mbbirdy

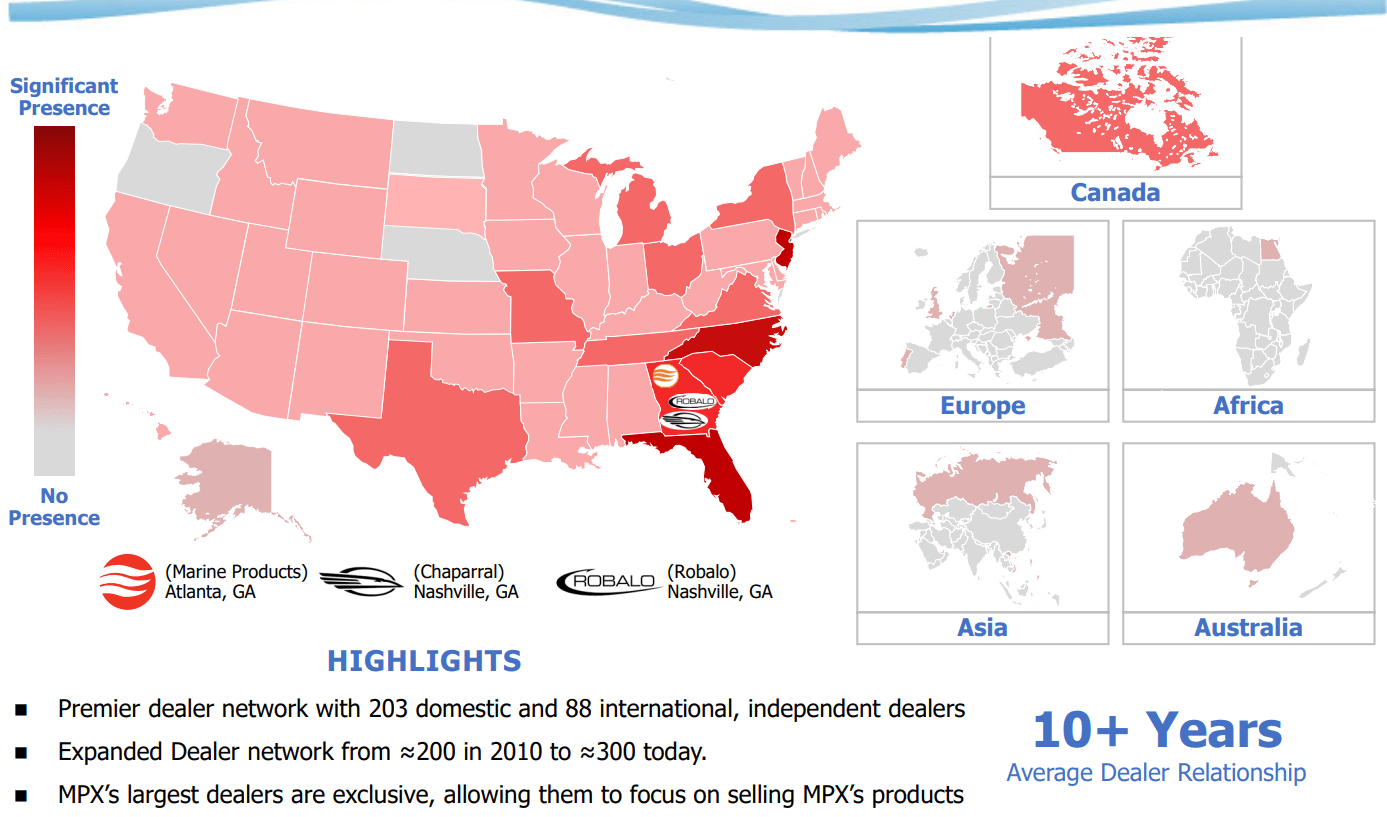

Marine Products Corp. (NYSE:MPX) is a leading manufacturer of smaller, lake and seaside boats for families and fishing businesses. Located in Georgia, all design and production is handled through one U.S. plant, with a vertically integrated business model. Yet, 300 independent dealers across the world sell product for the company. In their size range for outboard boats, the MPX Chaparral brand holds the #1 market position, while Robalo holds the #3 market spot.

