JHVEPhoto

Dear readers,

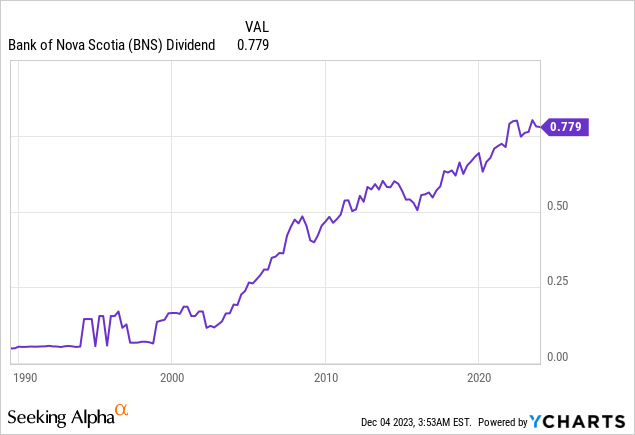

Bank of Nova Scotia (NYSE:BNS) or Scotiabank for short is one of five major Canadian commercial banks. Canadian banks, in general, have a great track-record of paying high, reliable and growing dividends and therefore make a great addition to any income-oriented portfolio. BNS in particular started paying its dividend in 1833, has increased it pretty consistently by 4-6% per year and now has the highest dividend yield of the peer group at 6.9%.

I’ve covered the stock before and called BNS the best value amongst Canadian banks. Since then, the stock has underperformed the S&P 500, but has held up quite well in light of the mini banking crisis which we had earlier this year.

Seeking Alpha

The stock has a significantly higher yield and consistently trades at lower multiples than its biggest peers The Toronto-Dominion Bank (TD) and Royal Bank of Canada (RY). Historically, a large part of this discount could be attributed to relatively weaker management, which has failed to create significant value for shareholders. This is evident if we differentiate the total annual return over the past 10 years of TD and RY of 8.5% vs. 3.9% for BNS, and has led many to call BNS a value trap.

But that tide could be turning.

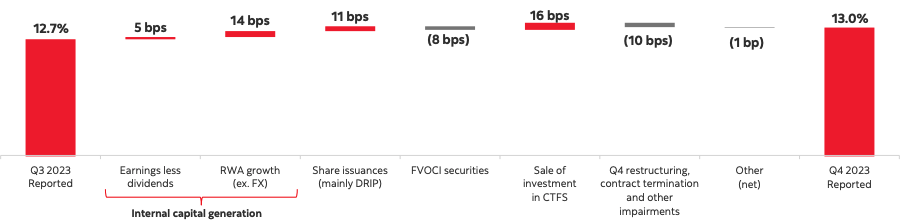

In January of this year, management made a commitment to fortify the bank’s capital position and enhance the CET1 ratio from 11.5% at the time (barely above the 11% regulatory limit) to 12%+ by the end of the year. And they have overdelivered on that promise, as the ratio now stands at 13%.

BNS Presentation

The bank has also significantly improved their liquidity coverage ratio from 119% to 136% and their net stable funding ratio from 111% to 116%.

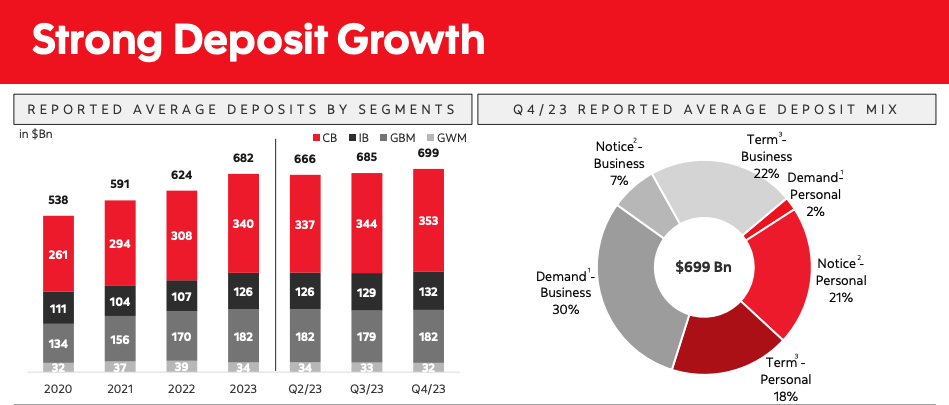

Moreover, the capital position has been reinforced by continually growing deposits, thanks to a number of newly introduced cross-sell methods, as deposits across the whole bank increased by 9% YoY.

