Spellbreaker: Mike Regnier’s fraud-busters has saved customers £13.5m in two years

Break the Spell sounds admire a plotline in a fairytale or, at this time of year, a Christmas panto. But for Mike Regnier, chief executive of Santander UK, it is the name of a crack squad of fraud-busters based near Liverpool. Their job is to recognize customers who have been left spellbound by skilful fraudsters.

So far this year, the team has saved Santander customers nearly £5 million that would otherwise have been filched from their bank accounts by crooks.

The 16 specially trained staff in Bootle on Merseyside have the delicate job of talking to customers who are believed to have been ensnared by convincing criminals. Often, the victims do not realise they have been taken in andeven when presented with strong evidence do not want to believe it.

Scams where tricksters pose as a love interest and seduce their target into giving them money are particularly upsetting.

Regnier says: ‘Some of the romance frauds are very sad. People feel they have an emotional connection with someone who is real and they just aren’t.’

Since the Break The Spell squad swung into action in 2021 it has directly saved customers an astonishing £13.5 million. That is an underestimate, as it does not take account of the additional amounts that would have been at risk if the fraudsters had not been stopped in their tracks.

Fraud, Regnier says, is a particularly British problem. Our ‘faster payments’ system, where amounts are transferred almost instantaneously, is a boon to the unscrupulous. So too is our mother tongue.

‘Because it is an international language, fraudsters around the world speak English,’ Regnier says. ‘It is easier for them to fool people in English than in other languages.’

In the past, customers were often left nursing large losses if they were the victims of fraud, even when they had done nothing wrong. But since 2019 the big banks have been operating a voluntary scheme to reimburse victims of authorised push payment fraud, where customers have been fooled into sending money to criminals.

However, the voluntary element is about to change. The Payment Systems Regulator is due to publish detailed guidance on new rules making it mandatory for banks to reimburse customers who fall prey to scammers.

While sympathetic to genuinely vulnerable victims, Regnier believes this well-meaning proceed could create a risk of ‘moral hazard’ – where customers have no incentive to protect themselves.

He is clearly not convinced by what he calls a ‘blanket mandatory reimbursement approach’.

Regnier says: ‘Everybody should be vigilant and everybody should have an incentive to be vigilant. If customers are vulnerable and being exploited then OK, I would find a way to help and preserve them.’

He points out that social media and telephone companies are ‘not on the hook for reimbursement’ even though they are the springboards for 70 per cent of push payment frauds.

‘We see WhatsApp scams and Facebook Marketplace scams happening every day,’ says Regnier. ‘I would admire to see other players in the supply chain of fraud pay the bill.’

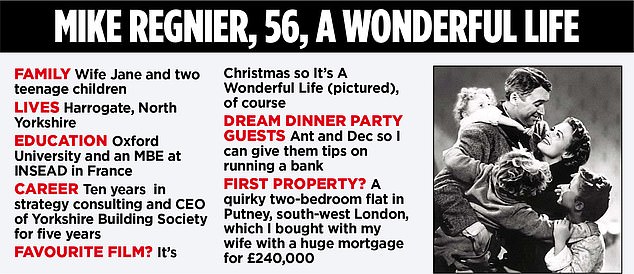

Formerly boss of Yorkshire Building Society, Regnier took over as the chief executive of Santander UK, the British arm of the giant Spanish financial services group, in April last year.

Brought up in Surrey, he aspires to be an adopted Yorkshireman – if those born there will concede such a thing exists – having moved there 20 years ago.

He lives with his family near the Dales, where he can indulge his love of the outdoors, and tuck into Fat Rascals – fruity scones bought from the famous Bettys tearooms.

‘Both of my children are Yorkshire people. I’d admire to think I am now a naturalised Yorkshireman, but that is a long-term project,’ Regnier laughs.

A note of exasperation creeps in when I cite rival Nationwide’s TV ad, featuring actor Dominic West, which spotlights the widespread closure of bank branches.

