zorazhuang

Plains All American Pipeline (NASDAQ:PAA) is an attractive distribution play for investors who want to gain a foothold in the master limited partnership space. The pipeline company generates more than half of its adjusted EBITDA from its fast-growing pipeline operations in the Permian basin and has very strong distribution coverage. Based off of the MLP’s outlook for FY 2024, the pipeline company is set to achieve a massive 190% distribution coverage ratio which creates upside for the distribution as well. I believe that Plains All American is a well-run master limited partnership that trades at a reasonable unit price, and the 8% distribution yield is well-secured by cash flow. I initiate Plains All American with a hold rating!

Plains All American’s business model and operations

Pipeline companies like Plains All American tend to be structured as master limited partnerships. These MLPs are typically engaging in some kind of natural resource activities and are considered a pass-through entity.

Plains All American owns and operates midstream energy infrastructure assets and provides logistics services for crude oil, natural gas liquids, and natural gas. The key EBITDA source for the pipeline company is crude oil, which generates about 85% of EBITDA, followed by NGL products with an EBITDA share of 15%.

The pipeline company delivered impressive results in FY 2023 due to strong growth in one of its key areas, the Permian. Plains All American generated $1.25B in adjusted net income last year which showed an increase of 15% year over year while its adjusted EBITDA gained 10% Y/Y to $3.2B. Adjusted free cash flow also gained in the double-digits (+12% Y/Y), allowing the company to pay unitholders a generous distribution.

Plains All American

Plains All American’s pipeline, storage, and processing assets are located in the U.S. and Canada and the pipeline company has developed a core operating focus on the Permian basin… an especially fast-growing and promising shale area that is located in western Texas and southeastern New Mexico. The Permian basin is a key growth engine for the pipeline company as strong production growth requires pipeline and storage capacity to transport shale oil to consumer end markets. Permian volume growth is therefore a key driver of Plains All American’s EBITDA and free cash flow growth in FY 2024.

Plains All American

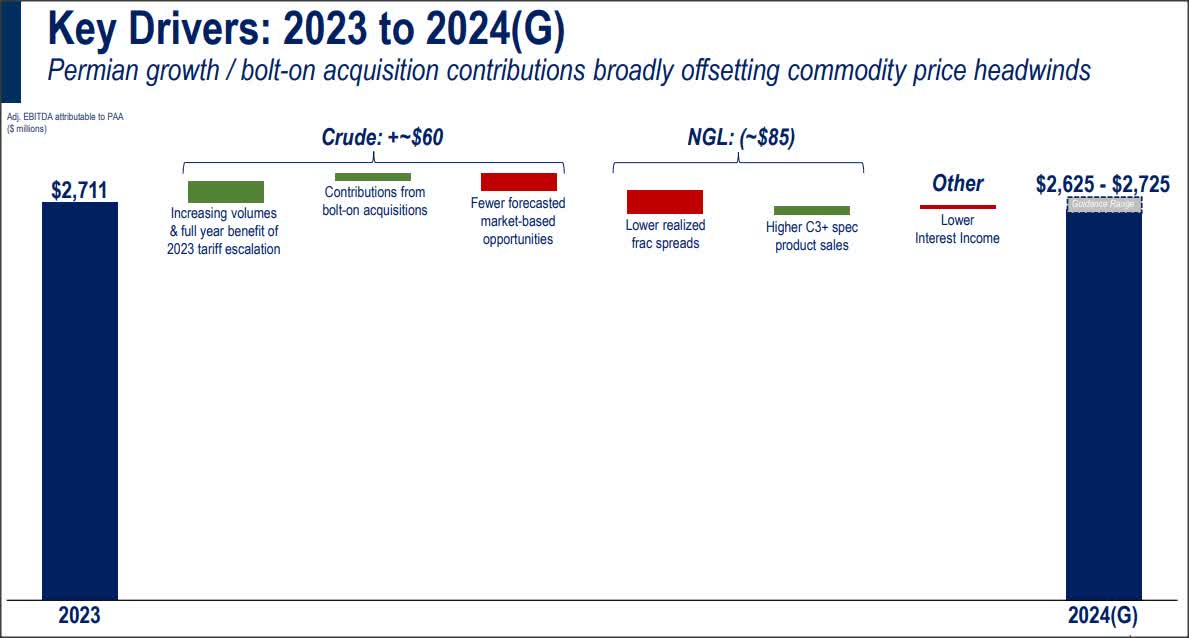

About 60% of the company’s EBITDA is expected to be contributed just from the Permian this year…

Plains All American

Outlook for FY 2024, implied distribution coverage ratio

Plains All American has guided for FY 2024 EBITDA of between $2.625B and $2.725B. This guidance implies fairly stable EBITDA and a 1% Y/Y decline at the mid-point, chiefly due to lower spreads in the NGL business. The crude oil business, however, is expected to make a positive EBITDA contribution this year.

