Bloomberg/Bloomberg via Getty Images

Introduction

Scorpio Tankers (NYSE:STNG) is still my favorite product tanker stock. The company delivered good results in 2023, expanding its profit margins, reducing its debt, and actively repurchasing shares. The macro and geopolitical headwinds are still intact. They act as catalysts for the already hot tanker market. The aging fleet, low order book, and limited shipyard capacity constrain the supply side. On the other hand, the demand remains strong due to higher refinery output and a global shift in oil demand and supply. I believe we are in the middle of the tanker cycle. So, there is more upside potential to be exploited. STNG still offers the best bang for the buck relative to TORM Plc (TRMD) and Hafnia Limited (OTCQX:HAFNF). Scorpio remains a strong buy.

Product tankers and Scorpio fleet update

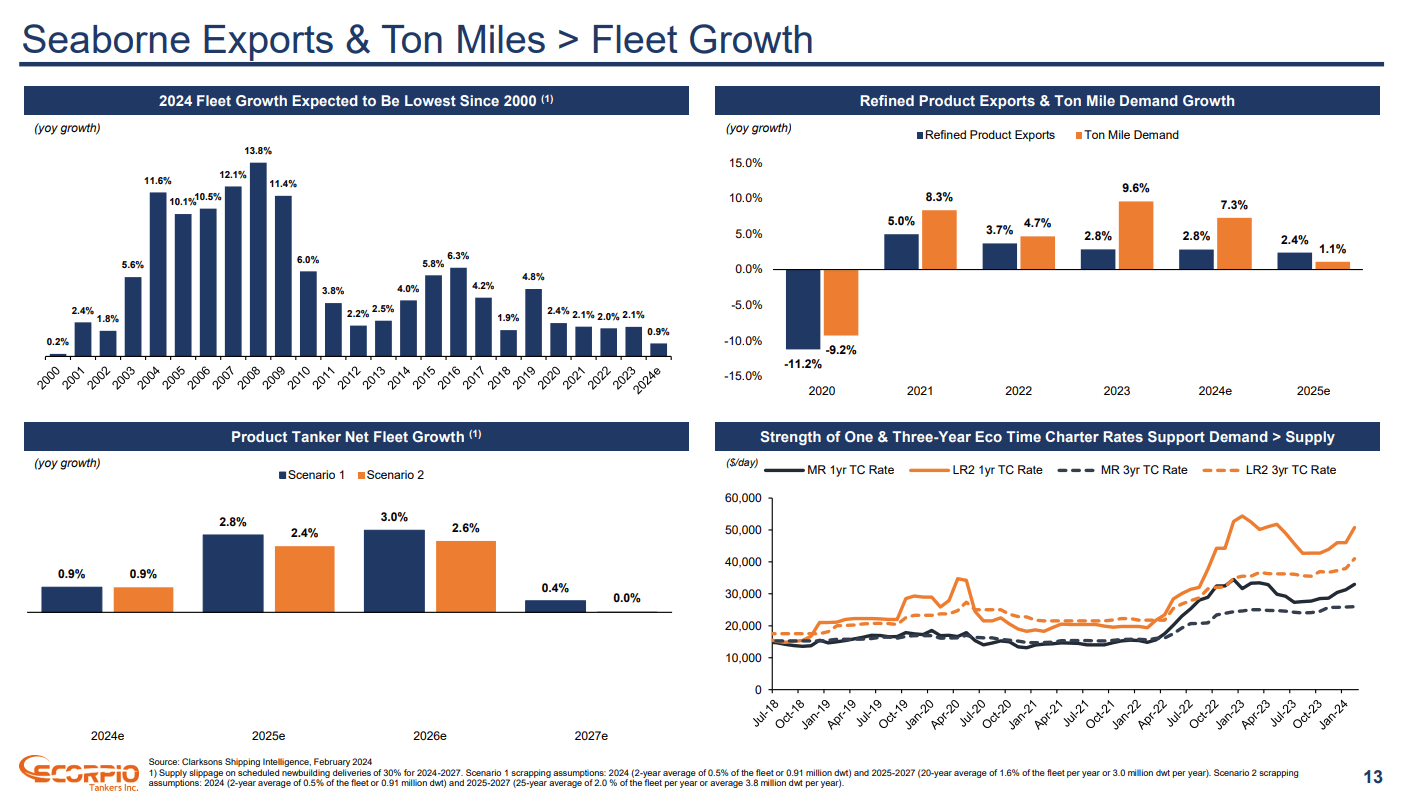

My expectations on the product tanker market remain unchanged. All variables I discussed in my first article on STNG are still intact. The supply side is impacted by order book below 10% and overloaded shipyards with LNGs, containers, and car carriers; a growing percentage of the global product tanker fleet is approaching 20 years.

In 2024, the product tanker fleet growth is expected to be 0.9%, while refined product exports will rise by 2.8% and ton-mile demand by 7.3%.

