onurdongel/E+ via Getty Images

PubMatic (NASDAQ:PUBM) is going from strength to strength at the moment, with growth accelerating and margins improving. This is occurring despite the demand environment being fairly sluggish and could be due to some of the company’s newer products.

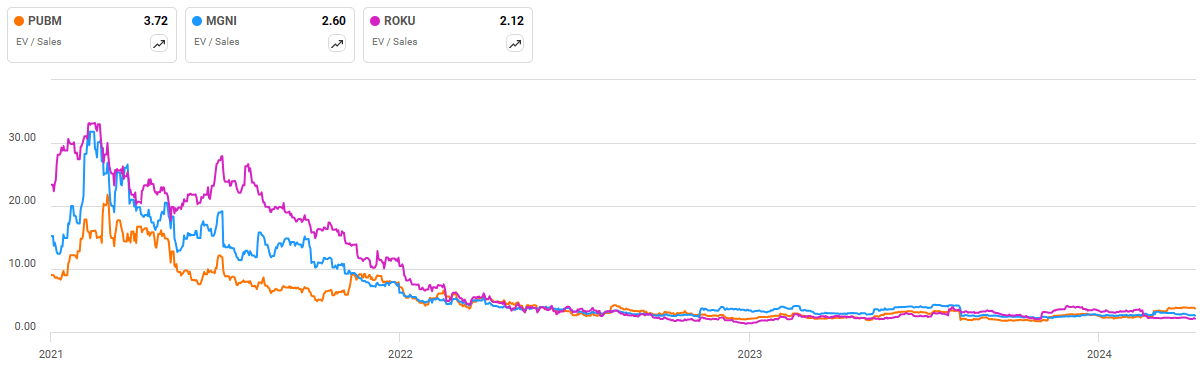

On an absolute basis, the stock still appears inexpensive given the company’s ability to generate free cash flow, leaving room for further upside. PubMatic is beginning to look expensive relative to peers, though, and the broader market also looks stretched. The path of least resistance is probably still up, provided that PubMatic’s financial results continue to improve.

The last time I wrote about PubMatic I suggested that the company’s near-term outlook was strong, although its competitive position was unclear. Since then, PubMatic’s growth has accelerated, and the stock is up over 35%. Given the strength of PubMatic’s portfolio of newer products, the company’s competitive position also looks much stronger than I had given it credit for.

Market Conditions

While the macro environment for digital advertisers still appears to be soft, conditions have stabilized, and many companies are now seeing stronger growth. Pricing remains a headwind, though, and this is likely to continue as companies like Amazon introduce ad-supported tiers to their streaming services. PubMatic expects future growth to be driven by a stable demand environment, industry consolidation, CTV and commerce media.

The business, technology, and personal finance categories increased by more than 30% in Q4 and travel, food and drink, automotive, health and fitness were all up double-digits. PubMatic also witnessed a recovery in the shopping vertical.

PubMatic’s recent performance looks particularly strong in comparison to Magnite (MGNI). Magnite’s CTV and desktop businesses were down slightly YoY in Q4, while growth from its mobile business was close to 20%. Magnite has guided to 10% growth in 2024, driven by CTV.

Roku (ROKU) saw a solid rebound in video advertising in the fourth quarter, which is expected to persist in Q1. CPG, health and wellness, and telecom were areas of strength, while categories like financial services and insurance were relatively soft. Roku expects its platform business to grow approximately 13% YoY in the first quarter.

PubMatic Business Updates

PubMatic continues to build out its product portfolio, helping the company to address the needs of buyers, sellers, retailers, and data providers. PubMatic now offers a range of solutions beyond ad monetization services, including:

- Header bidding wrapper software (OpenWrap)

- Buyer solutions like Activate

- Post-cookie targeting with Connect

- Commerce Media with Convert

These solutions help to make PubMatic’s platform stickier and increase differentiation. They also appear to be driving growth in what remains a challenging macro environment.

SPO

Supply Path Optimization refers to creating a more direct path from buyers to sellers, with less fees and greater transparency. This is currently contributing to consolidation in the SSP market, benefitting larger players like PubMatic.

