Justin Sullivan

Amid extreme market volatility especially in small and mid-cap stocks over the past month, one thing rings true: investors have to be willing to constantly update their theses as different companies respond differently to macroeconomic conditions, and as valuations change. Being a committed bull or bear is only workable as long as our convictions don’t get in the way of reacting to the most recent information.

I had been a longtime bear on Pinterest (NYSE:PINS), the social media stock that largely trails behind rivals like Meta (META). After the company released Q2 earnings, I nudged up my rating on the stock to neutral, but still cited concerns over both user/ARPU growth.

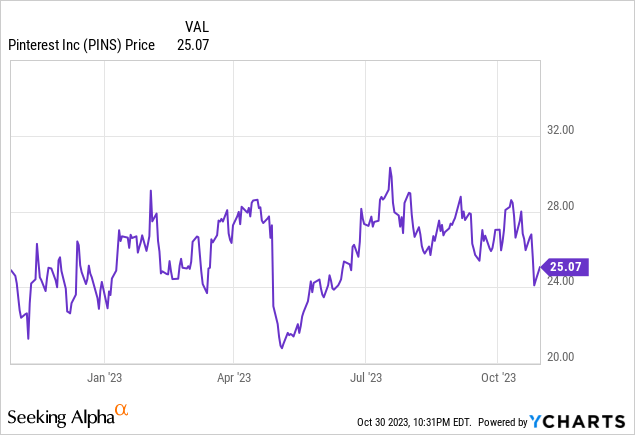

Now, after both a slash to the stock’s valuation plus very positive Q3 results, I’m finally willing to give the stock a bullish rating, especially when most of its YTD gains have vanished.

The bull case for Pinterest

Pinterest occupies a difficult position in the social media landscape. It’s not as popular as rivals like Instagram (across the Facebook/Instagram family of apps, Meta counts roughly 2 billion daily users; Pinterest barely has 500 million monthly active users). It’s very possible that this interest-based site, modeled off the concept of a “pinboard” where users post threads on their niche topics of interest, is a fad.

But at the same time, especially after dissecting the company’s Q3 results, there are a number of bullish drivers to point to:

- Intentional, purpose-driven user base leads to a very easily monetized platform. Because Pinterest users are already scrolling through items that they are interested in, among social media platforms, Pinterest is one of the most directly appealing to advertisers. The company has been building out its advertiser solutions and has succeeded at retaining large brand partners.

- User growth in international markets. Though the U.S. currently drives the lion’s share of Pinterest’s revenue, the company is seeing double-digit growth in emerging markets. Its popularity with Gen Z ensures us that Pinterest has found a footing with a younger generation and will hopefully not fade as millennials age and get busier.

- Strong click-through rates. Higher outbound ad clicks are driving up ARPUs, which is a key source of revenue growth even in the U.S. where user growth is drying up.

- High gross margins. Pinterest’s high-70s gross margins leads to plenty of scalability for the company, if it can manage to both bring in a steady recurring advertising revenue base plus keep spending in check.

- Cost discipline. Pinterest’s recent across-the board cost cuts (the company executed several rounds of layoffs over the past year) have helped promote a surge in profitability.

Valuation is reasonable

Even after the company’s immediate post-earnings reaction spike to ~$29/share, Pinterest still trades at reasonable multiples of FY24 consensus expectations. At $29, Pinterest trades at a market cap of $19.52 billion. After we net off the $2.33 billion of cash on the company’s most recent balance sheet, the stock’s resulting enterprise value is $17.19 billion.

Meanwhile, for FY24, Wall Street analysts are expecting Pinterest to generate $3.49 billion in revenue (+15% y/y). If we assume the company is able to hold 24% adjusted EBITDA margins (flat to Q2) on that revenue profile, adjusted EBITDA in FY24 would be $838 million. This puts Pinterest’s valuation multiples at:

- 4.9x EV/FY24 revenue

- 20.5x EV/FY24 adjusted EBITDA

A sub-5x forward revenue multiple for a company with mid-teens revenue growth and several growth catalysts (ARPU expansion from higher ad click rates, international MAU growth) and meaningful bottom-line expansion is not unreasonable, in my view.

My take here: wait for Pinterest’s post-earnings pop to cool off, but the stock is a solid buy in the $24-$27 range.