STNG presentation

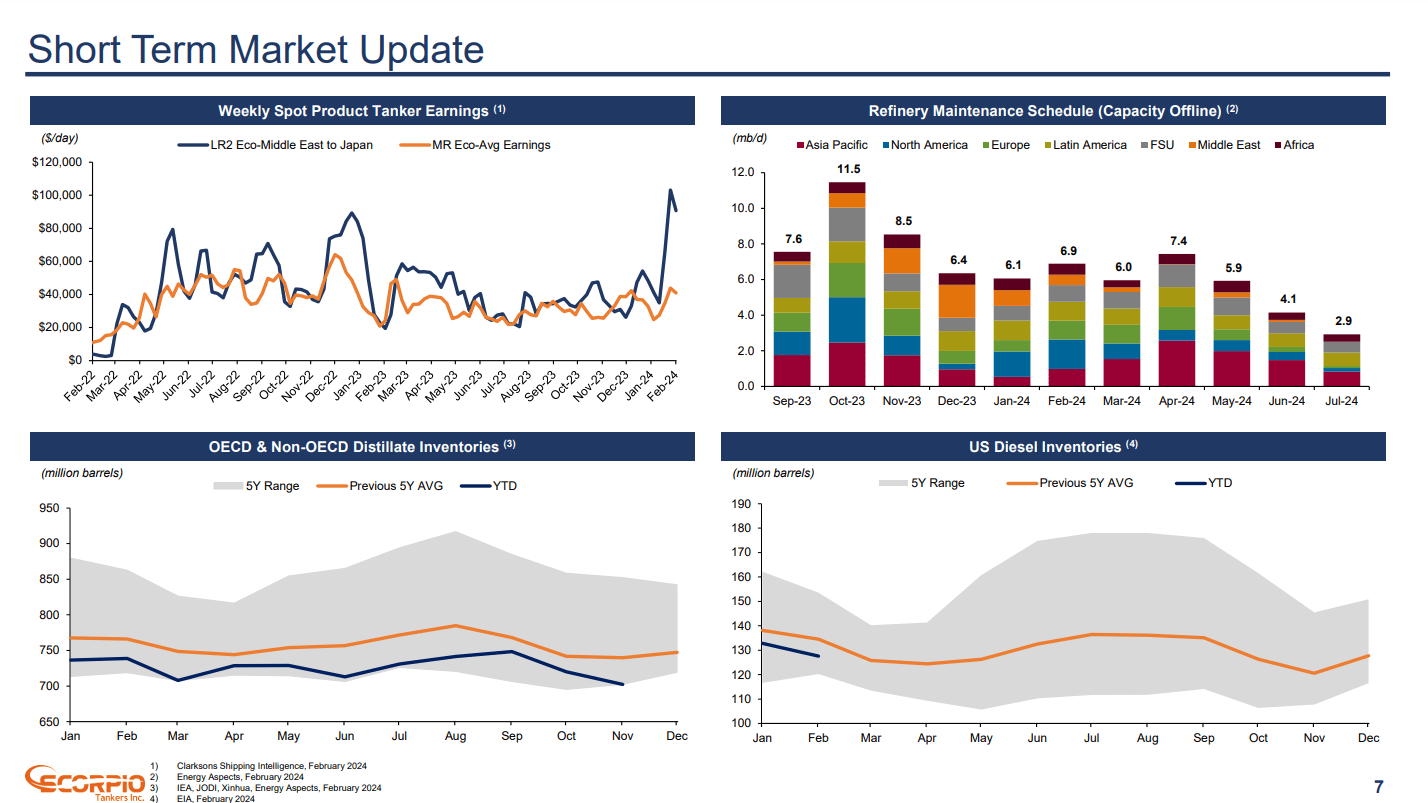

The demand is pushed by the declining number of refineries scheduled for maintenance and low distillate inventories in the OECD and the US, approaching the lower limit of the 5Y range. The image below from the 4Q23 presentation shows short-term market updates.

STNG presentation

On the other hand, long-term factors such as shifting oil production from East to West and consumption from West to East will inevitably impact the demand for product tankers. More refining capacity is planned in Asia, while more production capacity is expected in the Western Hemisphere. Simply put, more tankers are needed first to carry the crude from West to East, then to transport the CPP (clean petrol products) to its final customers.