BNS Presentation

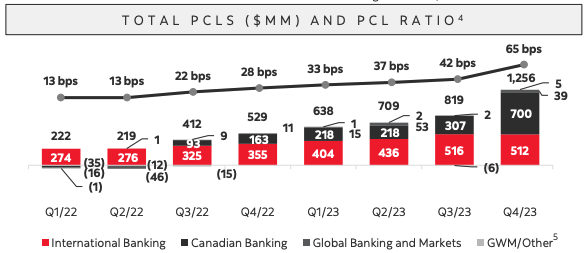

Management has clearly been playing defense in 2023. Nowhere is this more evident than in significant increases in allowances (ACLs) and especially provisions (PCLs) for credit losses, which reached $3.4 billion in 2023, about $2 billion higher compared to last year.

These increases took place primarily during the fourth quarter as the PCL ratio increased from 42 bps to 65 bps in response to worries of weakening consumers in Canada. However, a sizeable part ($1 Billion) of the enhance in PCLs was precautionary and related to performing loans. Moreover, net write-offs stayed flat in Q4 and 90+ day delinquencies have only ticked up marginally (0.22% in Q3 vs. 0.25% in Q4).

BNS Presentation

Steep YoY increases in PCLs have had significant implications on earnings.

Recall that BNS generates about 40% of its revenue in Latin America and operates in four key business lines – Canadian Banking, Global Wealth Management, Global Banking and International Banking.

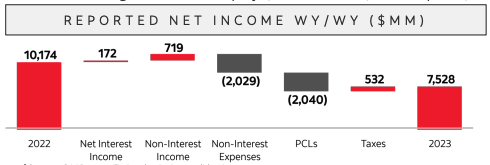

Total earnings have declined by 26% to $7.5 Billion. On a business line level, the biggest segment, Canadian Banking has seen earnings refuse by as much as 16% YoY, while International Banking was the only segment with positive (+3%) YoY earnings growth.

BNS Presentation

BNS’s future results will in large part depend on the strength of the economy and the consumer, which will ultimately ascertain whether the performing PCLs can be reversed or whether more loans will become impaired.

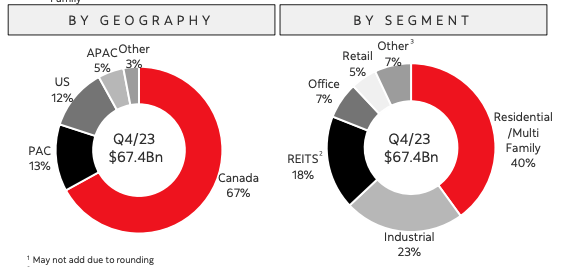

All things considered, I appreciate that management has taken steps to improve their liquidity position. Moreover, I also appreciate that of the bank’s $70 Billion commercial real estate portfolio, office only accounts for $6.2 Billion or 7%, which helps alleviate a large part of commercial real estate risks.

