da-kuk

Investment Outlook

I previously wrote about Qualys (NASDAQ:QLYS) in August 2023 with a Hold outlook due to slowing sales cycles.

The firm is losing Microsoft (MSFT) as a VMDR client, which is a material loss that it will have to make up for in 2024.

Current valuation appears to be high even after a 10% stock price drop recently.

My outlook on QLYS is to Sell, as the firm will likely spend 2024 and beyond on a lower growth trajectory and possibly higher R&D and sales expenses as it tries to replace substantial lost revenue.

Qualys’ Approach And Model

Qualys generates revenue from a variety of applications, with the primary functionalities being to enable companies to deal with vulnerability detection, management, and related compliance requirements.

The company’s business model is split between direct customers and customers through partners.

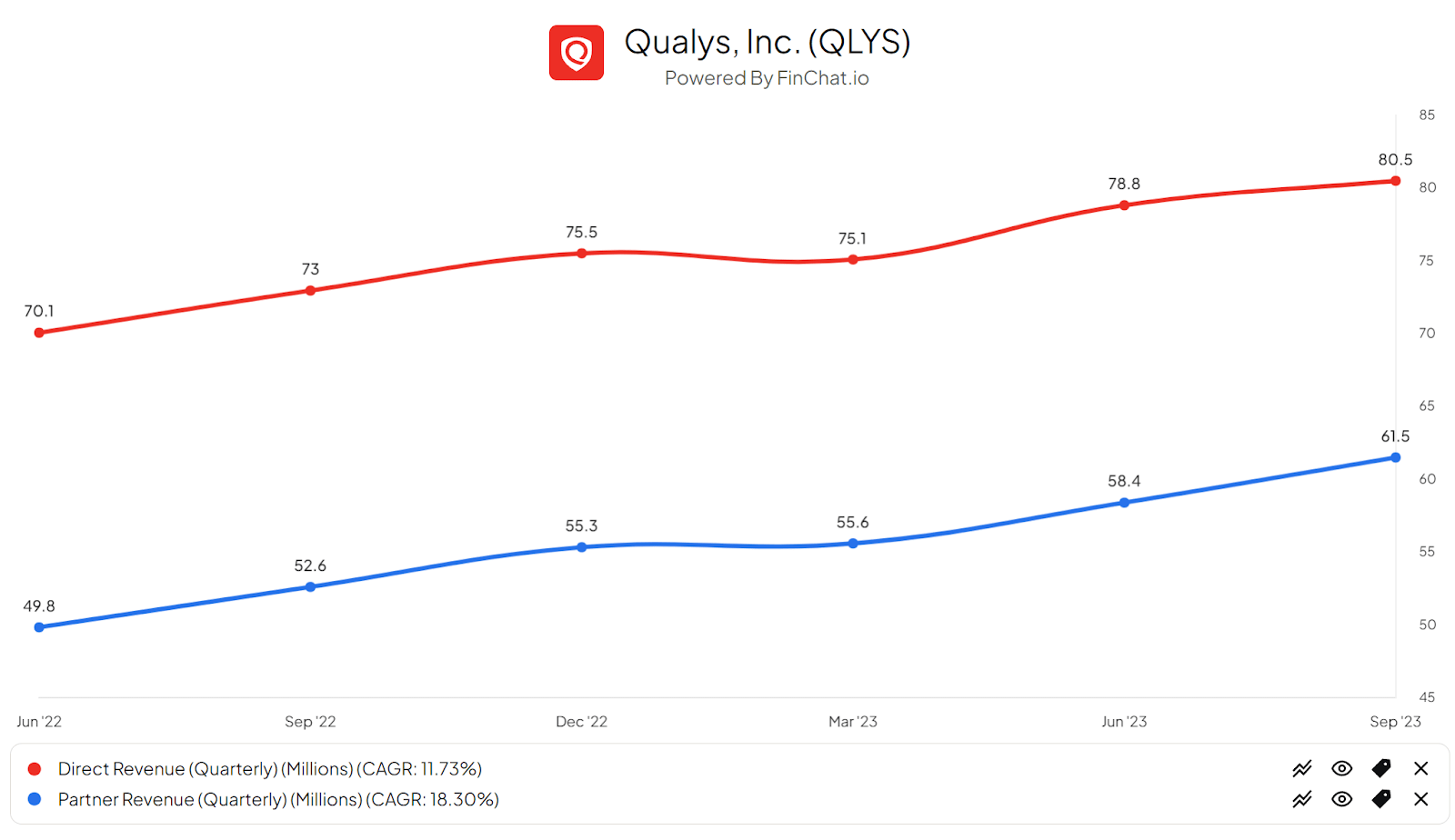

The chart below shows the trend in split between these two channels, with Direct Revenue being the red line and Partner Revenue, the blue line:

FinChat.io

Direct Revenue accounts for a higher portion of the firm’s revenue but has been growing at a slower rate of growth than Partner Revenue.

