JJ Gouin/iStock via Getty Images

This is a follow up to an earlier article written in 2018 that received a lot of attention called The Risk Of The Roth IRA Revolution II, which you can find by clicking this link. The previous article dealt with a couple having a starting Social Security of $40,000 and an after tax income need of $100,000. At the lower levels studied in the previous article, unless you are in the 12% or lower tax bracket when making a Roth IRA contribution or a conversion, it turned out that something less than 3% Roth would keep you out of the higher marginal tax rate under the conditions given. In this article I will suggest by example why the size of your Social Security may be a large contributing factor in this analysis. If you are concerned your spendable money in retirement is marginal, you certainly want to try and maximize it. Like most of my articles, first we must understand what the optimal condition is before we can decide whether it needs fixing.

Be sure to realize these examples do not consider the effect of state income tax, or the effect of increased Medicare premiums, or other nuances that are unique to your own situation.

The previous article had no need to study the non-linearity of the taxation of Social Security, since Social Security was taxed at its maximum 85% throughout the study. Once again the intent here is to give you food for thought as each person’s retirement income can have multiple sources that are taxed differently. I will discuss this later in the summary.

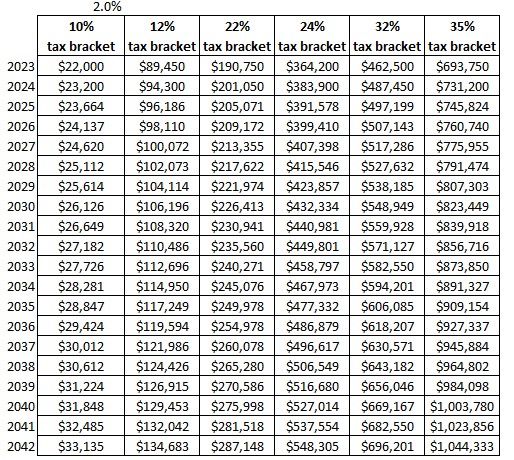

I will however add some techniques that are rarely used even in published works of this type, but I believe are important to the overall view. One is inflation adjustment of the Social Security payment as well as the income need by the couple. Secondly, and even more important is the inflation adjustment of the tax brackets and Standard Deduction. This was all part of the previous article I reference above. In that article I used a 1.5% inflation factor based on the historical data available at the time, but in this article I have chosen to use 2%, which is more in-line with the long-term average. The new standard deduction levels of 2023 will be inflated by $100 per year starting in 2025 as another estimate of what could possibly be expected based on past history. For my tax table I will use both 2023 and 2024 actual numbers since they are known at this time. Once again past history is no guarantee but it is important to at least consider the inflation factor.

Reviewing the Ground Rules

First some definitions and abbreviations are in order:

I will use the term Roth to indicate any number of what are typically tax-advantaged retirement accounts funded with after-tax dollars for which you can withdraw all contributions and earnings tax-free later. These come in many different forms such as the Roth IRA, Roth 401(k), Roth 403(b), Roth 457(b), and others. I will use the term TIRA to indicate any number of tax-advantaged retirement accounts funded with pre-tax dollars for which all withdraws are treated as ordinary income in the year of the withdrawal. You could find many types of these such as Traditional IRA, Traditional 401(k), 403(b), SEP-IRA, 457(b), SIMPLE IRA, and others. It should be noted that it is possible to have a mix of after-tax and pre-tax dollars in most of these accounts, but when I use the term TIRA from now on, I will be considering these accounts holding only pre-tax dollars in them. This article is mainly concerned with contrasting the Roth and TIRA to determine what techniques can be used to maximize your income during retirement. If you are putting money in a taxable account consider that money more like a Roth, as it is after-tax money, with at least a lower tax bracket on any long term capital gains and qualified dividends received in a given year. Let’s review the characteristics of the two accounts types.

