Andriy Onufriyenko/Moment via Getty Images

Good Things Come in Threes: Small Caps, Life Science and International Equities

At the end of 2023, the stark contrast between this year and the last was evident from the headlines. However, beneath the surface, several significant trends that emerged in late 2021 continued and even accelerated throughout the year. These trends have created what we consider one of the most exciting opportunity sets in our firm’s history. We are intensely focused on three specific factors that seem entirely unloved by Mr. Market today:

- Small cap equities

- Life Science Tools and Instruments

- International Equities

Our love for these three areas need not preclude us from investing in large cap US equities. In fact, two of the so-called “Magnificent 7” represent a sizable portion of our invested assets; however, our buying over the past year and our watchlist are full of securities within each of these three buckets.

The Federal Reserve Bank’s fight against inflation progressed rapidly throughout the year, with inflation exiting 2023 at levels approaching the Fed’s 2% target on some observable metrics. We covered the fight against inflation in depth in last quarter’s letter, but are mentioning it again both to note the remarkable progress to date and because there is as a corollary with to these unloved areas in which we are interested. Small caps, life sciences and international equities for various reasons are far more rate sensitive than large cap companies. As such, with rates (as represented by the 10-year) already falling, spreads tightening and the Fed with a line of site to easing, we think the setup looks increasingly favorable for these areas to recover lost ground.

Let us be clear: our investments in these areas are not a directional bet on inflation or rates. When we scout for investment ideas, we do so by employing both bottom-up and top-down approaches to idea generation. Bottom- up ideas are ones where the process is purely about the fundamental setup of one specific security, while top- down ideas are ones where a high-level thematic thesis lends to the search for interesting, specific investments. With respect to both small cap and international equities, we conducted our typical idea generation and diligence processes and consistently unearthed the most interesting ideas in these areas.

As for Life Sciences, this is a corner of the market where we have generally kept a watchlist of interest companies and twice before this past stretch made meaningful moves into the space. We have long held a belief that this unique corner of the market was one that generalists with discipline could profit from immensely. Upon recognizing what had formerly been an orderly area becoming disorderly due to post-COVID headwinds, we determined it would be an opportune time to build out expertise and approach the sector methodically. To simplify, small caps and international were very much bottom-up emphases while Life Sciences has been a top-down exercise that led us to bottom-up ideas.

Most importantly, we have a deep belief in the quality and valuation at each of the companies we have invested in. We approach these three corners of the market with enthusiasm, though also with the benefits of the painful lessons we have learned over the past few years. In doing so, we are mindful that small companies are inherently less resilient than large ones, we are cognizant that there is a high degree of domain expertise that specialists possess in the life scientists and we are conscious that outside the US there are unique regulatory risks and challenges from a volatile currency regime and global supply chain. Valuation gives us considerable comfort that we are approaching each individual opportunity with a margin of safety and diversification via smaller position sizes leaves us comfortable that no one opportunity gone awry can inflict substantial damage.

Below, we will explore what draws us to each area and how we approach these opportunities.

SMALL CAP EQUITIES: A GENERATIONAL BUYING OPPORTUNITY

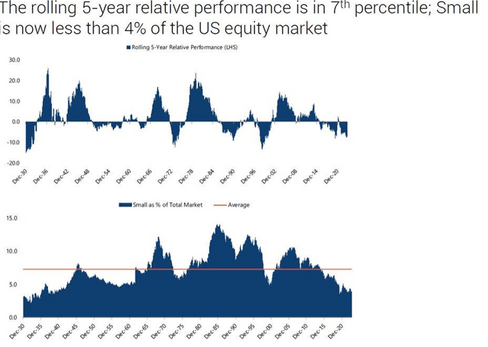

We consider the current situation a “generational buying opportunity” for small-cap equities. Over the past two years, we’ve highlighted the significant underperformance and valuation gap between small and large caps. Currently, small caps make up less than 4% of the entire US equity market, a level reached only twice before (the 1930s, the COVID crash and now). Their performance relative to large caps over the past five years is in the 7th percentile, indicating a rare degree of relative underperformance.[1]

And it is amongst the widest valuation spreads between big and small observed in recent times:[2]

