da-kuk

I published an article on SentinelOne, Inc. (NYSE:S) about 9 months ago. To summarize my thoughts at the time, I think the company was obviously very promising but I was worried that profitability was looking increasingly far off. On the contrary, management was actually targeting at the time to reach profitability on a cash flow basis already by the end of FY2024. With the fiscal year now behind us, this seemed like the right moment to have a look at the stock again considering that at the time I found it very hard to believe that management could pull it off, considering how far they were from reaching profitability from any point of view.

Although the target was indeed missed somewhat as expected, it turned out that those were not hollow words: SentinelOne has quite obviously veered towards profitability by dramatically decreasing the operating expenses’ growth rate compared with the top line growth. Reducing sales and marketing expenses has quite clearly taken a toll on revenue growth, however I would argue that a business growing at 30-ish percent while being cash flow positive is much more attractive than one growing twice as fast but bleeding cash left and right.

As a matter of fact SentinelOne is not cash flow positive yet, but is clearly working towards it and I will not be surprised at all to see already from this year (FY2025) the first quarter of positive free cash flow. Considering that the company is still growing above 30%, has a mountain of cash and zero debt, is signing new customers at very healthy rate, I must say that an investment in SentinelOne appears to me much more palatable now than simply 9 months ago, despite the stock having appreciated about 67% since my previous article.

The new path towards profitability

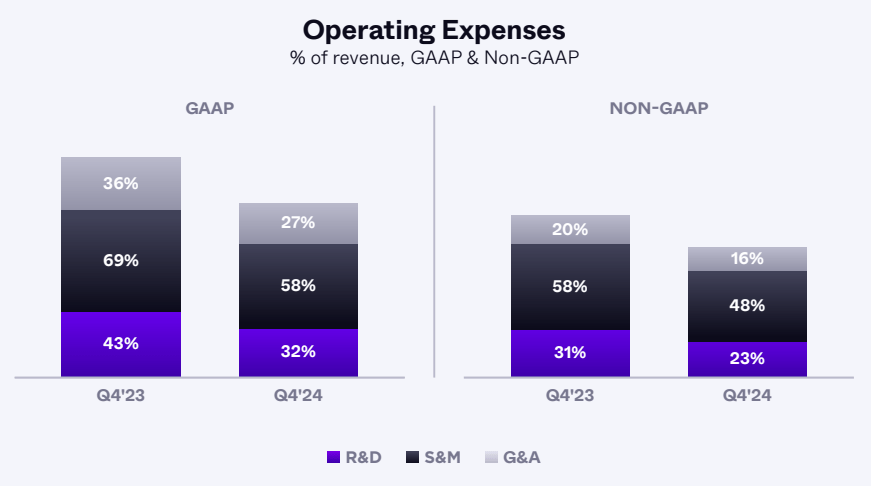

Revenue is slowing but GAAP margins are improving (YCharts)

During the last year, revenue growth has obviously slowed down from the sky-high rates (triple digits) that the company has maintained since its IPO in July 2021. In the latest quarter a further deceleration was recorded as revenue came in at $174 million, up about 38% from the same quarter the year before. However, Total Operating Expenses in the same period grew only 9.5%, a stark improvement of operating efficiency. In particular, SG&A expenses went dramatically down and in the quarter represented 84% of revenue. Don’t get me wrong, that is still an outrageous portion of revenue going towards overhead, but in the past SentinelOne used to spend over 120%-130% of their revenue in SG&A, which helps to put the latest figure in context.

SentinelOne Q4 2024 Letter to shareholders

Truth be told, it has been a while since SentinelOne was trending in the right direction given that it has been nine quarters in a row that they expand revenue at a faster clip than total operating expenses; however, the spread between the two figures used to be quite small and it has been only in the past year or so that the company has dramatically changed strategy to more seriously pursue profitability. Although SentinelOne is not there quite yet, the path is very clear to me and I have no doubt that management will continue to reign in expenses in order to achieve profitability quite soon.