SPO is a growth driver for PubMatic at the moment, particularly Activate, with a little over 45% of PubMatic’s total activity now coming from SPO. There remains a significant growth opportunity in this area, though. It is estimated that only one third of advertisers have engaged in SPO and that the average advertiser still works with 15-20 SSPs.

Figure 1: SPO Share of Total Activity on the PubMatic Platform (source: PubMatic)

CTV

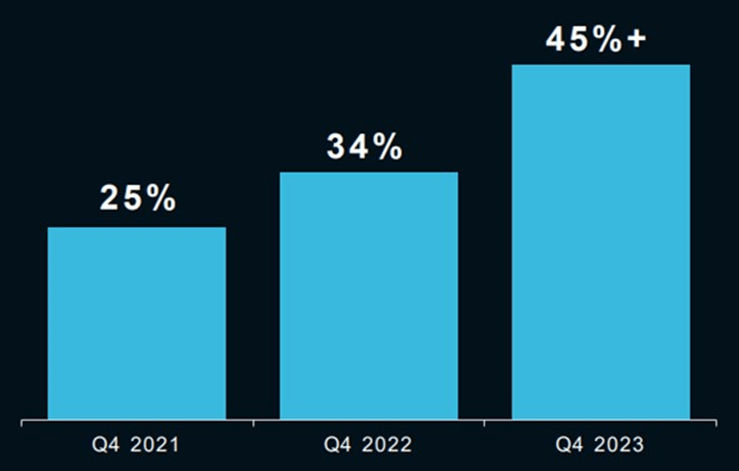

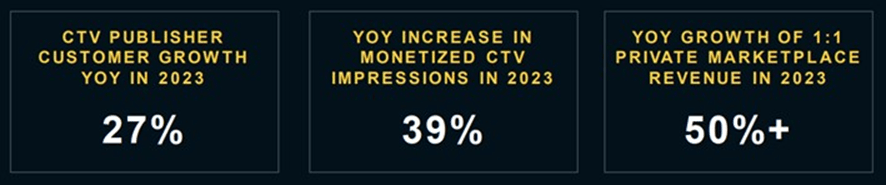

While CTV presents a large opportunity, it has been a challenging business over the past few years as ad budgets are significantly trailing viewers in the transition from linear TV to streaming. The introduction of ad supported services has also contributed to excess inventory and declining CPMs. While PubMatic’s CTV growth has been relatively modest, the company is making solid progress. PubMatic now has 271 premium CTV publishers on its platform, up 27% over 2022.

Buyers are seeking efficiency, programmatic advertising and measurable outcomes. Activate is an SPO solution that enables buyers to execute direct deals on CTV and premium video inventory through PubMatic’s platform. PubMatic believes that Activate’s addressable market is nearly 65 billion USD.

Figure 2: PubMatic CTV 2023 Financial Performance (source: PubMatic)

Privacy

PubMatic offers a number of solutions to help organizations as the digital advertising market becomes more privacy focused, including:

- Connect

- Identity Hub

- Privacy Sandbox

PubMatic’s Connect aims to simplify the implementation and management of new identity solutions. Connect is ramping, with the number of revenue-generating Connect customers increasing 20% sequentially to over 100. This could be a result of buyers and publishers preparing for the end of third-party cookies.

Identity Hub is also performing well, with several hundred publishers having deployed Identity Hub. Identity Hub helps publishers to convert user data into a variety of alternative IDs. Over 80% of impressions on PubMatic’s platform now have alternative signals available to buyers, and PubMatic estimates that when alternative IDs are present, publisher revenue increases by 16%.

Convert is a Commerce Media solution which addresses use cases like sponsored listings, audience extension and deal ID generation. It helps customers turn media inventory and data assets into scalable revenue streams. Data access and control are important capabilities for commerce media, both areas where PubMatic already has market leading solutions.

Financial Analysis

Revenue growth accelerated to 14% YoY in Q4, which drove strong profit and cash generation. Excluding Yahoo, fourth quarter revenue growth accelerated to 19%. Emerging revenue streams, like Activate and OpenWrap, added approximately 3% to growth in the fourth quarter. These revenue streams are expected to contribute mid-single-digit percentages of revenue in 2024, more than doubling YoY.