A number of enterprise software companies have recently focused more on channel revenue through partners as a way to gain scale while maintaining their in-house footprint.

Qualys has been growing its Partner relationships for several years now, so the loss or downgrading of the relationship with Microsoft, while a high-visibility loss that may account for 5% to 10% of revenue per a report of the relationship change, may not be as big of a challenge to the company due to its broad efforts to create as many partnerships as possible.

Recent Financial Trends And Valuation

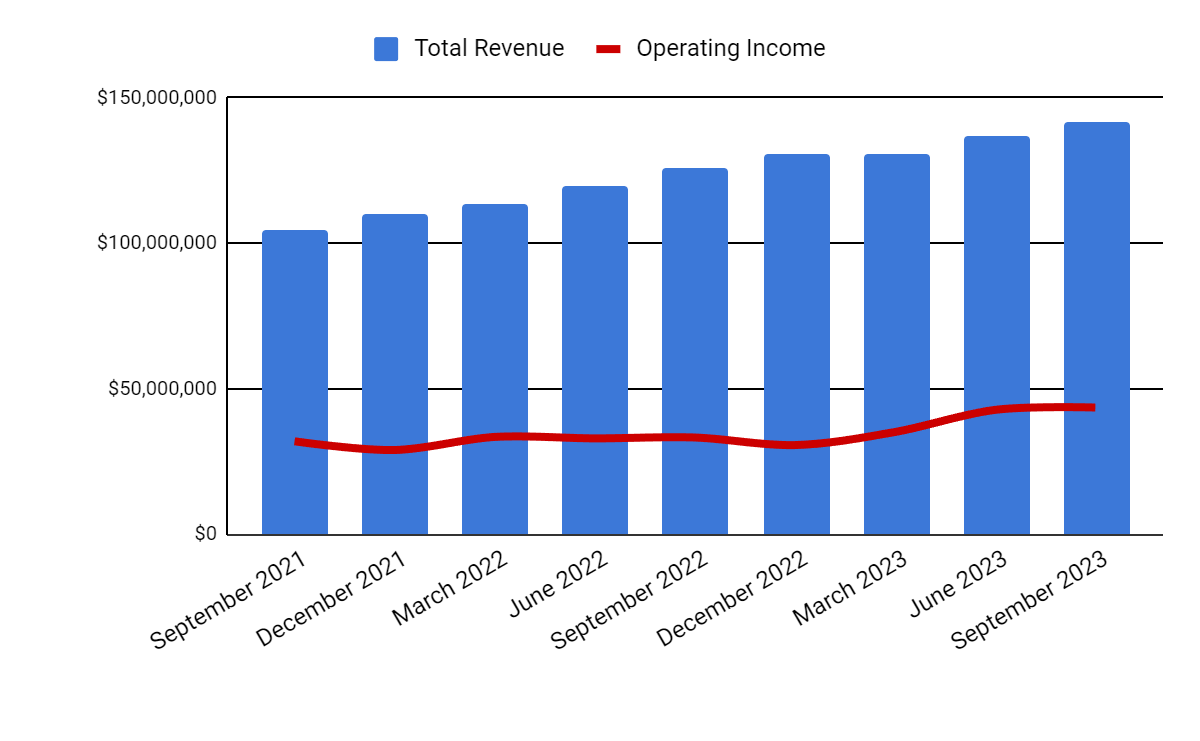

Total revenue by quarter (columns) through the end of Q3 2023 has continued to rise, although I expect this growth to taper off due to the MSFT situation; Operating income by quarter (line) has also risen in line with revenue growth.

