Brett_Hondow/iStock via Getty Images

Introduction

Just over a year ago, I argued Richelieu Hardware Ltd. (TSX:RCH:CA, OTCPK:RHUHF) was an interesting company. Although it had just outperformed most expectations, it likely still was a good candidate to pick up on dips, as I liked its balance sheet where the total net debt position represented less than 0.5 times EBITDA. I also liked how the company is managed as the management likes to pursue small bolt-on acquisitions to expand its product offerings.

This article is meant as a follow-up article on previous coverage. I’d recommend you to read the older article here to get a better idea and understanding of what Richelieu does.

The revenue decreased, the margins shrank

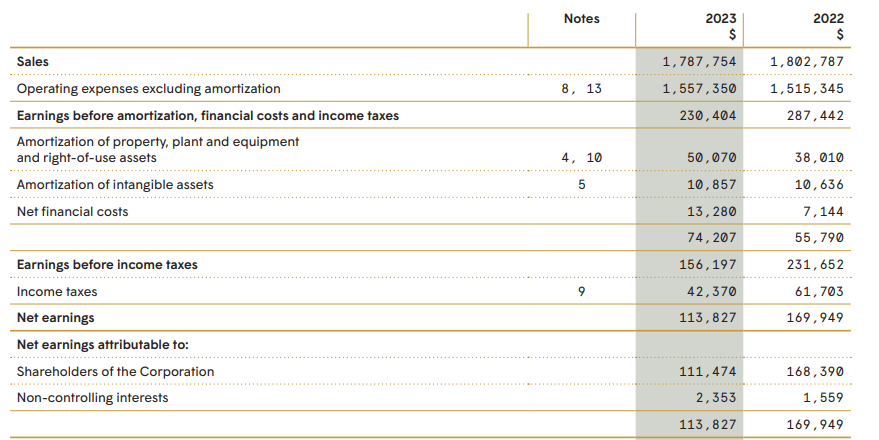

The company’s financial year ends in November, and the most recently reported full-year financials obviously discuss FY 2023. In that year, Richelieu generated a total revenue of approximately C$1.79B, a decrease of approximately 1% while the operating expenses increased by approximately 3%.

Richelieu Hardware Investor Relations

This indeed put pressure on the EBITDA result, which decreased by approximately 20% to C$230M. The EBITDA margin decreased from almost 16% in 2022 to just 12.9% in 2023. While that sounds like a steep drop, it’s worth noting 2021 and 2022 were exceptional years for Richelieu with EBITDA margins of 16.3% and 15.9% respectively. The EBITDA margin in 2019 and 2020 were just 11.9% and 13.7%, respectively, and you could consider a 12.9% EBITDA margin to be a reversal to the mean.

The company’s depreciation and amortization expenses increased, as did the net finance expenses, resulting in a pre-tax income of C$156M and a net profit of just under C$114M of which C$111.5M was attributable to the common shareholders of Richelieu Hardware. As the total share count remained virtually unchanged, the EPS dropped from C$3.01 in 2022 to just C$2 per share in 2023.

