Thinkhubstudio

ServiceNow (NYSE:NOW) is a great recent example of why it can pay off to pay up for quality. The stock has delivered incredible returns over the past year and now trades at all-time highs. But has the stock run too far? The stock does trade at the higher end of my fair value range, but between the net cash balance sheet and GAAP profitability, the stock has earned a premium valuation. I still see market-beating returns ahead as the company moves into the mold of the next Microsoft (MSFT) or Salesforce (CRM). Perhaps this is no longer a “table pounding” buy as it was one year ago, but I remain bullish on the name.

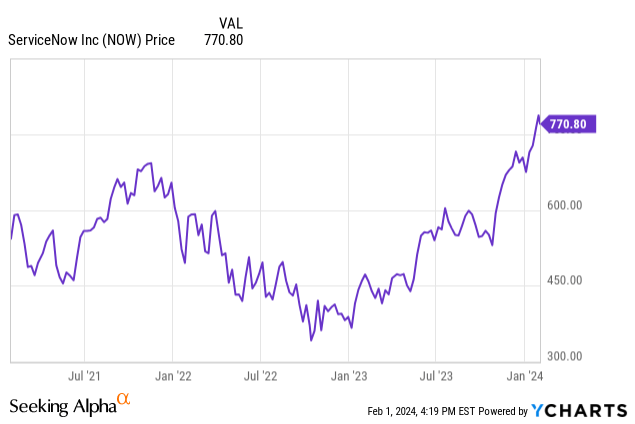

NOW Stock Price

It isn’t just unprofitable tech stocks that are enjoying this rally. NOW has returned nearly 40% since I last covered the name in October.

The stock has clearly benefited from the generative AI boom, but unlike many other generative AI “wannabes,” this is a profitable name with clear generative AI applications.