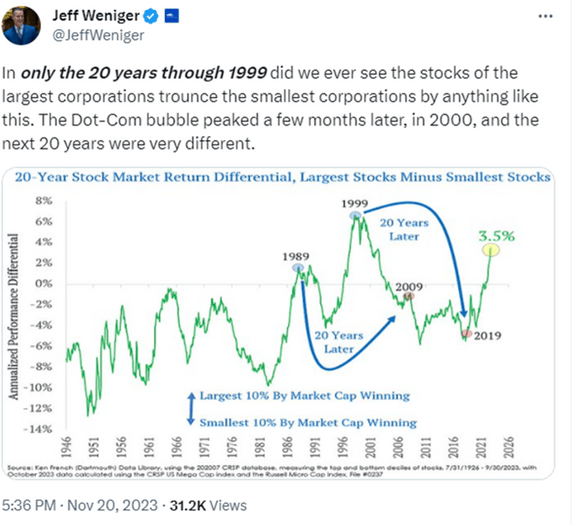

This chart below stands out, because it is now a 20-year stretch of underperformance which has only been exceeded by the 20-years leading up to the Dot Com peak in 1999:[3]

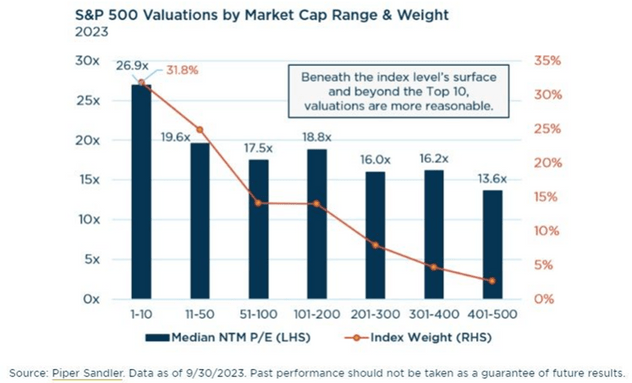

This is an extremely long stretch. Notably this preference for large over small is observable even within the S&P 500:[4]

To us, this size divergence that is observable across all size-based stratifications suggests structural forces are at work. We covered why we believe this to be in our Q1 2023 section entitled “How did we get here?” and have become increasingly convinced in this reality today.[5]

In December 2023, Elliot had the opportunity to interview his friend and mentor Mario Cibelli of Marathon Equity Partners at the MOI Global Latticework conference.[6] Mario shared a profound piece of wisdom on investing in small caps–”small cap investing is activist investing.” To that end, we have become increasingly engaged with the companies in which we are investing. We have written four behind-the-scenes letters to our portfolio companies and so far, three responded favorably to our suggestions. Notably, two of these three have performed well enough to graduate into the Mid Cap size class and the third was greeted warmly by Mr. Market for adopting our suggestions. The lone company who ignored our overtures suffered mightily. (In the future, the degree to which companies listen and thoughtfully respond will be incorporated in our willingness to stay the course or not at a given investment.)

Each of our letters covered three distinct, overlapping areas with similar messages:

- Take steps to immediately enhance profitability.

- Use sizable cash balances in order to repurchase shares.

- Improve communication around strategy and capital allocation and enhance disclosure.

We have witnessed the nature of disclosure as a counter-cyclical phenomenon. In harsh environments, companies who treated investors to minimal disclosure during the good times lose the benefit of the doubt. When investors must make assumptions to understand business realities, those assumptions will skew to conservatism or down-right skepticism. Companies must revisit their “good times” disclosures and feed investors more granular information. Disclosure helps shed light on the appropriate realities the business is facing and, in many cases, even when downright skepticism is warranted, investors can at least appropriately handicap the situation. Few investors are comfortable stepping into the unknown, and therefore realistic handicapping allows investors to take an educated risk and embrace opportunity.

As we proceed further into the small cap space, we see real opportunities to engage constructively with companies and help orchestrate better approaches and/or outcomes.

LIFE SCIENCES: THE NEXT CYCLE’S “TECH”

We view life science companies as the next cycle’s tech sector—performance leaders of the market for an extended period of time. These companies benefit from an aging population, an abundance of “razor-and-blade” business models, significant regulatory barriers to entry, and the necessity of extensive R&D for market entry and scaling. Despite these advantages and a decade of rapid innovation, the market has yet to fully appreciate the value.