The company has enjoyed killer returns and margins over the years. MPX has zero debt, plus plenty of cash on hand (representing roughly 20% of the equity capitalization currently). Even with boat demand slowing during 2023, following the high demand period of the pandemic years of 2021-22, the company remains quite profitable.

For investors, the net result of a big swoon in the share quote since August and the 50% haircut from 2018’s all-time high is the valuation proposition is now top notch. So, if the U.S. and global economy surprises (myself included) with a soft landing or no landing scenario in 2024 as the Big Tech stock boom in wealth potentially helps refloat GDP output, I believe enormous upside potential exists in this name. If a brighter economic future becomes reality, I would expect broadening gains into other sectors of the stock market, including leisure and high-dollar transportation manufacturers.

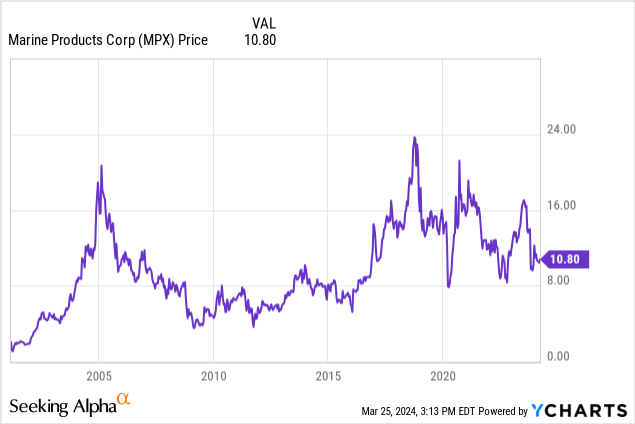

YCharts – Marine Products, Monthly Share Price, Since 2001

The Business

Marine Products has a 60-year history, building steady company growth using old-fashioned, self-funded sources for capital spending. The company earns a profit, pays some out as a dividend to owners, and reinvests the rest into upgrading facilities, designing better boats, or acquiring related assets. This formula has been a winning one, without the use of much debt over the years.