Omnichannel video revenue increased 7% YoY, driven by a 30% plus increase in monetized impressions, somewhat offset by CPM declines. Video CPMs have reportedly been relatively stable since August 2023, though.

Display revenue increased 9% YoY, led by Mobile display growth of more than 20%. Excluding Yahoo, total mobile and desktop display revenue grew 27%. Strong growth in impressions was also offset by CPM headwinds.

PubMatic believes that it is in the early stages of a multi-year growth period, driven in large part by market share gains. Shifts in ad budgets to CTV and Commerce Media, continued industry consolidation, and a stable demand environment should also support growth.

PubMatic’s early Q1 results appear solid, with a double-digit increase in monetized impressions observed. CPMs were also in line with expectations, and emerging revenue stream growth remains robust. PubMatic is expecting 61-63 million USD revenue in the first quarter, representing 12% growth at the midpoint. For the full year, revenue growth is anticipated to be in excess of 10%, or over 12% excluding Yahoo.

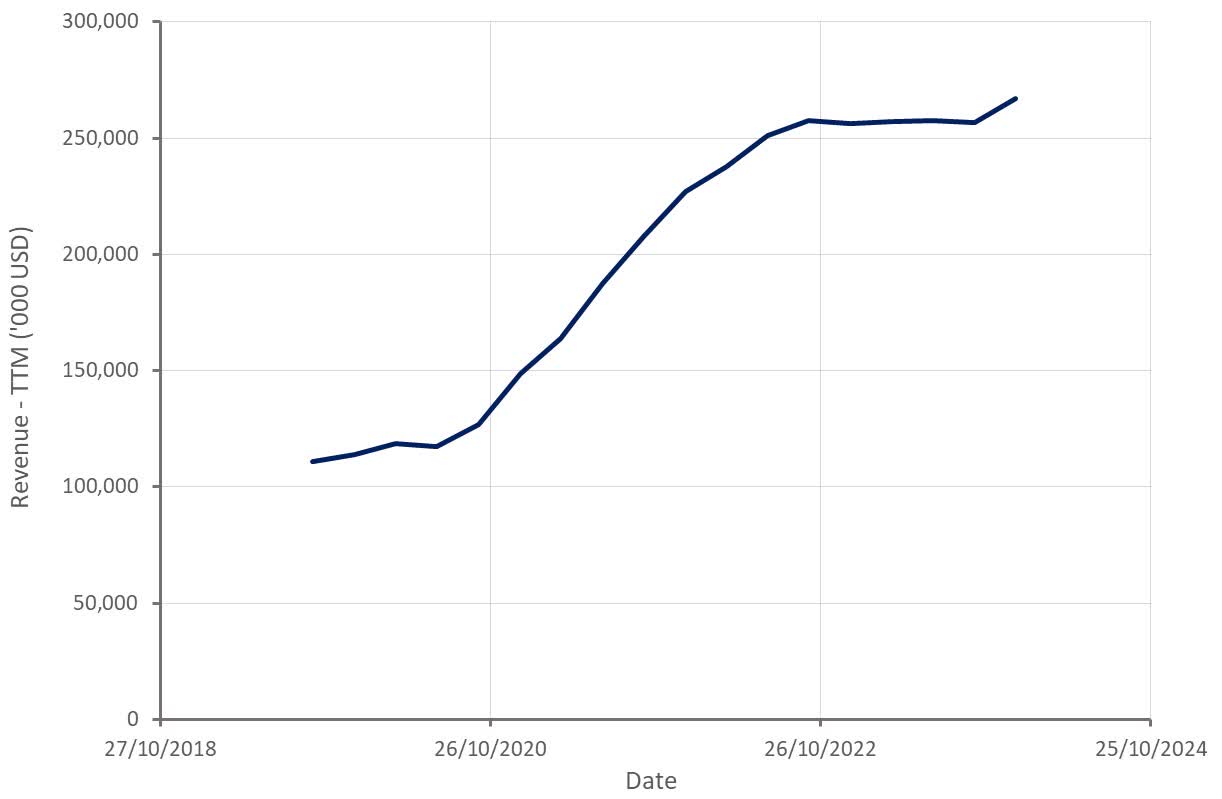

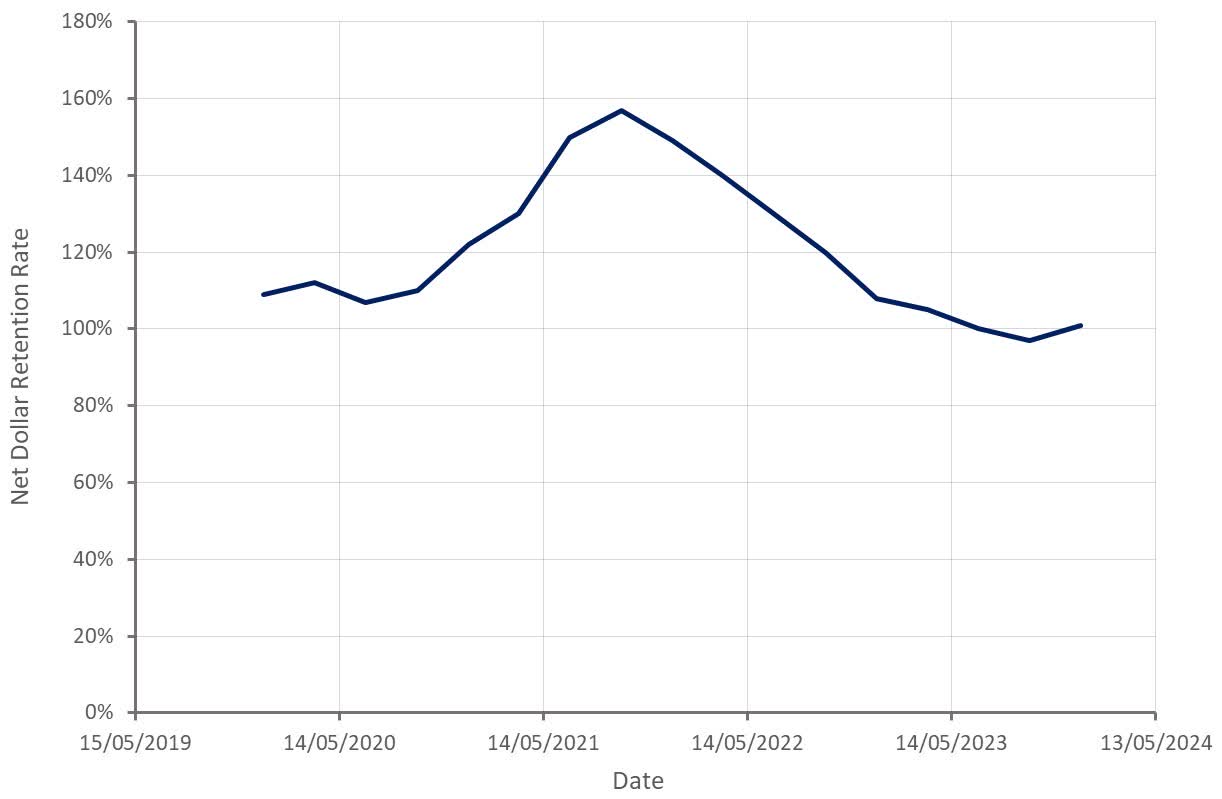

Figure 3: PubMatic Revenue (source: Created by author using data from PubMatic) Figure 4: PubMatic Net Dollar Retention Rate (source: Created by author using data from PubMatic)

