oversnap

In May 2023, I initiated coverage for Qantas Airways (OTCPK:QUBSF, OTCPK:QABSY) with a buy rating. However, that call has not been a good one with the stock losing 16% compared to a 26% gain for the S&P 500. One of the reasons that Qantas stock has been under pressure is the scandals that it has been involved in as discussed in a previous report. In my view, Qantas did remain a buy despite the scandals on further recovery in travel demand in Australia and the Asia Pacific. In this report, I will be discussing whether the buy rating is still warranted.

Qantas Capacity Expansion Does Not Translate To The Bottomline

Qantas

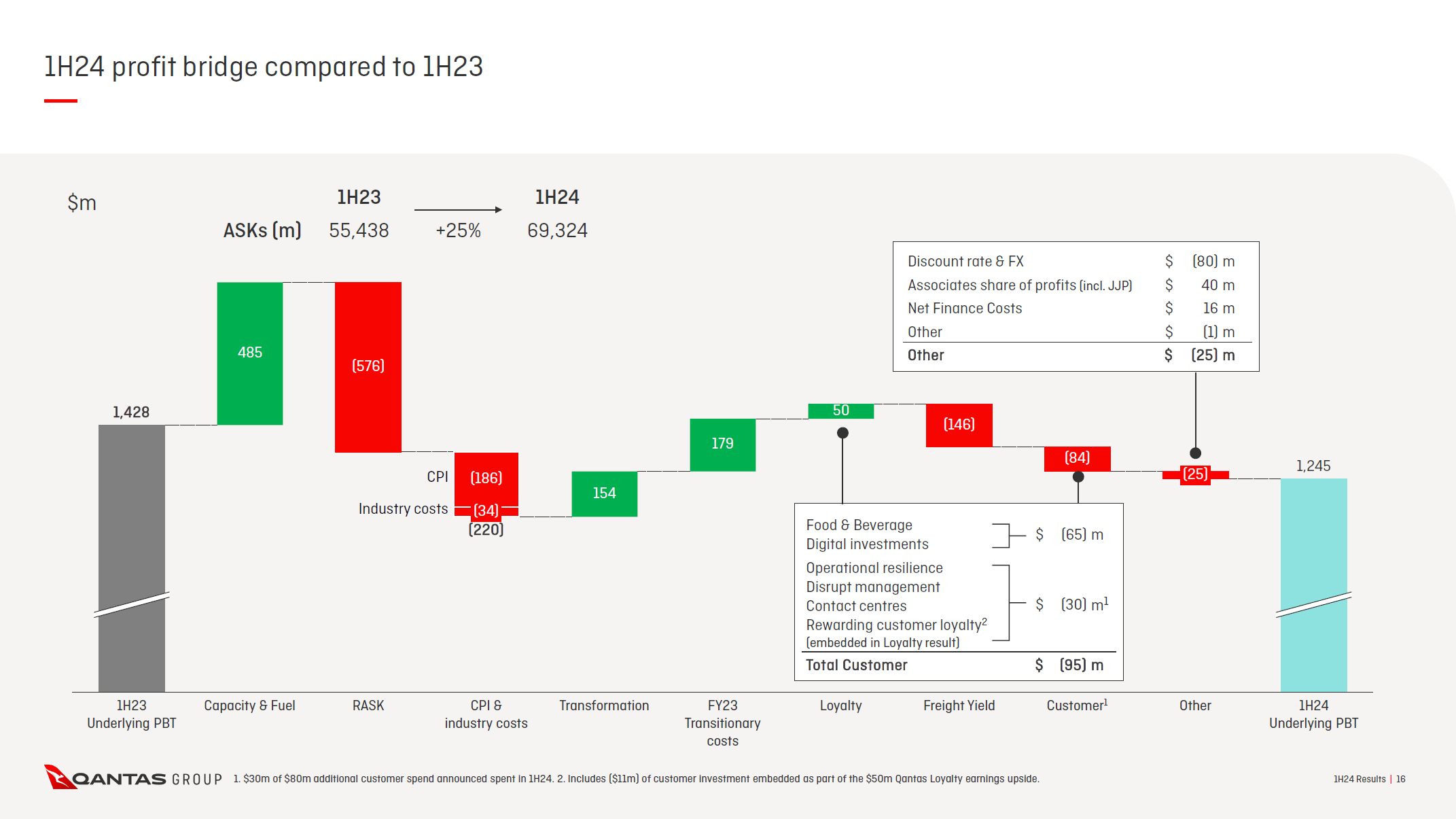

After having a look at the financial results for H1 2024, I can somewhat understand why Qantas stock is trailing the market. Pre-tax profit dropped almost 13% on a 25% increase in capacity. Higher capacity was fully offset by a reduction in unit revenues and a reduction in load factor for Qantas. Furthermore cost inflation and industry costs continue to be a drag on cost performance, but there is a positive offset from transformation initiatives and transition costs that are not present in FY24. Unsurprisingly, freight yields have also come under pressure even more putting a 146 million AUD drag on results.

On a unit basis, unit revenues reduced 10.7% with a 5.2% unit cost reduction excluding fuel with another 70 basis points in reduction driven by lower unit fuel costs. Overall, the results are not bad but we don’t quite see the recovery of demand translating to value and that might be driven by increased competition that pressures Qantas’ unit revenues. The lower unit