Roth:

Tax deferral on all earnings inside the Roth if you follow IRS guidelines. All contents of the Roth become tax free when a Roth IRA has been held at least 5 years (at any age) and the owner attains at least age 59 ½. Note, both of these conditions must be met for the Roth withdrawal to be deemed “qualified.” Tax free withdrawal of your contributions at any time or age from a Roth IRA. A note on this as it applies to employer sponsored plans is that you should check with your plan administrator as each plan has their own set of rules as to when withdrawals are allowed. Tax planning flexibility – Since there are no forced withdrawals by age 73, you have more tax-planning flexibility during retirement. If a Roth IRA owner dies, certain of the minimum distribution rules that apply to traditional IRAs will apply to the Roth.

TIRA:

Tax deferral on contributions during working years will lower your taxable income while working and can increase some tax-credits. Increasing some tax-credits could actually allow you to save more. The TIRA RMD year depends on the year of birth

|

If Birthday falls |

Age of first RMD |

First RMD year |

Req’d Begin Date |

|

< 7/1/1949 |

70 1/2 |

<2020 |

=< 4/1 of 2020 |

|

7/1/49 – 12/31/50 |

72 |

2021 – 2022 |

4/1 of 2022/2023 |

|

1/1/51 – 12/31/59 |

73 |

2024 -2032 |

4/1 of 2025-2033 |

|

>= 1960 |

75 |

>=2035 |

4/1 >=2036 |

Note the first RMD year can be determined by adding the above RMD age to the birth year. So one born in 1958 will have their first RMD year in 1958 + 73 = 2031 and a RBD (required begin date) of 4/1/2032

Inherited IRAs have a complete set of RMD tables and rules which will not be discussed here and are discussed in the link below concerning the Secure Act and Secure Act 2.0 recently passed by Congress. Some other nuances of the Secure Act 1.0 & 2.0 can be found here:

There are many other nuances to the above two types of accounts and even within different types of Roth or TIRA accounts, most of which can be found in the IRS publication 590, which has now been split into two parts – pub 590-A (contributions) and pub 590-B (distributions).

This article will cover this subject in a similar manner as my previous article from 2018. I will study 3 different couples, the TIRAs, the Roths, and the Optimas, all of which decided to emphasize their Roth and TIRA contributions differently.

