Sean Anthony Eddy

Procore Technologies, Inc. (NYSE:PCOR) is a construction management software company that offers a cloud-based platform to help construction companies manage their projects more efficiently. The platform includes tools for project management, quality and safety, financial management, and more. In FY 2023, PCOR surpassed the $1 billion ARR mark.

Procore generates revenue through subscriptions to its product, offering unlimited users to encourage all project participants to use the platform. Though it offers fixed pricing, the total price is partly determined by the construction volume managed on the PCOR platform.

Since going public in May 2021 at $86 per share, PCOR has seen some ups and downs. Price over the past 52 weeks ranges from $48 to $78. Currently trading around $76, it sits slightly below its debut day price for an all-time return of roughly -16%.

I initiate my coverage with a buy rating. My modeled 1-year target price of $88.7 presents a projected 17% upside from today’s price of $75.9, suggesting an attractive upside.

Financial Reviews

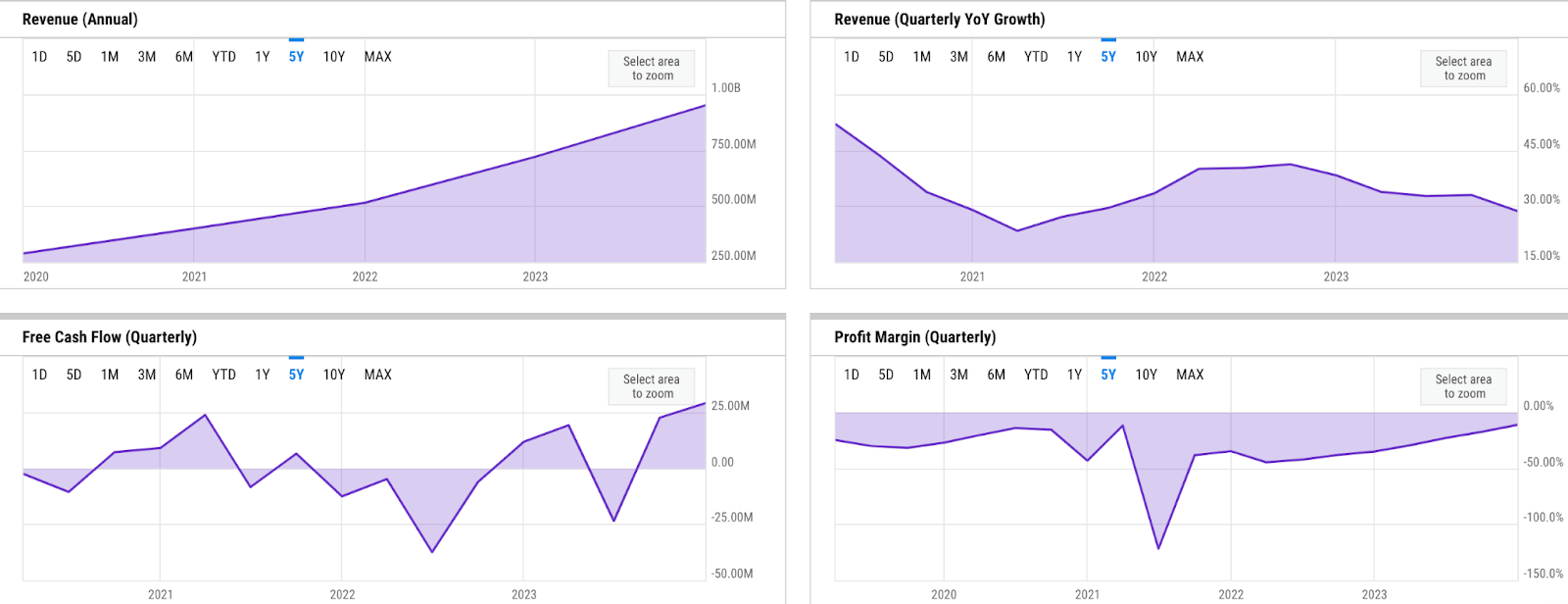

key metrics (ycharts)