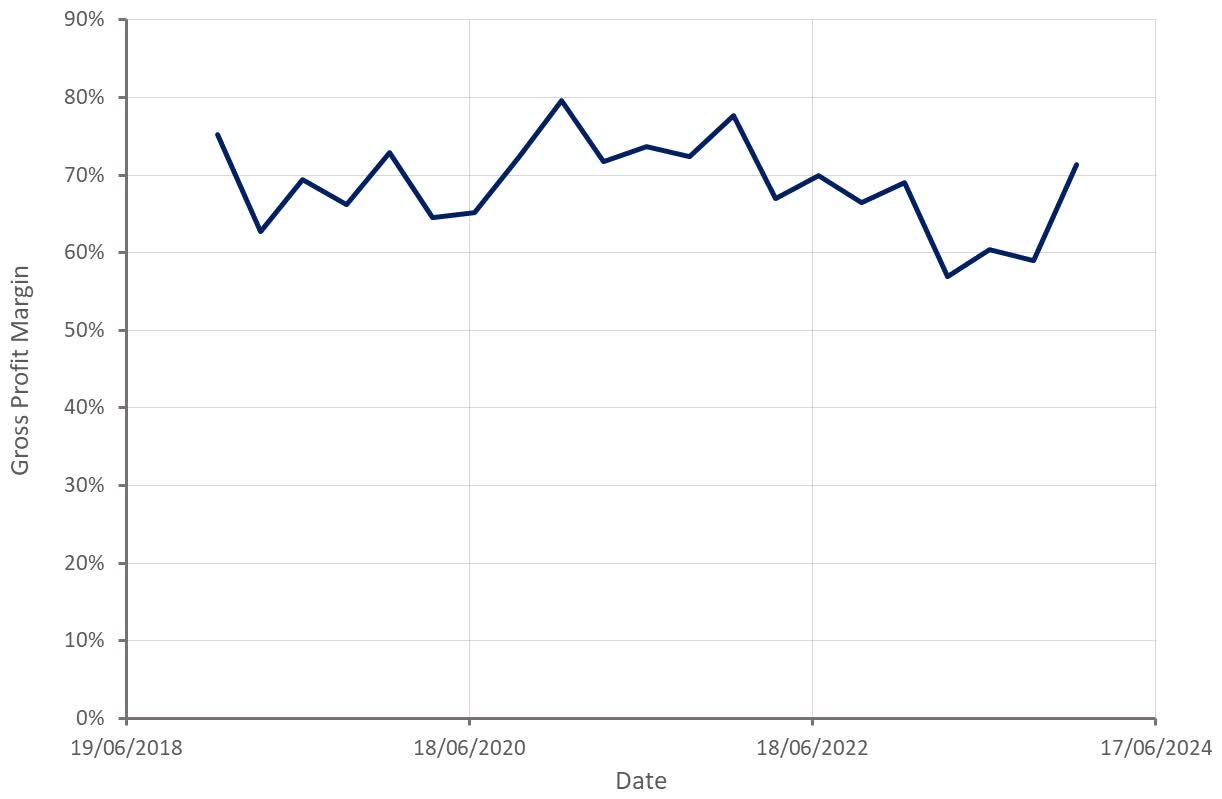

An increased focus on efficiency going forward should lead to margin improvements, along with operating leverage. In particular, PubMatic owns and operates its own infrastructure, providing cost of revenue leverage. For example, cost of revenue per impression processed declined 8% YoY in Q4. This hasn’t been apparent over the past few years due to pricing headwinds but could now be changing, with PubMatic’s gross profit margin up significantly in the fourth quarter.

Figure 5: PubMatic Gross Profit Margin (source: Created by author using data from PubMatic)