General Assumptions

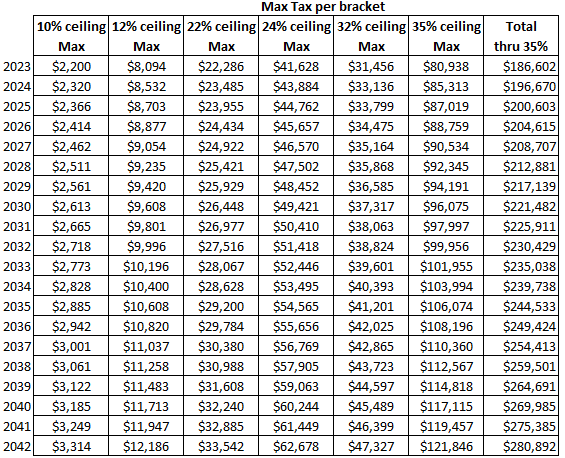

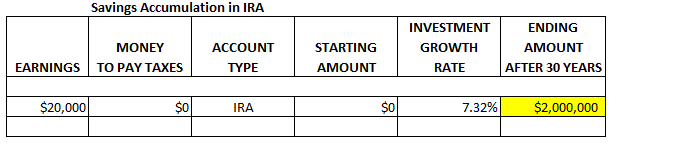

The results are for a married filing joint couple, MFJ, both age 70 in December of 2023, which is the starting year for this analysis. The result of this is their first RMD will be paid in 2026 on the starting TIRA balance at the end of 2025. The TIRA or Roth withdrawals required for the year are withdrawn at the start of the year on January 1st. The couple has a combined Social Security income of $80,000 per year, which will be inflation adjusted at 2.0% per year. The couple’s total income need starts at $160,000 per year and will also be inflation adjusted at 2% per year for the 20 years of this study. Each couple has saved $20,000 per year for 30 years, and gotten an annualized return on those investments of about 7.32%, which translates to a pre-tax TIRA balance of $2 million or split adjusted amounts with varying dollars of after-tax Roth money as detailed in the case outlines below. The annualized growth rate of their TIRA and Roth investments will be 3% in all cases. The tax brackets used to calculate their tax will also be inflation adjusted at a 2% rate. Tax year 2023 will be the starting point for the tax tables. In the examples studied it turns out that Social Security will not be taxed in years where the supplemental funds are 100% Roth, since the couple has no other supplemental income. Each couple takes the standard deduction which for them starts at $30,700 in 2023, $32,300 in 2024, and increases at $100 per year thereafter. Three tax rates for Roth contributions will be studied to contrast how your working tax rate later affects your spendable income when a Roth account is involved.

The three couples which decided to invest in Roth accounts will be studied under three different cases in which they were able to put their earnings into the Roth at the below rates:

Money went into the Roth while working at an average of 12%. Money went into the Roth while working at an average of 20.6%. Money went into the Roth while working at an average of 25%.

It turns out that the above 20.6% is the “breakeven” tax rate where 100% Roth will equal 100% TIRA.

In each of the cases below the families have a different idea of how much money should be devoted to the Roth account. The TIRA’s true to their namesake put all their savings, pre-tax, into the TIRA, while the Roth’s do just the opposite and put all their savings, after-tax, into the Roth. The Optima’s use the spreadsheet developed here to try and calculate the most “bang” for their earnings dollar. They do a very good job of this calculation as we shall see below.

The Setup

The following tax tables will be used:

my spreadsheet

my spreadsheet

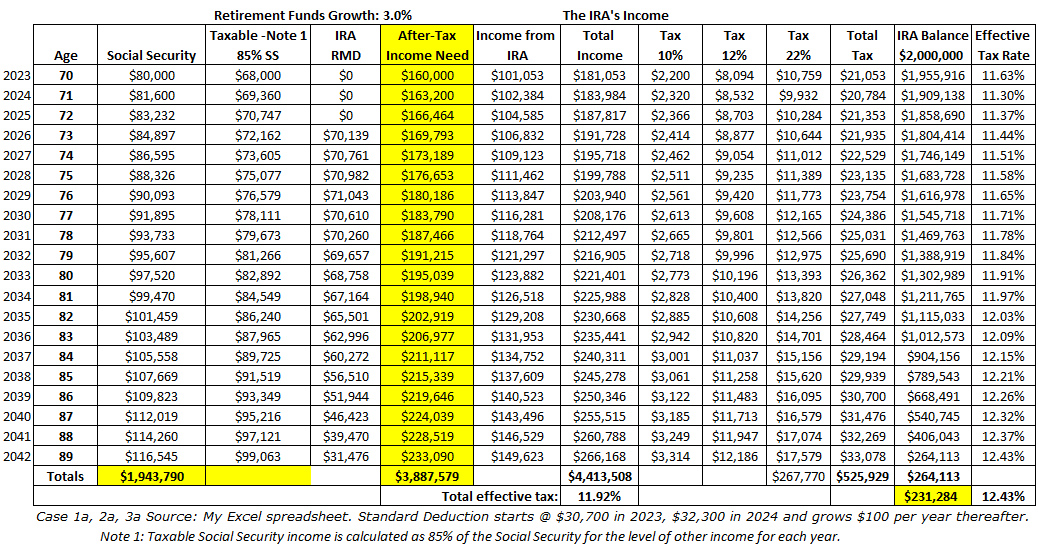

Results for the TIRAs

my spreadsheet

my spreadsheet

As you might have guessed, the working tax rate does not matter to the TIRAs as their retirement will always end with effectively $231,284 of after-tax money, or $264,113 of pre-tax money, left to spend after 20 years.