The market did not like the latest quarter

The cybersecurity provider published their 4Q 2024 results on 13 March and the market reaction was very negative. Shares were aggressively sold off, and still now are trading about 18% down since the quarterly release. The main culprit was guidance, as management has targeted Revenue for FY2025 to come in between $812 and $818 million, while Wall Street was expecting $817.5. The market reaction seems quite aggressive considering how tiny the guidance miss was, however it signals in my opinion how Wall Street is worried about the slowdown in sales as a whole, considering that SentinelOne comes from six straight quarters of lower YoY revenue growth. The downbeat guidance has probably spooked investors as there seems to be no end to the slowdown in sales.

I personally think there is more to the story. The data clearly say that management has willingly accepted lower revenue growth by turning down marketing expenses aggressively. I believe the two figures are directly correlated and it is simply a matter of executing strategy. SentinelOne could turbo charge its growth into much higher top-line growth rates, but that will come at the expense of the cash reserves as it will push profitability further and further away.

Sales and marketing expenses are correlated with Revenue growth (YCharts)

Despite the lower sales and marketing expenses the company has continued to record good customer growth numbers. In the latest quarter, customers contributing at least $100,000 in Annual Recurring Revenue grew 30% to 1,133, while also those that accounts for at least $1 million of ARR grew at “record numbers” according to management’s commentary, although no clear numbers were provided.

SentinelOne Q4 2024 Letter to shareholders

Although SentinelOne has no cash problem (about $926 of cash or investments and no debt), management is currently willing to sacrifice short-term growth in order to retain cash on the balance sheet. That is probably in response to a challenging macro environment, with many enterprise customers still today rationalizing their expenses. I personally applaud the strategy because interest rates are not zero anymore, money now has a cost and companies should be more prudent in the way they manage their liquidity. Investors too should expect companies (growth ones too!) to behave differently in this regard compared with the 13 years of expansive monetary policy that we have recently left behind.

One funny note that I have seen more and more recently: growth stocks that IPOd when money was cheap and raised tons of cash in the process, are now actually earning more from their cash than from their business. While SentinelOne has never recorded a quarter of positive operating cash flow, in their latest quarter they recorded $12 million of interest profit on their invested cash. In the trailing twelve months, that figure came in at $44.7 million. That is not bad at all for a company that in the same period recorded negative operating cash flow of $68.4 million.

Cybersecurity is still the place to be

The bull thesis surrounding SentinelOne is still intact. Cybersecurity is increasingly treated as a must-have by enterprise and mid-size businesses alike. New generation cybersecurity providers such as Crowdstrike and SentinelOne are growing like weeds, quickly supplanting incumbents as they offer generally better quality and value. Cybersecurity threats have become harder to detect as they constantly evolve, while they also start to deploy AI technologies themselves to bypass current security systems. From the latest earnings call:

For so long, disjointed platforms and legacy vendors have played whack-a-mole with point solutions, trying to cover security gaps just to see new ones emerge. We believe this is a failed approach. It drains resources and gives a false sense of protection. The frequency and intensity of modern-day attacks make it abundantly clear that legacy solutions, siloed products and disjointed platforms are failing. SentinelOne delivers the best protection in the market. Our Singularity platform is data-driven adaptive and delivers AI-based security, all of this through a unified platform and single agent.