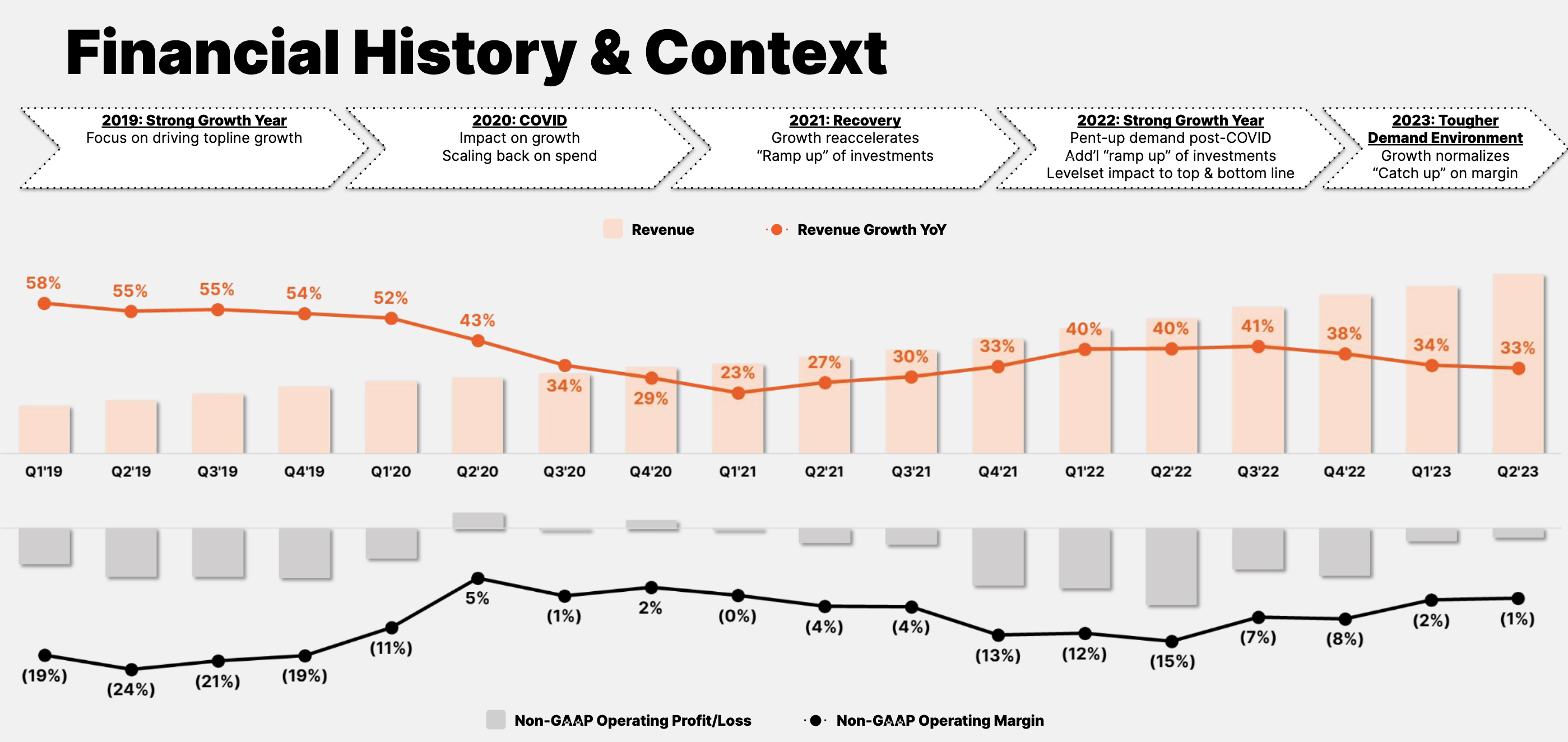

PCOR has decent fundamentals. Revenue growth has been between 20% – 40% YoY in the past five years, a solid performance by any standard. More importantly, it demonstrates resilience amid recent macro challenges. PCOR has not had positive net earnings over the same period, but the net loss margin has narrowed significantly. Upon reaching the lowest point of over -50% in 2021, the net loss margin continued trending upward and reached -20% in FY 2023.