Results for the Roths

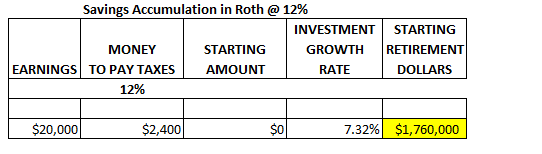

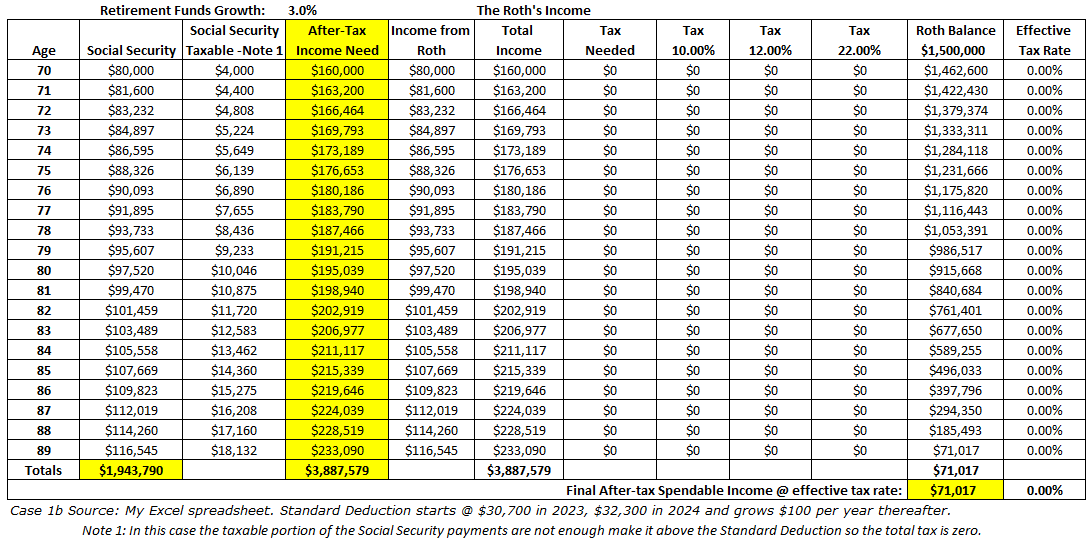

First let us look at results when the Roths keep their average Roth tax burden while working at 12%.

