Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

Apropos the SEC approving spot bitcoin ETFs overnight, choose your fighter.

Deutsche Bank: ‘this is good for bitcoin! Aargh!!!!’

Despite prevailing consumer sentiment leaning towards negativity,* we anticipate further [bitcoin] price increases in the coming year due to three primary factors. First, the approval of a Bitcoin ETF opens the doors for greater institutional investment. A spot Bitcoin ETF will make it easier for investors to gain exposure through a regulated vehicle, potentially appealing to both retail and professional investors. This could drive large inflows into the market. Bitcoin’s supply is limited, so increased demand amid constrained supply would put upward pressure on prices. We’ve already seen prices climb significantly this year on anticipation of the decision.

Second, central banks rate cuts in 2024 will drive more investors to invest in crypto for higher return. The macroeconomic landscape of 2020 and 2021 – characterised by low interest rates and high liquidity – created a one-of-a-kind environment for the growth of non-traditional investments like cryptocurrency. As governments pumped billions into economies through successive stimulus packages, Bitcoin exceeded $65k. Then came the global inflationary spike of the last 18 months. In response, central banks raised their respective interest rates sharply, making traditional investment products a more attractive option once more, and the price of cryptocurrencies collapsed. Our US and European economics teams now expect the Fed and the ECB to cut rates 175bps and 150bps in 2024, respectively. This will once again stimulate liquidity, driving more investors to invest in crypto in the search for a higher return, putting upward pressure on prices.

Third, comprehensive regulation is on the horizon. [ . . . ] We perceive regulation as a net positive for the industry as it will: (i) increase adoption as a clearer regulatory framework should drive more corporate adoption, higher liquidity (and less concentration); and ultimately (ii) partially help address volatility. This should drive an increase in Bitcoin prices.

In conclusion, based on the factors discussed, we anticipate the price appreciation trend in Bitcoin to continue through 2024. However, one must be cautious not to conflate price gains with broader predictions of cryptocurrency overtaking traditional finance. At its core, a spot Bitcoin ETF simply provides standardised access to the digital asset as an investment, without altering Bitcoin’s core proposition. Only time will tell if greater adoption leads to more transformational outcomes for the crypto ecosystem and financial system. For now, the spot Bitcoin ETF approval opens a new chapter for Bitcoin prices, though volatile conditions are likely to persist.

JPMorgan: ‘digital gold = gold, so big whoop’

ETF approval does not change [mining] economics, demand for mining services, or competitive [mining] dynamics. We see this spot Bitcoin ETF race focused, for the moment, on management fees (of the ETFs) with managers revising their fees lower—we think to attract the initial flows that will drive more sustainable growth. We note that gold prices appreciated in anticipation of a Gold ETF in 2004, but sold off following the launch of GLD. We look forward to seeing both the direction of Bitcoin’s price and the magnitude of the Bitcoin ETF flows. We note that the Gold ETF (GLD) gathered ~$3.5bn in its first year, a far more modest level than many in the cryptocurrency community are anticipating. We remain skeptical of the elevated expectations for inflows into Spot Bitcoin ETFs and calls for $20bn of net new assets in year-1 seem to us overly optimistic.

Morgan Stanley: ‘digital gold = gold, so small whoop?’

An incremental positive for the asset mgmt industry. This has potential to help the industry capture new customers and assets, and at the least allows the industry to defend itself against the potential of money leaving the industry for direct Bitcoin exposure through crypto platforms such as Coinbase.

[E]very 1% penetration of Bitcoin’s current ~$900b market cap would equate to $9b of AUM, potentially representing $26m of revenue at 29 bps median fee rate. As a point of comparison, we see ~$209b of gold ETF AUM, representing 1.5% of the ~$13.6tr of gold market cap worldwide and a weighted average fee rate of 0.29% on gold ETFs.

UBS: ‘this is positive for AI somehow’

Approved ETFs can help investors who face technical challenges in storing digital assets. But fundamentally, we remain unconvinced of the structural case for the industry. Rather than seeking direct exposure to cryptos, we advise longer-term investors to focus on disruptions in both public and private markets—i.e., leading firms that deliver, enable, or use new technology for growth, to gain market share, or to cut costs. We see opportunities in companies that apply and monetize artificial intelligence (AI) across the software, internet, and semiconductor sectors.

* The public (via Deutsche Bank): ¯\_(ツ)_/¯

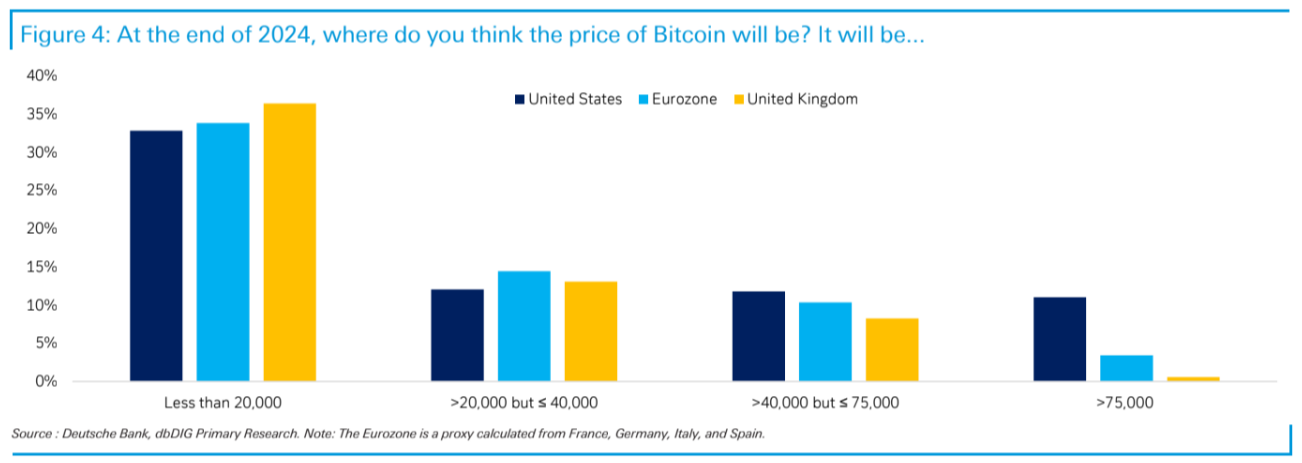

Our December survey of 2,100 consumers revealed that over a third consumers expect the price of Bitcoin to remain below $20,000 in 2024, while 38% responded with ‘do not know’.

[zoom]

Further reading

— Imaginary bitcoin ETFs are already 30 times more valuable than all the actual bitcoin ETFs (FTAV, October 2023)

Q2 2024 Earnings Call Transcript")

{kind=link}