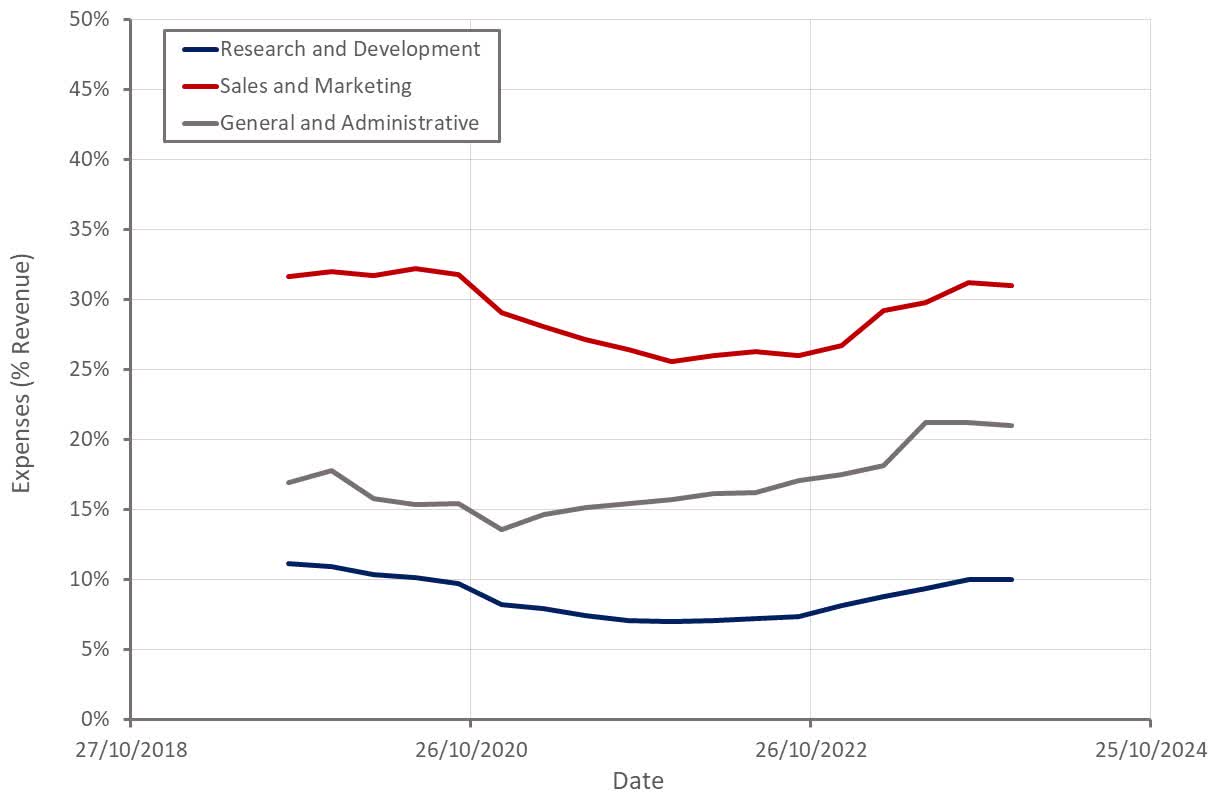

PubMatic plans on increasing its headcount by over 150 people in 2024 in order to capitalize on the opportunity ahead of it. Key investment areas include product development (post-cookie solutions and performance advertising) and sales. PubMatic plans on growing its buyer-focused sales and customer success team by 50% to support its SPO and Activate businesses. The company also plans on hiring more salespeople to support its OpenWrap software, post-cookie targeting and commerce media businesses.

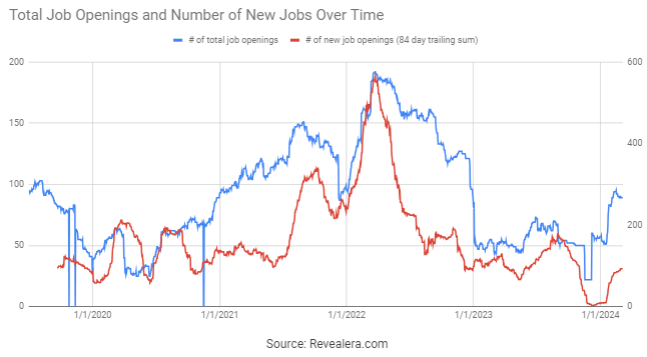

Generative AI is reportedly already contributing to PubMatic’s engineering productivity. The company also anticipates a 15-20% increase in engineering productivity in 2024, led by areas like automated software testing.