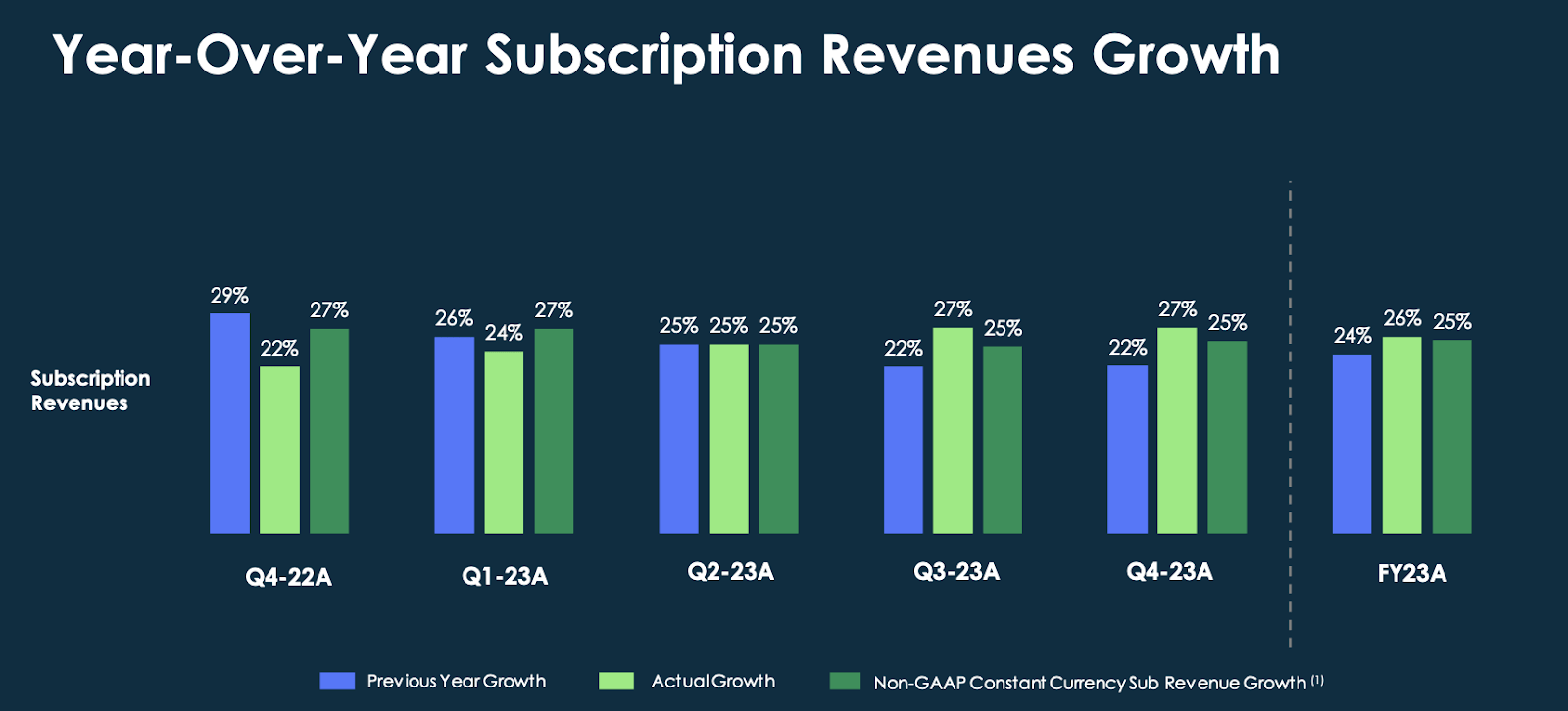

NOW Stock Key Metrics

In its most recent quarter, NOW delivered 27% YoY revenue growth, comfortably beating guidance by 200 bps. In the current environment, a 200 bps top-line beat is unheard of, let alone for a company of this size.

