Scott Olson

Procter & Gamble Company (NYSE:PG) has had a tough 2023, but the stock could be ready for a reversal heading into 2024.

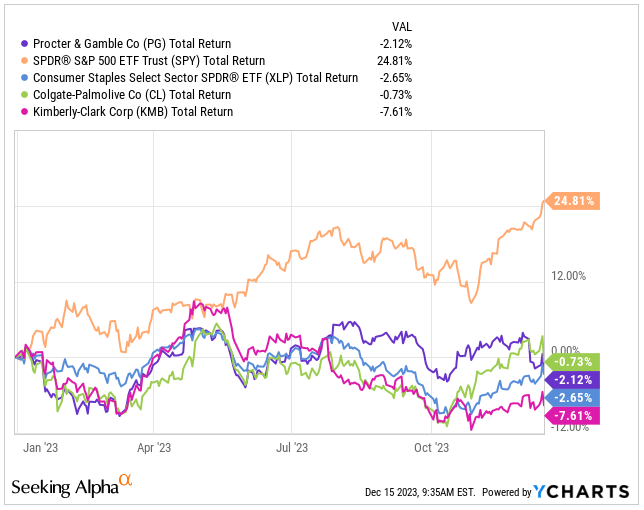

PG is one of the world’s leading fast-moving consumer goods companies, with 65 brands serving more than 5 billion consumers across all continents, yet, shares of PG have fallen 4.6% this year, a result that reflects sentiment far more than fundamentals.

The S&P 500 index’s rally following 2022’s bear market saw investors reject anything remotely defensive, including consumer-staples stocks. Higher bond yields also made the sector’s dividends less attractive, with short-term money markets yielding north of 5%.

Total Return (Seeking Alpha)

But as 2023 comes to an end, sentiment might be about to turn. As a result of the highly anticipated FED’s pivot signaled this Wednesday, bond yields have fallen from their peaks, while concerns about economic growth are slowly returning, something that could make staples a must-own once again.

If you are one of the more cautious investors and expect 2024 to year of sub-par growth, or perhaps worse, mild recession, PG could a good place to park your money, providing very healthy 2.46% dividend yield with a growth and recession resistant business model.

By saying ‘a recession-resistant business model,’ I mean a company whose products are highly needed no matter the economic cycle. PG ticks all the boxes, and as a cherry on top, you get strong pricing power among everything else. Some other companies which I put into the same box would be PepsiCo (PEP), Coca-Cola (KO), and Colgate-Palmolive (CL).

While we should not be expecting significant top-line growth, PG’s EPS growth appears ready to speed up as investments made over the last years start to pay off and positively impact the bottom line.

From my standpoint, PG is one of the most durable businesses out there and if the economy indeed slows down next year, this is a place to be.

Let me show you why I admire their business model.

Business Update

PG’s products are crucial for people’s daily health, hygiene, and cleaning needs. PG saw strong growth in the Q1 FY24 due to its well-performing brands and effective strategies, leading to increased sales.

PG’s reported net sales of $21.9 billion, showcasing 6% YoY boost. Organic sales, which excludes the impacts of foreign exchange and acquisitions and divestitures, increased 7%. This rise came from a 7% boost in pricing and a 1% boost from a positive product mix, offsetting a 1% reject in volume.

All segments of the company experienced growth in sales:

- Beauty by 5%

- Grooming and Fabric & Home Care by 9% each

- Health Care by 10%

- Baby, Feminine & Family Care by 7%

Diluted net earnings per share were $1.83, an boost of 17% versus prior year.

Q1 FY24 (PG IR)

Looking ahead to fiscal 2024, PG is optimistic based on its strong first quarter performance. PG now expects overall sales to grow by 2-4% and organic sales to rise by 4-5%.

The company also forecasts a 6% to 9% boost in reported EPS, aiming for a range of $6.25 to $6.43, compared to $5.90 per share in fiscal 2023.

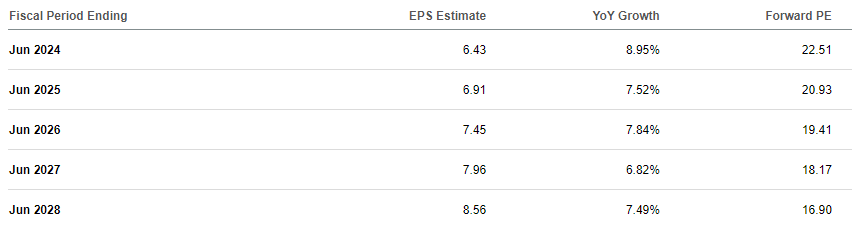

This falls in line with analysts’ forecasts for fiscal 2024. Yet, the strong performance isn’t anticipated to fade after this year. It’s quite reasonable to expect PG to preserve an EPS growth rate of around 7.5% up until 2028.

