Jamakosy

Co-authored with “Hidden Opportunities”

As summer approaches, the anticipation of a memorable road trip builds. Fueled by excitement and a full tank of gas, you eagerly set off on your journey. However, adversity strikes when a flat tire occurs amidst pouring rain. Despite the initial panic, you find comfort in your preparedness, having stashed away a first aid kit, a spare tire, and necessary tools. With some DIY ingenuity, you swiftly overcome the setback and transform the experience into another unforgettable adventure.

Investing in preparedness helps mitigate the impact of unforeseen challenges before they escalate into more significant problems. This is why we buy homeowner, automotive, health, travel, and other insurance products. Life is unpredictable, full of twists, turns, and occasional turbulence. But with a bit of preparation – whether it’s a spare tire in the trunk or an inflatable vest in the overhead compartment – you can face whatever comes your way confidently, turning obstacles into opportunities and adventures into triumphs.

Economists are predicting a hard landing, as the impact of high interest rates has yet to sink in the economy. Add to it the Fed’s tightening regime and geopolitical conflicts, and we will have a hard landing at some point. It is a good idea to be prepared for it with defensive investments whose business fundamentals stay robust through economic cycles. Let us review two picks with up to 10.9% yields to get started.

Pick #1: BCE – Yield 8.6%

Bell Canada Enterprises Inc., also known as BCE Inc. (BCE) is Canada’s largest telecom company with more than 10 million wireless subscribers, and 24.28 million consumer, business, and wholesale customer connections. BCE boasts Canada’s fastest internet and internet and Wi-Fi for the second year in a row. BCE also operates a media business with a subscription product “Crave” with over 2.8 million customers.

BCE is a time-tested dividend steward, with no missed payments since 1881 and the telecom leader has issued annual raises for 16 consecutive years. The company recently issued a 3.1% raise to $3.99/share annually, a 8.6% yield.

Note:

-

BCE is a Canadian Corporation with listings on NYSE and TSE. BCE declares and pays dividends in Canadian Dollars, and U.S. investors will receive an amount that varies based on USD-CAD conversion rates.

-

All figures discussed in this article are in Canadian Dollars.

For FY 2023, BCE reported $10.4 billion adj. EBITDA, a 2.1% YoY increase, and an industry-leading 42.2% EBITDA margin. Bell CTS reported full-year revenues of $21.9 billion (up 2.9% YoY), and Bell Media reported $3.1 billion (down 4.2% YoY). Notably, Canadian telecom is a significant oligopoly, with strict regulations to prevent international companies from competing with the big three – BCE, Telus (TU), and Rogers (RCI). Moreover, regulatory protections prevent small and new players from emerging or competing effectively.

BCE is the 16th largest employer in Canada and has significant sway in policy-making by virtue of its role in the job market. A recent undertaking by the telecom regulator to open up more of the country’s broadband infrastructure to wholesale-based competitors has met serious push-back from established players. BCE announced a workforce restructuring initiative, its largest in nearly 30 years, reducing ~4,800 positions, including 750 contractors, or 9% of all BCE employees. The fact that BCE raised its dividend while pursuing workforce reduction demonstrates management’s intent to keep shareholders happy but send a message to the regulators. Historically, such regulatory efforts have ended up causing benign changes to the moat and dominance of the Big Three.

As a result of the layoffs and associated workers compensations, BCE expects lower FCF and EPS in FY 2024, and the telecom leader has guided 0-4% revenue growth, and 1.5-4.5% adj. EBITDA growth. Management maintains their commitment to the dividend growth objective.

BCE ended FY 2023 with a net debt to adjusted EBITDA of 3.48x, with $5 billion of debt due within a year. The firm maintains $5.8 billion liquidity, including $547 million cash assets to handle these maturities.

Canada has the highest immigration of any OECD country. Adult population growth through immigration in Canada is a significant long-term growth driver for BCE and peer telecom firms. BCE’s 8.6% dividend that was recently raised is a significant incentive to buy amidst valuation pressures from interest rates.