2023 Q4 Presentation

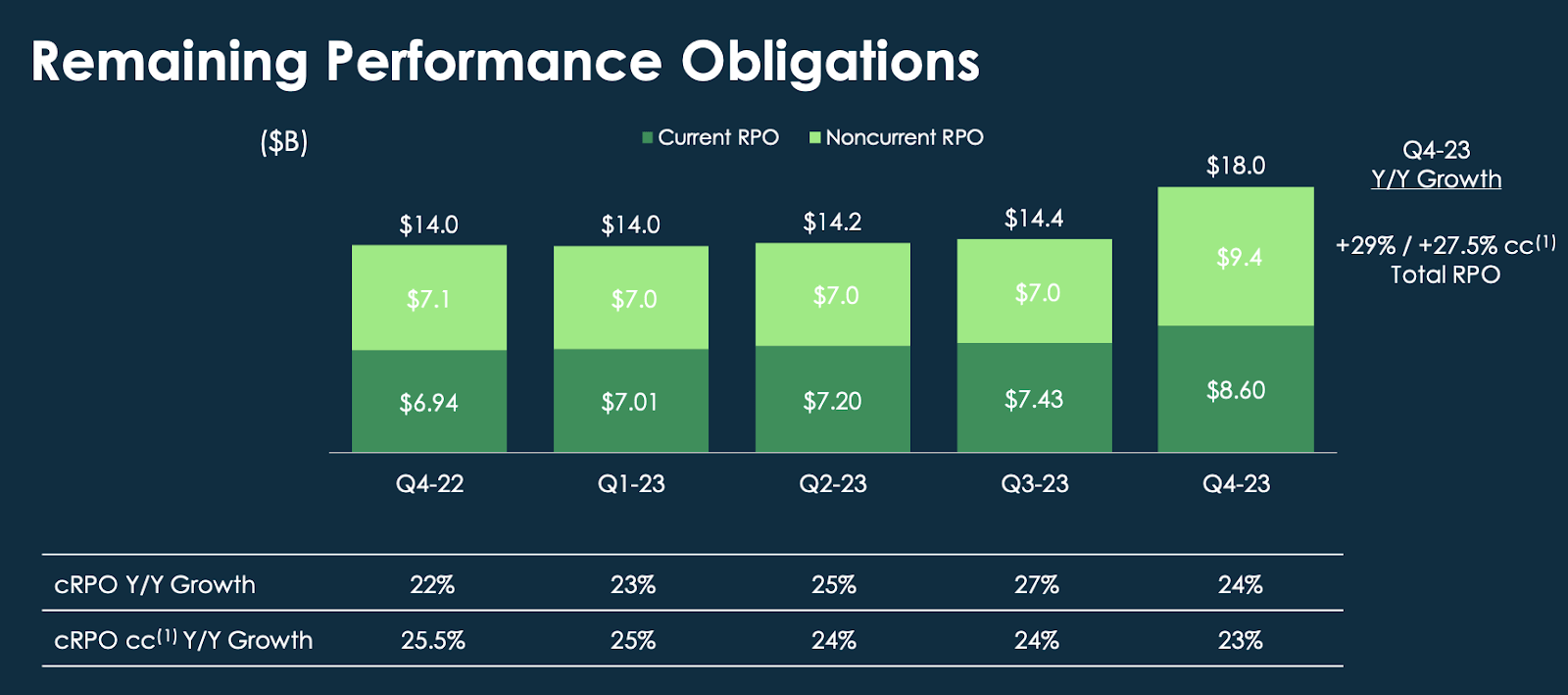

NOW paired that strong revenue growth with 27.5% growth (constant currency) in remaining performance obligations (‘RPOs’) and 23% growth in cRPO. I view cRPO as the best leading indicator of forward revenue growth – NOW appears poised to sustain its 20+% revenue growth rates over the near term.