Seeking Alpha

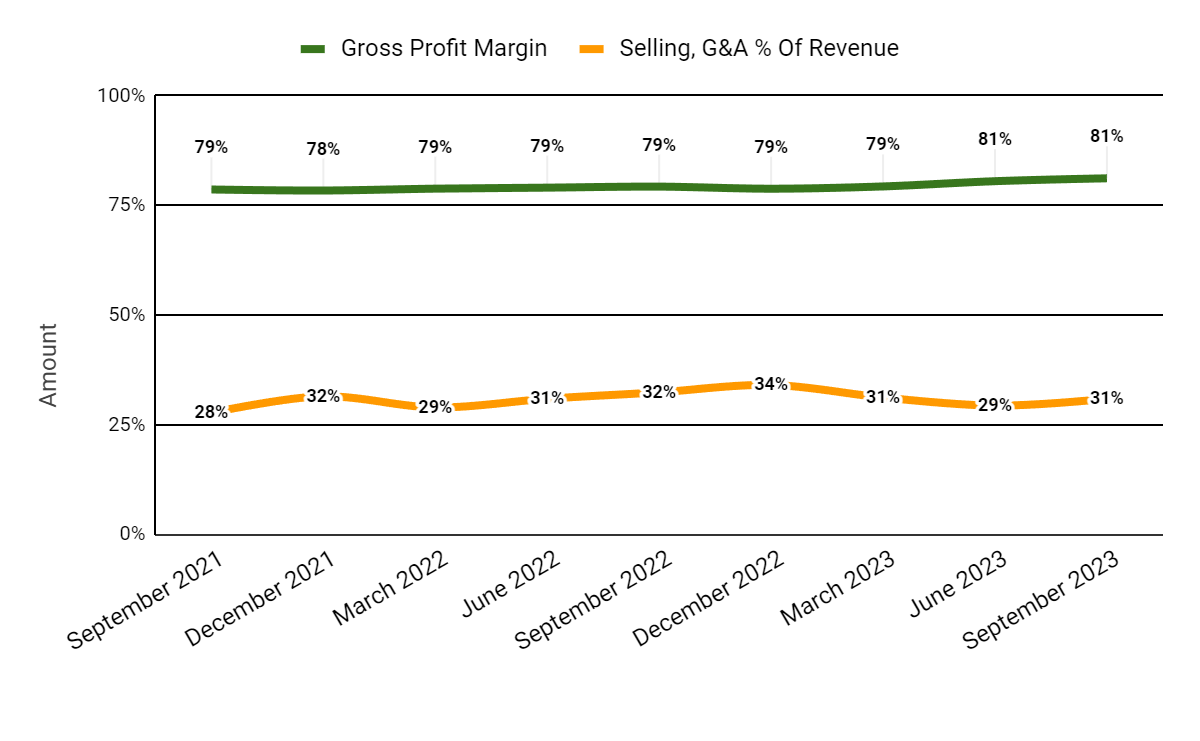

Gross profit margin by quarter (green line) has continued to grow as the firm increases its Partner revenue, while Selling and G&A expenses as a percentage of total revenue by quarter (orange line) have trended lower in recent quarters due to cost control efforts by management.