EPS Forecast (Seeking Alpha)

This strong EPS growth is partially drive through enhanced margins, as PG has focused on productivity and cost-saving measures. PG continues to invest in its businesses while countering macro cost challenges, ensuring growth in both revenue and profit. Their efforts in cost savings and efficiency improvements are visible across their operations.

The implementation of the supply chain 3.0 program has allowed PG to better capacity, flexibility, transparency, and productivity. They expect reaping benefits of $800 million after tax in fiscal 2024 due to favorable commodity costs.

Keep in mind, PG holds an “AA-” rating from S&P Global, marking it as the second-highest rating attainable for a company.

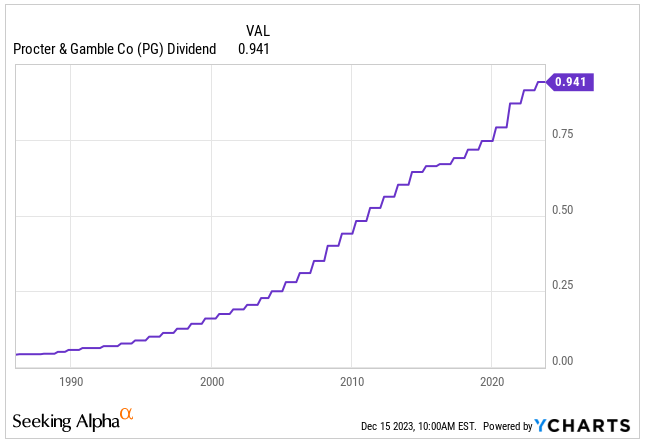

133 Years Of Paying Dividends

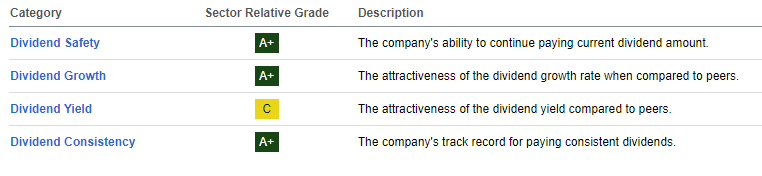

PG remains focused on its commitment to rewarding shareholders through dividend payments and share repurchases.

This commitment also translates to an action and that is also one of the reasons, why PG scores 3 out of 4 straight A+ grades from the Seeking Alpha.

Dividend Grade (Seeking Alpha)

The company returned $3.8 billion of value to its shareholders in first-quarter fiscal 2024.

This included $2.3 billion of dividend payouts and $1.5 billion of share buybacks.

Considering the current dividend stands at $0.941 per share or 2.46% yield the company intends to make dividend payouts of more than $9 billion, along with share repurchases of $5-$6 billion in fiscal 2024, representing roughly 1.7% of the total market cap.

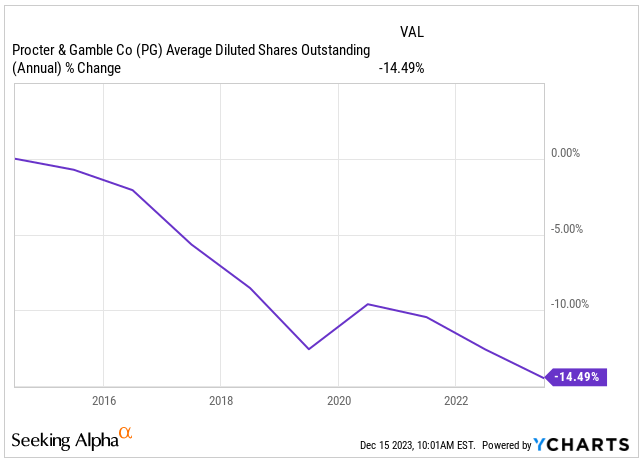

That’s all on top of the already 14.5% reduced shares cost over the past decade.

Shares Outstanding (Seeking Alpha)

With the last dividend boost of 3% earlier this year, this boost marked the 67th consecutive year that PG has increased its dividend and the 133rd consecutive year that PG has paid a dividend since its incorporation in 1890.

While the 5 year DGR is only 5.63% CAGR it holds a crown for one of the longest dividend streaks ever.

PG sports also a healthy dividend payout ratio of 61%, and a free cash flow yield of 3.9%.

Dividend Per Share (Seeking Alpha)

Valuation

All of these favorable attributes such as:

- Recession resistant business model

- Reasonable high-single-digit EPS growth

- Non-cyclical business

- 133 years of consecutive dividends

… come at a price.