Cash flow generation has been strong. While PCOR also occasionally realized quarterly FCF losses in any given FY, the overall outlook is positive due to two things, in my opinion. First off, recent trends point in a positive direction. In the most recent quarter, for instance, FCF reached its 5-year high of $29 million, a 30% growth sequentially from the previous quarter, suggesting an upward trend.

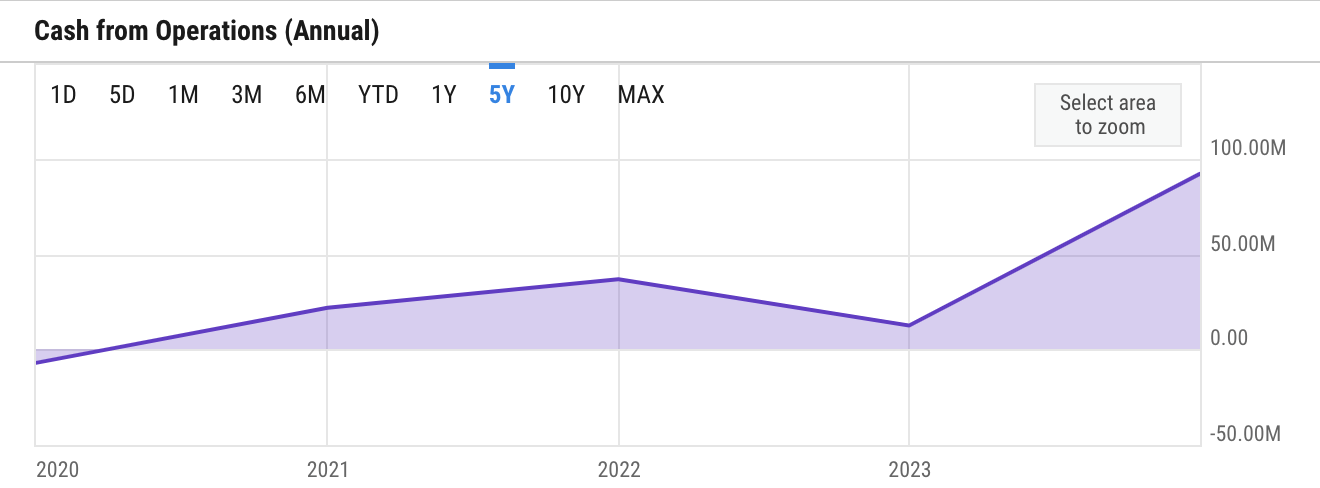

OCF (ycharts)

Secondly, PCOR’s operating cash flow / OCF has been expanding significantly, demonstrating sustainability of its business model. OCF was still in the red just five years ago. However, it continued trending upwards, and In FY 2023, PCOR delivered over $92 million of OCF, almost 8x more than the previous FY.