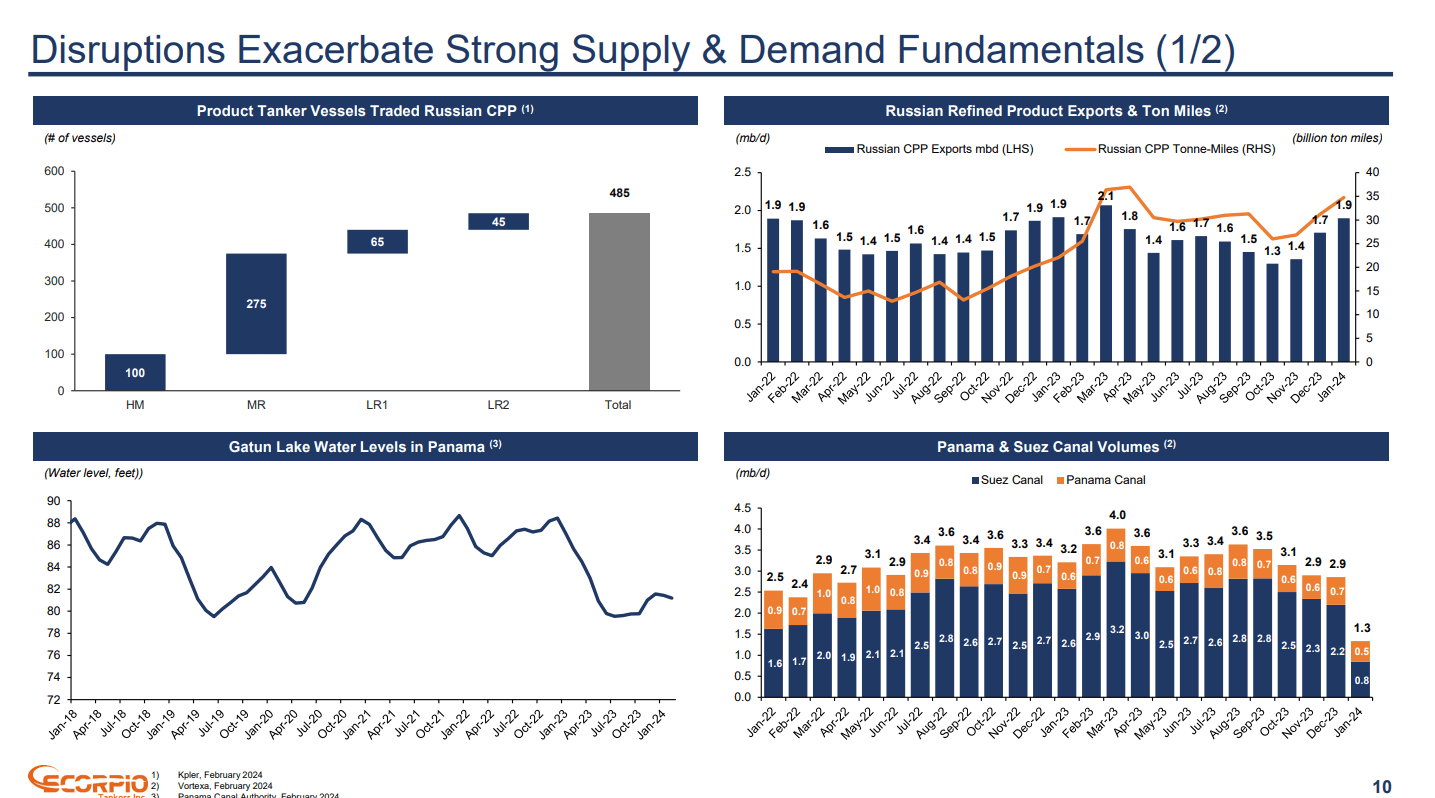

The Red Sea crisis will remain predetermining, boosting the already rising tanker deficit. It does not seem to be resolved any time soon. The image below shows the impact of the Gatun Lake drought and the Red Sea crisis on shipping traffic.

STNG presentation

The bottom right graph illustrates the impact of supply chain disruptions on CPP transportation. In January 2024, 0.8 mb/d sailed via the Red Sea and 0.5 mb/d via the Panama Canal. Combined, it is a 1.6 mb/d (55%) decline month over month. For reference, in January 2024, the total CPP exports were 20.6 mb/day. This means 7.7% of CPP exports had to be rerouted due to the disruptions. So, I expect the tanker rates to keep rising following increased product ton-miles.

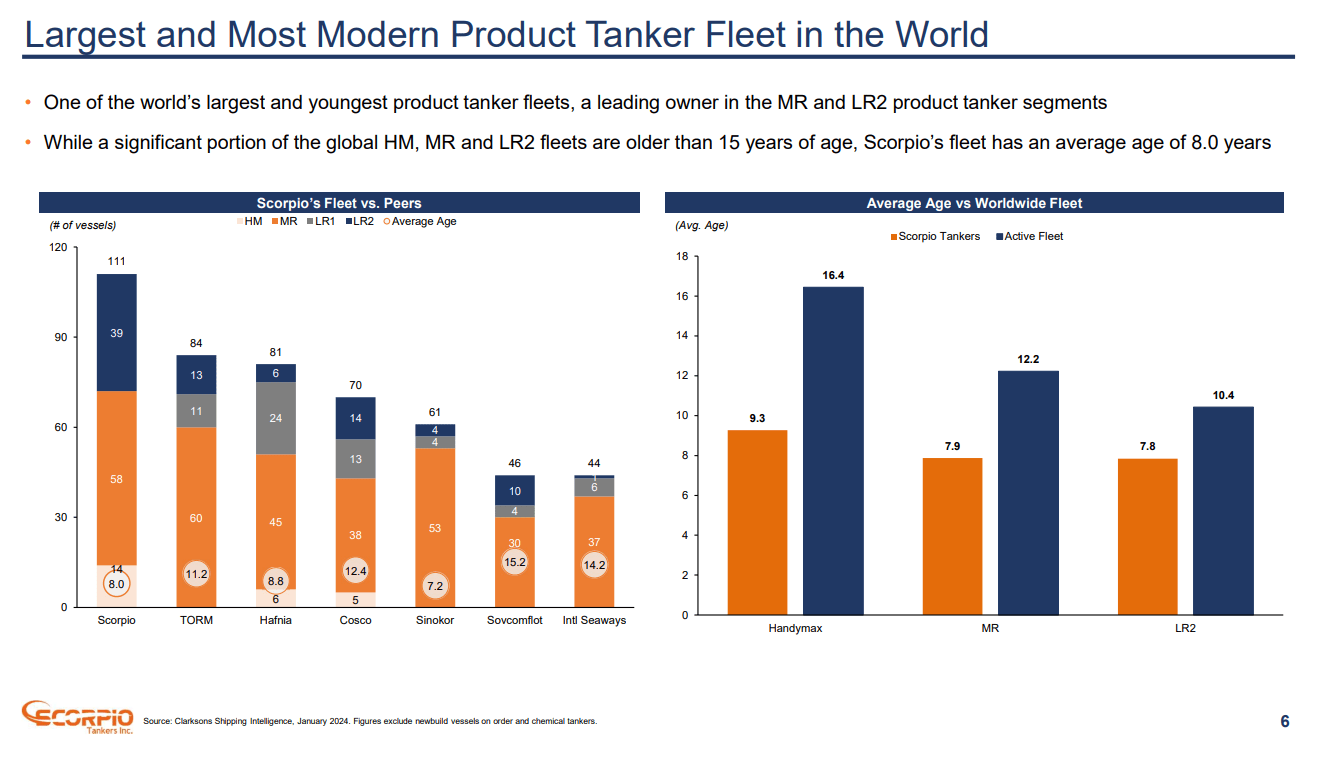

Scorpio has 111 vessels with an average age of 8.1 years. The fleet composition is 39 x LR2, 58 x MR, and 14 x Handymax. In 4Q23, the company sold one of its MRs, STI Tribeca, for $39.1 million. In the meantime, it exercised its purchase options in four Handymax vessels built in 2014 and one MR 1025 built. 85 of the ships are scrubber fitted.