BNS Presentation

Valuation

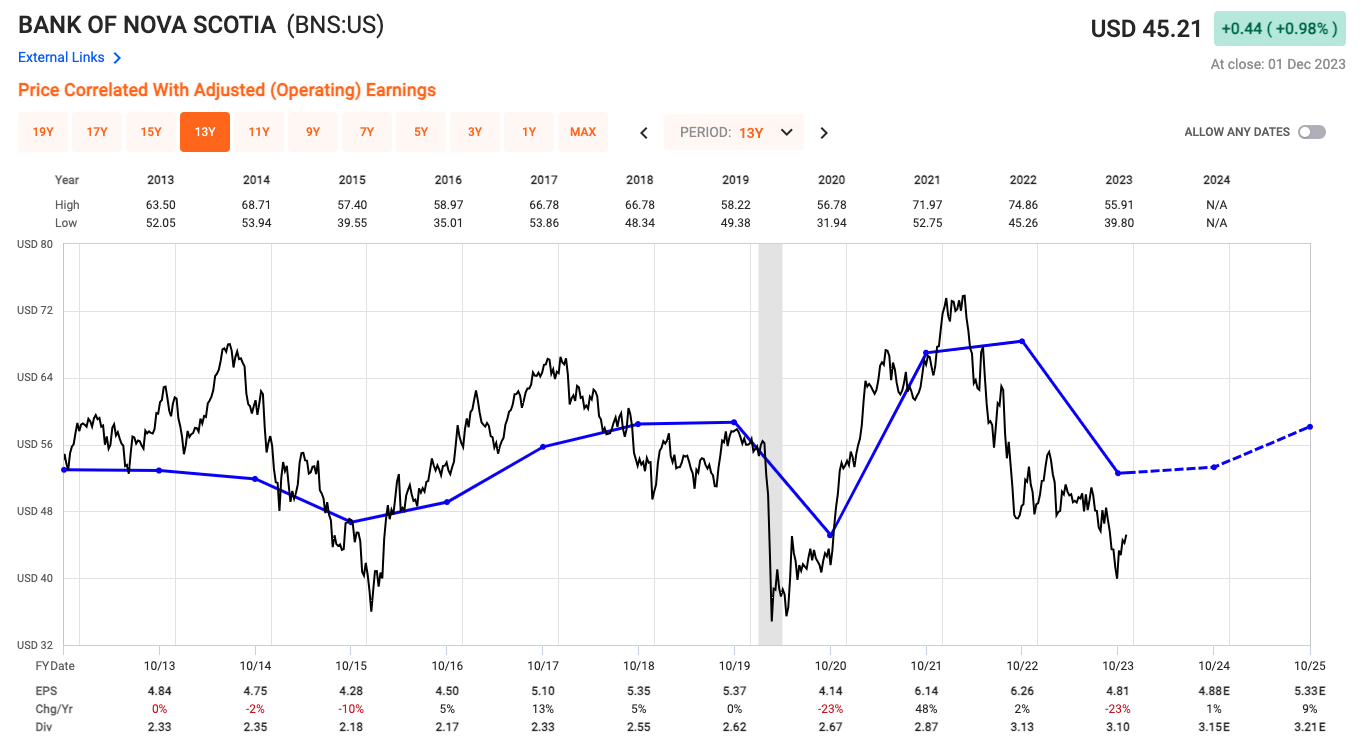

BNS is an A+ rated company with a well-covered dividend (payout ratio of 65%). As such, it can form a reliable basis of any income-oriented portfolio. At the same time, the stock now trades at a very reasonable 9.4x earnings, despite what I consider trough EPS. BNS remains cheap relative to peers, with TD at 10.2x earnings and RY at 10.8x earnings.

The consensus is for flat earnings in 2024 and potentially growth of up to 8% in 2025. I’m not a fan of forecasting steep acceleration of growth out of nowhere, though here it’s likely related to the general consensus that the economy will slow next year, rates may decrease somewhat and growth could return in 2025.

Still, even assuming no EPS growth from here, the stock offers a nearly 20% upside potential to its historical average P/E of 11x. I think the stock can easily accomplish $55 per share in the current status quo.

And if earnings rebound from trough levels, which I have high confidence that they eventually will (think 3-5 years from now), the stock could easily accomplish $65 per share. For this to happen, we will likely have to get through the current period of high interest rates, but the good thing is that BNS pays a high dividend, which will make the foresee quite bearable.

Fast Graphs

For these reasons, I continue to rate BNS a BUY here at $45 per share.

Q2 2024 Earnings Call Transcript")