my spreadsheet

my spreadsheet

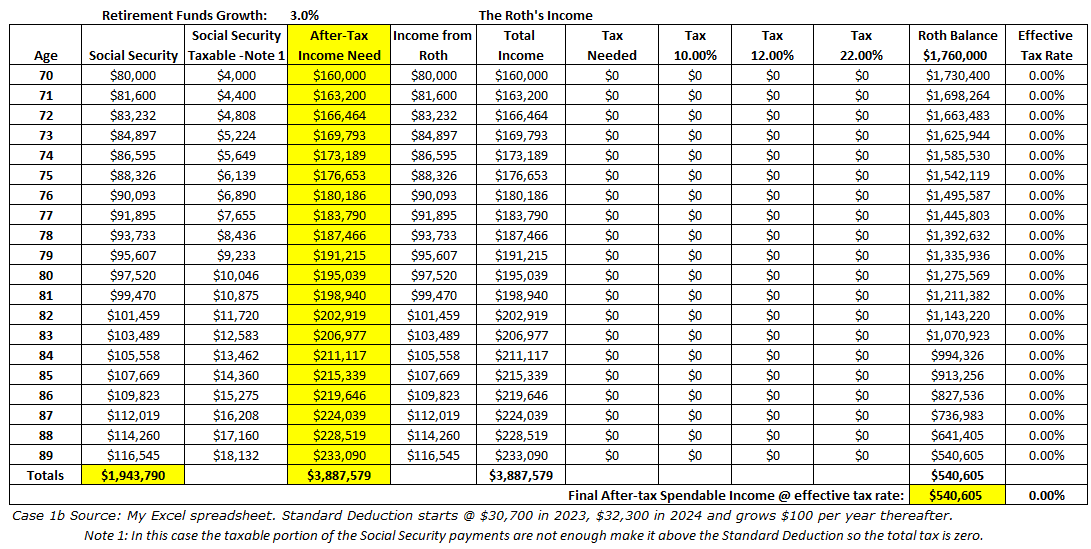

In the above case an interesting thing happens because the couple has no other taxable income such as a pension or even taxable gains from a taxable account and that is that the Social Security taxable income does not become greater than the Standard Deduction so no tax is generated. The Roth balance starts at $1,760,000 after the $240k tax is subtracted from the $2 million of gross savings and the ending balance after 20 years is $540,605 for a total advantage over the 100% TIRA account of $309,321.

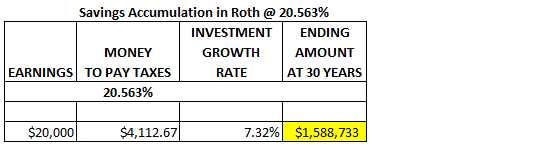

Second let us look at how much tax could be paid on the 100% Roth scenario for it to exactly equal the results of the 100% TIRA withdraw, which is an ending value of $231,284. From some trial and error this result turns out to be a tax rate on Roth contributions (or Roth conversions) of 20.563%. Meaning that if the Roth conversion rate is above that it loses to the pure 100% TIRA scenario.

my spreadsheet

In this case the 100% Roth scenario ends with the same after-tax income as the 100% TIRA scenario.

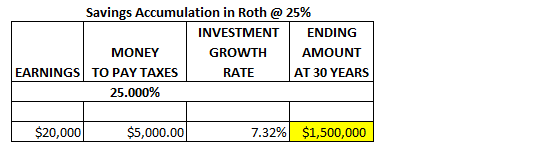

Finally let us look at results when the Roths keep their average Roth tax burden while working at 25%.

my spreadsheet

my spreadsheet

As can be seen from the above, the lack of tax diversity in their savings has caused them a serious setback in their retirement cash flow as they will run out of savings at age 90 and are therefore forced to live only on their Social Security income.

Results for the Optimas

The Optimas have figured out from reading other articles on Seeking Alpha that if you want to have more money in retirement it is best to save your Roth money for expenses that push you into a higher tax bracket in retirement. To be more specific, spend Roth money in retirement in a higher marginal tax bracket than when your money went into the Roth in the first place. For example if your average working Roth marginal tax rate is 21% then use that money to supplement your income when other methods would put you in the 22% tax bracket or higher.

First let us look at results when the Optimas keep their average Roth tax burden while working at 12%. In this case the optimal TIRA size is just enough money to use up the zero tax bracket. They are extremely lucky by estimating this is going to be about a 10% allocation to their TIRA account, and here are the results:

my spreadsheet

my spreadsheet

In this case most of the TIRA money is spent tax free and this leaves a total of almost $582,000 of after-tax dollars, mostly in the Roth. It is better than the 100% Roth account by about $41,000, due to the fact that most of the TIRA money was spent tax-free. That is something to be aware of if you are in that situation and have a very low tax base of Roth contributions.