STNG fleet remains one of the best in the industry:

STNG presentation

As seen on the right chart, its ships (Handymax, MR, and LR2) are well below the average age for the worldwide fleet.

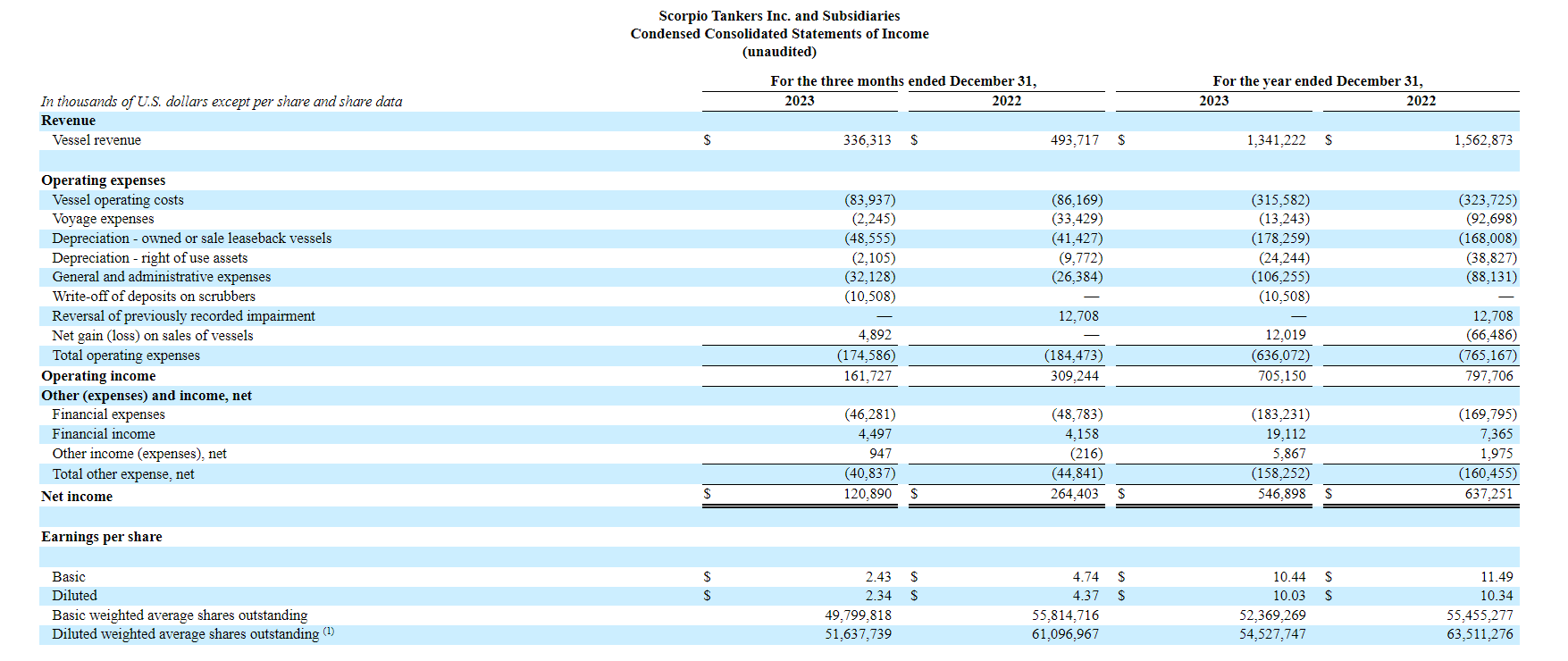

STNG 4Q23 and 2023 results

The table below shows the company’s 4Q23 vs. 4Q22 and 2023 vs. 2022 results.

STNG 4Q23 filling

4Q23 revenue is $336 million, 32% lower than 4Q22. Voyage costs declined from $33.4 million in 4Q22 to $2.2 million in 4Q23. The operating expenses dropped by $2.2 million, reaching $83.9 million in 4Q23. TCE rates for the whole fleet were $32,949/day, $12,600 lower than 4Q22. On the other hand, the daily operating costs dropped, reaching $8,181/day. STNG delivered a $120 million net income and $2.43 EPS in 4Q23. The net income decreased by 54% YoY while the EPS by 48%.

STNG delivered $1.34 billion in revenue for 2023, $262 million lower than in 2022 when the company achieved $1.56 billion. Fleet composite TCE rates for 2023 were $32,711/day, while in 2022, $37,548. Daily OPEX per ship increased by 3%, from $7,460 in 2022 to $7,692 in 2023. Handymax day rates realized the largest decrease compared to MR and LR2 ships, from $39,525/day in 2022 to $29,578/day. LR2 and MR TCE day rates dropped by 0.7% and 7.3% respectively. MR daily OPEX per ship grew by 10%, while LR2 OPEX increased by 6%. 2023 STNG achieved $705 million operating income and $546 million net income. In 2022, the company delivered $797 million in operating income and $637 million in net income. As a result, EPS declined by 9%, reaching $10.44 in 2023.

