While regional-bank stocks continue to be dragged down by the troubles assailing New York Community Bank, their bonds are holding up — suggesting bondholders view NYCB’s issues as isolated.

NYCB’s

NYCB,

sole traded bond tumbled last week as its stock shed more than 40% of its value after the bank posted a surprise quarterly loss and disclosed trouble with its commercial real-estate loans. The company also slashed its dividend to build up capital to meet regulatory requirements.

The stock is now down almost 60% in the year to date, and its bonds are trading at around 75 cents on the dollar after Moody’s Investors Service downgraded the credit to junk status.

On Thursday, D.A. Davidson downgraded the stock to neutral from buy and said it is trading “untethered from fundamentals.”

Analyst Peter Winter cut his price target for the stock to $5 from $8.50 after the downgrade and the company’s disclosures about a rise in deposits and its plans to hire a new chief risk officer in the near future.

The bank confirmed that both its chief risk office and main audit executive had left the bank, stirring unhappy memories of Silicon Valley Bank and its March 2023 collapse. That bank also had no chief risk officer when it was hit by a run on deposits last year that sent shock waves across the regional-bank sector.

NYCB raised its loan-loss reserves by 790%, or $490 million, in the fourth quarter, the most of any regional bank — although others also made sizeable hikes, as MarketWatch’s Steve Gelsi reported.

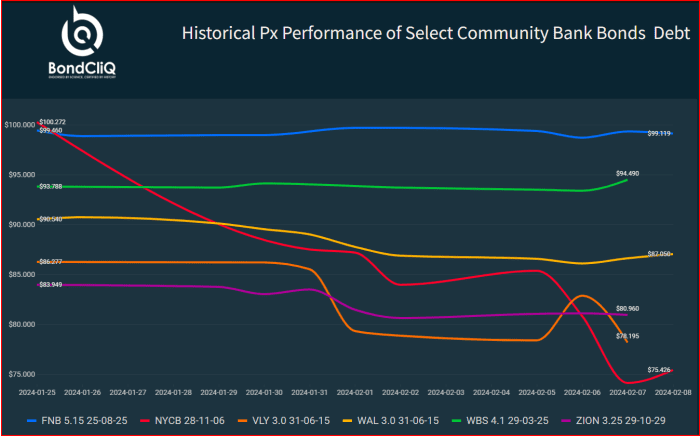

The following chart from data-solutions provider BondCliQ Media Services shows how select community-bank bonds have performed over the past two weeks, with NYCB’s floating-rate notes that mature in 2028 showing the most dramatic decline.

Don’t miss: New York Community Bancorp looks to sell rent-regulated commercial real estate after surprise quarterly loss

Those bonds actually rose about 5 basis points on Thursday, as the chart indicates.

NYCB is followed by Valley National Bancorp’s

VLY,

3.0% notes, which mature in June 2031 and have fallen to 78 cents on the dollar. That bank, which operates as Valley Bank, is a regional lender based in Morristown, N.J., with about $61 billion in assets.

Historical price performance of select community-bank bonds.

BondCliQ Media Services

As the chart shows, the bonds of other small lenders have remained steady as the selling of NYCB’s bonds has picked up. These include Western Alliance Bancorp.

WAL,

a Phoenix-based lender with $70.9 billion in assets as of Dec. 31.; Zions Bancorp N.A.

ZION,

a Salt Lake City-based bank with $87.2 billion in assets; First National Bank of Pennsylvania

FNB,

a Pittsburgh-based lender traded as F.N.B. Corp. with $34.74 billion in assets; and Webster Financial Corp.

WBS,

a Stamford, Conn.-based lender with $74.95 billion in assets.

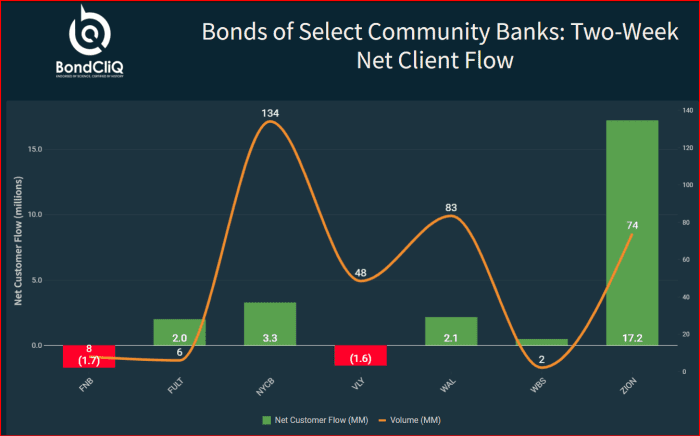

The bonds have also seen net buying over the past two weeks, even as the drama at NYCB has unfolded.

Bonds of select community banks’ two-week net client flows.

BondCliQ Media Services

The bond market “seems to think this is an isolated problem and there’s no contagion,” one market source told MarketWatch.

The SPDR S&P Regional Banking ETF

KRE,

an exchange-traded fund tracking the sector, was down 0.3% on Thursday and has fallen 11% in the year to date, while the S&P 500

SPX

has gained 4.6%.

Q2 2024 Earnings Call Transcript")