sommart

Richmond Mutual Bancorporation (NASDAQ:RMBI) investment case relies highly on its above-average dividend yield compared to other regional banks, while its growth prospects and business diversification could be better.

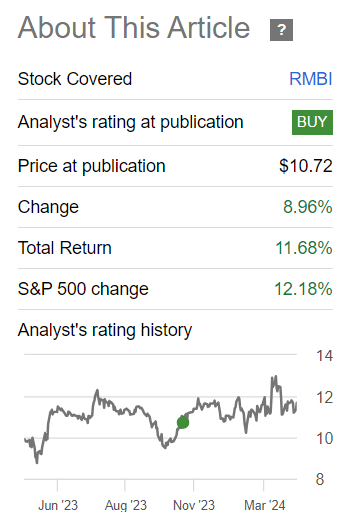

I analyzed Richmond Mutual Bancorporation back in November and concluded that its relatively high-dividend yield was the most attractive feature of its investment case. Since then, its shares are up by close to 12%, including dividends, in-line with the market performance during the same period.

Article performance (Seeking Alpha)

In this article, I update its most recent financial performance and investment case, to see if it remains an attractive income pick or not.

Earnings Analysis

Richmond Mutual Bancorporation (Richmond) is a bank based in the state of Indiana, having a current market value of about $128 million, being therefore quite small by this measure. At the end of 2023, its total assets amounted to $1.46 billion, and its deposits were slightly above $1 billion.

Its core business is quite simple being focused on deposit gathering and lending, providing full banking services in Indiana and Ohio. Its loan book can be considered to be quite conservative, even though it has significant exposure to real estate. However, most of its loans are secured, backed by commercial and multi-family properties, thus the risk of potential credit losses is somewhat low.

Beyond traditional lending activities, Richmond also provides trust and wealth management services, even though the revenue coming from these operations are somewhat low.

Not surprisingly, given its business profile geared to commercial and retail banking, the vast majority of its revenue comes from net interest income (NII), which represents the difference between interest earned from lending and interest paid on deposits and other funding sources.

While usually a rising interest rate environment is good for banks with high reliance on NII, this was not the case for Richmond. Indeed, during 2023, Richmond’s total revenues amounted to $42 million, of which 89% were generated by NII, thus it would be expected that NII would have increased during the last year.

However, due to the banking turmoil in the regional banking sector, Richmond’s cost of deposits increased quite significantly, offsetting gains from higher lending margins. This led to an unexpected decline in NII during 2023, to some $37.6 million (vs. $41.6 million in the previous year). This is a negative outcome showing that Richmond’s leverage to rates was not great during the past few quarters, mainly due to external factors. This is also visible in its net interest margin, which was 2.78% in 2023, compared to 3.36% in the previous year.

Due to its business profile, its high reliance on NII is not expected to change meaningfully over the next few years, but its poor top-line performance last year clearly shows the benefit of having a more diversified revenue profile and, in my opinion, Richmond should push its growth strategy toward non-interest revenue sources, namely through payment services or offering a broader product suite, including mutual funds or other types of financial products.

While the company has to some extent acknowledged this need to diversify its business, by forming an insurance company in 2022, it’s not showing great signs of success given that total non-interest income declined slightly in 2023 to $4.6 million.

Regarding expenses, despite the inflationary environment and pressure on costs, Richmond reported operating expenses of $30.7 million, representing an increase of only 2% from the previous year, which is a good outcome compared to peers. Its efficiency, measured by the cost-to-income ratio, was 72%, which is a ratio that is above the average of the banking sector. On the other hand, due to its small size, it’s difficult for Richmond to have much better efficiency, as regulatory or technology costs have a higher impact on its cost structure when compared to larger banks.

Regarding its credit quality, it remained at very good levels given that its provisions for loan losses were only $0.5 million, which is basically near zero, being quite stable compared to the previous year. This shows that despite the negative impact of higher interest rates, its good underwriting criteria and conservative balance sheet have protected Richmond’s credit risk, which is a very positive outcome during a challenging macroeconomic environment.

Given this backdrop, its bottom-line was pressured by lower revenues and higher costs, leading to a net income of $9.5 million in 2023, a decline of 27% YoY, from $13 million in the previous year. Its profitability level, measured by the return on equity (ROE) ratio, was 7.4% (vs. 8.8% in 2022), which is not impressive within the banking sector.

Going forward, Richmond’s business profile is not expected to change much, even though it’s pushing for growth in consumer lending or insurance, which should gradually lead to higher revenue coming from non-interest income, but NII is expected to remain its most important revenue source for the foreseeable future.

In the near term, Richmond is likely to continue to benefit to some extent by high rates in the asset side, while reducing somewhat its cost of deposits is key to higher revenues in the coming quarters. As confidence levels for regional banks have increased in recent months, Richmond may be able to revise its rates on time deposits downward, which would be a boost for its NII and earnings.

Regarding its capitalization, Richmond’s CET1 ratio was 12.85% at the end of 2023, which is a good capital position and above the average of its peers. Moreover, it’s also way above its capital requirement of only 6.5%, showing that Richmond has a great excess capital position and can provide an attractive shareholder remuneration policy ahead.

Its current quarterly dividend is $0.14 per share, or $0.56 annually, which represented an increase of 40% compared to its total dividends distributed in 2022. Despite this increase, its dividend payout ratio was only 61%, which is a relatively low level of distribution considering its stable and low-risk business profile. This shows that Richmond’s management is clearly committed to distribute a good part of excess capital to shareholders, a strategy that is not expected to change in the future.

Its capital return strategy has been based on both share buybacks and dividends, something that is expected to continue in the future. At its current share price, Richmond offers a dividend yield of 4.9%, which is quite interesting for income investors, and is above the average of the U.S. banking sector.

Conclusion

Richmond Mutual’s operating performance was negatively impacted by the regional banking turmoil in the spring of last year, which led to higher deposit costs and lower margins. On a more positive note, its credit quality remained quite strong during a challenging period, boding well for the long-term sustainability of its business model.

Regarding its valuation, its shares are currently trading around book value, which seems to be fair considering the bank’s weak growth prospects and profitability levels. Therefore, its above-average dividend yield remains the most attractive feature of its investment case, supported by a sustainable dividend that has positive growth prospects over the coming years.

Q2 2024 Earnings Call Transcript")