2023 Q4 Presentation

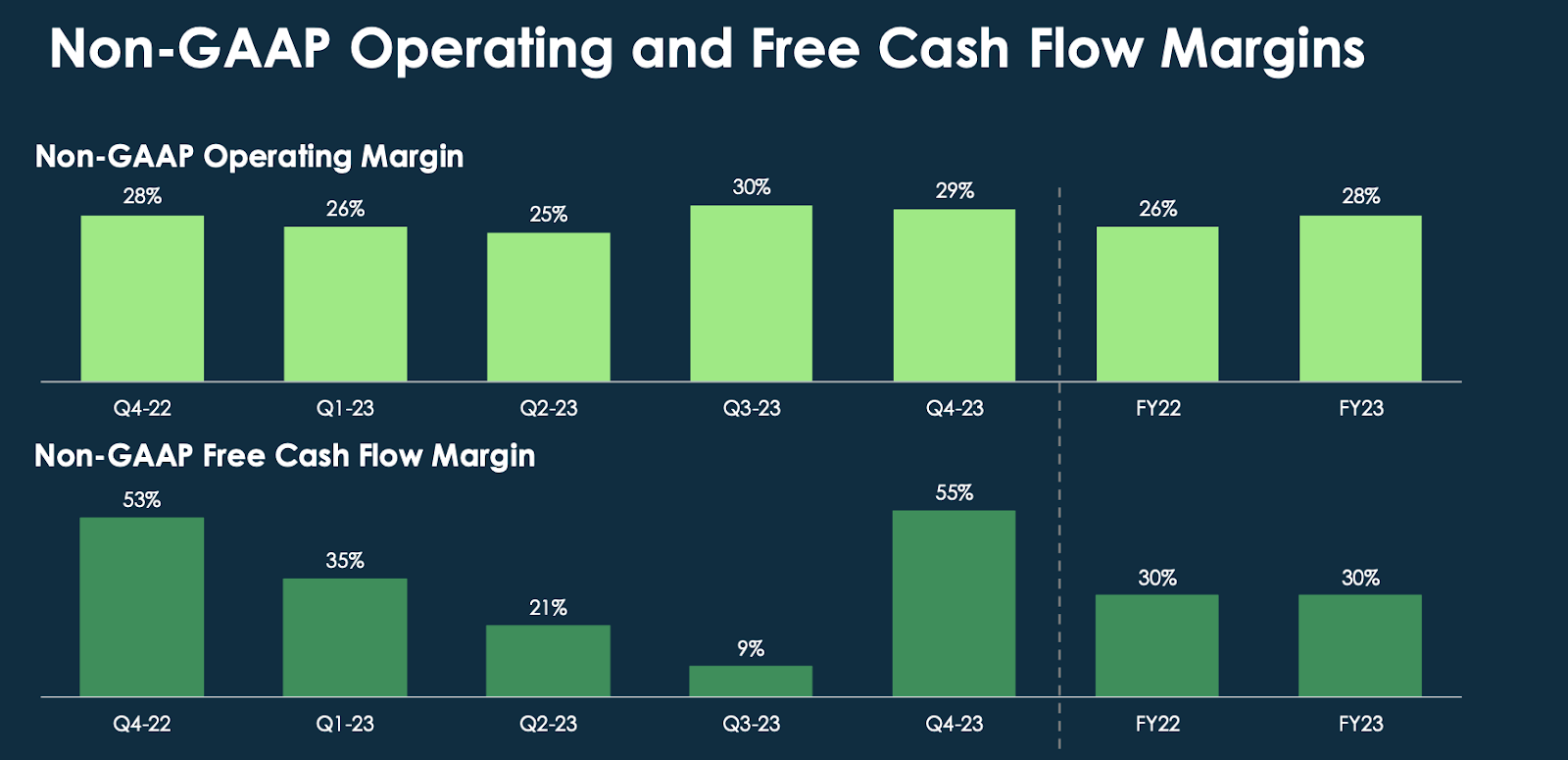

On the profitability front, NOW remained profitable on a GAAP basis and delivered 150 bps of non-GAAP operating margin expansion.

2023 Q4 Presentation

NOW ended the quarter with $8.1 billion of cash versus $1.5 billion of debt. The company repurchased 400,000 shares in the quarter in an effort to manage dilution. One could make an argument that share repurchases might not be the best use of capital given NOW’s relative premium to peers, but share repurchases are also a critical lever in gaining a premium valuation.

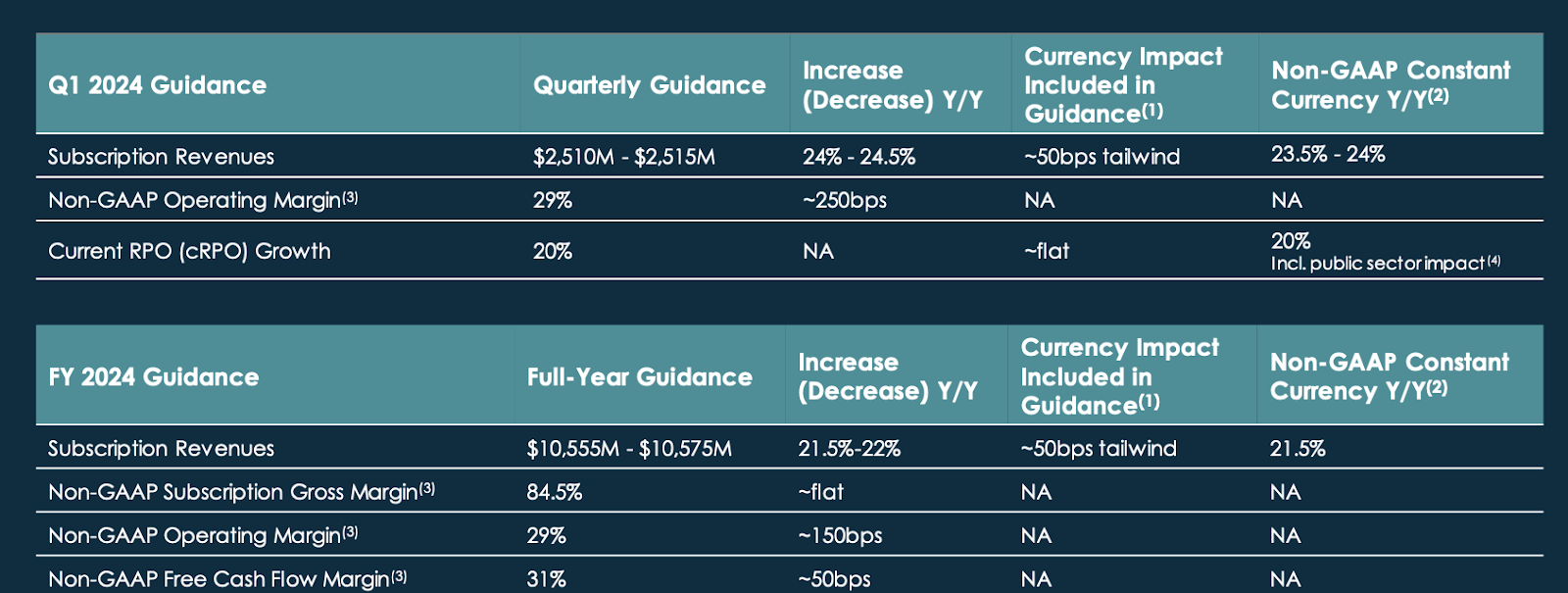

Looking ahead, management has guided for the first quarter to see up to 24% YoY growth in subscription revenues (constant currency) and for the year to see up to 21.5% growth.