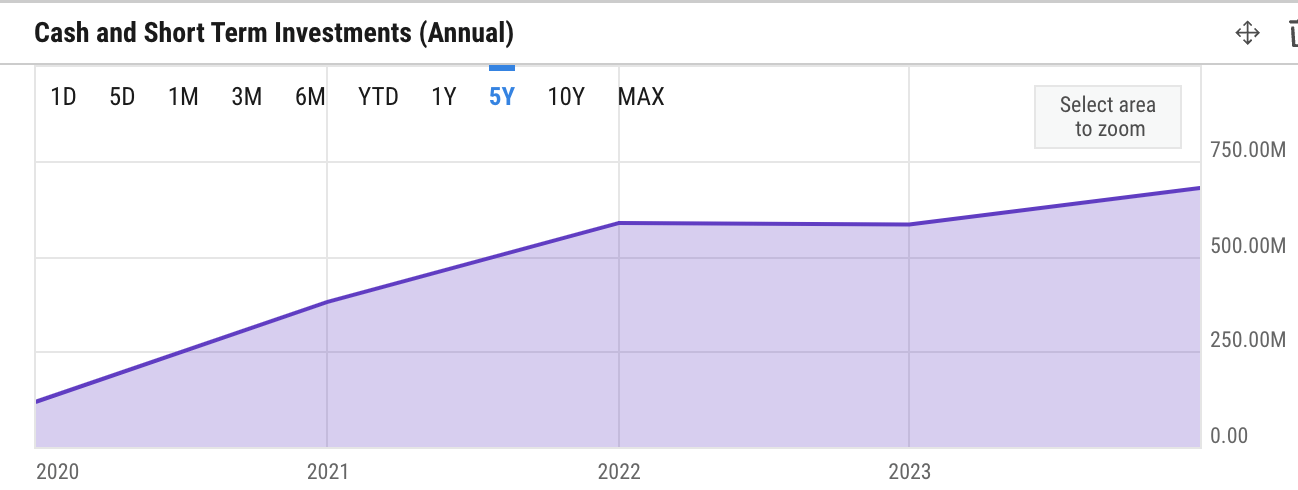

cash (ycharts)

As a result, PCOR promises financial stability, even under a relatively high growth outlook, in my opinion. The balance sheet is very solid. Upon raising over $700 million from the public offering in 2021 and deploying the capital, cash and short-term investments are steady and even on an upward trend. PCOR finished FY 2023 with $678 million in liquidity with no debt.

Catalyst

There are a few identifiable catalysts that could help PCOR maintain its solid revenue growth and profitability outlook in 2024 and beyond.