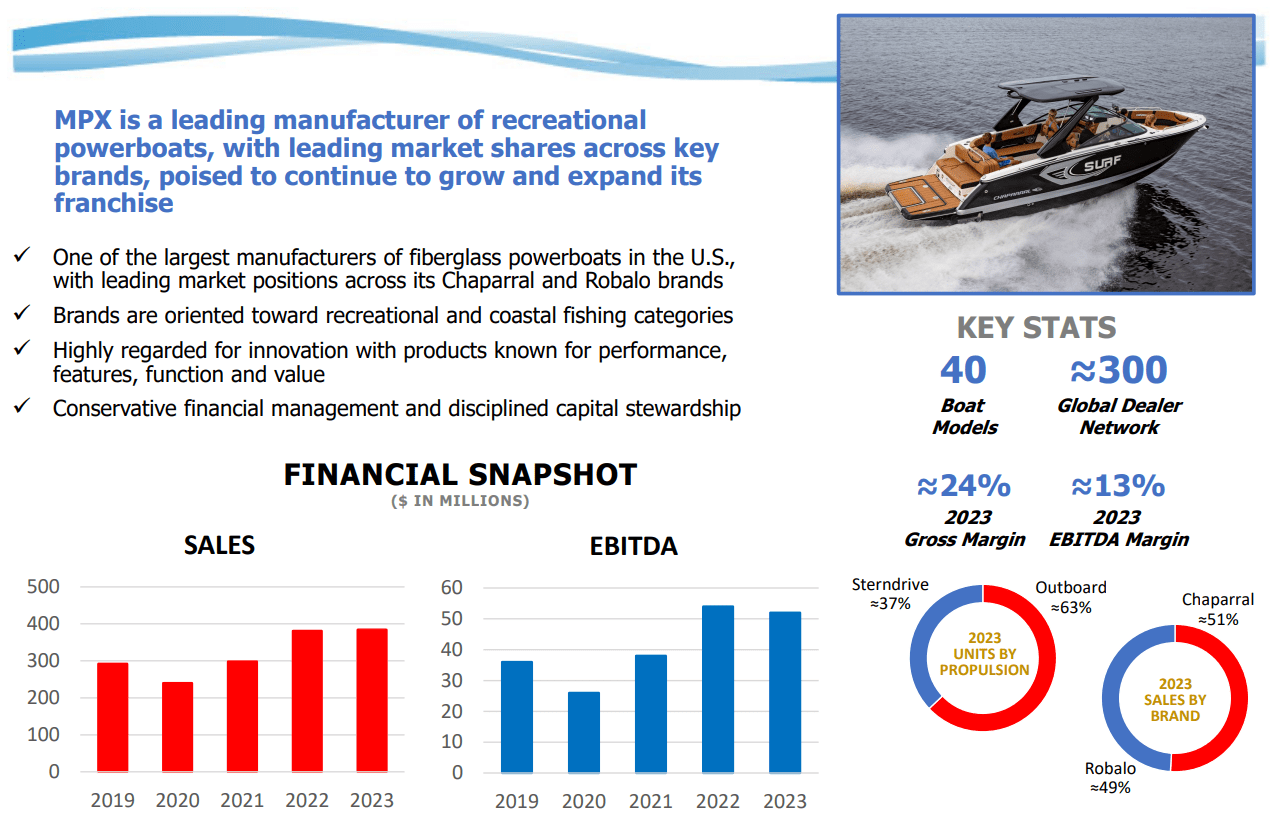

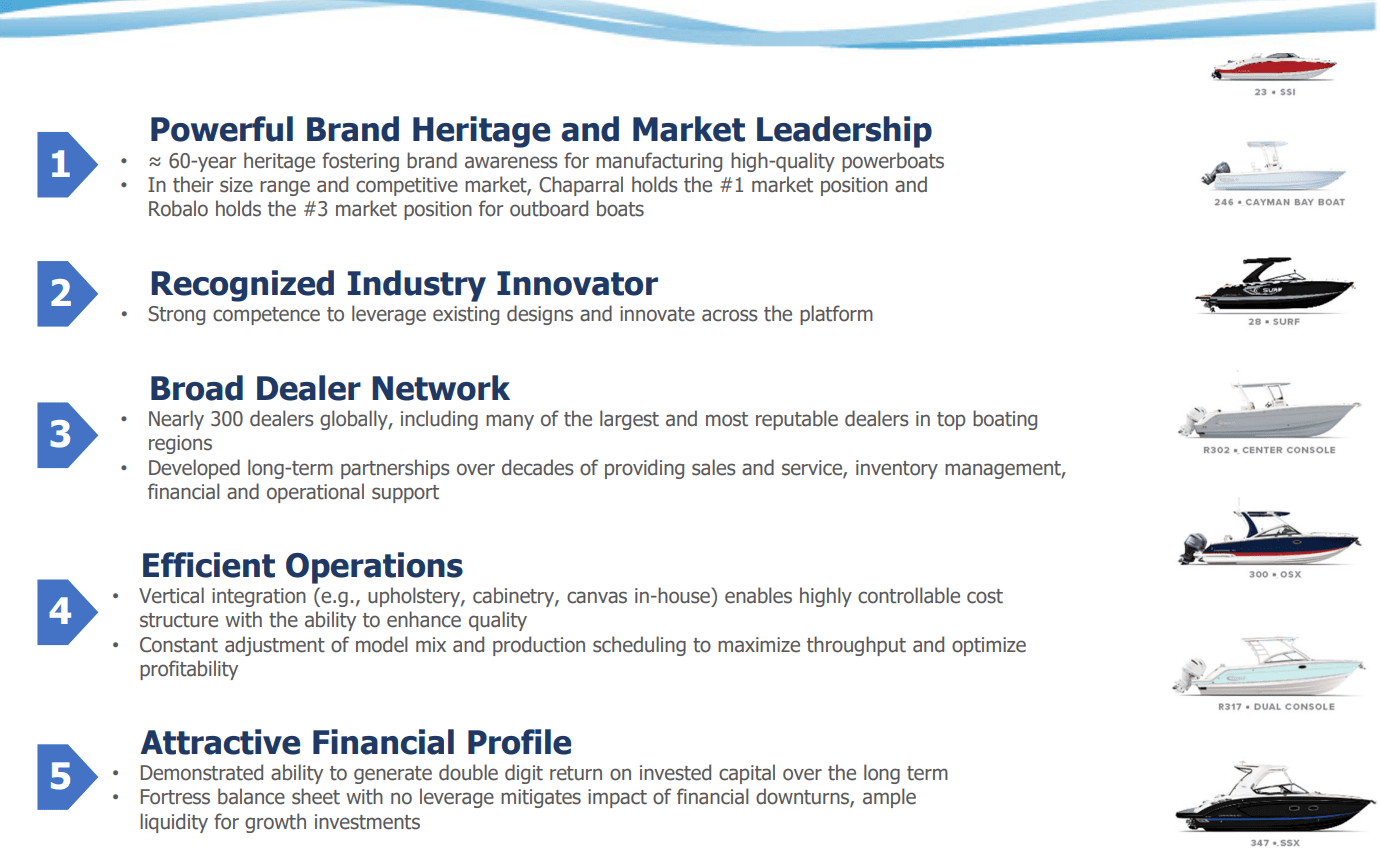

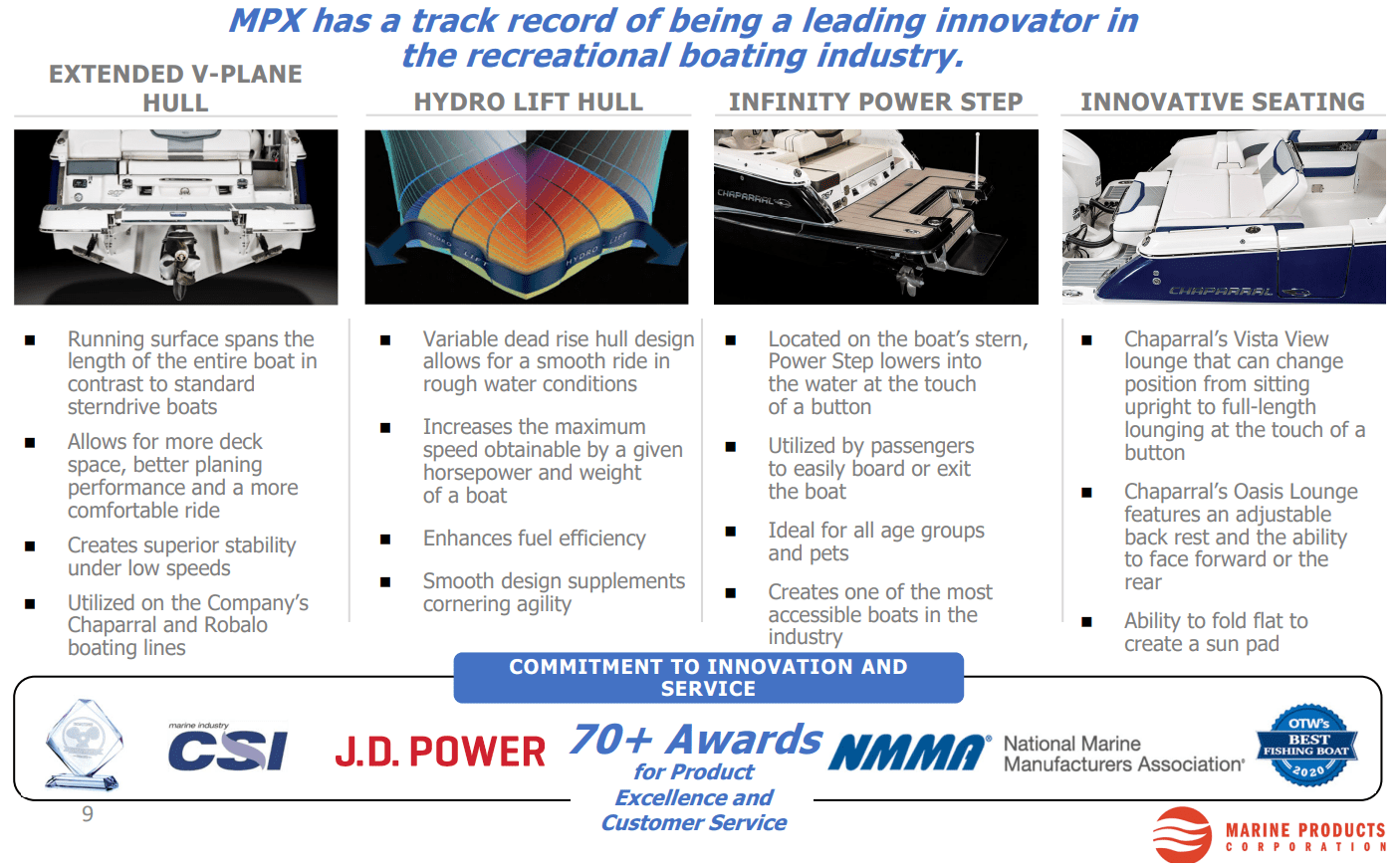

Below are slide highlight from its March 2024 Investor Presentation, describing the business in more detail. The financial returns and margins are the ones grabbing my attention most.