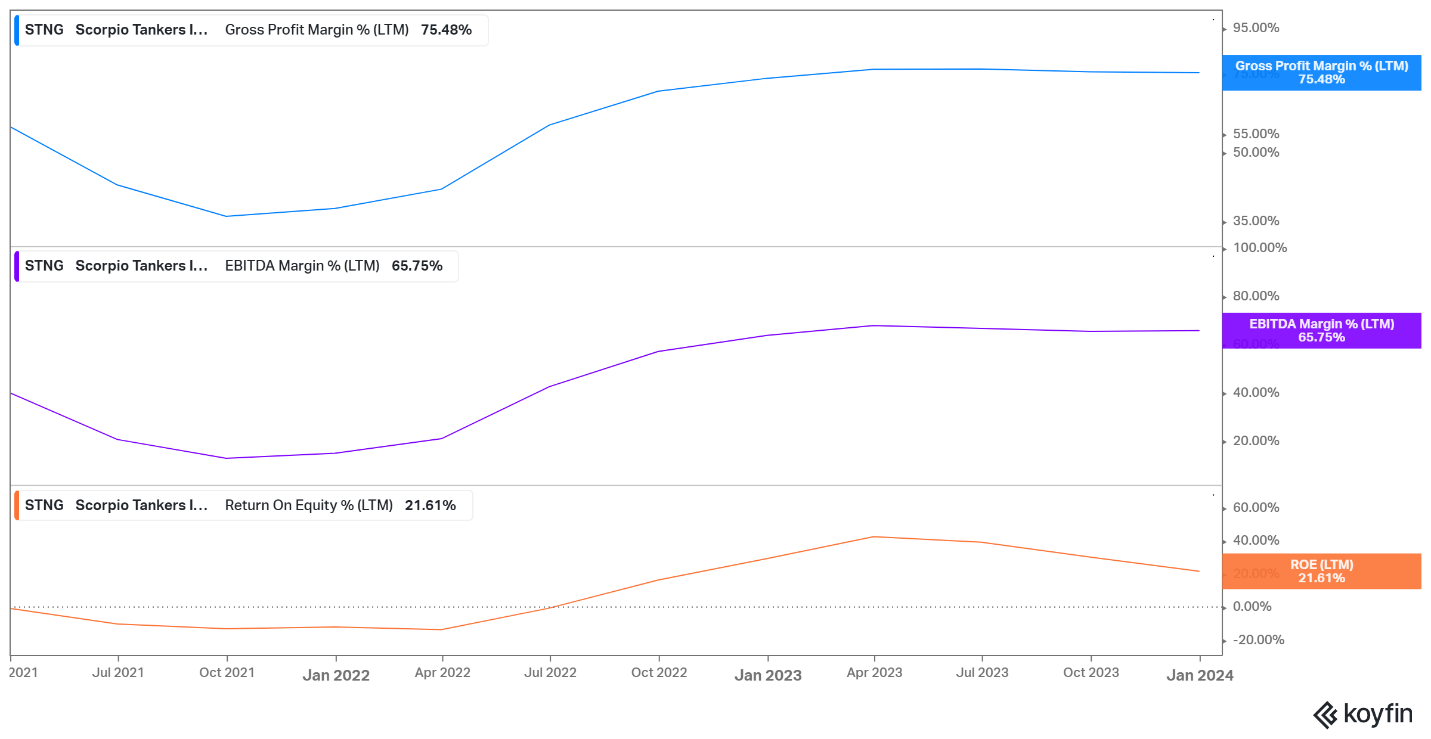

STNG improved its margins over the last several quarters, as seen in the chart below.

Koyfin

Since 2022 gross profit margin grew from 41% in March 2022 to 77% in March 2023. The EBITDA margin increased from 21% to 66% for the same period. Return on equity has dropped in the last three quarters following the declining net income.

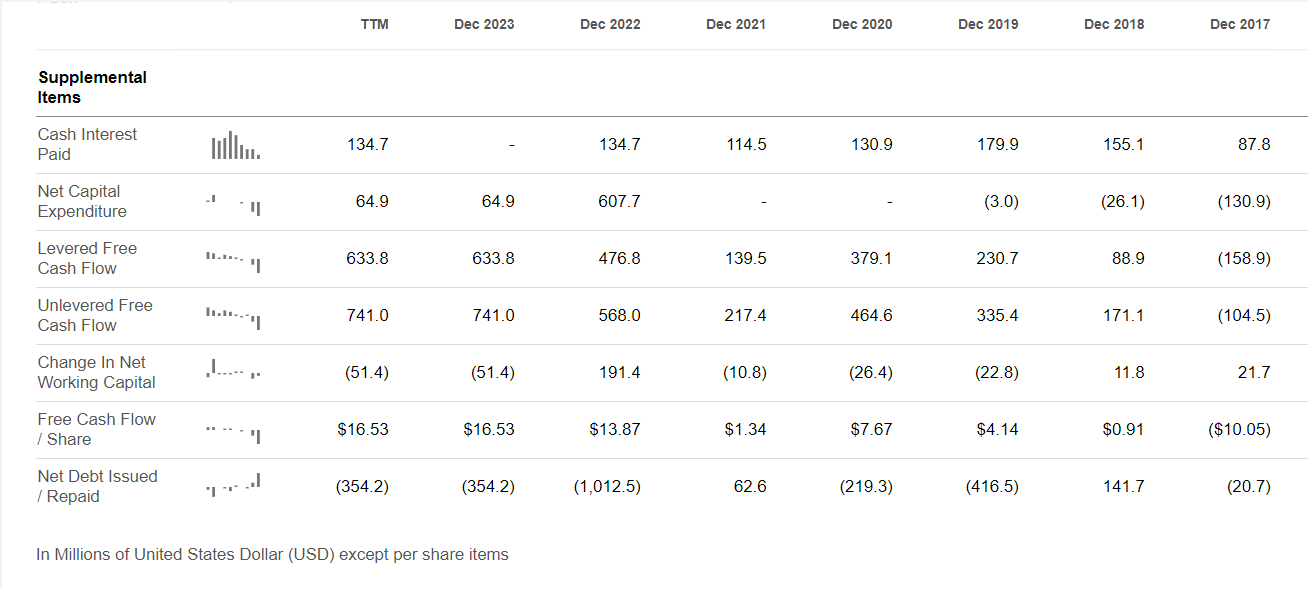

It is worth mentioning the growing free cash flow YoY.