Seeking Alpha

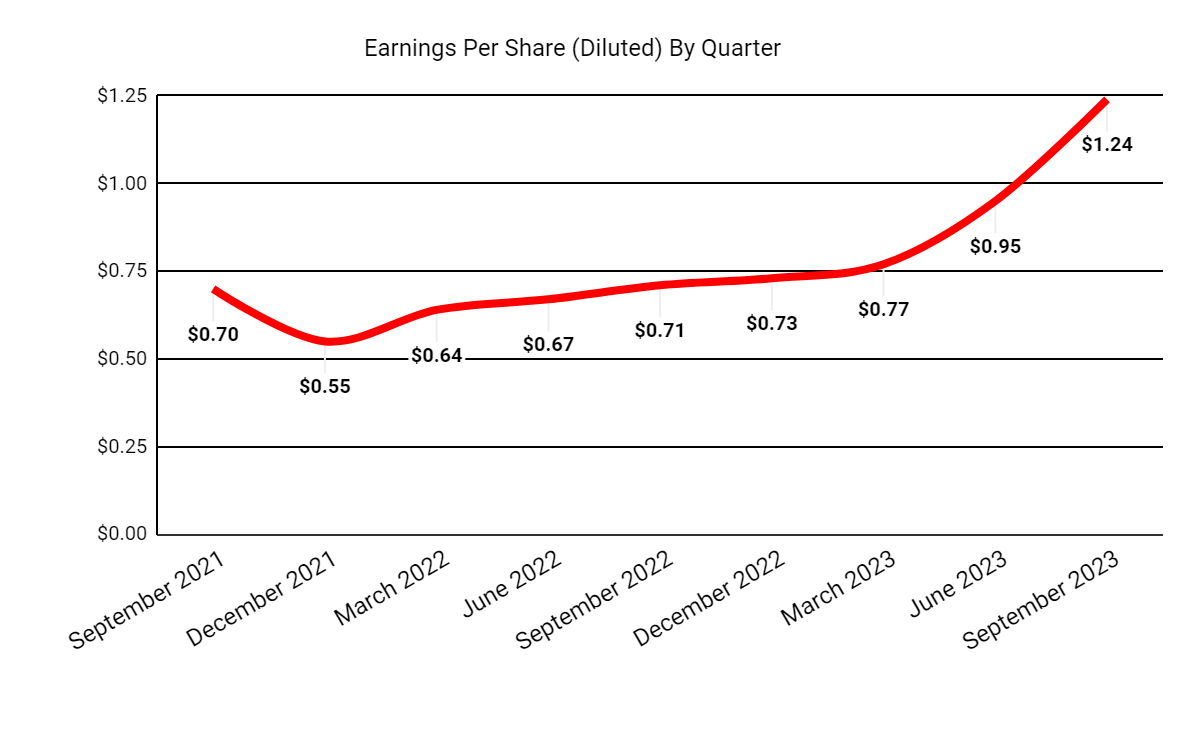

Earnings per share (Diluted) have been trending higher quite impressively in recent quarters as a result of growing revenue, higher gross profit, and lower SG&A expense ratios:

Seeking Alpha

(All data in the above charts is GAAP.)

Performance Metrics And Valuation

Qualys’ current valuation metrics are shown in the table below:

|

Metric |

Amount |

|

EV/Sales (“FWD”) |

11.7 |

|

EV/EBITDA (“FWD”) |

25.6 |

|

Price/Sales (“TTM”) |

12.9 |

|

Revenue Growth (“YoY”) |

15.4% |

|

Net Income Margin |

25.8% |

|

EBITDA Margin |

33.7% |

|

Market Capitalization |

$6,910,000,000 |

|

Enterprise Value |

$6,480,000,000 |

|

Operating Cash Flow |

$254,610,000 |

|

Earnings Per Share (Fully Diluted) |

$3.69 |

|

2024 FWD EPS Estimate |

$5.32 |

|

Rev. Growth Estimate (“FWD”) |

14.5% |

|

Cash Flow/Share (“TTM”) |

$6.36 |

|

Seeking Alpha Quant Score |

Strong Buy – 4.72 |

(Source: Seeking Alpha Data)

Notably, the company’s Rule of 40 performance has been quite strong, per the table here:

|

Rule of 40 Performance (Unadjusted) |

Q3 2023 |

|

Revenue Growth % |

15.4% |

|

Operating Margin |

30.7% |

|

Total |

46.1% |

(Source: Seeking Alpha Data)