March 2024 Investor Presentation – Marine Products March 2024 Investor Presentation – Marine Products March 2024 Investor Presentation – Marine Products March 2024 Investor Presentation – Marine Products

Bargain Valuation Setup

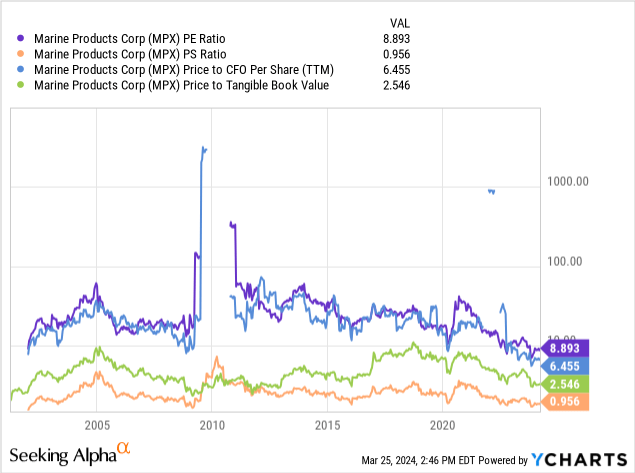

A unique combination of factors has led to a super-low valuation for Marine Products today. For starters, a stagnant share price over a number of years has not properly discounted the inflow of cash held by the enterprise, since 2021. Already, on basic financial ratios of price to trailing earnings, sales, cash flow, and tangible book value, MPX is getting close to a record-low valuation (the business was formed through an asset combination in 2001).

