cholwanich/iStock via Getty Images

In our last coverage of iShares Preferred and Income Securities ETF (NASDAQ:PFF) over two years back, we highlighted that the fund was destined to give you relatively poor returns for the risk.

With both asset classes that drive preferred share valuations remaining insanely expensive, caution is the name of the game. We don’t think diving into an ETF to get 4.17% a year is the best choice. While most websites (and even Y-Charts below) list PFF’s trailing yield of 4.50%, the current SEC yield is now 4.17% and that is what you will most likely get in dividends over the next 12 months at current price.

Source: Preferred Shares In The Danger Zone

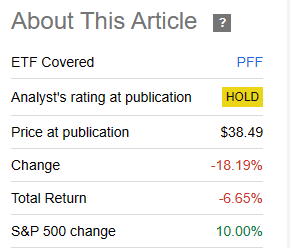

PFF has held true to the forecast and has returned a negative 6.65%, even after adding back 2.5 years’ worth of taxable dividends.

Seeking Alpha

We update our forecast here and tell you three reasons you should stay away, or consider exiting.

1) Rich Valuations Breed Complacency

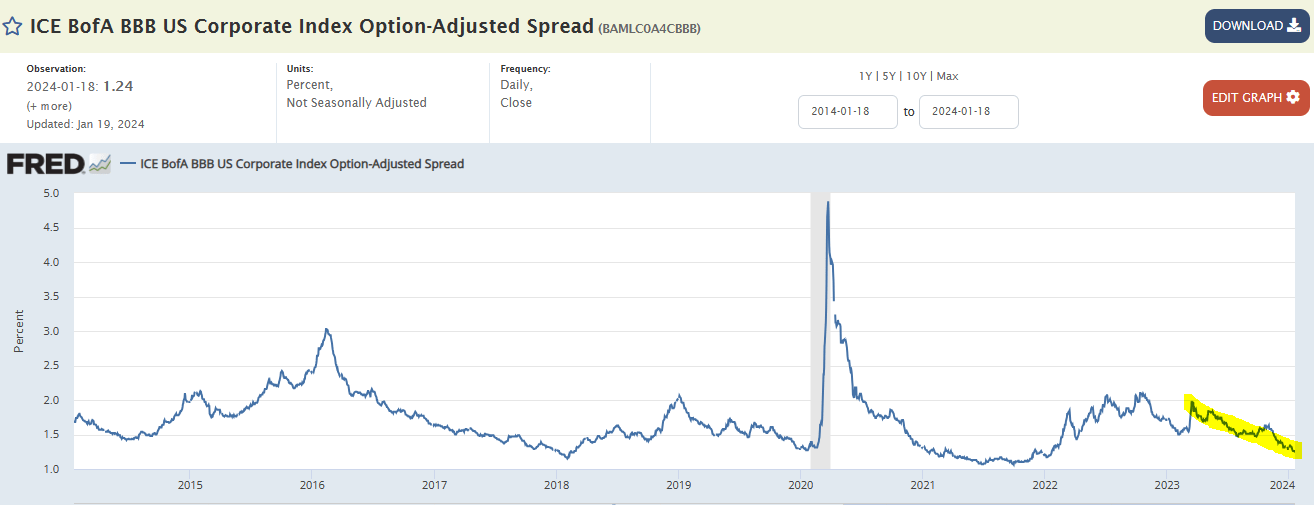

With stocks you have a wide range of valuation measures, and they all point too poor to extremely poor long term outcomes. But how do you measure whether fixed income is attractive or not? While, we always evaluate on a case by case basis to find undervalued plays, one can get a broad view of the asset class by examining spreads. These can be in junk bonds, investment grade bonds or even in preferred shares. There is a lot of room to play around with these metrics and there is really no hard and fast rule. One simple measure that gives a broad view of how things line up, is the ICE Bank of America (BAC) BBB US Corporate Index option adjusted spread.