Seeking Alpha

In 2023, the company achieved $741 million unlevered FCF, $173 million higher than in 2022. FCF per share increased from $13.8 in 2022 to $16.5 in 2023. At the current stock price, it is a 23.9% FCF yield.

Company financials

STNG maintains an excellent balance sheet, with 62.2% total debt/equity and 39.6% total liabilities/total assets. In its 4Q23 report, the company declared $355 million cash, $939 million long-term debt, and $221 lease agreements. In 2023, STNG generated $865 million operating cash flow and $705 million operating income. For 2023, the company had to pay $164 million in net interest expenses.

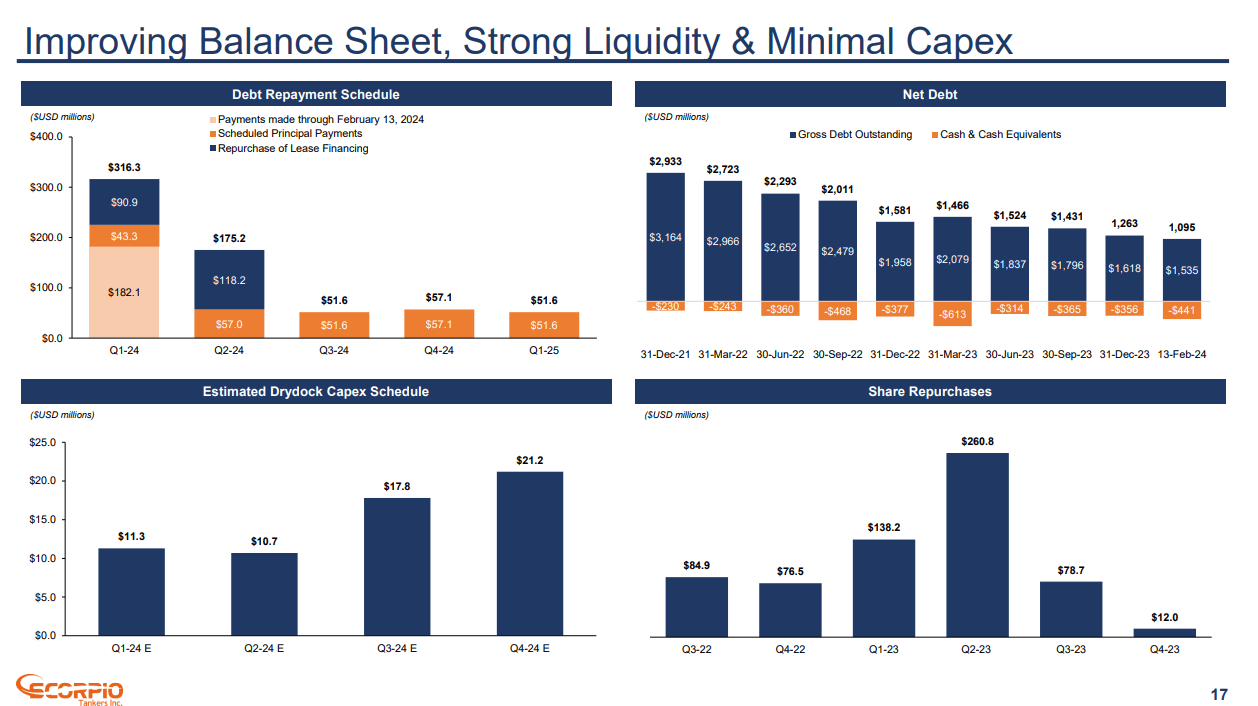

The table below shows the company debt repayment schedule for 2024, dry dock plans for 2024, and share buybacks for 2022/2023.

STNG presentation

$600 million debt is due for 2024. In 1Q24, STNG must pay a $316 million debt. Until February 13, 2024, $182 million in payments has been made. In 2Q24, $175 million is due. In 2024, 9 LR2, 30 MRs, and 14 Handymax are due for drydock. The total dry dock CAPEX is $61 million.