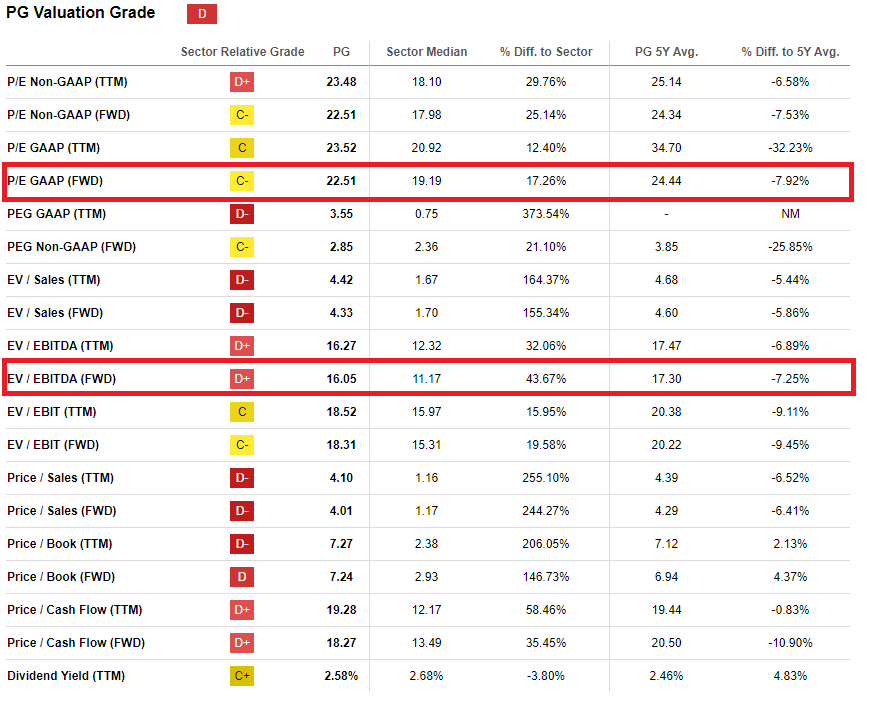

PG is not cheap by any means. For a consumer staple company, its trading at a 17.3% premium to the sector median.

Yet, I am of the opinion that its worth to pay for a quality over quantity and that is why I think Forward PE ratio of 22.51x its fiscal 2024 earnings can be justified and its actually close to 8% below its 5-year averages.

Forward EV/EBITDA confirms the discount to its fair price with 16.05x being 7.3% lower than the historical averages.

Even though it appears the PG is trading at a discount of at least 7% to its fair value, I am not going to claim that it is a cheap.

Especially for a consumer staple company, but what I am going to say is that today’s valuation is reasonably better than it was in the last 5 years and the company with its improvements in the supply chain and pricing power is firing on all cylinders and I think if you are looking for a defensive addition to your portfolio, this may be a good time to pull the trigger.

Valuation Grade (Seeking Alpha)

If we consider PG’s expected growth in EPS of about 7.5% between 2024 and 2028 and factor in its historical Forward PE ratio of 24x, we might expect PG’s stock to hit around $210 by the end of 2028.

This projection suggests an approximate 8% boost in stock value annually over the next 4 years. Additionally, when we consider the dividend yield of approximately 2.5%, it seems reasonable to expect PG to offer returns exceeding 10%, which aligns closely with what I expect from my other favorite consumer staple company, PepsiCo and the market (SPY) alike.

| Fiscal Year | 2024 | 2025 | 2026 | 2027 | 2028 |

| Revenue (b) | $ 85.0 | $ 88.2 | $ 92.0 | $ 96.2 | $ 100.9 |

| Revenue Growth | 3.6% | 3.7% | 4.3% | 4.6% | 4.9% |

| EPS | $ 6.4 | $ 6.9 | $ 7.5 | $ 8.0 | $ 8.6 |

| EPS Growth | 9.0% | 7.5% | 7.8% | 6.8% | 7.5% |

| Forward PE | 24.0 | 24.0 | 24.5 | 24.5 | 24.5 |

| Stock Price | $ 154 | $ 166 | $ 183 | $ 195 | $ 210 |

Conclusion

Procter & Gamble is among the most durable businesses globally, boasting a non-cyclical, recession-proof business model.

The company faced challenges in 2023 as rates surged, leading people to favor bonds and money markets over what I’d call ‘dividend darlings.’

However, as market dynamics shift and the Fed’s pivot gains traction in 2024, it’s likely that yield-seeking buyers will return, benefiting companies admire PG.

Currently, PG offers a 2.46% yield and has consistently paid dividends for 133 consecutive years, holding the status of a dividend king for the past 17.

While I don’t consider PG’s valuation cheap for a consumer staple company, I believe today presents a good opportunity knowing the stock is trading at a 7% discount to its fair value.

Q2 2024 Earnings Call Transcript")