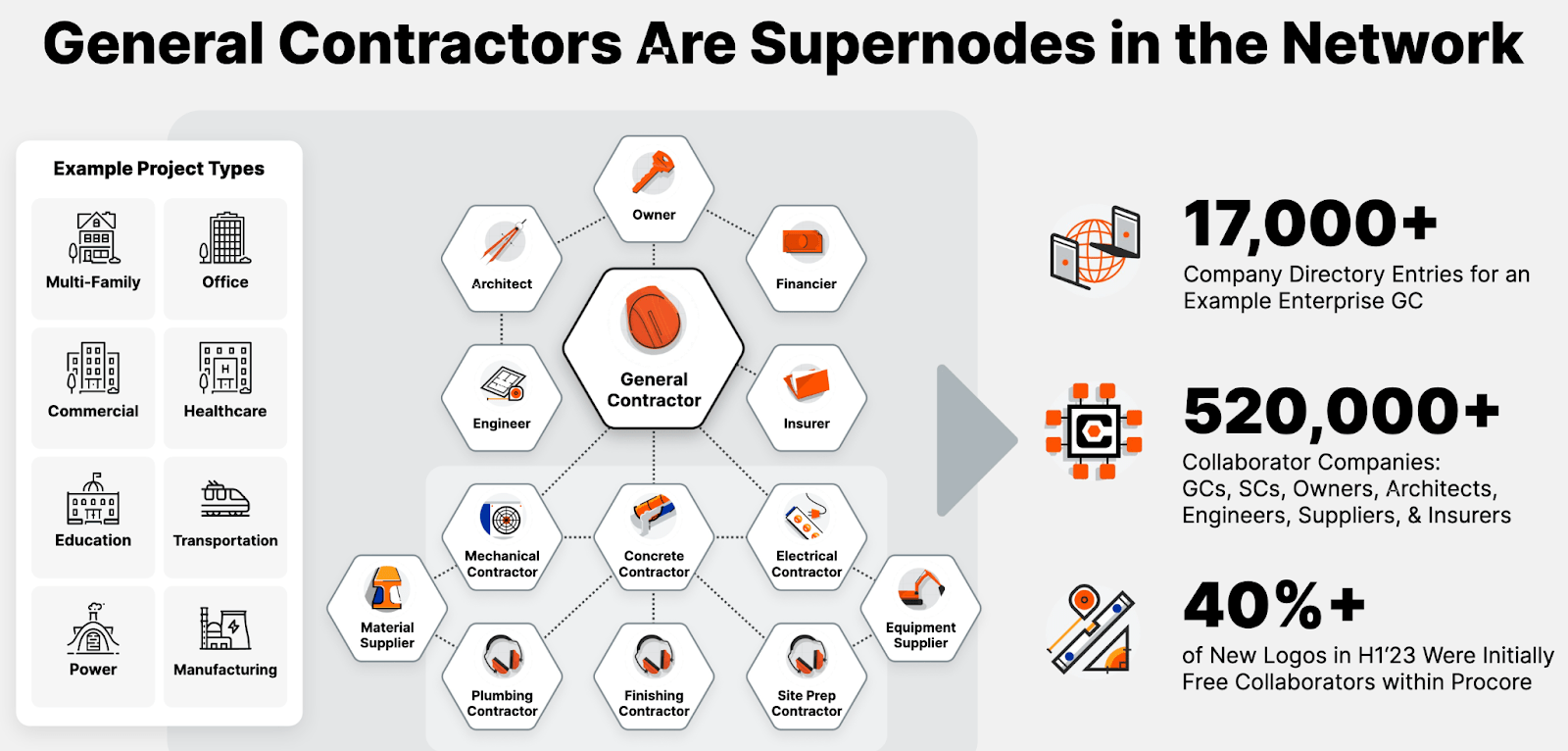

network effect (company presentation)

PCOR’s business model, which enables its general contractor / GC customers to invite their network of architects, specialty contractors, and engineers to collaborate for free inside its cloud platform, delivers a proven network effect that unlocks broader awareness of its offerings and future conversion opportunities. With 40% of new customer lands in the first half of 2023 coming from this particular activity, GCs appear to be a viral and high-quality customer acquisition channel for PCOR.

In my opinion, this has likely been one of the key reasons why PCOR has been able to deliver strong growth performance with cash flow expansions – PCOR’s pricing model requires customers to pay upfront for its offerings. This high-quality business model remains a sustaining catalyst for the stock, in my opinion.

