Gordon Brown’s decision to sell more than half the UK’s gold reserves on the cheap 25 years ago is regarded by some as the behaviour of a sensible investor looking to spread the nation’s financial risk.

As the former chancellor would protest to the International Monetary Fund in the summer of 2007 – shortly after becoming prime minister – it was a ‘perfectly reasonable portfolio’ decision to reduce Britain’s reliance on such a fickle asset.

It was also one echoed by central banks around the world at the time.

For his critics, however, it remains one of the worst financial decisions in British political history, and one which has cost the Treasury billions in lost profits.

With the 25th anniversary of Brown’s announcement on May 7, 1999 looming, it is certainly not ageing well.

Glittering: Investors in gold have been on a winning streak, with prices up some 30% in the past six months

Gold prices stormed to a record high of $2,365 an ounce yesterday as its remarkable rally continued.

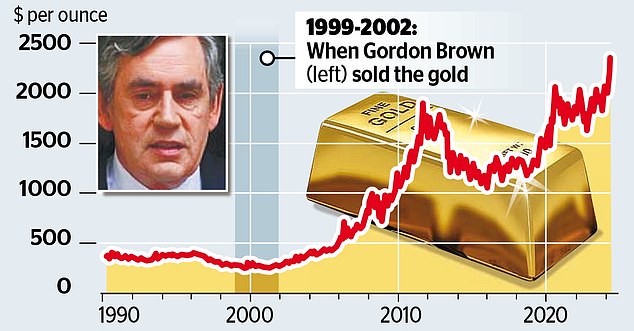

The Bank of England sold 395 tonnes of gold bullion between 1999 and 2002 at an average price of $276 per ounce – making a total of around $3.5billion which was largely invested in US Treasury securities.

Had it been sold today, it would have raked in just shy of $33billion or £26billion – a handsome sum for a government strapped for cash.

Investors in gold have been on a winning streak, with prices up some 30 per cent in the past six months.

Miners digging the stuff out of the ground have been licking their lips, not least in Australia – home to around a fifth of all known gold deposits, the largest share of any country in the world.

As a highly prized and relatively rare physical asset, the precious metal is traditionally regarded as a ‘safe haven’ during times of turmoil, and a hedge against high inflation.

There is plenty of both around at the moment. Although inflation has eased in many countries, including the US and the UK, Russia’s invasion of Ukraine and Israel’s war against Hamas in Gaza have created precisely the kind of chaos that makes gold particularly attractive to investors.

Meanwhile, financial markets have been banking on the US Federal Reserve cutting interest rates towards the middle of the year to boost the economy, despite strong jobs data over the weekend.

Gold prices tend to rise as interest rates are cut, as interest-bearing assets such as government bonds look less attractive and inflation creeps up.

Uncertainty over when rates will fall, by how much they will be cut, and the impact on inflation has also helped push up gold prices.

Bad call: The Bank of England sold 395 tonnes of gold bullion between 1999 and 2002 for around $3.5bn. Had it been sold today, it would have raked in just shy of $33bn or £26bn

On top of this, there is a looming US election in November and the prospect of Donald Trump getting a second stab at the White House.

Demand for gold has been driven by the central banks – particularly the People’s Bank of China – which have been boosting their gold reserves at a time when production has been virtually flat.

Gold demand from central banks totalled 1,037.4 metric tonnes last year, just below the record set the previous year, according to trade association, the World Gold Council.

Meanwhile, mines churned out 2,644.4 tonnes of gold last year, just 1 per cent more than the previous year.

The upshot is there is elevated demand for the precious metal and not much more of it to go around.

Markets expect strong demand from central banks to continue this year, with a Chinese official reporting at the weekend that it had purchased gold for its reserves for the 17th straight month in March.

For some, however, the metal’s enduring appeal makes little sense. US investor Warren Buffett summed up his misgivings during a speech he gave at Harvard University in 1998.

‘Gold gets dug out of the ground in Africa, or some place,’ he said.

‘Then we melt it down, dig another hole, bury it again and pay people to stand around guarding it. It has no utility. Anyone watching from Mars would be scratching their head.’

For once, the Sage of Omaha for his uncanny ability to spot market trends, appears to have missed a trick.

Russ Mould, investment director of AJ Bell, said: ‘Gold is durable, has a history of being money since time immemorial and is difficult and expensive to produce, so it can be seen as a store of value at a time when inflation is eroding the purchasing power of money in the West.’

Some links in this article may be affiliate links. If you click on them we may earn a small commission. That helps us fund This Is Money, and keep it free to use. We do not write articles to promote products. We do not allow any commercial relationship to affect our editorial independence.

Q2 2024 Earnings Call Transcript")