Q3 download

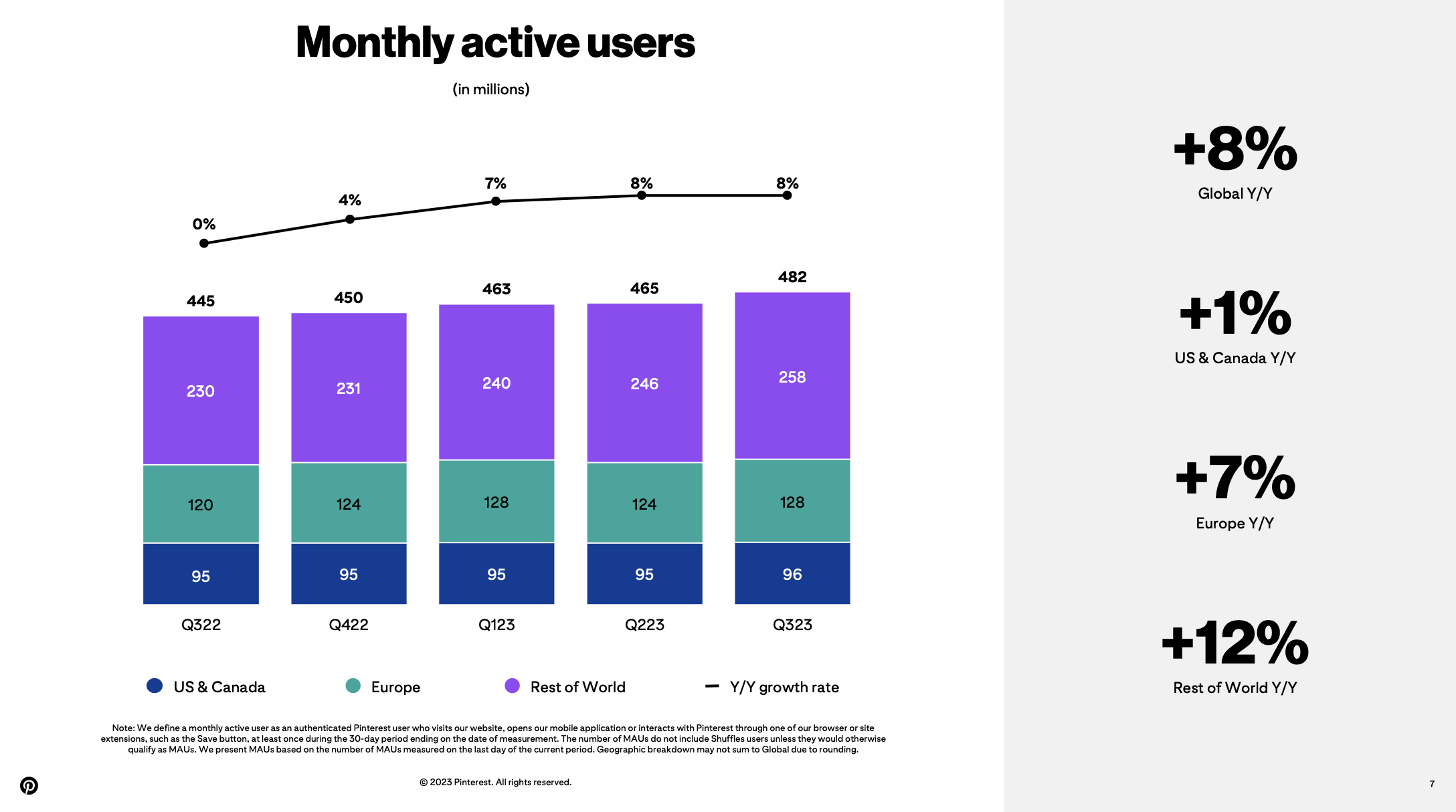

Let’s now highlight the trends that made Q3 so favorable. We’ll start with the user trends below:

Pinterest MAU trends (Pinterest Q3 investor deck)

Now, the one caveat here is that my chief concern with Pinterest: sluggish US user growth, where the majority of Pinterest’s revenue (81% of the Q2 total revenue) is generated, is not improving, suggesting saturation in Pinterest’s most important market. This user base is growing at only 1% y/y and has flatlined at a nominal 95-96 million users for more than a year. The upside to this, however, is 12% y/y growth in non-US/Canada, non-Europe: yet with relatively low monetization here, it will be awhile before these users generate meaningful revenue.