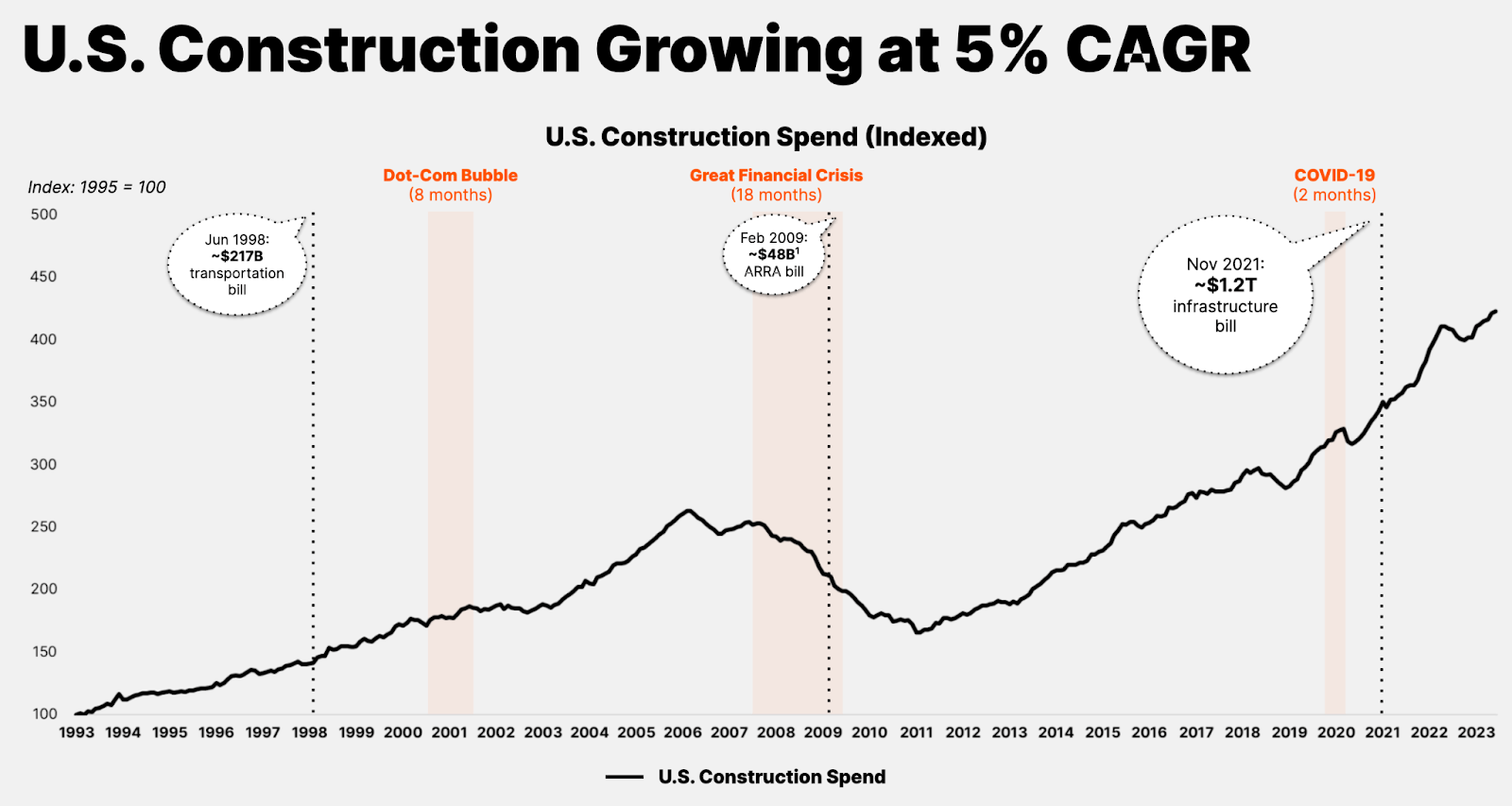

US construction growth (company presentation)

Moreover, I also see PCOR benefitting from the growing demand for its solutions due to the rising demand for infrastructure constructions in the US, driven by several policy tailwinds. The US remains PCOR’s key market where it generated over 85% of its revenue as of last FY. While the management correctly pointed out the potential of an infrastructure bill in 2021 to help boost demand for construction, my view is that PCOR is strategically positioned to also benefit from a confluence of other policies, such as The CHIPS and Science Act and Inflation Reduction Act (IRA) of 2022.

.