While we have labeled small caps a generational opportunity, we think similarly of the life sciences space. We believe that life science companies are set to become the next tech giants. Technology companies have achieved remarkable market success, driven by impressive compound growth rates and healthily increasing valuations. Although investors have grown to favor tech companies, now seeing them as indispensable parts of investment portfolios, this was not always the case. Just over a decade ago, following the dot-com crash, tech companies were often seen as risky investments more likely to lose money than earn it. Around this time, Warren Buffett famously said that “I have avoided technology sectors as an investor because in general I don’t have a solid grasp of what differentiates many technology companies.”[7] Meanwhile, this decade, Buffett made perhaps his greatest investment ever in the technology sector with Apple.

When we speak with generalists, they typically quote Buffett in asserting that life science companies “are in the too hard pile” and “not in my circle of competence.” This captures the notion that industries that are challenging to understand may present attractive returns but should be avoided for fear of missing critical information that only specialists possess. Contrary to conventional wisdom, we have found that in some respects, life science companies are in fact easier to grasp than those Phil Fisher might suggest. We think there are extremely appealing elements to life science companies, specifically the service providers, which all generalists can grasp. These traits include the following:

- A structural growth tailwind in the form of an aging population, selling literally “mission critical” substrate for life itself.

- A large number of razor-and-blade business models, whereby selling an instrument leads to years of high margin consumable demand.

- Regulatory barriers to entry, including many features that are “spec’d in” (industry parlance for components that are written into the regulatory approval of a product or drug).

- Years of accumulated R&D necessary for a product to reach market and scale.

The sector will leverage its phenomenal business models and tremendous barriers to entry to profitably capture these structural growth tailwinds.

Importantly, we think the entire life science space has delivered profound innovation over the last decade, that has yet to be reflected in market prices. The XBI (a biotech ETF) has essentially been flat for a decade, which looks like stagnation, when in fact progress has come at an accelerating rate:[8]

In the book The Cloud Revolution: How the Convergence of New Technologies Will Unleash the Next Economic Boom, author Mark Mills details how technological breakthroughs take years to manifest as mass market products with critical economic impact. Mills explains:

The key to forecasting whether something will soon be different about our future is in knowing whether new technologies have reached the point of…irruption. And to know whether this is the case, the pattern that’s relevant is not one about growth rates, but about the intersection of related but independent technological developments that, when they happen contemporaneously, lead to an erruption.[9]

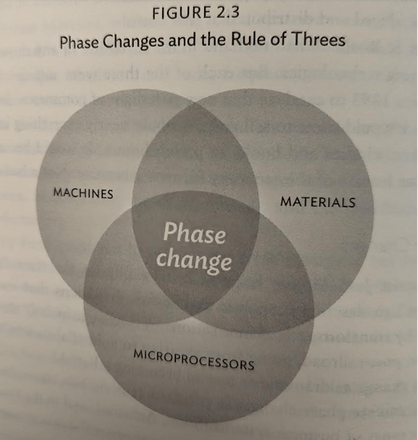

Mils proceeds to explain that “All inventions are built on layers of combinations of other more foundational things that can be traced…back to early inventions, insights and discoveries” in “Rules of Three” where three critical pieces combine to create a phase change:

We believe three critical pieces today are aligning to create such a phase change for the industry: (1) genomics, (2) cell editing led by CRISPR and (3) big data/artificial intelligence. Genomics provides the materials through which the application of artificial intelligence can analyze and find relevant targets for the application of biologics. Only in June of 2000 did scientists announce the first fully sequenced genome was completed after thirteen years of work, at a cost of $2.7 billion (about $5 billion in 2024 dollars).[10] Today, a full genome can be sequenced in less than half a day for $200 or less!! This advancement is profound.

It is challenging to harness the power of such an advancement in isolation. As we take advantage of the drastically reduced time and cost to sequence a genome, we accumulate massive troves of data. Analyzing the data to garner insights had largely been a brute force task that combined a combination of persistence and luck to generate actionable scientific insight. With big data and artificial intelligence, our ability to extract insights expands exponentially.