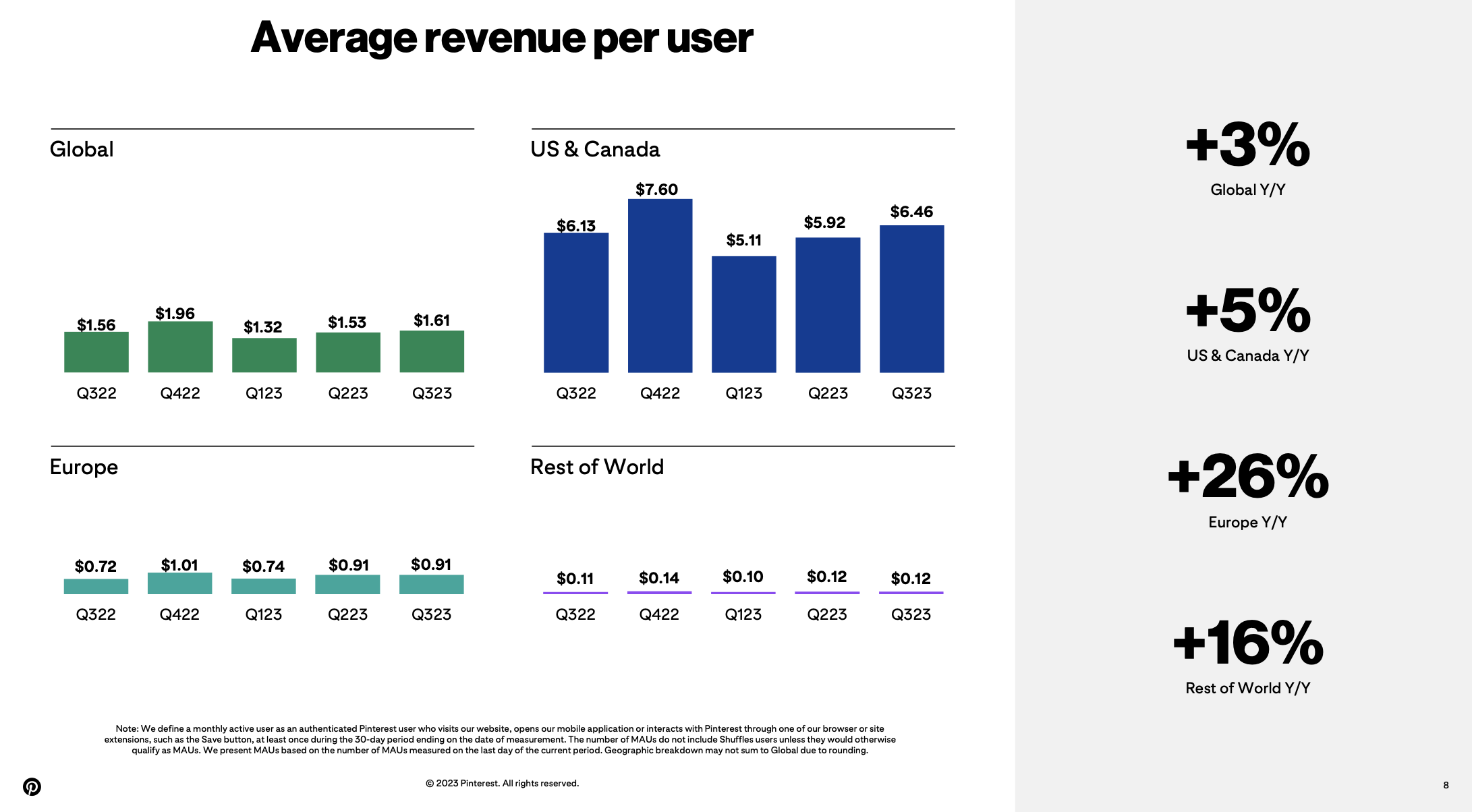

Thankfully, even though user growth in the U.S. and Canada has stagnated, ARPUs have risen sequentially in each of the past two quarters. ARPU in the U.S. grew 5% y/y in Q3, helping to stimulate 3% y/y growth in global ARPU. This is better than a 3% y/y U.S. ARPU increase in Q2, which due to a heavier Europe/Rest of World user mix actually caused global ARPU to contract -1% y/y.

Pinterest ARPU trends (Pinterest Q3 investor deck)

Improved click-through rates, partially driven by the company’s own feature rollouts, have driven this ARPU favorability. Per CEO Bill Ready’s remarks on the Q3 earnings call:

We discussed the success we’re seeing with Mobile Deep Links, or MDL, where advertisers can now direct link users directly into the relevant product page and checkout experience in their mobile app. This is a great solution for merchants who have stand-alone apps with broad consumer penetration. As we’ve noted before, MDL is performing extremely well in our tests.