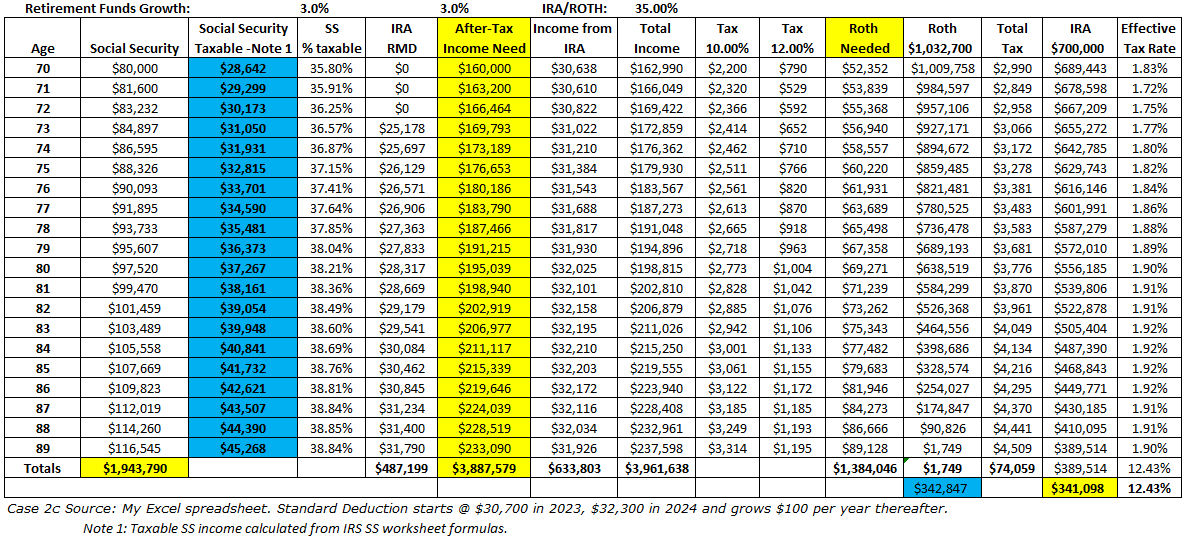

Second let us look at results when the Optimas keep their average Roth tax burden while working at 20.563%. In this case the optimal TIRA size is just enough money to keep them out of the 22% tax bracket. They are extremely lucky by estimating this is going to be about a 65% allocation to their Roth account, and here are the results:

my spreadsheet

my spreadsheet

In this case the goal is to keep from spending TIRA above the 20.56% tax cost of the Roth money which for this case turns out to be a Roth allocation of 65%. This turn out to be almost $112k better than either 100% or 0% Roth.

