J. Vespa/WireImage via Getty Images

Intro

We wrote about Rocky Brands, Inc. (NASDAQ:RCKY) back in November 2020 when we assessed whether the momentum shares were undergoing at the time could continue to the upside. At the time, Rocky’s customers in the wholesale segment were coming out of lockdown and opening up once more, which resulted in significant sales and earnings beats for Rocky’s fiscal third quarter. This led to a strong rally in Rocky shares post the earnings announcement. Nevertheless, we remained cautious concerning our rating (Hold) due to the possibility of renewed lockdowns at the time, overhead resistance on the technical chart as well as an overextended valuation.

Fast forward just over three years and our cautious stance was justified in that shares of Rocky have returned a negative 8%+ in this period even when we included dividend distributions from the company. This negative 8%+ return has ended up being a sizable opportunity cost as the S&P has managed to return over 40% over the same period.

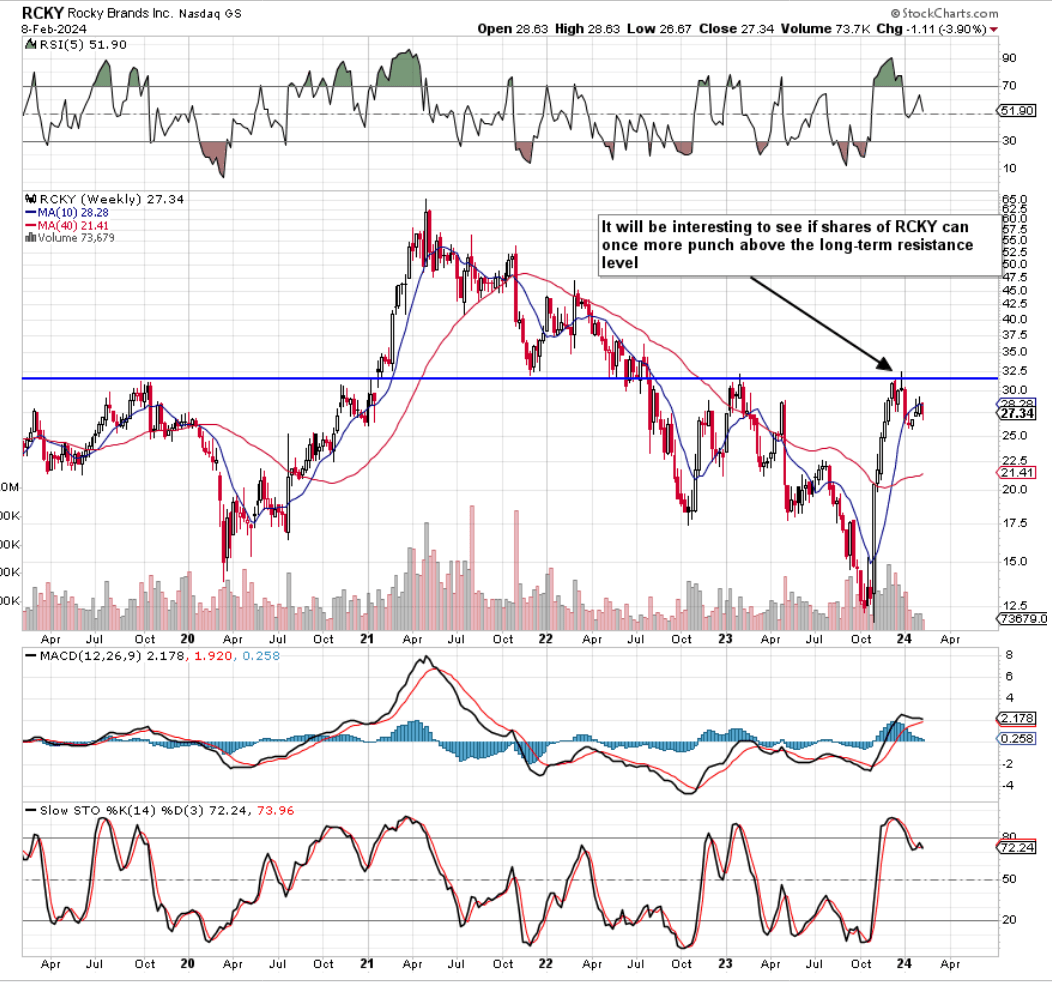

Ironically, as we see from Rocky’s intermediate technical chart, shares did manage to break out above long-term resistance in early 2021 but have since come right back down to lose this key support level. The fact that the momentum of the blistering rally Rocky underwent over the past 3+ months was still not sufficient to register a bullish breakout has led us to maintain our ‘Hold’ rating in the stock for now. Here are some fundamental reasons that explain our reasoning.