2023 Q4 Presentation

On the conference call, management noted that the 20% guide for cRPO growth includes around 150 bps of negative impact from the “tremendous strength of our federal business.” While management did not explicitly state as much, the implication may be that “normalized” cRPO growth may hover around 21.5%.

Management credited some of their strong performance as coming from generative AI, noting that around “half” of their outperformance may be generative AI related. Management noted that they personally have experienced the generative AI impact, with their software helping them to realize that they should not invest so much time and resources on contracts less than $250,000 in size. It is impressive to see not only how quickly NOW has integrated generative AI into its products, but also the real tangible impact. Management reiterated their confidence in their 2026 revenue guide of at least $15 billion, but did note that they will be “definitely increasing hiring as we go into 2024.” Generative AI may hold back profit margin growth in the near term due to the increased investment, but it may help power greater revenue growth over the long term.

Is NOW Stock A Buy, Sell, or Hold?

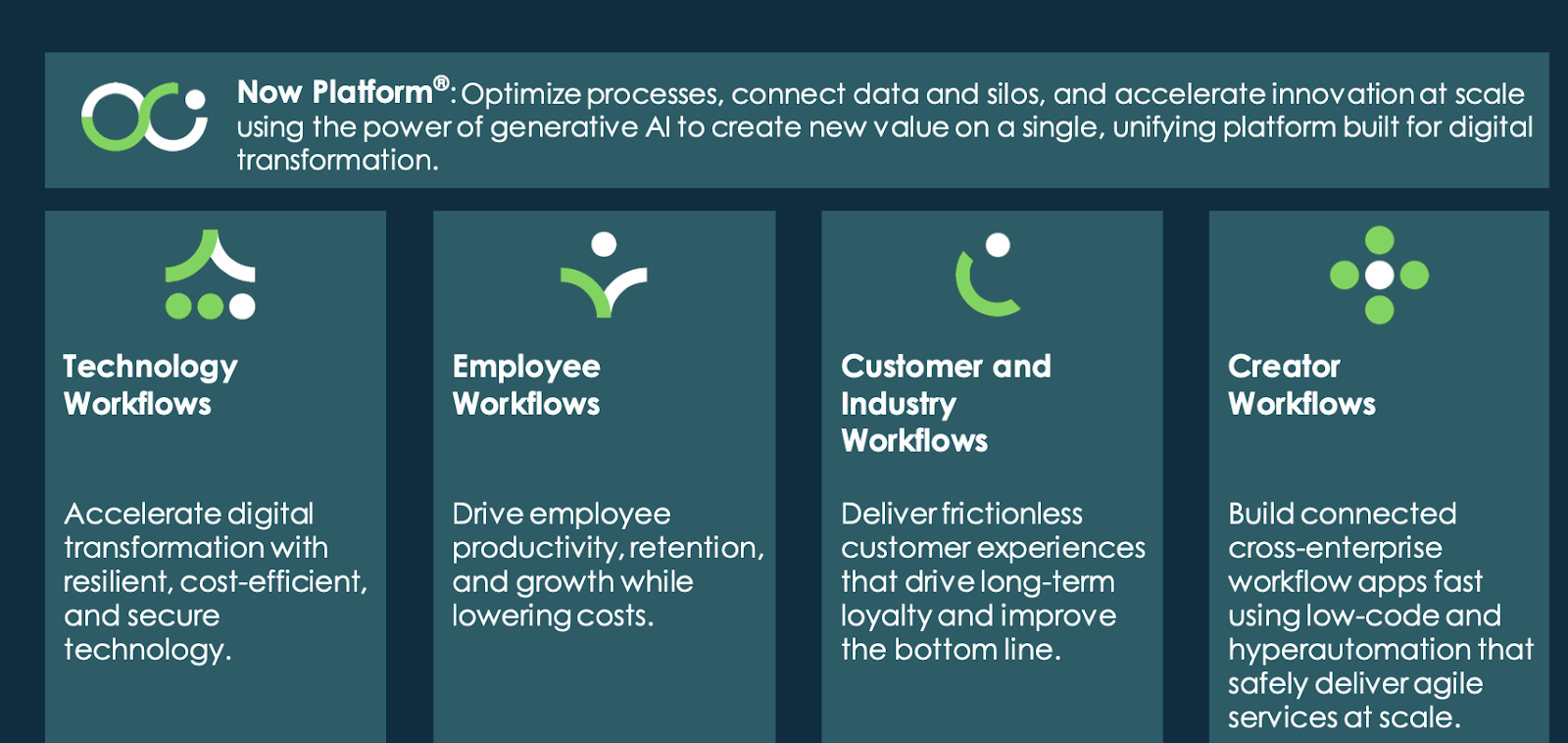

NOW is an enterprise tech company that enables digital workflows. This can range from helping employees complete onboarding tasks as well as helping customers (customers of customers, that is) troubleshoot issues on their own.

