champc

Investment thesis

I’ve been following RCM Technologies (NASDAQ:RCMT) closely and I’ve written three articles about the company on SA. The latest of them was in November 2023 and back then I said that the valuation was starting to look stretched despite my expectations that EBITDA for the FY23 would surpass $20 million.

I think this could be a good time to revisit RCM Technologies as the company released its Q4 FY23 financial results on March 13. In my view, they were strong as EBITDA for the full financial year came in higher than my expectations at $24.8 million. However, I’m concerned that the debt burden is expanding, and free cash flow (FCF) was below $10 million as receivables kept on growing. I’m keeping my rating on RCM Technologies’ stock at neutral. Let’s review.

Introduction to the business

If you’re not familiar with the company or my earlier coverage, here’s a short description of the business. RCM Technologies was established in 1971 and focuses on the design, development, and delivery of business and technology solutions to commercial and government sectors. This is an asset-light business and over 95% of sales come from the USA.

The company has three operating segments, namely engineering, life sciences and information technology, and specialty health care services. The latter usually accounts for more than half of revenues and is involved in staffing, and permanent placement solutions for rehabilitation, nursing, health information management, and allied healthcare professionals. While this segment serves hospitals, schools, and long-term care facilities, about 80% of its revenues come from school districts.

The engineering segment, in turn, offers engineering and design, engineering analysis, technical writing and technical support, and EPC services. It has over 20 Fortune 500 customers and its retention rate is about 95%, making its financial performance relatively easy to predict.

Finally, the life sciences and information technology segment focuses on enterprise business, application, infrastructure, and life sciences solutions. This business typically has the best margins out of the three, with the gross profit margin usually surpassing 35%.

RCM Technologies has been pivoting its business to more managed services and higher-margin work over the past few years, so growth in the life sciences and information technology segment has been crucial for improving operating margins.

The Q4 FY23 financial results

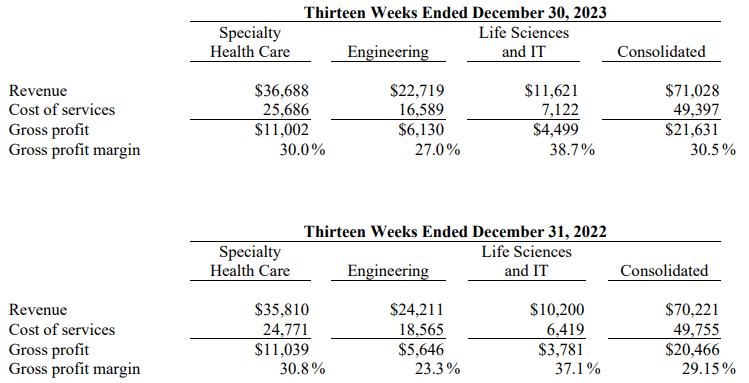

Looking at the Q4 FY23 financial results, we can see that revenue inched up by 1.1% to $71 million while the gross margin improved to 30.5% as the revenue growth came mainly from the higher margin life sciences and information technology segment. I was surprised to see another quarter of double digit percentage revenue growth in this segment in light of lower hiring activity in the US IT sector in late 2023. While the engineering business had a soft quarter in terms of revenue, its margin improved to 27%. Considering revenues in this segment were negatively impacted over the previous few quarters by lower aerospace revenue due to a contract reduction with a major client, I think it could take several more quarters for it to return to growth.

RCM Technologies

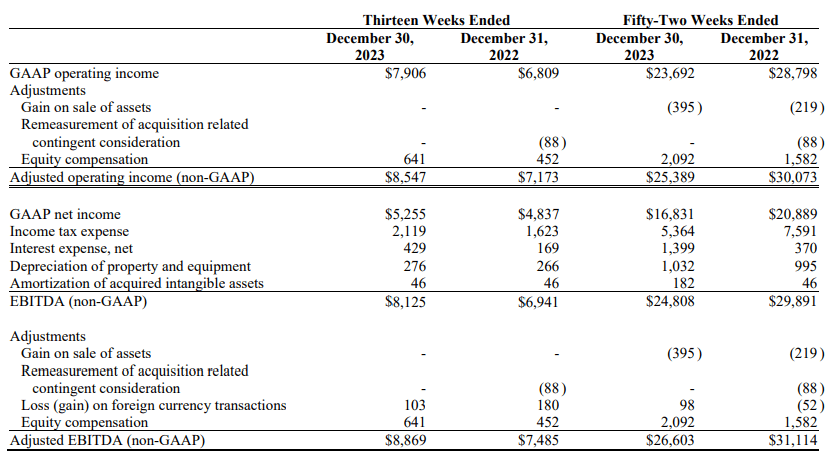

The higher gross margin for the quarter led to a 17.1% year on year increase in EBITDA to $8.1 million, which boosted the total for the financial year to $24.8 million. While I was expecting EBITDA for FY23 to surpass $20 million, I’m positively surprised it almost touched $25 million.