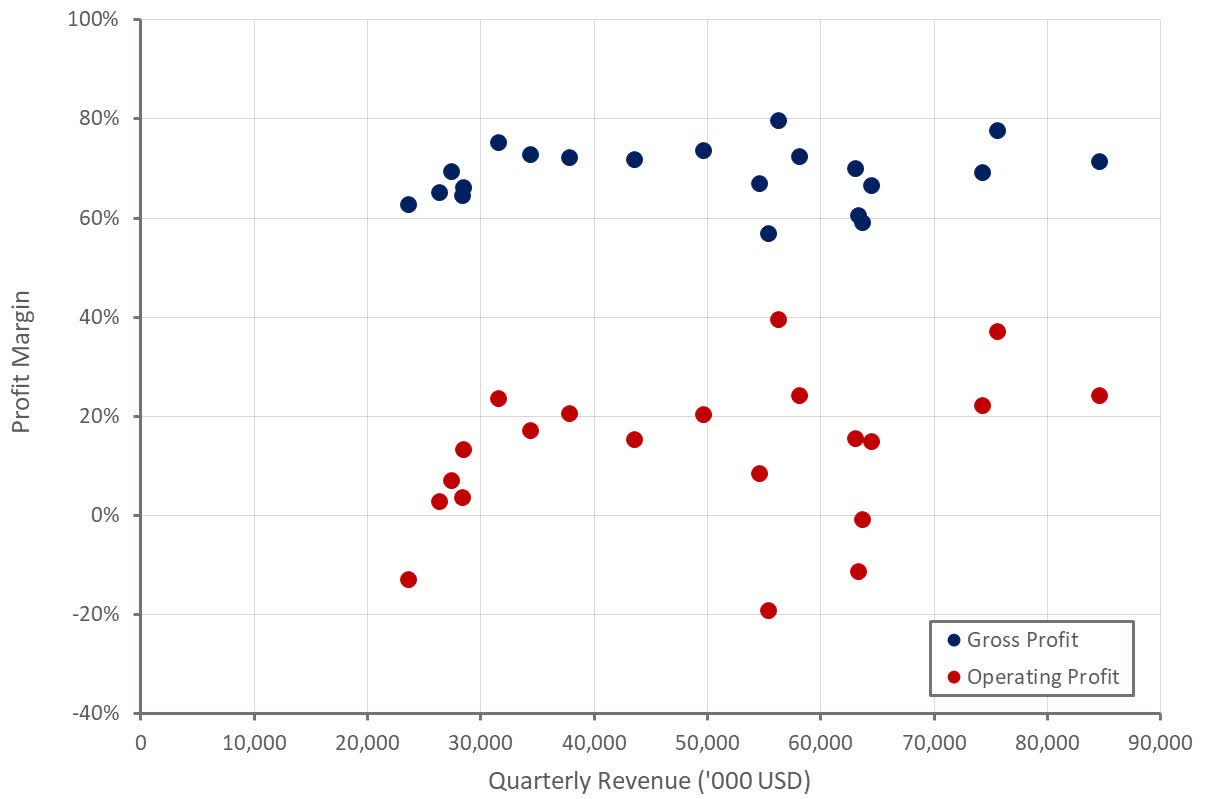

Figure 6: PubMatic Profit Margins (source: Created by author using data from PubMatic) Figure 7: PubMatic Operating Expenses (source: Created by author using data from PubMatic) Figure 8: PubMatic Job Openings (source: Revealera.com)

Conclusion

My concern with PubMatic has been how sustainable the company’s business is. Given the infrastructure necessary to operate an SSP, scale is potentially important, and in this regard, PubMatic is at a disadvantage to Magnite. I am less concerned about competition than I previously was, but the overall strength of the SSP business model remains questionable. DSPs like The Trade Desk (TTD) could eventually disintermediate SSPs, and there is an ever-present risk of commoditization.

Given PubMatic’s growing success with solutions like Activate, Connect and Convert, I believe the company’s competitive position is strengthening. If SSPs can demonstrate that their businesses are not susceptible to disruption, valuations should rise substantially. While PubMatic’s share price is up significantly over the past 6 months, the company’s valuation is still reasonable given potential cash flows. Supporting this, PubMatic repurchased 4 million shares for 59 million USD in 2023 and wants to expand repurchases going forward.

Figure 9: PubMatic EV/S Multiple (source: Seeking Alpha)

Q2 2024 Earnings Call Transcript")