revenues also did not increase the load factor, which dropped from 85.4% to 83.6%. In some sense, given continued demand strength, it does seem that Qantas is having some challenges effectively competing in the worst case and in the best case its capacity expansion has been unbalanced from unit-revenue management perspective.

Qantas Domestic operations saw its revenues increase by 3% on a 5% increase in capacity while EBIT declined 18%. EBIT was impacted by continued investments to improve customer experience, introduction costs of the Airbus A220 and phase out of the Boeing 717 and cost inflation. The 17% margin indicated a 4.5 percentage point decline, but still was well above the 12% margin for the group.

Qantas International and Freight saw a 14% boost in revenues on a 39% increase in capacity and a 4.2 percentage point reduction in load factor bringing the operating margin down from 12.2% to 7.4%. The lower results are primarily caused by lower freight service earnings as well as continuing declines in revenue per available seat-mile.

The Jetstar Group expanded revenues by 19% on a 27% increase in capacity with unit revenues being modestly lower and stable load factors. EBIT grew 84% to $325 million AUD.

The results posted by the Jetstar Group were most promising with higher profit, margin and load factor. For the Qantas network, we saw lower margins, lower load factors and lower profit. I believe that Qantas has not aimed to maintain unit revenue strength and instead has for capacity expansion to amortize costs and drive unit costs down. However, from margin perspective this has not really helped the airline.

Is Qantas Stock Still A Buy?