Pick #2: SLRC – Yield 10.9%

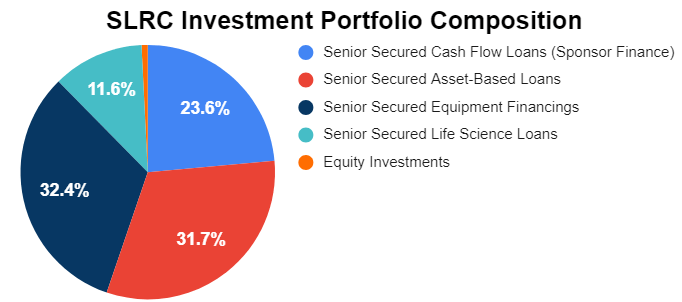

SLR Investment Corp. (SLRC) is a unique BCD (Business Development Company) focusing on Asset Based Lending, Equipment Financing, Life Science Finance, and Sponsor Finance. The BDC ended FY 2023 with $986.6 million in net assets, diversified across ~790 issuers in over 110 industries, with a significant majority of 99.2% invested in senior secured loans. When we first bought SLRC, it was failing to cover its distribution. Last year, it covered its distribution with a cushion to spare.

Following its merger with SUNS, SLRC has evolved from a BDC that barely covered its distribution to one that consistently out-earns the payout. SLRC marked four straight quarters of NII (Net Investment Income) growth, reporting Q4 NII of $23.9 million, up 7.3% YoY, reflecting a per-share value of $0.44. This is in excess of its $0.41/share quarterly distribution. SLRC ended Q4 with a net asset value per share of $18.09 (vs $18.06 at the end of Q3) and net debt to equity of 1.19x (down from 1.21x at the end of Q3).

During the fourth quarter, the BDC reported $449.8 million in loan originations and $462.1 million in repayments, indicating healthy turnover into new loans at better interest rates and more stringent underwriting standards in the current economy. During the fiscal year, SLRC reported a record-high $1.47 billion in loan originations and $1.34 billion in repayments.

At the end of FY 2023, SLRC reported a weighted average portfolio yield of 11.6%, down from 12.3% in September 2023, and 65.3% of the investments carried floating interest rates. The BDC reported a notable increase in the composition of equipment financing and life sciences loans due to the turnover.

Author’s Calculations

These categories are essential in current market conditions. Businesses need equipment to stay in business, and during economic volatility and recessions, smaller companies tend to be strapped for cash, making equipment financing a powerful utility to preserve cash flows. Post-covid healthcare is a cash-starved industry with historically low market valuations. Yet, the sector continues to innovate and produce meaningful solutions to ailments and requires capital to survive and grow. These factors make these segments very attractive for BDCs to issue funding and support.

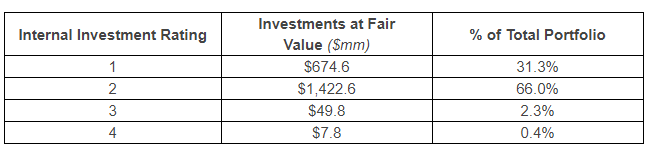

As of December 2023, 99.6% of SLRC’s portfolio was performing on a fair value basis, with one loan in non-accrual status. However, some deterioration has started to show, with 2.7% of the portfolio carrying a rating of 3 or higher, implying that it requires closer monitoring or in nonaccrual status (up from 0.6% at the end of Q3). 0.4% of SLRC’s portfolio is not expected to be repaid in full (up from 0.3% at the end of Q3). Source

Q4 Earnings Report

With heavy allocation to senior secured loans and a focus on financing methods that prosper in a strained economy, SLRC is a defensive BDC to buy and hold. At an 16% discount to NAV, SLRC makes one of the biggest bargains in the BDC sector.

Conclusion

As the old joke goes, economists have successfully predicted nine of the last five recessions. Sometimes, analysts from the same company might have different opinions on the economy. This way, the company appears right no matter what happens, especially when the media reports on their successes years later.

Predicting whether we will have a hard or a soft landing is quite difficult. But it’s smart to be prepared with defensive investments. It’s even better when you make money from them. This is why our Investing Group holds several telecom, utility, infrastructure firms, BDCs, and many fixed-income securities. These help protect us if the economy gets shaky and provides us with healthy income regardless. Heads I Win, Tails I Win. This showcases the heart of my Income Method, the essence of income investing.

Q2 2024 Earnings Call Transcript")