BraunS

The cruise line sector has seen a strong and multi-year recovery after the COVID-19 pandemic decimated the industry in 2020 and in 2021. Royal Caribbean (NYSE:RCL) has also seen a strong valuation recovery in 2023, reflecting positive fundamentals as well as a raised guidance for the current fiscal year. Since a major re-rating has already taken place and shares are not as cheap as they were earlier last year, I believe that shares of Royal Caribbean Group are about fairly valued and I see limited upside in FY 2024!

Previous rating

I recommend Royal Caribbean Group in August — The Rally May Continue — after the company raised its earnings forecast for FY 2023 in light of a positive booking situation relating to both passenger volumes and trip pricing. Royal Caribbean Group is benefiting from robust demand for its ocean-going cruises and the company saw a massive rebound in its revenue picture in the first half of the year. However, optimism about the cruise line industry is now very high which makes me think that this may be great time to sell into the strength.

Strong revenue growth, return to positive operating income, optimistic outlook for FY 2024

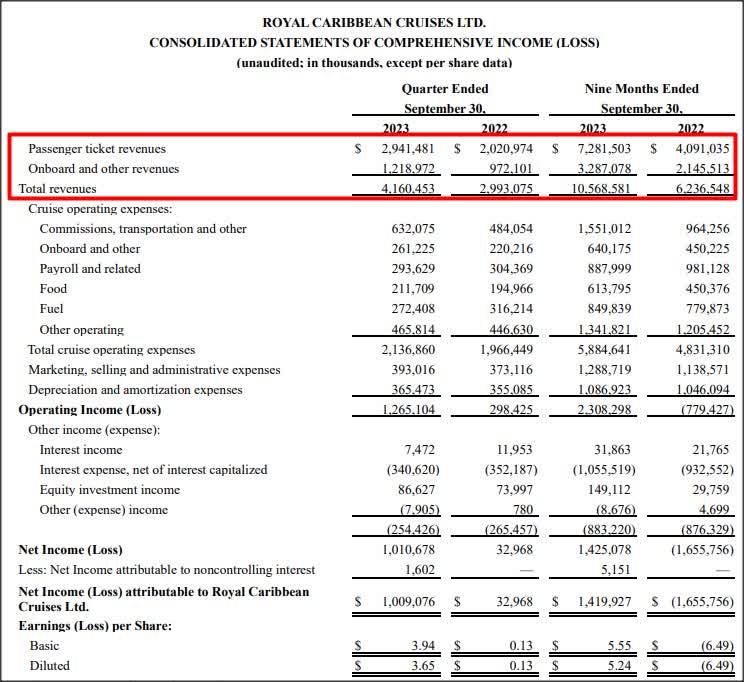

The cruise line industry has seen a strong revenue recovery on the back of returning passengers in the last two years. In the first nine months of FY 2024, Royal Caribbean Group has seen a massive 69% increase in its revenues and, for the same time period, also reported a return to positive operating income. In the breakdown of the cruise line company’s operating revenues, we can see that both passenger ticket sales (which were up 78% Y/Y) and onboard revenues (+53% Y/Y) saw strong growth as passengers opened their wallets and turned things around for Royal Caribbean Cruises in a truly epic way. What was likely the biggest achievement of FY 2023 was that the company returned to positive operating income after years of major losses that hurt RCL’s equity value.

RCL

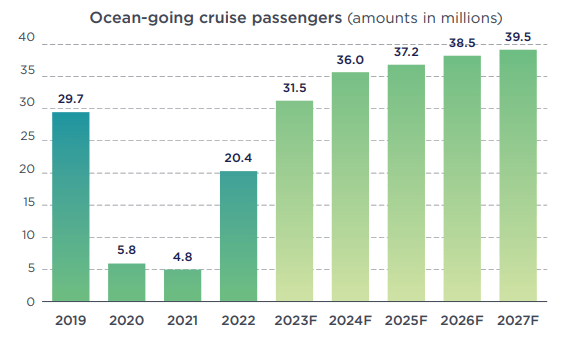

The passenger numbers for ocean-going cruises dropped like a rock in 2020 as the COVID-19 pandemic caused a major panic in the industry as passengers rushed to cancel their cruises. However, the picture drastically improved in 2022 as passengers returned in large numbers and, according to projections by the Cruise Lines International Association (Source), an industry advocacy group, 36M passengers are projected to participate in some kind of ocean-going cruise this year. Therefore, 2024 would be the second year in a row in which total passenger numbers could exceed the pre-pandemic record of 29.7M passengers.