The Aerospace Forum

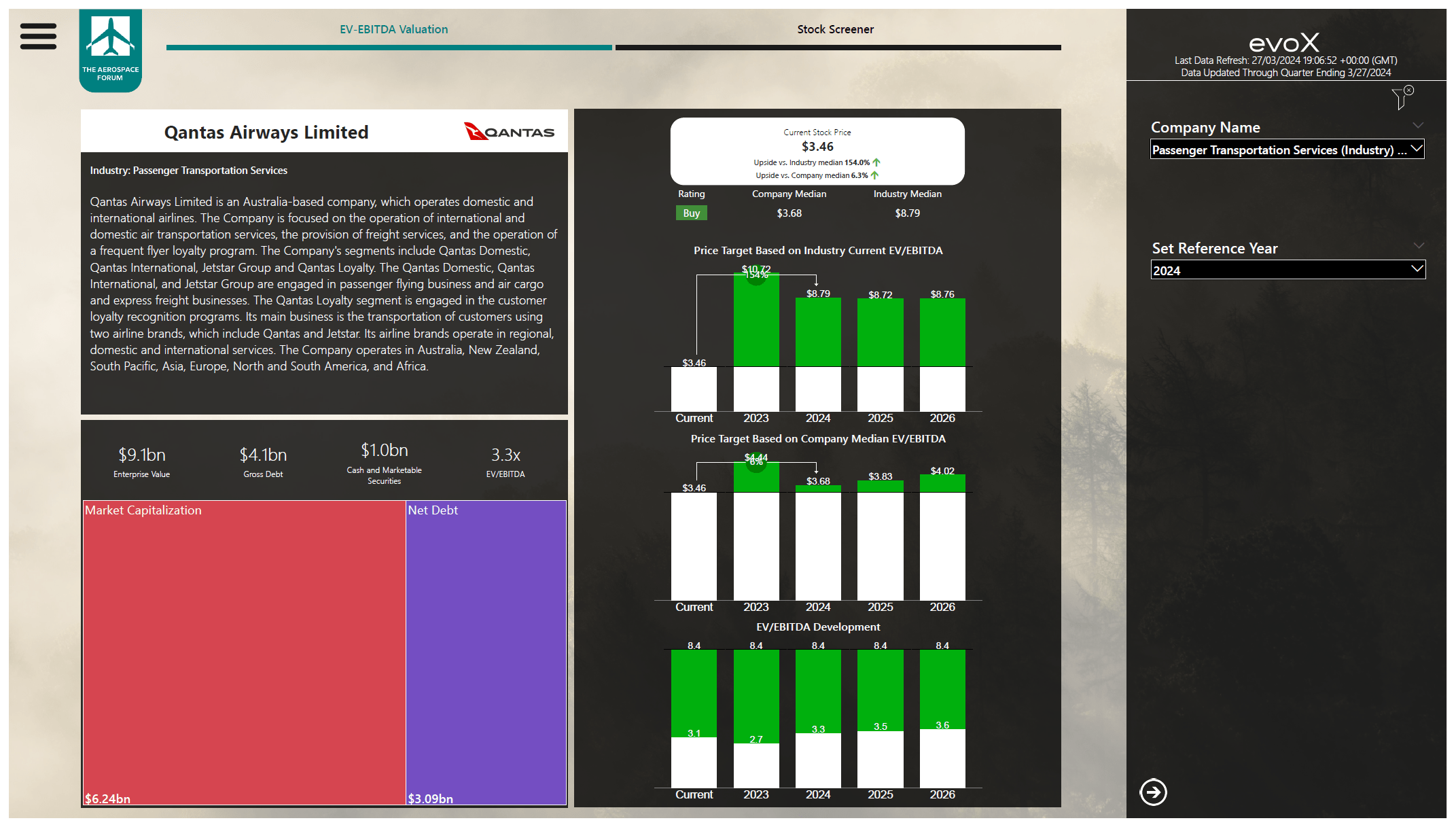

Valuing Qantas stock is quite challenging. The company expects to continue returning value to shareholders via share repurchases, but it also expects its net debt to grow which is also what our modeling would suggest based on attempts to keep cash on hands stable. Based on the company EV/EBITDA median there is little upside. The company expects to increase domestic capacity by around 7% in FY2024 and international capacity expansion of roughly 33%, which should be positive for unit cost development but will likely result in further pressure on unit revenues. I am maintaining my buy rating for the stock based on the low valuation of Qantas stock compared to the peer group. At a 5x EV/EBITDA valuation, there would be roughly 60% upside in which case the company would continue to trade below its peer group.

Conclusion: Qantas Focuses On Unit Cost Reduction

Qantas is not necessarily trying to keep unit revenues elevated and instead is looking to reduce its unit cost and that is what the H1 2024 results also showed. I am maintaining my buy rating for Qantas stock as I believe the stock is trading at a level that is far too low compared to its peers. However, given the expected rise in net debt, I am putting my buy rating on watch.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")