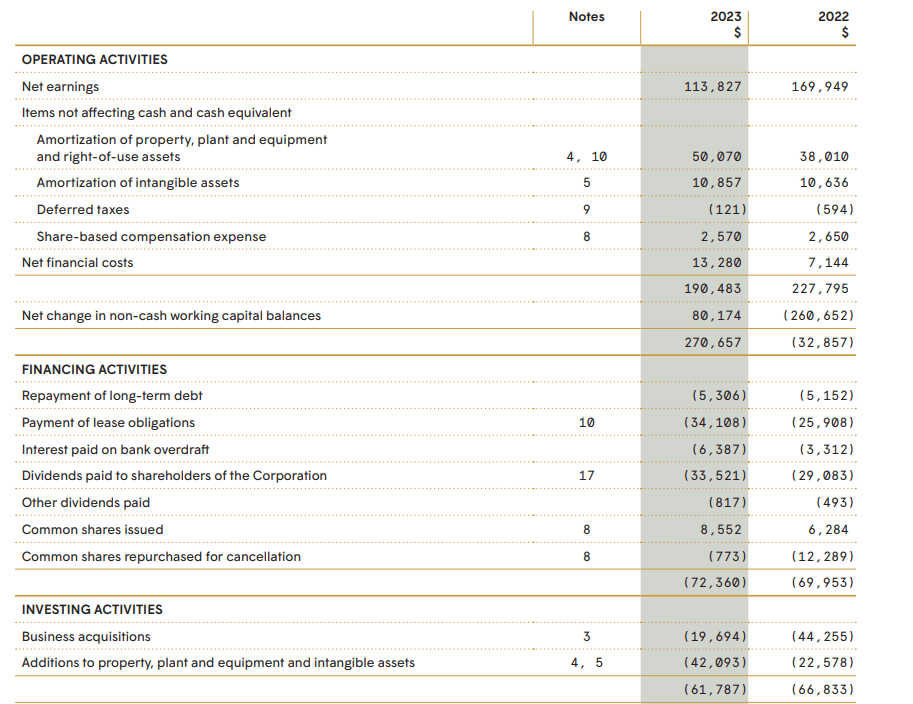

The operating cash flow generated by Richelieu during 2023 was approximately C$270.7M but as you can see below, it includes a C$80.2M working capital contribution while it did not take the C$34M in lease payments into account, while the C$6.4M in interest paid should also be deducted from the total.

Richelieu Hardware Investor Relations

This means the adjusted operating cash flow including lease payments and interest payments was approximately C$150M. That was obviously still sufficient to cover the C$42M capex (which came in at almost twice the level it spent in the preceding year), resulting in an underlying free cash flow result of C$108M. This represents C$1.93 per share.

That’s slightly lower than the reported net profit, and that’s entirely caused by the large discrepancy between the total of C$61M in depreciation and amortization charges versus the in excess of C$76M actually spent on lease payments and capex. Richelieu Hardware indeed continued to invest in organic growth (it spent money on three new centers in the USA, while an expansion project in Calgary was completed towards the end of the calendar year as well), but on top of that, it also spent a total of almost C$20M on acquisitions.

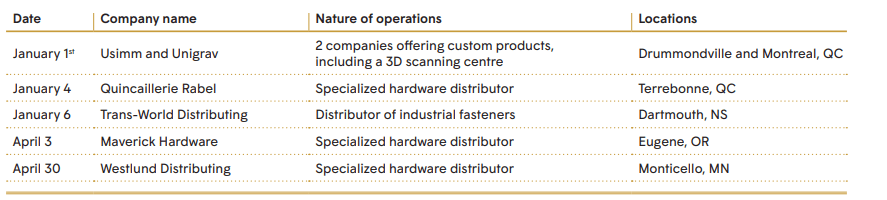

These were all relatively small acquisitions but that’s not a big surprise as that exactly is Richelieu’s modus operandi: rather than pursuing “mega-mergers,” it focuses on small bolt-on acquisitions. The C$20M was spent on five separate acquisitions.

Richelieu Hardware Investor Relations

The company did not disclose the EBITDA contributions of the acquired companies but it did mention that if all companies would have been acquired at the beginning of the financial year, they would have generated C$27M in total revenue (versus the C$23.5M in pro rata revenue they contributed during FY 2023). Subsequent to the end of the financial year, Richelieu completed two additional [small] acquisitions.

While Richelieu’s management indicated on its Q4 conference call it expected FY 2024 to start off pretty neutral or “slightly negative,” it expects the second half of the year to be much better. Meanwhile, the margins should remain stable between 12% and 13% on the EBITDA level, which further strengthens my thesis the negative evolution we saw in 2023 was just the reversal to the historical EBITDA margins after two very strong years.

Investment thesis

During 2024, Richelieu’s reported free cash flow (adjusted for working capital changes and lease payments) should increase by a double digit percentage as the company’s EBITDA margins will remain stable while the capex will decrease. The Richelieu management confirmed on the Q4 call that all major investment projects have now been completed, which likely means we will see the net cash position further increase again. As of the end of FY 2023, Richelieu Hardware had C$46M in cash on the balance sheet with just C$28M in total financial debt excluding lease obligations), for a net cash position of C$18M. Assuming a stable EBITDA of C$230M (and thus C$192M excluding lease amortizations), the company is currently trading at an EV/EBITDA ratio of approximately 12 (and this ratio is decreasing).

Although Richelieu’s financial performance should stabilize at the current levels, the stock still isn’t cheap, as it is trading at a free cash flow yield of approximately 5%. I still think the company is a “buy on dips,” as I like the management’s “bolt-on M&A” strategy. I currently have no position in Richelieu Hardware.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")