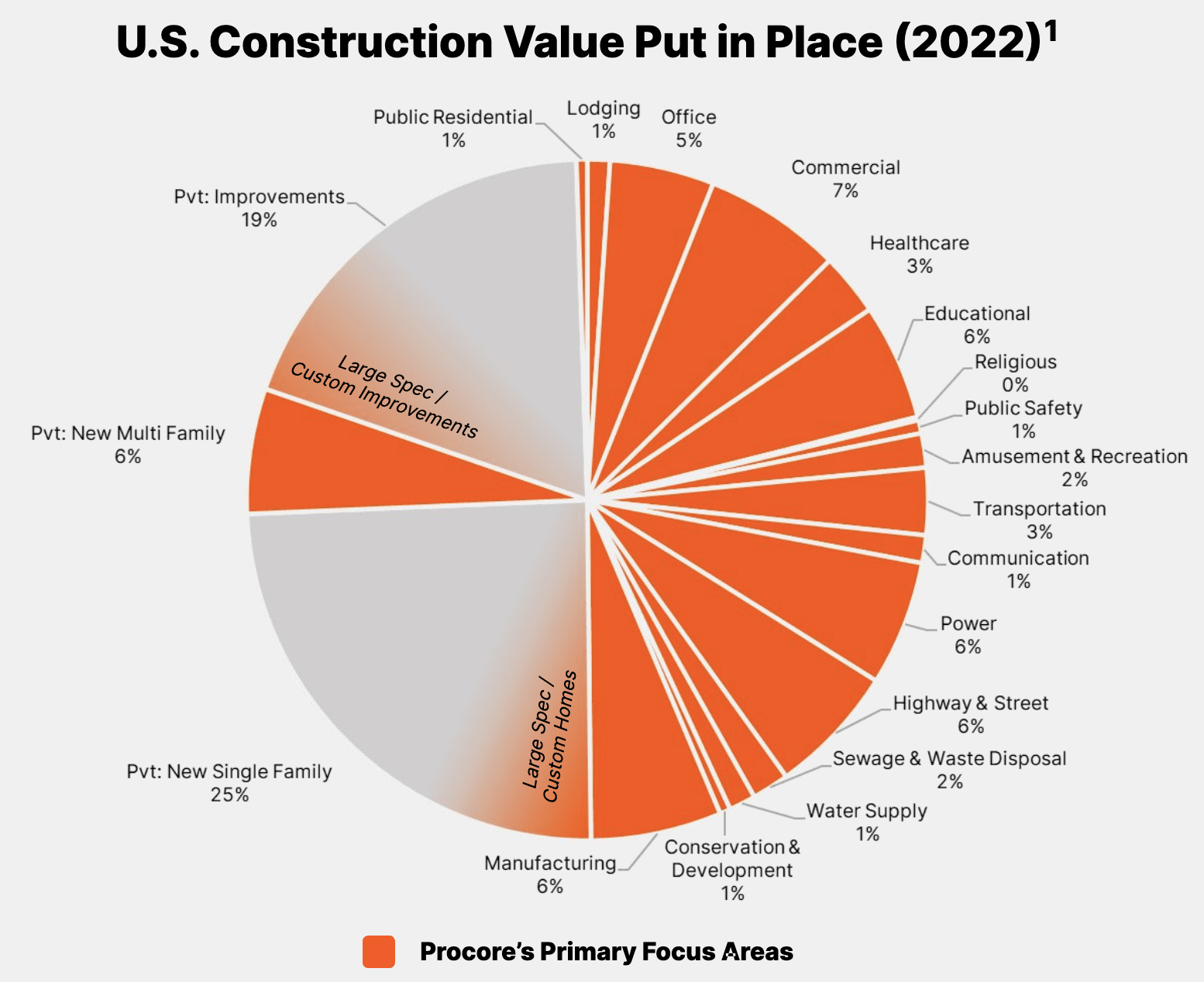

US construction value 2022 (company presentation)

Introduced almost within a relatively short time frame of each other, all of these policies collectively represent substantial government investments to pave the way for major construction projects in clean energy infrastructure, manufacturing facilities, and highway upgrades, all core areas within PCOR’s expertise.

The CHIPS Act and IRA allocate billions towards building semiconductor production facilities and clean energy infrastructure, triggering a surge in construction projects that directly align with PCOR’s focus areas in manufacturing and power.

Additionally, the infrastructure bill focuses on modernizing essential infrastructure like roads, bridges, and public transportation, creating another wave of construction demand in highway & street and transportation segments, other key areas for PCOR.

Risk

While PCOR generally faces minimal risk, two key areas deserve investor attention, in my view. In particular, while the new leadership undoubtedly brings fresh perspectives, the impact of the newly-appointed Chief Revenue Officer (CRO) on sales strategy and execution remains to be seen. In the Q4 earnings call, this topic was also brought up by one of the analysts:

Congrats on a very good end of the year, Tooey and Howard. Tooey, one thing for you is that you have a new Head of Sales. Generally, when there is a Head of Sales change in software or a CFO change in software, in your case it was a very seamless transition with your CFO change. But Head of Sales change, we always ponder if that’s going to lead to any changes in go-to-market, territory reassignments, quota reassignments, maybe that’s a little bit too radical to expect something like that happening in such a short-term time horizon. Can you just walk us through what are the things that your new Head of Sales, Larry, is going to be tweaking and what are the things that are going to stay unchanged.

Source: Q4 earnings call.

