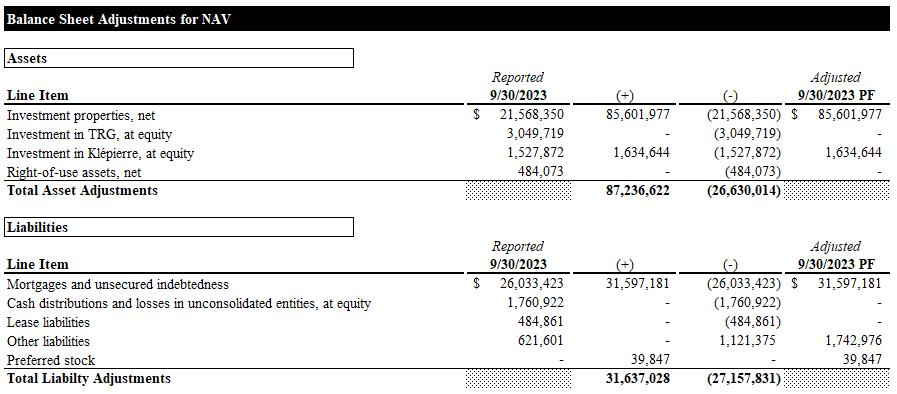

The major balance sheet adjustments for our NAV calculation are outlined below.

Balance Sheet Adjustments (Empyrean; SPG)

Our new NAV-based price target of ~$153/share implies a ~7% upside and an NTM FFO multiple of ~13x.

Target Price (Empyrean; SPG)

With the market still being undersupplied and highly favorable to landlords and the company looking to further monetize its OPIs and repurchase shares, we feel compelled to upgrade our rating. However, the shares still do not look highly dislocated. Given the opacity of Simon’s portfolio, we would prefer a wider margin of safety before giving a Buy rating. We will instead go with a bullish Hold.

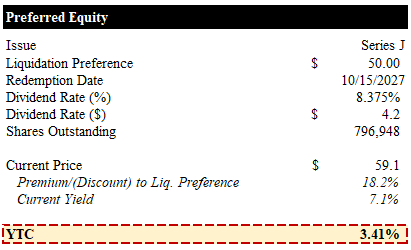

Series J Preferred

Since our initial report, the Series J has sold off a modest ~2% to $59.1/share. It still trades at a substantial ~18% premium to liquidation preference, implying a yield of ~7%.

Series J Pref (Empyrean; SPG)

Despite the modestly lower price, the Series J still appears highly unattractive, with a YTC of ~3.4%. This is lower than the entire US treasury yield curve and most 3-year US CDs (n.b., mid to high-4% range on CDs). From a pure investment perspective, we see this as a poor risk/return profile and maintain our Sell rating. However, there is an argument to be made that the effective YTC on the Series J could be closer to ~4.5%, considering the potential tax benefit of the capital loss due to the amortization of the premium approaching the redemption date (n.b., assuming 40% marginal tax rate). However, this is still not competitive with treasuries and CDs, particularly on a risk-adjusted basis.

Conclusion

Despite a good Q4, we remain largely neutral on Simon’s common and bearish on the Series J preferred on valuation concerns. We would likely become more constructive on the common around $125/share (n.b., ~6.1% yield and ~10.5x NTM FFO) and the Series J below $53/share (n.b., ~7% YTC).

Q2 2024 Earnings Call Transcript")