YCharts – Marine Products, Basic Fundamental Raito Analysis, Since 2001

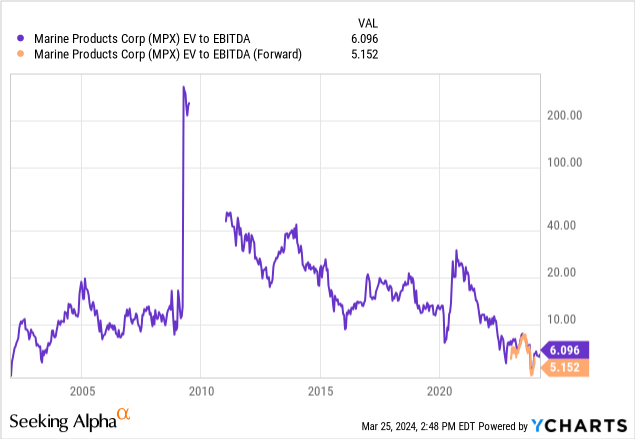

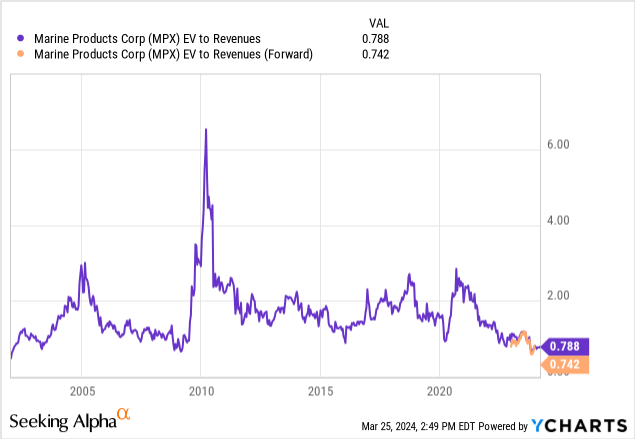

But, when we factor into our equation record cash holdings and no debt on the balance sheet, enterprise valuations are bordering on the absurd for cheapness. Trading at a 6x multiple of EV to EBITDA on trailing numbers (or 5x forward estimates), and 0.79x EV to trailing sales (or 0.74x forward estimates), “deep value” investors should be very interested in buying the business.

YCharts – Marine Products, EV to EBITDA, Since 2001 YCharts – Marine Products, EV to Sales, Since 2001

For perspective, EV to EBITDA stands at a 50% discount, and EV to revenue at a 60% discount to long-term averages. The only logic to support this undervaluation setup is boat demand could be set to implode in a serious recession. While a recession is definitely possible (in fact, it’s my baseline projection for 2024), the balance sheet is well prepared for one. Plus, there are no guarantees boat demand will be sucked down the drain in a mild recession. On the flip side, a soft landing or no landing scenario could actually send new boat construction demand substantially higher.

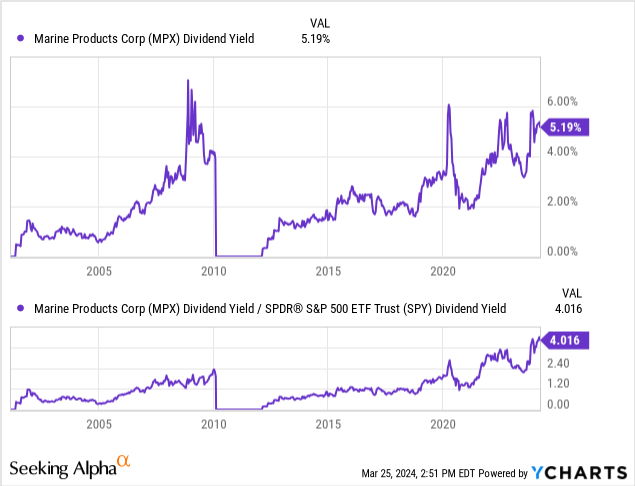

Then, we can review the dividend proposition from Marine Products, which is today standing in its best position maybe ever for buyers of the stock. The 5% dividend yield represents less than half of income created over the last four quarters. In addition, this rate is 4x the equivalent cash distribution level of the S&P 500 index, which represents MPX’s strongest “relative” yield ever.

YCharts – Marine Products vs. S&P 500 ETF, Dividend Yield, Since 2001

Improving Chart Pattern

Marine Products has not participated in the +30% S&P 500 index price appreciation jump over the last 12 months. In fact, shares are slightly lower than a year ago, despite another solid year of adding to its underlying fortunes.