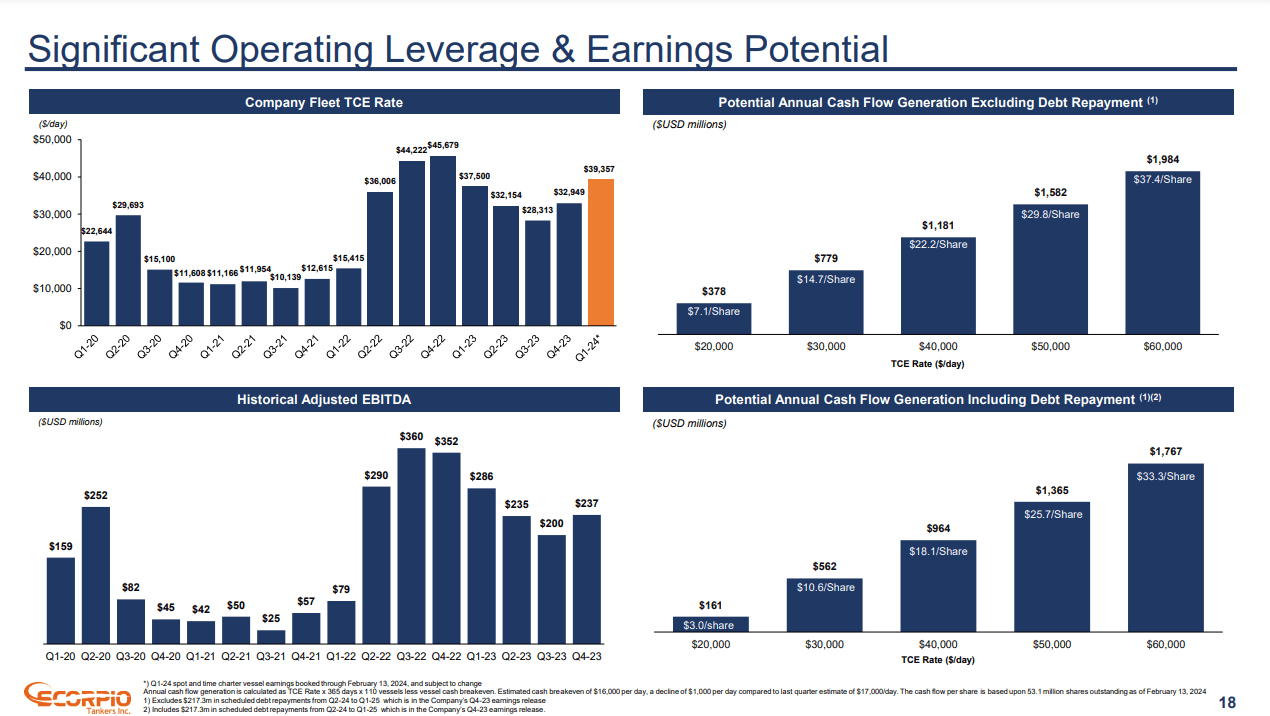

The following image shows STNG’s profitability and TCE rates.

STNG presentation

STNG 1Q24 TCE rates are $39,357/day, 20% higher than 4Q23. At TCE $40,000/day, the company is expected to deliver $1,181 million in cash flow ($22.2 per share), excluding debt repayments, and $964 ($18.1 per share) million, including debt repayments.

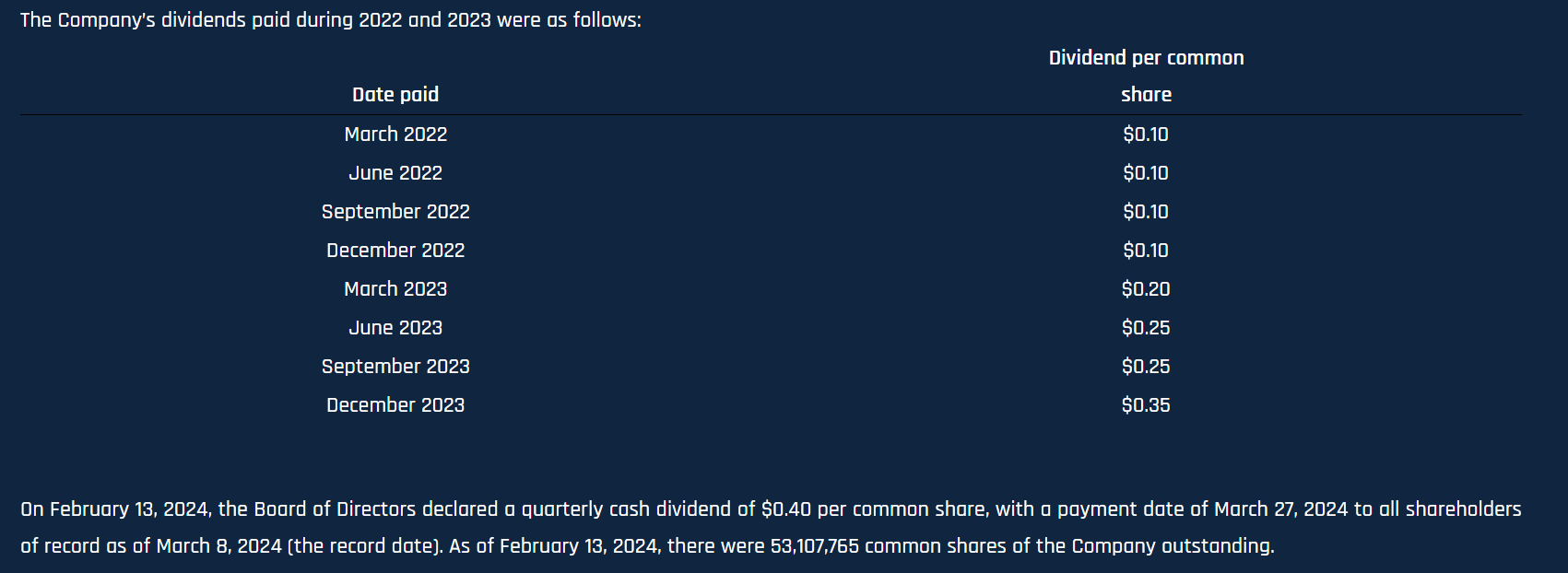

The table below shows STNG dividend payments over the last two years.