Rocky Brands Technical Chart (Stockcharts.com)

Income Statement Concerns

Although Rocky announced much-improved earnings and sales numbers in its recent third quarter of fiscal 2023 ($125.61 million on earnings of $1.09 per share), we recommend that investors focus on long-term trends. Rocky’s trailing 12-month GAAP earnings of $10.2 million, for example, only amounts to roughly half of the company’s bottom line profits (GAAP earnings of $20.5 million in fiscal 2022). Furthermore, when one scours through recent quarterly reports, it is evident that there were no ‘one-item’ impairment charges that caused the significant drop in earnings thus far this year. The CEO put the rough start to the year down to a tough macro-environment as well as elevated inventory levels which restricted Rocky from turning over its capital quickly.

Suffice it to say, although trailing gross margins come in above average for Rocky at 39%+, the company’s sluggish sales growth is the primary culprit for trailing net profit margin having slumped to a mere 2.15%. To give some context, Rocky’s trailing 12-month revenues of $474.8 million come in 23% or $140 million less than the company’s top-line number in fiscal 2022 ($615.5 million). No matter how well management can improve operational efficiencies or increase prices on the front end, this level of revenue decline is always bound to hurt bottom-line profitability over time. Based on recent trends as we head into the fourth quarter earnings announcement due later this month, the CFO has guided $470 million (23.6% expected year-over-year top-line decline) in top-line sales for the fiscal year.

Inventory Overhang

Rocky’s ‘Wholesale’ segment made up almost $100 million of the recent third quarter’s top-line take of $125.6 million, making it the biggest segment in the company by far. Although Rocky continues to bring down its inventory (where the latest year-ending target has fallen to $175 million) the company’s large debt load & subdued profitability may imply that shareholders may not be getting full value for company inventory over time. Let me explain.

If we go through some of Rocky’s ‘work’ brands, we see that lower prices on specific ‘Georgia’ styles helped in increasing forward-looking demand. Management has talked up in recent times how significant costs have been saved and how these savings have been passed on to customers in certain brands and styles. The problem, however, is that when one is trying to nurse a debt load of almost $214 million (with trailing GAAP earnings of $10+ million), inventory is usually the first port of call to start bringing in some badly needed cash. Suffice it to say, when talking about cost efficiencies that can be passed on to the customers through the likes of the Georgia brand or the ‘Durango brand in the Western business, investors need to consider the relationship between sustained inventory reduction and preserving profitability. My opinion is that cash collection efforts at present outweigh the company’s desire to grow margins, which is why Rocky’s profitability numbers should continue to be watched closely, especially in an environment of negative top-line growth.

Consensus Revenue Revisions Trend

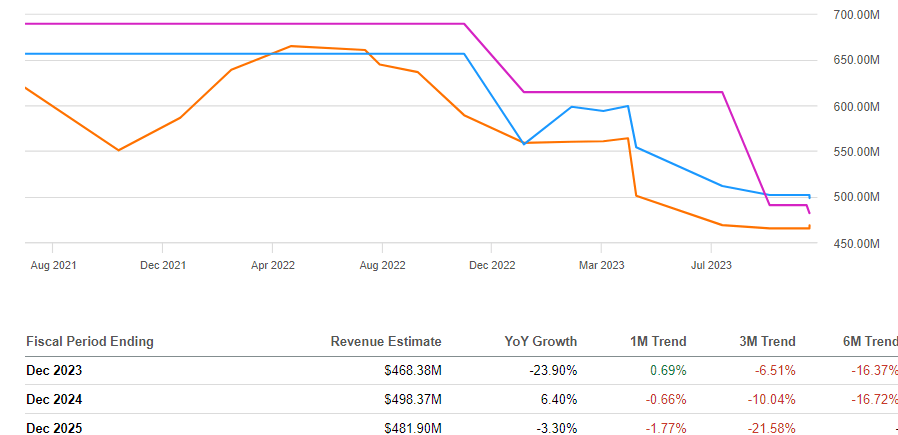

As we see below, Rocky is expected to bounce back next year and post 6%+ top-line growth. However, top-line revisions have not been encouraging in recent months plus the $498+ million current fiscal 2024 expectation still comes in well below Rocky’s top-line sales numbers for both fiscal 2021 as well as fiscal 2022. This is why we mentioned earlier that investors should continue to focus on long-term trends in this play.

Rocky Brands Consensus Revenue Revisions Trend (Seeking Alpha)

Conclusion

To sum up, we are maintaining our ‘Hold’ rating on Rocky Brands due to subdued bottom-line profitability trends, a large inventory overhang, and forward-looking revenue revision trends. Although Rocky has been making inroads into its high debt load, investors will be hoping that this is not being done at the detriment of getting full price for the company’s inventory. Let’s see what Q4 brings. We look forward to continued coverage.

Q2 2024 Earnings Call Transcript")