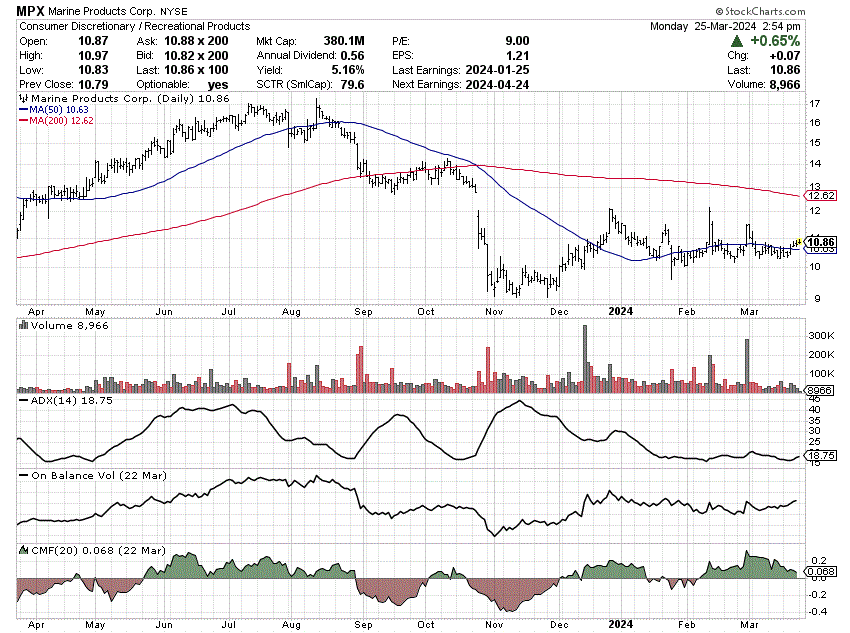

A weak earnings report in late October sent MPX down almost -35% over a few weeks. Really, the stock has been trying to recover in price since that selloff. The good news is a low 14-day Average Directional Index score since January has been indicating a lower-volatility balance between buyers and sellers.

More positives include a nicely trending higher On Balance Volume calculation since early November, and a 20-day Chaikin Money Flow reading almost entirely in the green since early December.

Rounding out the technical readout, price has been outlining rising lows since late January, and the 50-day moving average is ready to turn higher with any price upmove. It’s entirely possible a vacuum of sellers may now exist, meaning better company news flow soon could ignite a sizable price rally (the Q1 earnings statement is due in late April).

StockCharts.com – Marine Products, 12 Months of Daily Price & Volume Changes

Final Thoughts

My conclusion is Marine Products could be a steal at current quotes, given a deep recession is avoided this year. The pricing disconnect and opportunity is you can buy this leading boat maker at a fire-sale discount on recession fears, just before the opposite potentially materializes with a bump higher in orders, sales and income.

What are the downside risks? For sure, a recession would keep a lid on the share quote. Yet, I do believe MPX could surprise and not fall much in a recessionary future, because it has largely been priced for one since October.

A second risk is rising interest rates or an actual recession could torpedo the U.S. equity market generally. Long-term valuations remain in the stratosphere on Wall Street, based on the S&P 500’s all-time high 3x sales ratio presently, or total stock market worth to GDP reading approaching 2x (with long-term averages of this indicator well under 1x). If stocks crash in price (heaven forbid but not impossible), MPX will be dead in the water for another year, at a minimum.

However, assuming boat demand trends actually surprise by growing again this year, and we put a normalized 20-year valuation on the stock, I believe a potential double in price over the next 12 months cannot be ruled out for MPX (for a +100% investment gain, on top of the extraordinary 5% dividend yield).

Given management and insiders control 75% of the stock, not much float exists if a big institution or hedge fund wants to acquire a material stake. Such interest could turbocharge share gains. Further, a takeover bid by another boat manufacturer or private equity cannot be ruled out, if insiders want a profitable way to quickly monetize their holdings. When valuations get as low as today in a smaller company ($370 million market cap at $10.80 a share, minus $70 million in cash at the end of December, equals $300 million for net enterprise value), it’s inevitable financial number crunchers and activist investors of all types could be circling Marine Products soon. It’s likewise possible management could use the low price to take the company private, buying out the 25% of shares not already owned.

For now, the valuation story is so compelling, I have a Buy rating on Marine Products. I also recently purchased a position, after watching it closely since autumn. The technical basing pattern, with a clear bullish bias in recent weeks, is hard to ignore.

Thanks for reading. Please consider this article a first step in your due diligence process. Consulting with a registered and experienced investment advisor is recommended before making any trade.

Q2 2024 Earnings Call Transcript")