2023 Q4 Presentation

This kind of software is integral to day-to-day operations and helps to explain the stickiness of the product – NOW boasts 99% renewal rates. With minimal churn and high pricing power, NOW was able to cruise through the past year with flying colors, even as many tech peers struggled in the tough macro environment. The strong fundamental performance has earned NOW a premium valuation, with the stock trading at 60x forward earnings.

Seeking Alpha

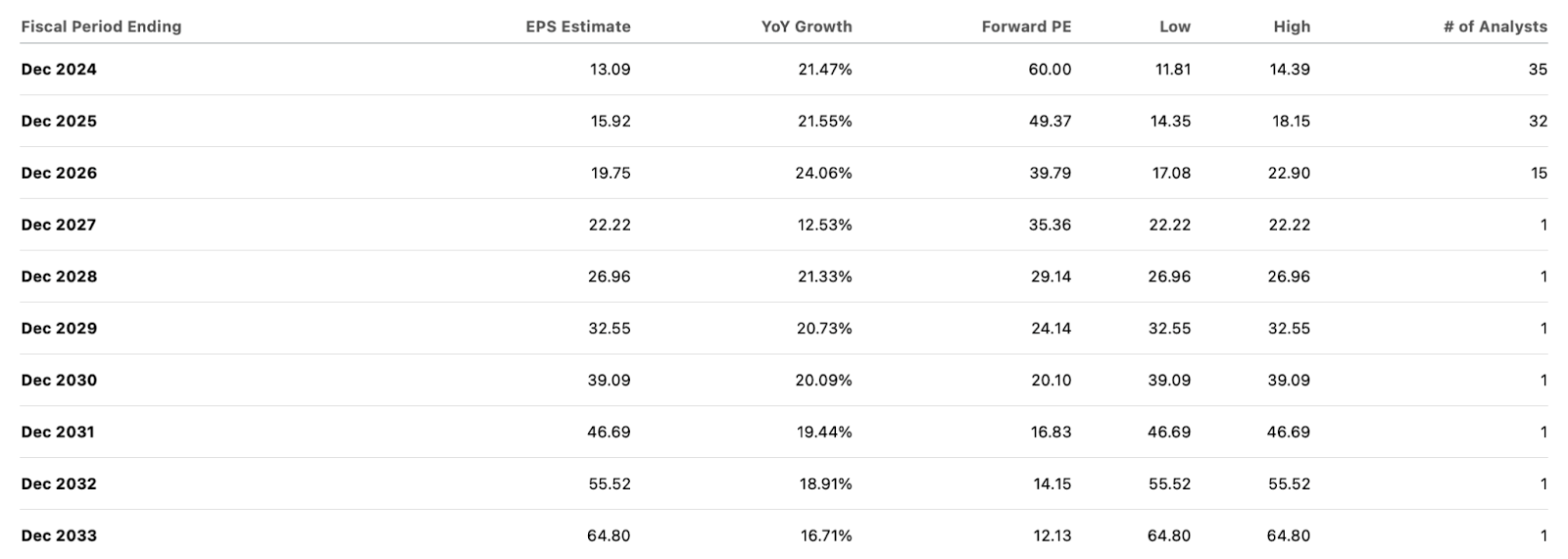

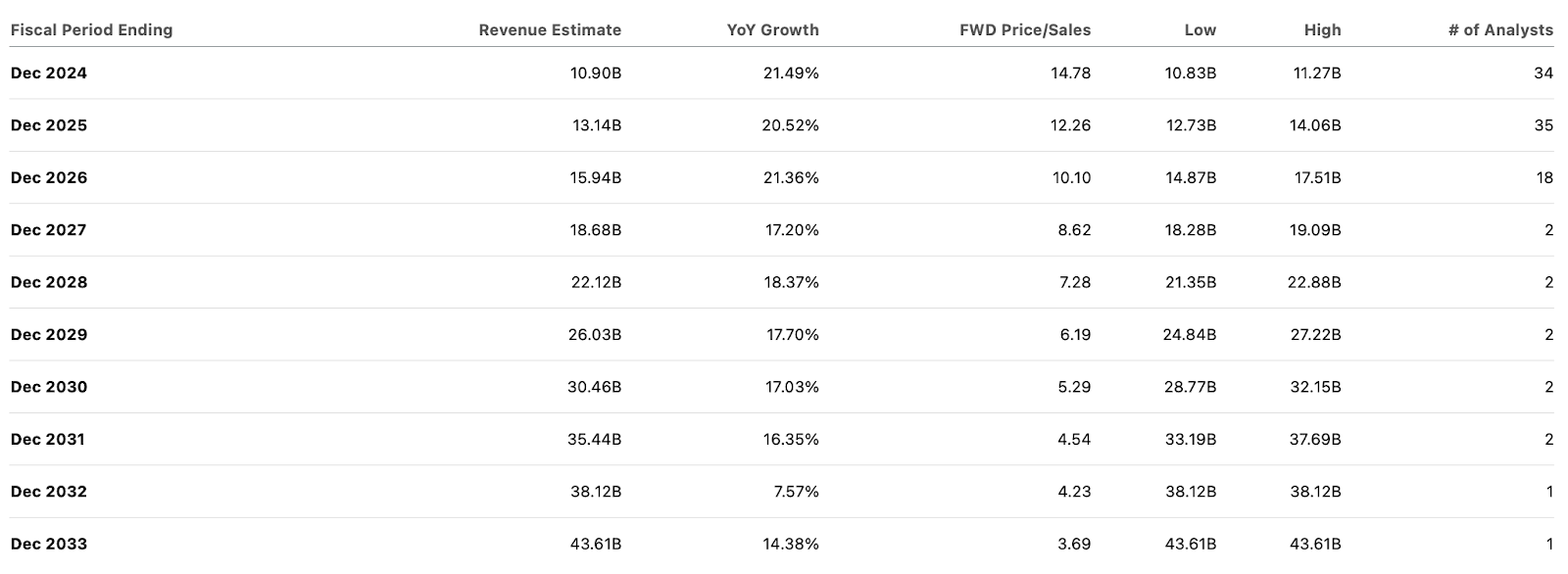

Consensus estimates have the company falling just short of guidance for $16 billion in revenues by 2026 but sustaining healthy double-digit growth over the next decade.

Seeking Alpha

I continue to expect NOW to generate around 40% net margins over the long term. I again use a long term earnings multiple of around 30x, or a price to sales multiple of around 12x. Assuming that NOW can meet consensus estimates until at least 2030, that would imply a stock price of $1737 in 2030, or 12.4% compounded annual returns over the next 8 years (roughly 13.5% inclusive of the earnings yield).

I have been downgrading many tech stocks over the past month due to valuation and lower projected return potential. But in the case of NOW, the company has arguably earned a premium valuation and the associated lower forward return profile. I justify that based on the sticky business model, GAAP profitability, net cash balance sheets, and ongoing share repurchase program.

What are the key risks? While competition is always a looming risk in the tech sector, the company is not showing signs of competitive pressures. Instead, the main risk is likely that of valuation. I see upside ahead for NOW based on it maintaining its premium valuation, and that valuation is tied to the multiples of names like MSFT and CRM. However, if MSFT were to see multiple compression or NOW were to lose its status as a top tier tech stock, then NOW may experience great volatility.

I estimate that NOW is trading at around a 30% premium to peers of a similar growth cohort. NOW will need to execute against its 2026 guidance as well as justify its premium valuation through other means. It isn’t always clear what that may entail, as investor sentiment can be finicky. In my view, buying back stock and maintaining a strong balance sheet are the most obvious courses of action here, given that the business model is already of high quality. But these actions might not always be enough to compensate for slower top-line growth.

I reiterate my buy rating for the stock but caution that the stock trades at the high end of its fair value range, and it is difficult to justify multiple expansion from here.

Q2 2024 Earnings Call Transcript")