In the past decade, a team of scientists led by Jennifer Doudna (discussed in our Q3 2022 commentary) discovered a systemic way to edit the genome of a living organism.[11] With biologics including monoclonal antibodies and cell and gene therapies we can harness the insights garnered from genomics and AI to more efficiently craft therapies that resolve all kinds of maladies. This manifests in an increasingly tangible way for the industry, as explained in a fantastic journal article in Nature entitled “Breaking Eroom’s Law” as follows:

Early in the last decade, researchers at Sanford Bernstein published ‘Eroom’s Law’— Moore’s Law in reverse — that the all-in cost of R&D on new drugs approved by the US FDA had risen exponentially for 60 years (Nat. Rev. Drug Discov. 11, 191–200; 2012). Starting around 2010, the trend line changed, with a net result of an additional 0.7 new molecular entity (NME) launches per billion US$ of R&D spending per year by 2018.[12]

In other words, for decades the cost of developing a new drug had risen year-after-year, but with genomics we are finally seeing green shoots of declining costs in drug development. These cost declines are driven by a combination of a clearer understanding of which targets lead to better outcomes and understanding the ways in which a target might adversely affect a patient. As a result, biotech companies are now able to select approaches with substantially lower likelihoods of adverse events and much greater likelihood of success. Nowhere is this confluence of benefit more evident than in the ability of two companies to bring COVID vaccines to market in less than twelve months from the emergence of the disease. Genomics is now having a delayed, but massive impact on drug discovery, a notion neatly encapsulated in the following chart:[13]

These developments are leading to a broadening of pipelines and modalities for treating patients, which will manifest in an explosion of business for the companies facilitating the discovery, development and manufacturing of approved treatments and therapies sometime in the next three to five years.[14]

With these new modalities moving past the lab, into the clinic and now commercialization, we are only now in the earliest stages of the exponential growth phase for the industry. Late 2023 saw a watershed moment for the entire industry when Casgevey, the first CRISPR-based gene therapy received FDA approval (notably Casgevy is powered by Maxcyte, a company we featured in the aforementioned Q3 2022 commentary). The below chart features only monoclonal antibodies (mABs). Importantly, Cell and Gene Therapies are in their infancy, arguably around the year 2000 in the chart and mABs are growing swiftly from what is now a substantial market size:[15]

We spent most of our last commentary on how myopically focused markets are on the exact timing with which these companies will lap their COVID over-earning and supply chain noise, but with a long-term investment horizon it is impossible not to be excited by the opportunities that will emerge from today’s market challenges.

INTERNATIONAL EQUITIES: THE BEST OF ALL WORLDS

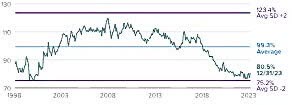

Our subtitle here is a bit tongue-in-cheek, but one can check all three boxes with an international, small cap life science company. When we started in this industry, the BRICs were the “Mag 7” of the day and the idea of investing internationally was perceived as obvious. Much like with the small cap vs large in the US, international securities have been cast aside by investors. As things stand today, this is one of the widest divergences in valuation that has existed between the US and everything else:[16]

In some respects, this divergence makes sense considering the world’s biggest, best companies are US-domiciled tech companies; however, as is often the case, what starts with a dose of logic can stretch well beyond reasonable bounds. The performance woes of international equities have been compounded by a strong dollar, even though many of these businesses have similar revenue bases. There are many internationally listed companies, with global franchises, some of whom do the majority of their in the United States. In these cases, obvious US comparables trade at considerably higher valuations. There is no obvious answer as to what closes the valuation gap, though in the meantime, we are happy to pick up the excess return associated with a cheaper valuation while waiting for either international markets to return to favor, or in some cases, a relisting to the US to catalyze a better valuation.