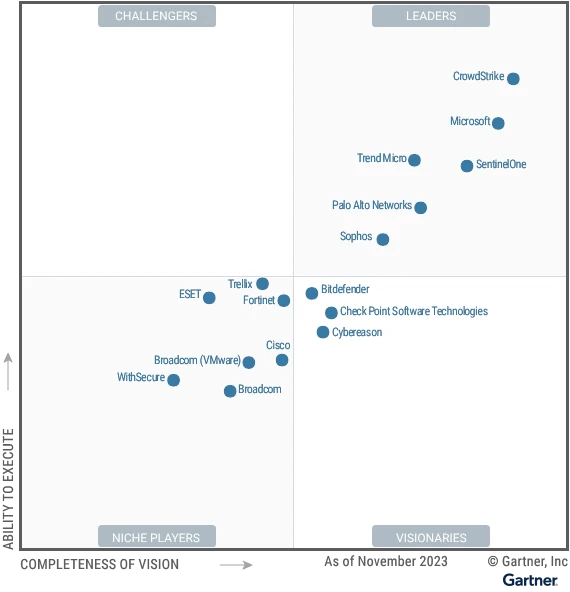

SentinelOne has been recently awarded as one of the leaders in the 2023 Magic Quadrant for Endpoint Protection Platforms by Gartner.

Gartner Magic Quadrant for Endpoint Protection Platforms. (Gartner (December 2023))

The size of the cybersecurity market that SentinelOne is targeting is huge and it is growing. Management identifies a Total Addressable Market of at least $100 billion, while also acknowledging that this market is so big and has so many nuances that it will always naturally accommodate many successful providers.

There are obviously risks as well. One of the more immediate ones when investing in cybersecurity providers is that if the company suffers a breach the reputational damage could be enormous. Moreover, as we talked about before, by being a smaller player SentinelOne cannot yet enjoy efficient scale and that is inherently riskier as an investment, but this risk is effectively mitigated by the very positive cash position the company is enjoying as well as by the operating costs reduction initiatives. The current fiscal year (2025) will be a pivotal moment for the company as I believe they will reach profitability for the first time, while next year will be crucial to understand how profitable exactly the company can become on a recurrent basis.

Valuation and key takeaways

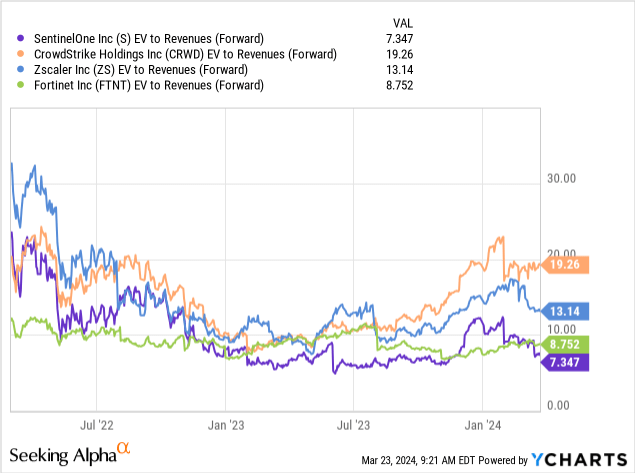

As mentioned above, SentinelOne’s stock crashed about 18% since the earnings release. Despite the drop, the stock is not exactly cheap considering that it is trading at a Price to Sales ratio of 10.82x. If we strip out the cash and only consider Enterprise Value, the stock is still trading at a steep EV/Sales of 9.50. However, even though revenue growth is declining the company is still a growth stock and thus forward values probably give a better indication of the valuation here (8.32x and 7.22x respectively). As of now SentinelOne is unprofitable, and thus more traditional metrics such as P/E or P/FCF are effectively useless.

Although in absolutes those are quite expensive ratios, the valuation starts to look much more compelling if compared with some of SentinelOne’s peers in the cybersecurity space.

YCharts

Most people consider CrowdStrike (CRWD) the leader in the space, and its crazy valuation indeed represents a huge premium on the rivals. Given how well SentinelOne is performing and considering they are turning the corner on profitability, this seems like a compelling moment to start accumulating some shares. Growth stocks are greatly affected by the general market behaviour, thus investors should know that all the above stocks will absolutely crash if the economy slows down or enters a recession. High valuations always imply that a good portion of them trades purely on market sentiment. It is always advised to mitigate this risk through appropriate sizing in a diversified portfolio. However, if SentinelOne continues to grow as a company, the next 5 to 10 years could very well be lucrative for buyers at today’s price.

Q2 2024 Earnings Call Transcript")