Cruise Lines International Association

The booking situation at the cruise line company has turned out to be increasingly robust, according to RCL’s Q3’23 update. These trends are driven, at least in part, by a desire of passengers to make up for missed holidays during the pandemic… a phenomenon commonly explained as “revenge travel.” RCL has said that it Q3’23 booking demand exceeded 2019-levels which is consistent with the company’s revenue trend as well as with CLIA projections for record passengers in FY 2023. As a result, Royal Caribbean Group raised its adjusted earnings per-share forecast to $6.58-6.63 in the third-quarter, suggesting that FY 2023 will indeed be a record year for the cruise line company.

Royal Caribbean Group’s valuation relative to cruise line rivals

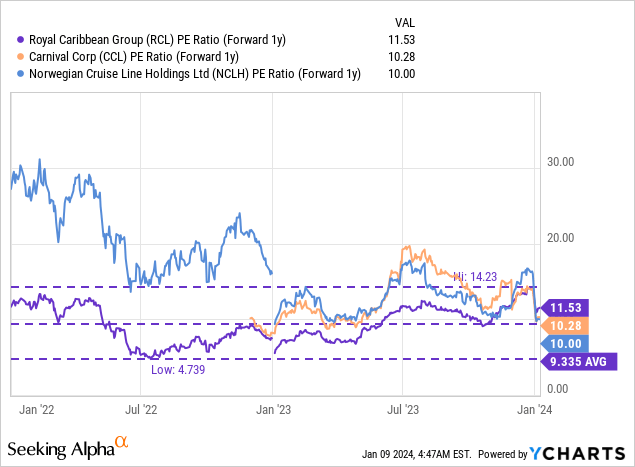

Shares of Royal Caribbean Group are trading at a price-to-earnings ratio of 11.5X, based off of a consensus EPS estimate of $10.77. Royal Caribbean Group’s P/E ratio is 24% above its 1-year average P/E ratio of 9.34X. Both Carnival Corp. (CCL) and Norwegian Cruise Line Holdings (NCLH) are cheaper than Royal Caribbean Group with P/E ratios of 10.3X and 10.0X. A P/E ratio of 10-11X indicates to me that the sector, which is very cyclical and dependent on strong consumer spending, is likely fairly valued at the current time. Given the strong increase in RCL’s share price in 2023, I believe this may not be the worst time to consider taking some profits.

Risks with RCL

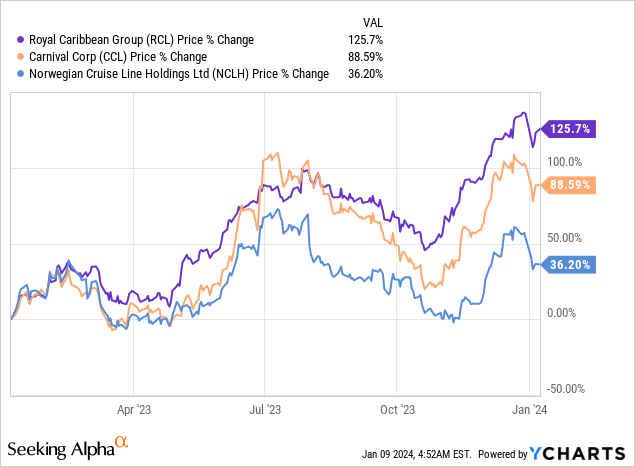

While the outlook is leaning positive for the industry as a whole, cruise line companies more broadly posted record results throughout FY 2023 as a major passenger return to cruise ships has boosted the booking situation quite dramatically. Royal Caribbean Group’s shares have soared 126% in the last year which indicates to me that the risk profile has actually deteriorated.

There are risks such as a potential downturn in the economy which could hurt the spending-sensitive cruise line industry. A new pandemic is also a key risk. Attacks on container ships in the Red Sea also pose a risk is shipping more broadly is put at risk.

Final thoughts

FY 2024 looks set to be a good year for the cruise line industry, according to passenger volume projections that are made by the industry advocacy group CLIA. Royal Caribbean Group has already seen a strong revenue recovery in 2023 which I believe is fully reflected in the company’s share price. As a result, it is my opinion that the massive re-rating that has taken place for shares of Royal Caribbean Group in 2023 is translating to a more unattractive risk profile. While FY 2024 is projected to yield a new record in terms of cruise line passengers, I believe it is time to sell into the strength!

Q2 2024 Earnings Call Transcript")