Our pursuits in international equities are almost entirely bottom up. We look for outstanding companies at cheap valuations and the hunting grounds are especially fertile. One of our favorite geographies today is the UK, with the UK Small Cap space perhaps the most decimated developed world asset class. UK stocks in general were disproportionately hurt by the financial crisis, then the European Crisis, followed by Brexit and more recently COVID. Each of these events led to a relative rerating lower compared to even their European brethren. UK Stocks hit financial crisis level P/Es in November of 2023:[17]

While European markets are cheap in general, European large caps are trading at historically wide premiums to small caps and the magnitude is similar within each of the key geographies:[18]

Such wide divergences lend themselves to stock picking in bottom-up fashion. While our pursuits here started purely from a bottom-up approach we have purposefully sought out international small caps with global franchises and diverse revenue bases. Many are attractive and we think this magnitude of spread will offer opportunities in the years to come.

Considerable opportunity ahead

As enter the middle years of the 2020s, we think some of the volatility and lessons learned over the recent past will lend themselves to considerable opportunity capture ahead. By building a portfolio orientation around the areas highlighted in this commentary, we aim to capitalize on undervalued opportunities with a focus on quality and valuation. Our strategy is informed by a thorough understanding of each sector’s unique risks and challenges, ensuring we approach investments with a margin of safety and a diversified portfolio. We are simultaneously humbled by the recent past and excited for the road ahead.

Thank you for your trust and confidence, and for selecting us to be your advisor of choice. Please call us directly to discuss this commentary in more detail – we are always happy to address any specific questions you may have. You can reach Jason or Elliot directly at 516-665-1945. Alternatively, we’ve included our direct dial numbers with our names, below.

Warm personal regards,

Jason Gilbert, CPA/PFS, CFF, CGMA Managing Partner, President

Elliot Turner, CFA Managing Partner, CIO

|

Footnotes 1Jefferies 2https://www.royceinvest.com/insights/small-cap-recap 3https://twitter.com/JeffWeniger/status/1726731323442647538 4Piper Sandler 5https://www.rgaia.com/commentary/q1-2023-investment-commentary-where-we-are-hunting-for-value/ 6https://moiglobal.com/latticework-2023-elliot-turner-mario-cibelli/ 7https://www.thinkfn.com/wikibolsa/Visita_a_Warren_Buffett 8https://rapport.bio/all-stories/the-way-through-the-biotech-downturn 9Mills, Mark. The Cloud Revolution: How the Convergence of New Technologies Will Unleash the Next Economic Boom. 10https://archive.nytimes.com/www.nytimes.com/library/national/science/062700sci-genome.html? scp=2&sq=%252522francis%252520collins%252522%252520god&st=cse 11https://www.rgaia.com/wp-content/uploads/2022/10/RGAIA-Q322-INVESTMENT-COMMENTARY.pdf 12https://www.nature.com/articles/d41573-020-00059-3, hat tip to Stifel for pointing us to this paper. 13ibid 14https://www.youtube.com/watch?v=0DIgT32bFV4 15https://jbiomedsci.biomedcentral.com/articles/10.1186/s12929-019-0592-z 16Guide to the Markets? gad_source=1&gclid=CjwKCAiA_OetBhAtEiwAPTeQZ3qtjCt9Do4ATiJ0Uwq1ODpj0LJ7OsBjTybRR_Nwr3_nKbSd9NXfrhoCyzcQAvD_BwE&gclsrc=a w.ds 17https://finimize.com/content/the-uks-stocks-are-almost-embarrassingly-cheap 18https://www.polarcapital.co.uk/gb/individual/Small-Caps/#europe Past performance is not necessarily indicative of future results. The views expressed above are those of RGA Investment Advisors LLC (‘RGA’). These views are subject to change at any time based on market and other conditions, and RGA disclaims any responsibility to update such views. Past performance is no guarantee of future results. No forecasts can be guaranteed. These views may not be relied upon as investment advice. The investment process may change over time. The characteristics set forth above are intended as a general illustration of some of the criteria the team considers in selecting securities for the portfolio. Not all investments meet such criteria. In the event that a recommendation for the purchase or sale of any security is presented herein, RGA shall furnish to any person upon request a tabular presentation of: (i) The total number of shares or other units of the security held by RGA or its investment adviser representatives for its own account or for the account of officers, directors, trustees, partners or affiliates of RGA or for discretionary accounts of RGA or its investment adviser representatives, as maintained for clients. (ii) The price or price range at which the securities listed. |

Q2 2024 Earnings Call Transcript")