Participating advertisers saw a 235% lift in conversion rates, along with a 35% improvement in their CPAs. We’re now bringing this solution to those advertisers who either don’t have an app or rely primarily on their website for traffic and sales. This product is called Direct Links, which we launched in Q3 […]

As we noted at our Investor Day, we saw 88% higher outbound click-through rates and a 39% decrease in cost per outbound click for CPC objectives from early adopters. We plan to roll Direct Links out to the remaining eligible lower funnel objectives, including CPC video ads and conversion ads by the end of Q1 ’24 to increase our penetration of Direct Links and lower funnel revenue.”

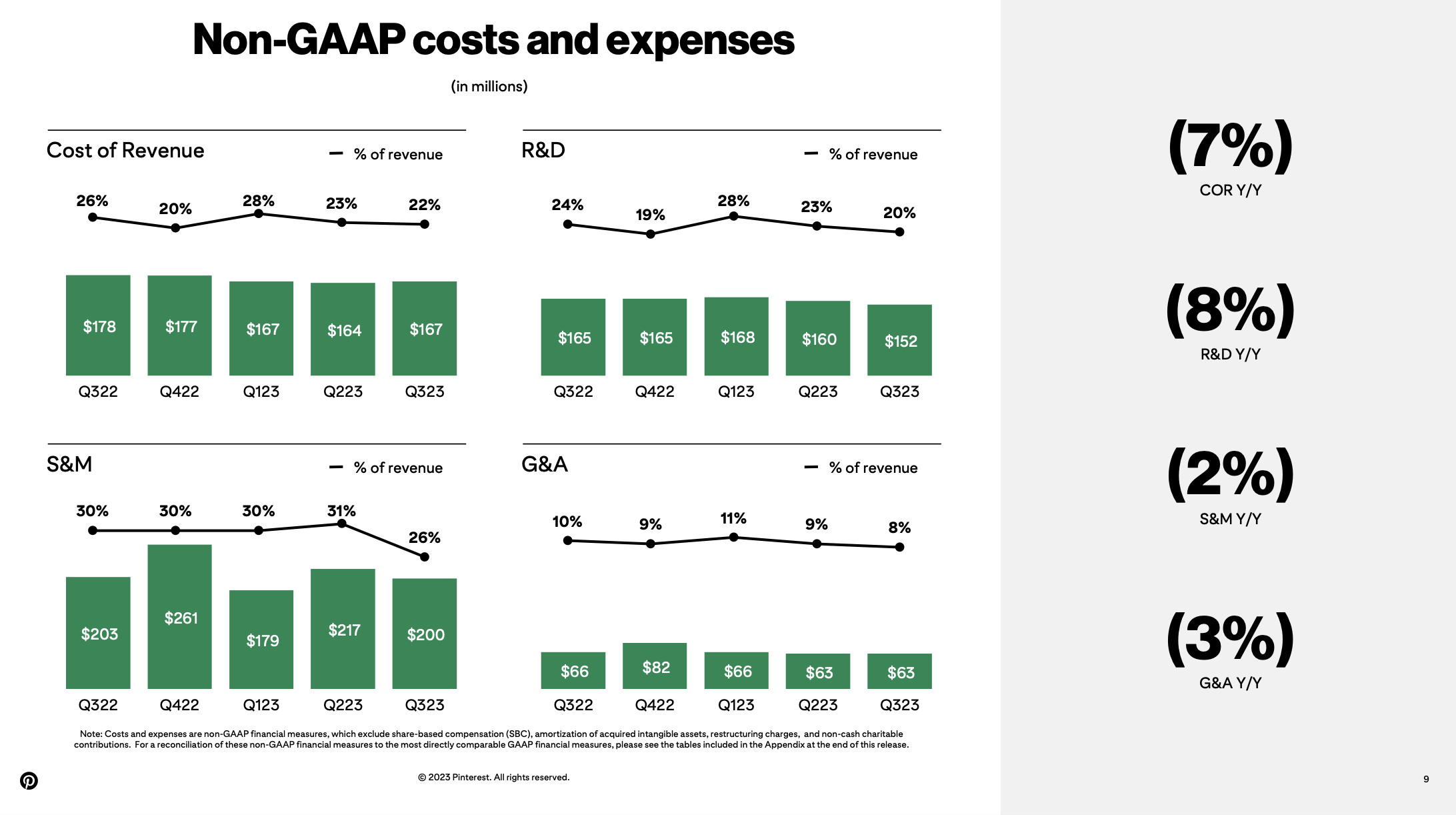

Combined with higher ad click-throughs, Pinterest’s wide-ranging cost cuts have also reduced spend in all areas of the company’s P&L:

Pinterest cost profile (Pinterest Q3 investor deck)

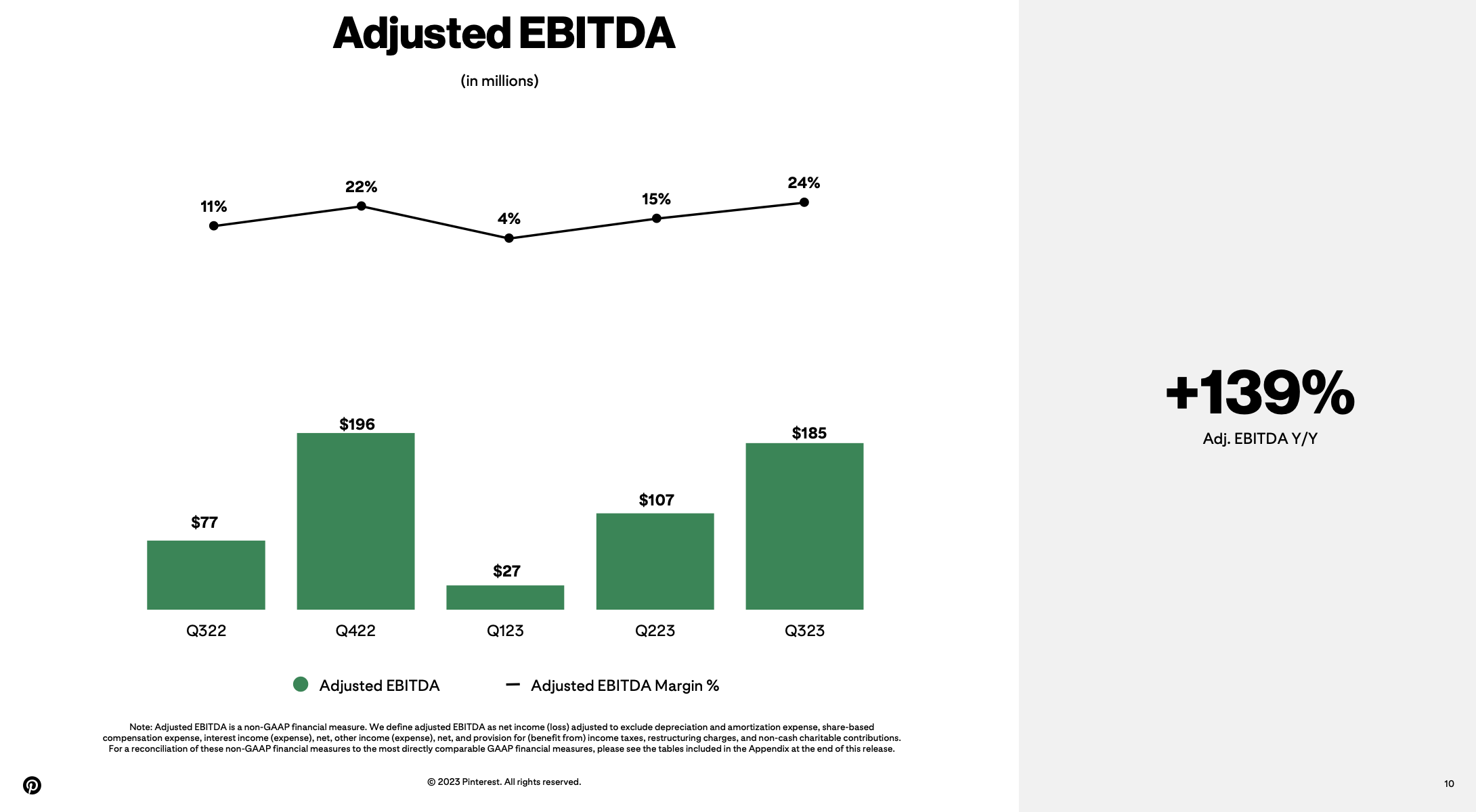

This, in turn, has driven a record adjusted EBITDA margin of 24%, while nominally adjusted EBITDA grew 139% y/y to $185 million:

Pinterest adjusted EBITDA (Pinterest Q3 investor deck)

Key takeaways

With a relatively modest valuation, ARPU growth in the U.S. plus MAU growth in the non-U.S., as well as a favorable cost profile that is leading to substantial adjusted EBITDA expansion, it’s a new day for Pinterest stock. Look for a buying opportunity in the mid/high $20s here.

Q2 2024 Earnings Call Transcript")