Furthermore, PCOR’s strategic shift towards larger clients may also present inherent execution risks. While the supportive policy environment creates a favorable market, the company’s past experience lies primarily with smaller players. Adapting to the complexities of larger client sales cycles and navigating their unique needs presents a learning curve that could potentially impact short-term growth, in my opinion.

In my opinion, larger deals could also be more challenging to close should the macro outlook worsen in 2024. The economic data as of late suggested persistent inflation and lower consumer spending levels, potentially influencing the Fed to reconsider rate cuts this year.

growth context (company’s presentation)

Furthermore, the potential time lag between policy enactment and tangible project impact adds an element of uncertainty, in my opinion. The slowdown in growth observed in 2023 compared to 2022 serves as a reminder that government policies alone don’t guarantee immediate results. It’s crucial to manage expectations and understand that 2024 may not mirror the spectacular growth of 2022.

Valuation / Pricing

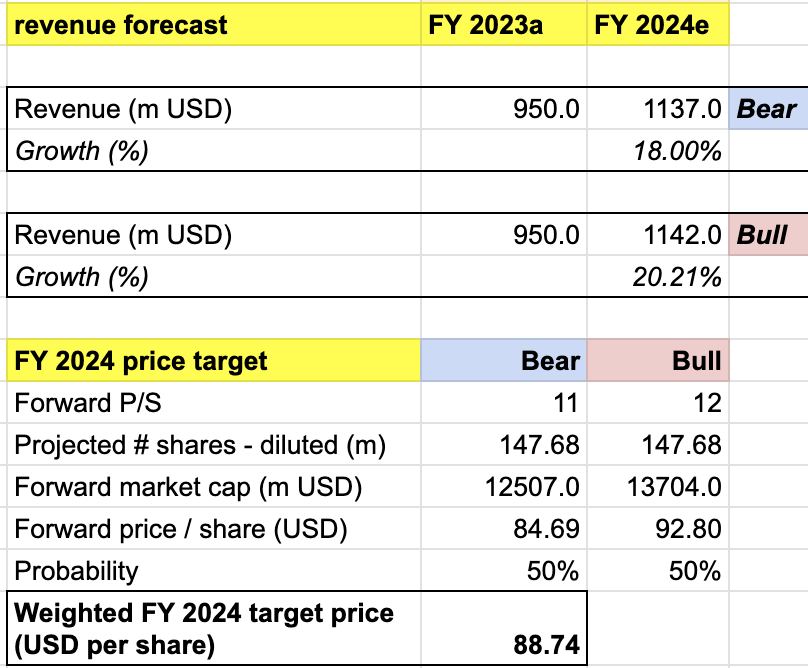

My target price for PCOR is driven by the following assumptions for the bull vs bear scenarios of the FY 2024 projection:

-

Bull scenario (50% probability) assumptions – PCOR to achieve FY 2024 revenue of $1.142 billion, a 20% growth, at the high end of PCOR’s guidance. I expect P/S to expand to 12x from 11x, where it is trading today, to reward PCOR’s performance in finishing at the high end of its top-line estimates.

-

Bear scenario (50% probability) assumptions – PCOR to deliver FY 2024 revenue of $1.137 billion, an 18% growth, missing PCOR’s low end estimate. In this scenario, I would expect PCOR to face challenges with a longer sales cycle due to the worsening macro outlook. I assign PCOR 11x P/S, where it is trading today.

price target (own analysis)

Consolidating all the information above into my model, I arrived at an FY 2024 weighted target price of $88.7 per share, suggesting a 17% upside from the current price level of $75.92. I rate the stock a buy.

Conclusion

I rate PCOR a buy. Despite the potential risks, PCOR’s core fundamentals remain strong, and the positive industry outlook fueled by policy tailwinds holds significant promise. The company’s success hinges on effective execution and smooth onboarding of the new CRO. While investors should temper their expectations for 2024 growth compared to 2022, a year of significant progress remains a realistic possibility. A cautious and optimistic approach, with close attention to the identified risks, is recommended for investors considering PCOR.

Q2 2024 Earnings Call Transcript")