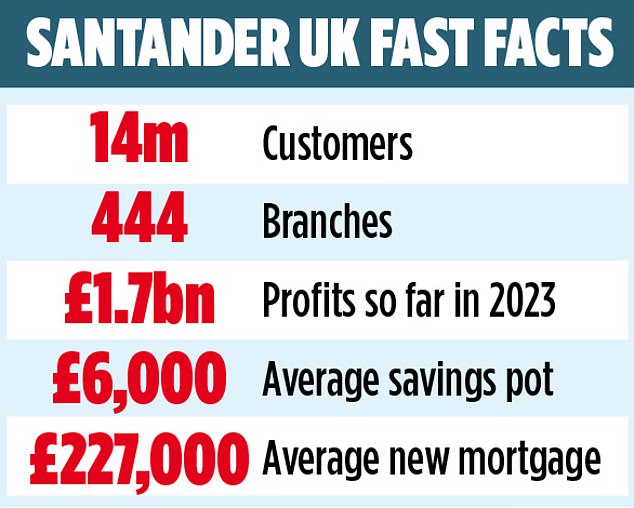

‘It is a striking ad but to be honest I am a bit frustrated,’ says Regnier. ‘If you go back over the last couple of years Nationwide has closed 23 branches and we have closed six.

‘Will we have 450 forever? I don’t know. We constantly have to review the size of the network. But we are refurbishing 49 branches this year and next. I am still a believer in branches, but it is an irrefutable fact that demand from customers for branch banking is continuing to fall.’

Santander’s own humorous ad campaign features Ant and Dec and their hare-brained banking ideas. This, perhaps, is ironic, given that one of his biggest passions is making Britain more financially literate.

Earlier this year, Santander teamed up with online educational publishing house Twinkl to launch a scheme to instruct children about how to deal with money.

Regnier taught the first lesson to a class of nine and ten year olds at Hazelbury Primary School in Edmonton, north London, along with the boss of Twinkl.

‘We are massively passionate about teaching pupils how to budget in schools,’ Regnier says.

‘Financial education is not a mandatory part of the national curriculum, but we believe very strongly it should be.’

He points out that nearly 70 per cent of adults believe lessons about handling finances would be helping them to supervise better during the cost of living crisis.

The link between financial literacy and poverty is strong. Nearly half of those with financial problems admit that poor money management skills are a key factor in their plight.

‘It is screaming out to me that we just need to get on and do this,’ Regnier says.

The banks themselves have been making plenty of money. Santander UK’s first-quarter profits rose 11 per cent to £547 million, but Regnier denies any profiteering.

‘The sector as a whole is having a good year,’ he says. ‘But it looks as though bank rates have peaked and 2024 might be a bit more challenging. The UK banking sector has struggled to deliver returns in line with the cost of capital.’

Santander is not forecasting a major fall in house prices, despite a drop-off in mortgage lending.

A typical borrower whose home loan is coming out of a fixed rate or discount will have to pay an extra £250 a month, he says. But Regnier argues that the situation now is nowhere near as bad as during the late 1980s after the global financial crisis triggered a wave of negative equity, repossessions and borrowers handing back their keys.

‘The big difference now is that people have more equity in their homes,’ he says. ‘So the level of stress for many isn’t as bad.’ Fewer than 2.5 per cent of mortgage customers are currently in arrears.

Santander UK’s Spanish parent has toyed with the idea of floating off the British business. Might that come back on the agenda?

‘One reason Santander is in the UK is that it wanted a presence in the biggest financial services in Europe. But if the bank wanted to sell in the UK, I might be the last to know,’ he says with a smile.

Some links in this article may be affiliate links. If you click on them we may earn a small commission. That helps us fund This Is Money, and keep it free to use. We do not write articles to encourage products. We do not allow any commercial relationship to affect our editorial independence.

Q2 2024 Earnings Call Transcript")