Plains All American

The pipeline company stated that its projected FY 2024 adjusted EBITDA is set to yield $1.65B in distributable cash flow. With the distribution, at current rates, costing ~$890M annually, Plains All American Pipeline is set to achieve a distribution coverage ratio of 1.9X. For comparison, Enterprise Products Partners (EPD), which I also like and recommend to dividend investors, had a distribution coverage ratio of 1.7X in FY 2023… and is set to achieve a comparable ratio in FY 2024 as well. The distribution, therefore, should be very safe and is likely to get raised as well later this year.

According to Plains All American’s capital framework for the current year, the company should be left with $500M in excess free cash flow (after payment of the distribution) which is money that could be used for reinvestment purposes or to lower the MLP’s leverage.

Leverage profile

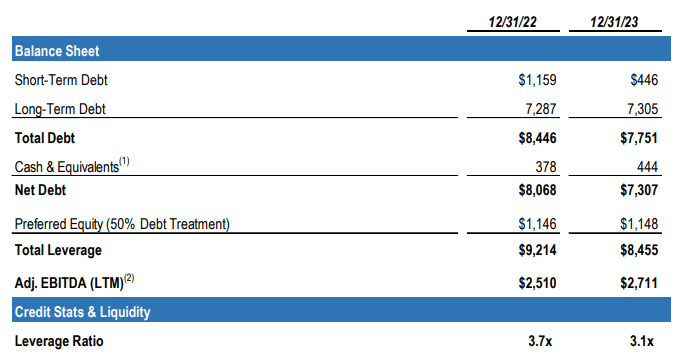

Plains All American has made progress in lowering its leverage and the MLP has stated that it is looking to bring down its leverage even further. The current leverage ratio is 3.1X compared to 3.7X in FY 2022 and 4.5X in FY 2021.

Plains All American

Plains All American Pipeline valuation

I value master limited partnerships based off of EBITDA because they tend to spend a lot of money on CapEx, which can distort and skew earnings results in any given year. EBITDA does not include depreciation and amortization expenses, which makes valuation ratios more comparable.

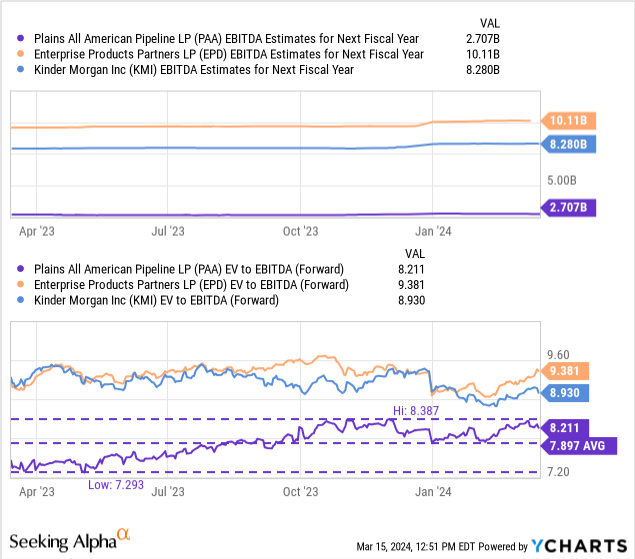

According to YCharts, Plains All American is currently valued at an enterprise-value-to-EBITDA ratio of 8.2X, showing a 4% premium to the 1-year average ratio of 7.9X. These ratios compare against an average industry group EV-to-EBITDA ratio of 8.8X, so Plains All American is only slightly cheaper. Members that I included in the industry group are Enterprise Products Partners and Kinder Morgan (KMI), both of which run sizable pipeline businesses themselves. From a valuation perspective, I believe PAA does not have a major advantage compared to Kinder Morgan and I therefore rate the pipeline company’s units a hold.

Risks with Plains All American Pipeline

Plains All American is heavily focused on fossil fuel activities and federal regulatory authorities may decide to crack down on expansion projects in the pipeline industry. This could limit Plains All American’s growth prospects and result in slower EBITDA and free cash flow growth going forward. What would change my mind on the pipeline company is if I were to see a significant drop in the distribution coverage ratio… which I frankly see as unlikely: with a 190% projected coverage ratio, Plains All American Pipeline should be safe here.

Final thoughts

Plains All American Pipeline is a crude oil-focused pipeline play with a core operating focus in the fast-growing Permian basin. The company generates a ton of EBITDA and free cash flow from its crude oil and NGL infrastructure assets and is currently slated to achieve, based off of its adjusted EBITDA outlook, a distribution coverage ratio of 1.9X in FY 2024. The distribution, therefore, should be very safe and the MLP’s leadership is likely going to continue to raise the distribution later this year. At current unit prices, dividend investors get an 8% return on their invested capital!

Q2 2024 Earnings Call Transcript")