Eoneren

Investment overview

I give a buy rating for RH (NYSE:RH) as I expect growth to recover in FY24, driven by the launch of modern sourcebooks and reinvestment in advertising dollars. From a fundamental perspective, I believe RH’s scale advantage will enable it to continue winning share from subscale players, and its design gallery strategy should continue to support growth as it transitions away from legacy retail formats.

Business description

RH is a luxury home furnishings retailer selling a variety of products ranging from furniture to textiles to outdoor and garden furniture, along with offering complementary interior design services for customers. Of which, furniture represented the largest revenue contributor at 69% of FY22 sales. As of the latest filing date, RH operates 83 stores (80 of them in the US), of which 36 are legacy galleries, 28 are Next Generation Design Gallery, 14 are Waterworks, and the rest are split between RH Modern Gallery, RH Baby & Child Gallery, and International. As a luxury furniture retailer, it is natural for the business to be very cyclical, heavily indexed to the economic cycle. Nonetheless, RH still managed to grow revenue from $958 million to ~$3 billion today, 3x over 11 years. While growth has been cyclical through the years, RH has always stated EBITDA has been profitable over the past 11 years (except FY12). As of today, RH has an EBITDA margin of 15% over the trailing 12 months.

Scale is a major advantage

I believe this industry is a matter of scale. The larger you are, the more competitive advantage you have over peers, and this advantage grows exponentially as one scales. If we look at how this industry typically operates historically, given the high degree of friction associated with product inaccessibility, opaque pricing, and a lackluster assortment breadth, customers in this space typically have a difficult purchasing journey. By bringing together famous, high-end artisans on one platform, RH’s business model bridges the gap between customers and designers, thus removing these problems. With a wide selection available in-store, online, and through source books, RH simplifies and lowers the cost of furnishing a home by catering to a wide range of tastes and needs. Underlying all of these is also the need for a strong balance sheet because of how working capital intensive it is to have goods in the gallery and the fixed cost associated with operating the galleries in prime locations. For the typical subscale player, firstly, it does not have sufficient scale (not enough customer base) to convince designers to list their product with them. Secondly, it does not have a strong balance sheet to sustain the high working capital pressure from holding a wide variety of inventories (with sufficient design breadth).

Design gallery strategy makes sense

I believe RH’s strategy to shift away from legacy retail formats toward brand-appropriate Design Galleries is going to be a long-term growth driver. Unlike the past retail format, where inventories are placed like a showroom, the new format offers an immersive retail experience. Specifically, the key differences are:

- Design galleries are located in prime street locations (vs. shopping malls), and as such, they are much bigger than the legacy format. Setting it up in a prime location naturally attracts more traffic and attention. Importantly, because of the size, RH is able to showcase more products.

- Design galleries product displays focus on collections instead of condensed representations of collections. I believe the former display format makes more sense because of the targeted customer profile. Remember that RH is selling luxury furniture, so its targeted consumers are the rich and sophisticated. Showcasing the entire collection increases the chance of these consumers buying the entire set.

- Design galleries are also localized to ensure each store does not have high assortment redundancies. This is important because it gives each gallery a unique image, such that consumers will be more willing to visit other galleries because there is something new. From a business standpoint, this also makes sense because RH is maximizing its retail spaces to offer a wider variety of products.

Product launches to drive top line growth

Turning to more current events, sales were poor in 3Q23 (a 13.6% year-over-year decline), mostly because of the increased headwinds in early October, when mortgage rates reached an all-time high of more than 8%. The modern sourcebook was postponed until 1Q24, so I don’t think we can extrapolate this performance to the future. For background, RH’s sourcebook mailings for interiors and contemporary were both launched in mid-September and early October, respectively. However, demand was affected by peak interest rates and the Middle East war. As a result of the soft demand environment, RH delayed the new Modern Sourcebook mailing until 1Q24. Looking ahead, I actually think the growth outlook is positive, as

- There are hopes for rates to be cut.

- Demand appears to be recovering, with management noting that they saw improved demand trends generated from the launch of its new RH Interiors and RH Contemporary collections.

- I expect RH to step up its advertising spend back to normalized cadence.

Valuation

May Investing Ideas

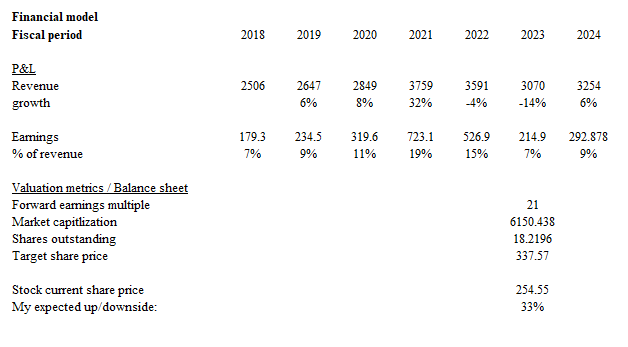

My expected target price for RH is $337.57. I expect revenue to continue its decline for the rest of FY23, following a management-guided 14% decline, and for FY24 to see a modest recovery of 6% (using FY19 growth as a benchmark as it was the start of the recovery since FY18). With the modern sourcebook and reinvestment of advertising dollars starting in FY24, growth of 6% is not implausible. As for earnings expectations, FY23 is going to be a tough year given the steep decline in growth, which has high decremental margins. FY24 should see a recovery as growth recovers. I believe the right way to value RH is by valuing it using its through-cycle valuation multiple, which is the average that it has traded throughout the years. Over the past 10 years, the RH average forward PE multiple has been 21x, and I am using that as a benchmark for valuing RH.

Risk

Furniture spending is impacted by mortgage rates as new homes drive demand for new furniture sets. As mortgage rates follow the Fed interest rate movement, this also means that RH sales are heavily impacted by the Fed’s decision to cut or raise rates. If the Fed decides that the economy is still too hot and requires further taming, they could raise rates further (there is precedent for rates being higher than this), which will hurt RH growth.

Conclusion

I recommend a buy rating for RH based on its strong scale advantage, design gallery strategy, and upcoming product launches. RH shift towards brand-appropriate Design Galleries, located in prime street locations, enhances its competitive edge and appeals to its affluent customer base. Despite a challenging FY23, I anticipate a recovery in FY24 driven by the launch of modern sourcebooks and increased advertising spend.

Q2 2024 Earnings Call Transcript")