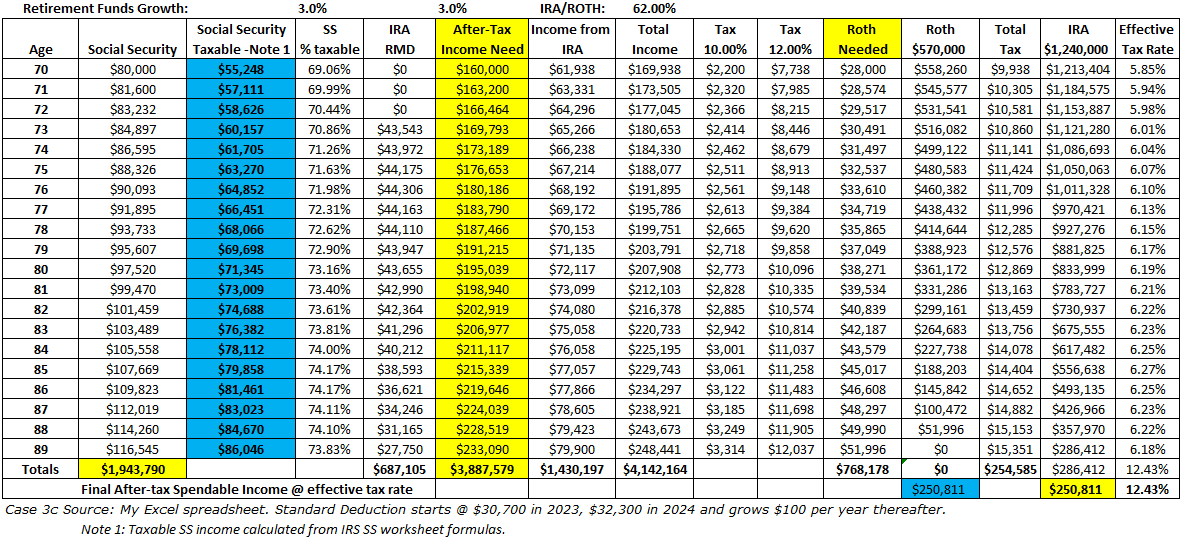

Finally, let us look at results when the Optimas keep their average Roth tax burden while working at 25%. In this case the astute reader might think that there is really no time frame when the retirement marginal tax rate is above 25%, since the largest tax bracket used even for 100% TIRA was 22%. That is not entirely true since for these higher levels of TIRA spending the contribution of taxable SS comes into play. In the 12% bracket for example the total tax is 12% + (.85*12%) [for SS] or 22.2%. In the same way the 22% bracket is actually 22% + 18.7% =40.7%, until SS is fully taxed. Our goal then is to just keep the tax on the spending from reaching the 22% bracket by using Roth money in that situation.

my spreadsheet

my spreadsheet

In the above case what is verified is that the Optimas had $19,527 more than if they had left 100% of their savings in the TIRA account, and 38% of their savings into the Roth was the sweet spot.

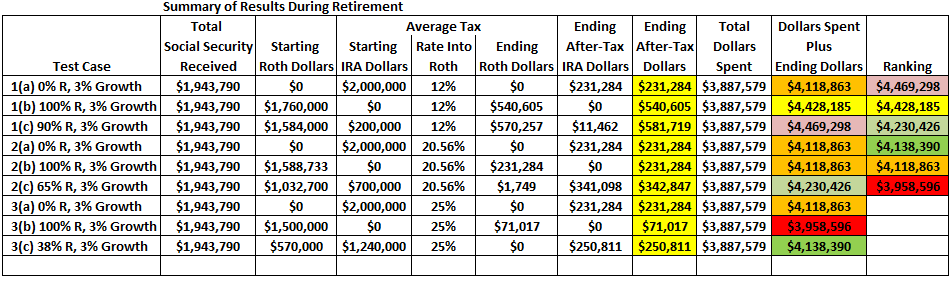

Tabulation of Results

my spreadsheet

First place goes to the Optimas, who managed to get 90% of their savings into their Roth account and 10% into the TIRA with an average 12% tax base. $41,113 behind them were the Roths, that put a 100% allocation into their Roth at a 12% tax base and then the Optimas that put a 65% allocation towards the Roth at a 20.56% tax base.

The Optimas with 38% Roth from the 25% tax base come in fourth. Those that felt putting 100% of their money in a Roth at 25% finished this race in last place falling $510,702 short of the Optimas who were able to save their Roth funds at an average 12% tax rate.

Summary

As I have often said, if you can save Roth money at 12% or lower it is pretty hard for you to go wrong. As in the previous article the top 2 spots went to the use of money saved in the 12% bracket, mostly in the Roth account.

What is going on with this higher level of Social Security is that at some points the taxable SS is coming into contact with the 22% tax bracket causing a marginal tax of 40.7% to occur over a narrow window. This window is defined by these two endpoints for the MFJ couple in 2023:

The starting point for the 40.7% bump is defined by the equation:

$81,918.92 – .22973*SS

The ending point for the 40.7% bump is defined by the equation:

$36,941 + .5*SS (This is the point above which SS in no longer taxed)

The lower bound of SS for which the 40.7% bump does not apply is where a) and b) above are equal. This equation (for 2023) is (81,918.92 – 36,941)/.72973 which equals $61,636.

So for our couple with a starting SS of $80,000, the bump starts at $63,541 of ordinary income and continues to $76,941.

In the couples second year if their SS was $81,600, the bump starts at $66,661 and continues to $77,741.