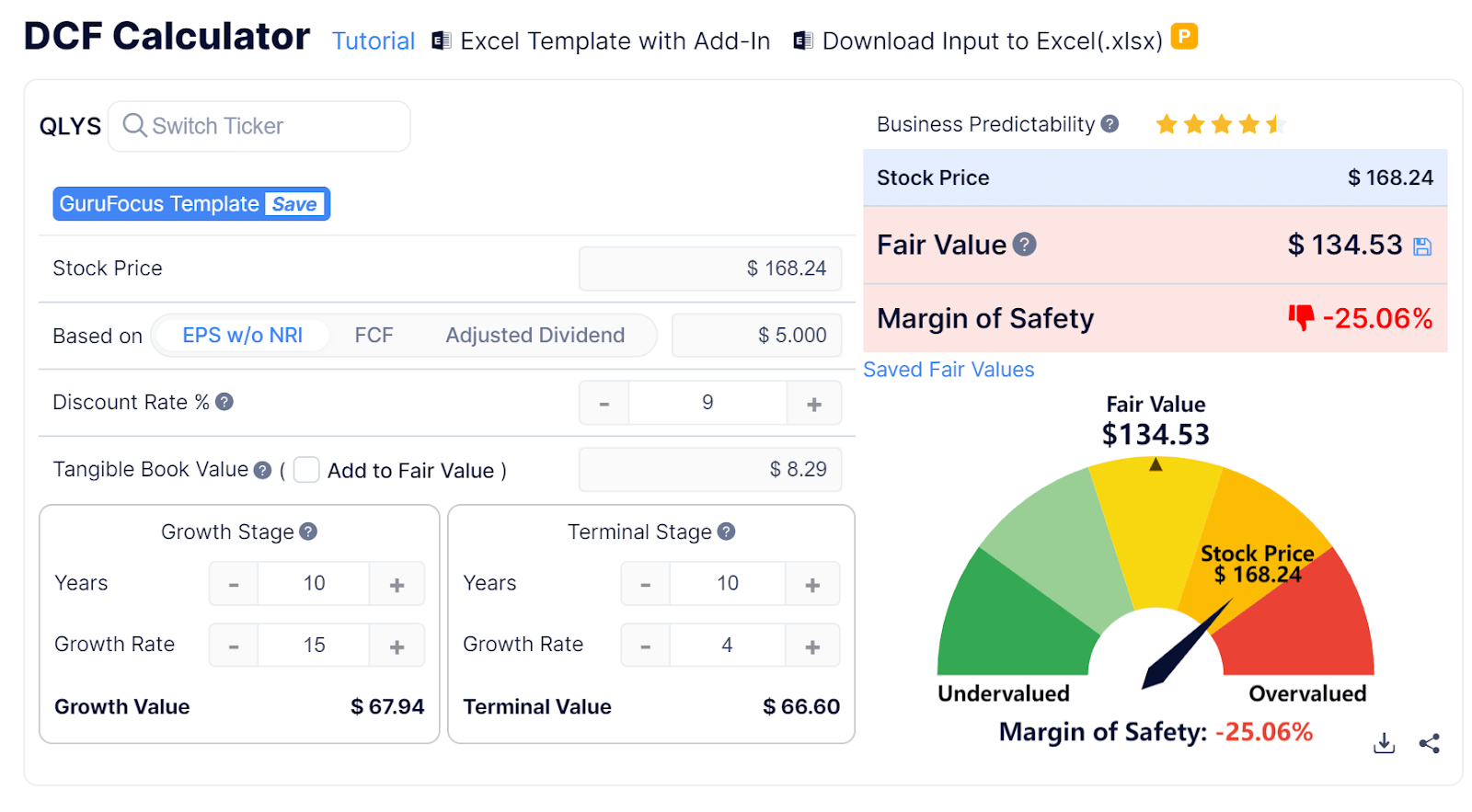

However, my discounted cash flow calculation indicates the stock is likely still overvalued, given a lower forward earnings outlook:

GuruFocus

My calculation assumes a generous forward growth rate of 15% and a lower discount rate of 9% and still comes up with a lower price target than Morgan Stanley’s revised target of $150.

So, I’m Bearish on Qualys despite the firm’s strong cash flow and previously good Rule of 40 performance.

While the company’s VMDR system is likely better than a more generic version that Microsoft will probably replace it with, Qualys will need to replace a 5-10% revenue hit with other major partnerships or through more expensive and time-consuming in-house, direct efforts.

Also, with a major partner like Microsoft bundling its own solution, it may present pricing pressures on independent solutions like Qualys’.

2024 will likely be a ‘rebuilding year’ as the company may spend more to continue development of its VMDR system, to differentiate it from the pack.

However, R&D spending has flattened in recent quarters at the mid-$27 million figure even as revenue has increased.

Other software companies have reduced their R&D spending as they seek higher profitability in the current market environment that rewards profitability over growth.

If cost of capital assumptions continue to trend lower, Qualys may benefit from a valuation multiple bump, but that macro possibility is outside management’s control.

Management may choose to reduce R&D spending to maintain profitability as revenue declines in 2024. If it does so, it may support the stock in the near-term, but reduce longer-term future growth potential as incumbents continue to develop their integrated solutions.

Much is up to how management responds to this significant setback. Will it spend more on revenue growth and R&D efforts, sacrificing profitability in the near term?

Or will it ‘hunker down’, continue to focus on Partner revenue channel growth and reduce R&D spending to improve profitability?

We should hear more next week when the company releases earnings for Q4 (February 12). I expect analysts to pepper leadership with questions about the effects of the Microsoft loss and its expected response on the firm’s earnings call.

In the meantime, my outlook is to Sell QLYS on revenue growth concerns and high valuation.

Q2 2024 Earnings Call Transcript")