STNG website

STNG TTM dividend yield is 1.51%, and FWD yield is 2.3%. In 4Q23, the company distributed a $0.35/share dividend. STNG returns value to its shareholders using buybacks. In 2023, STNG repurchased shares for $489 million, delivering a 14.39% LTM buyback yield. With a strong day rate, I expect this tendency to continue. A week ago, STNG announced its CEO, Robert Bugbee, purchased 5,556 call options with a $60.0 strike expiration in September 2024. The value of the options is $7.0 million.

Valuation

To estimate STNG value, I used Compass Maritime’s weekly report figures. Given the company’s fleet profile, I discounted the prices for 5-year-old vessels by a 5% annual depreciation rate.

- 5Y old LR2 $58 million

- 5Y old MR $39 million

- 5Y old Handymax $24.6 million

STNG inputs are:

- Current Assets: $577 million

- Total Liabilities: $1,674 million

- Fleet replacement cost $4,868 million

Scorpio’s NAV is $3,771 million, and its market cap is $3,400 million. STNG trades at 90% P/NAV. TRMD trades at 112% P/NAV and HAFNF at 98% P/NAV. I expect rising inflation in the coming months, pushing the shipping company’s NAV further. The equation below shows the impact of increased inflation on the shipping companies.

The rising cost of financing + rising cost of labor + rising cost of steel > rising price of newbuilds > growing NAV > declining order book > tighter supply side

Despite the rising share prices, STNG remains attractively priced. In 3Q23, STNG traded at 75-82% P/NAV. Unlike the vessel prices, the stock price is more erratic in the short term. However, the inflation pressures are like a tide; they lift all boats.

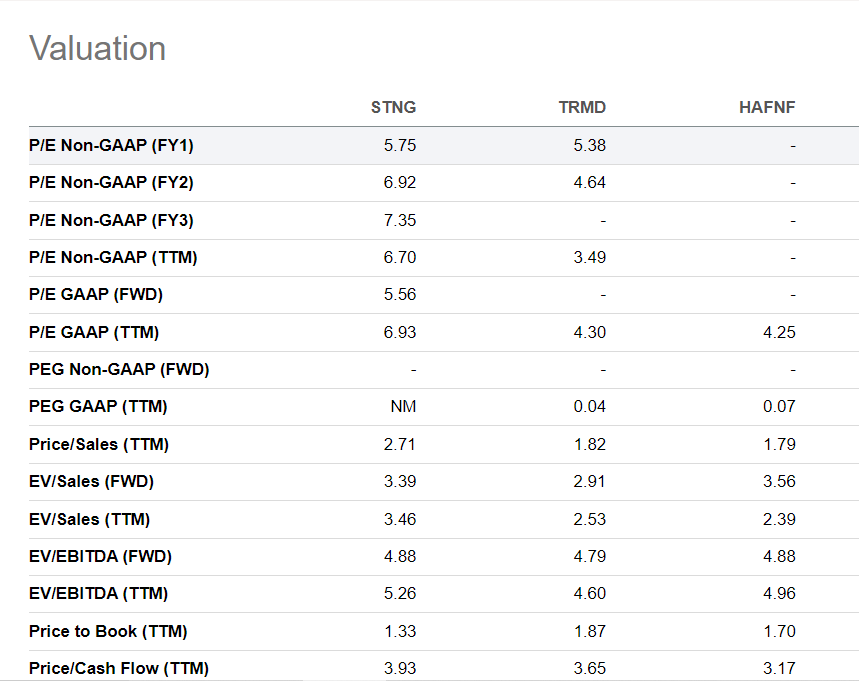

STNG trades at higher EV multiples (3.46 EV/Sales, 5.26 EV/EBITDA) compared to HAFNF (2.39 EV/Sales, 4.96 EV/EBITDA) and TRMD (2.53 EV/Sales, 4.6 EV/EBITDA).

Seeking Alpha

We must consider STNG fleet quality; 78% of its ships are scrubber-equipped, and its fleet average age is eight years. HAFNF fleet age is 8.5 years, and 18% of the ships have scrubbers, while the TRMD flee age is 12 years, and 72% of the fleet has scrubbers.

Investors Takeaway

STNG remains an integral part of my portfolio. Tanker industry fundamentals support my thesis that we are in the middle of the upward cycle. Adding macro and geopolitical tailwinds, I expect tanker stocks to perform well in 2024. Inflationary pressure will keep boosting shipping companies NAV, while the Middle East crisis will remain the major catalyst for supply chain disruptions.

The decline in CPP demand is a significant risk for my thesis. It can materialize in case of global recession. The Chinese economy has been in questionable condition. The Chinese government started to pour liquidity with fiscal stimulus to boost the economy. India takes the role of the global growth engine. Its economy is projected to grow by 6.4%-6.7% in 2024. So, for now, the global recession scenario remains plausible but not so probable. A rising geopolitical risk counterintuitively is positive for shipping in general. The Middle East crisis is a prime example. The Houthis have been attacking ships despite Prosperity Guardian’s operation. Financially, STNG is sound, with 62.2% total debt/equity and 39.6% total liabilities/total assets. The company’s operating cash flow and net income provide ample liquidity.

STNG is perfectly positioned with its relatively young fleet equipped with scrubbers. Despite its strengths, STNG trades at a lower P/NAV than HAFNF and TRMD. Nevertheless, the latter command higher EV/Sales and EV/EBITDA multiples. TRMD and HAFNF distributed dividends with impressive TTM yields at 20.5% and 14.6%, respectively. STNG, however, delivered a 14.9% buyback yield for 2023. My verdict remains unchanged: STNG deserves a strong buy rating.

Q2 2024 Earnings Call Transcript")