Of special note here is the top of the bump always goes up by 50% of the SS annual increase ($800 in above case), while the bottom goes up by a number related to the increase in the standard deduction and top of the 12% bracket (in this case the increase on the low end was $3120). Meaning that as time goes on, with no changes to the formula calculating SS the 40.7% bump becomes narrower, lowering the need to address the issue. This also shows up by the raising of the point where SS is affected by the 40.7% bump. In the last 3 years this point has changed as follows for a MFJ couple:

2022 – $55,784

2023 – $61,636

2024 – $66,414

So, below the numbers of SS income above, the MFJ couple won’t be subject to the 40.7% bump.

One final note about adding a taxable account to the mix. It carries the tax structure of the Roth with it, meaning that it is already after-tax savings and it will create a SS taxable income to the same extent as the ordinary income that we have been using in this article.

Assuming the taxable account generates only qualified dividend income or long term capital gains, the qualified income will be taxed only to the extent that your total taxable income goes above the maximum taxable income of $89,250 in 2023 or $94,050 in 2024.

So for example with a couple with $80k of Social Security and $80k of ordinary income from the TIRA, the tax on that combination in 2023 would be $16,421. If you take the same couple with $80k Social Security and pair that up with $80k of qualified dividends or LTCG, then the result would be $8,247 of tax.

Conclusion

Even though everyone’s tax situation is different, I would hope one take-away from this article is that the higher 40.7% tax bracket is first only a problem when your Social Security payments reach the higher limits of the scale. In 2023 that SS payment level was $61,636 for the couple above and as a reference to a single taxpayer this level is around $24k.

As time moves on with no changes to the way SS is taxed the amount of income that gets taxed at the 40.7% level goes down. This is not something that is taken into account by most software programs. In fact a recent article in the AAII journal completely neglected this issue, while most other analysis of the 40.7% bump does not even suggest that it changes year to year, or the formulas are inaccurate because they are not based on the changing tax brackets and standard deviations.

While RMDs can raise your taxable income and your tax rate in retirement they should not be something that is feared to extremes. In an article I wrote entitled Surviving the Tax Bite of Retirement, I pointed out that over the previous number of years the personal exemption, standard deduction, and the top of each of the tax rate bracket have grown by around 2% per year. Lower tax brackets today still improve the odds of you having a lower tax bracket in retirement, compared to while you were working. Hopefully you have learned that this favors the TIRA owner and the results are not insignificant, except for the few with higher SS incomes as suggested above.

In my volunteer work helping people with their taxes each season there are always cases where having some of their retirement in a tax-deferred TIRA could have resulted in some tax-free withdrawals from that TIRA, due to their low income level. For others the converse is also often true – that with at least a small Roth account it would have been possible to lower how much of their retirement savings goes to taxes. It is never a bad idea, in my opinion, to have both Roth and TIRA funds going into retirement. In my case I was able within the first couple of my retirement years to use some of that Roth to keep my tax rates reasonable while I paid off a sizable mortgage.

Of Notable Mention

For more detailed information on these subjects covered I suggest reading at least a couple of times the two IRS publications mentioned at the outset. Understanding the rules can avoid costly mistakes on the road to retirement as well as later when you are in retirement. I have also written an Instablog article titled, Roth Vs. Non Roth (401k, 403b, 457, Etc) & The Time Value Of Money which adds a casino example to the mix which you may find interesting.

Once again I also want to shout out a special thanks to Bruce Miller, who made my job much easier by providing a tax calculator for the new tax law going forward in 2018 as well as a Social Security tax calculator.

All tax calculations were started from a base of the new 2023 tax law and as I outline, they were inflation adjusted at 2% going forward from there.

This study is only as good as the data presented from the sources mentioned in the article, my own calculations, and my ability to apply them. While I have checked results multiple times, I make no further claims and apologize to all if I have mis-represented any of the facts or made any calculation errors.

The information provided here is for educational purposes only. It is not intended to replace your own due diligence or professional financial or tax advice.

Q2 2024 Earnings Call Transcript")