RCM Technologies

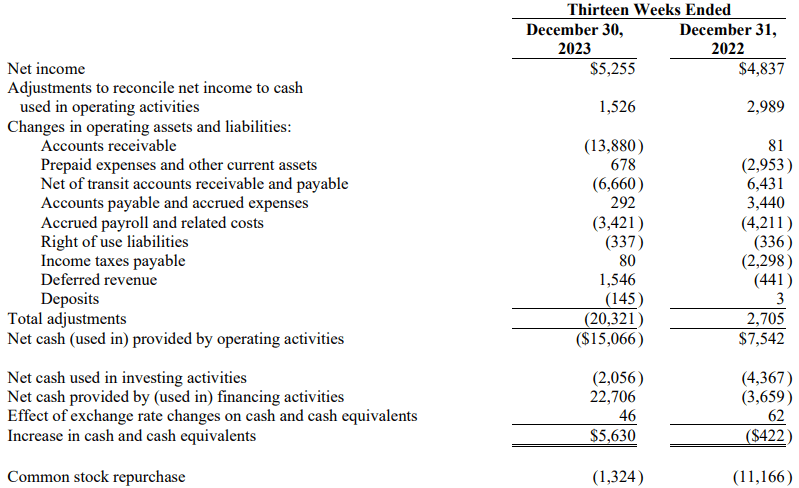

However, I think there were several red flags for the quarter. The accounts receivable continued to increase rapidly and ended December 30 at $70.7 million. This is almost $20 million higher than a year earlier while accounts payable declined by $1.7 million year on year to $12.5 million. The absolute amounts and spreads for accounts receivable and payable can fluctuate from year to year but such a high level is concerning, and it could be a sign there could be issues with some clients on the horizon. The higher level of accounts receivable also led RCM Technologies to take on more debt during Q4 FY23 as well as limit share buybacks to just $1.3 million. The FCF for the full financial year dipped to slightly below $10 million from $23.5 million a year earlier.

RCM Technologies

Looking at the balance sheet, the net debt of the company stood at $24.8 million as of December 30 compared to just $6.4 million on September 30, 2023. The tangible book value was only $3 million.

Future of the company

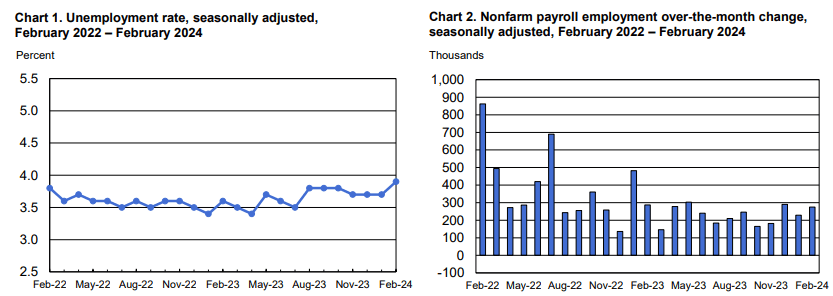

Staffing companies usually don’t perform well during periods of rising unemployment and with the US unemployment rate approaching 4%, I think that FY24 could be challenging for RCM Technologies. I find it particularly concerning that nonfarm payrolls in the temporary help services sector were down in both January and February 2024.

U.S. Bureau of Labor Statistics U.S. Bureau of Labor Statistics

If the unemployment rate in the country surpasses 4.5% in the coming months, I think the EBITDA of RCM Technologies for FY24 could fall below $15 million.

Valuation

As you can see from the chart below, RCM Technologies has often traded at EV/EBITDA multiples of between 7x and 11x over the past decade. The company is valued at 8.7x EV/EBITDA as of the time of writing thanks to the strong Q4 FY23 results, and it doesn’t look particularly cheap or expensive. However, I doubt that the company’s financial performance is sustainable in a rising unemployment environment, and I expect EBITDA to fall in FY24. In my view, the share price of RCM Technologies is unlikely to be higher by the end of 2024 even if accounts receivable decrease in the coming months and the company increases share buybacks.

Seeking Alpha

Investor takeaway

The financial results of RCM Technologies for Q4 FY23 surpassed my expectations as EBITDA for the full financial year almost topped $25 million. However, I’m concerned that FCF and share buybacks were limited by growing accounts receivable and net debt. While the company doesn’t look expensive at 8.7x EV/EBITDA, I think FY24 is likely to be softer than FY23 due to the rising US unemployment rate. In my view, this might be a good time for investors to trim or close their long positions at RCM Technologies.

Q2 2024 Earnings Call Transcript")