FRED

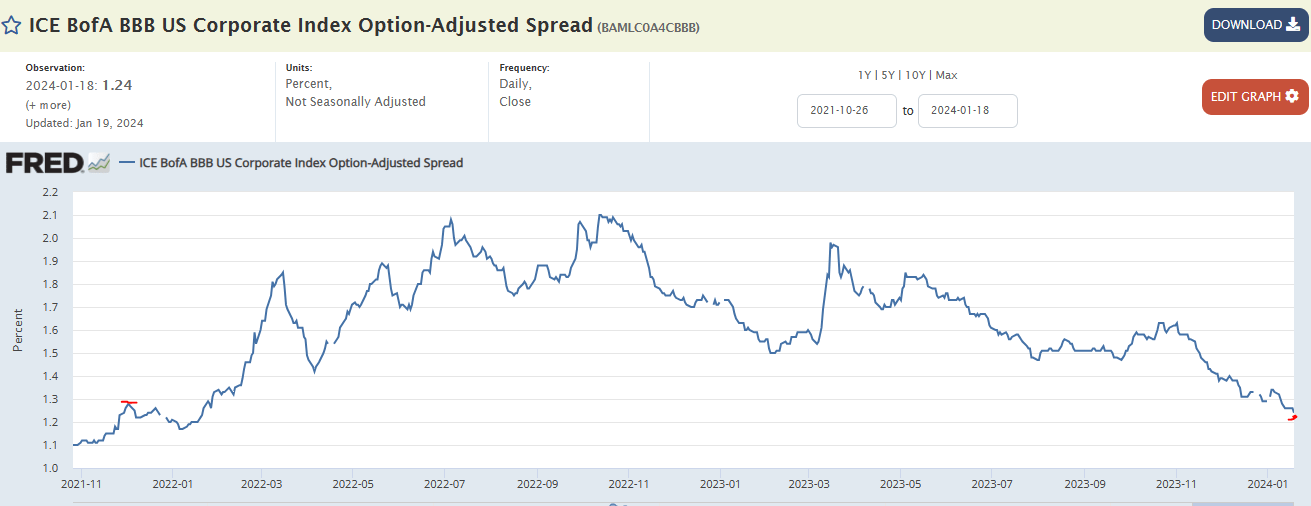

That metric peaked in late 2022 in this cycle and then made a lower high in March 2023, despite regional bank concerns. At present we are now closing in rapidly on the lows of late 2021. This might be hard to visualize in the chart above so we are going to zoom in. Note that the spread today is even below what we saw just before the 2022 selloff began.

FRED

We think at this point, fixed income should be approached with a high level of caution, similar to what we felt in October 2021.

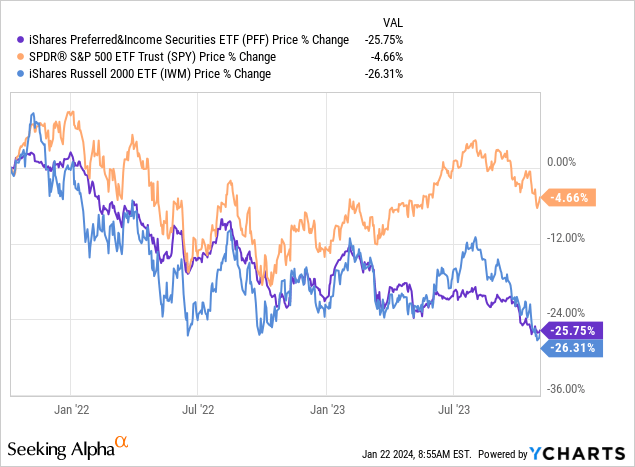

2) PFF Is Functioning Like A Small Cap Fund With Yield

PFF is full of financials and in there, you have a lot of mega banks and a lot of regional ones. Knowing that, what would you think its performance would mirror over the last 28 months? You probably would assume this would move like a large cap index. After all, fixed income should be less volatile than even large cap stocks. What has happened is that PFF has been hitched to the iShares Russell 2000 ETF (IWM). Below we show the price only performance from October 7, 2021 to October 31, 2023.

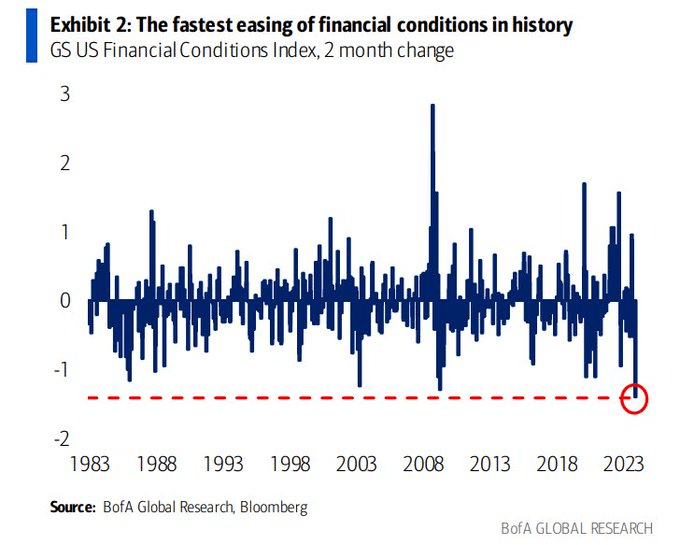

There have been good levels of recovery off those lows, but PFF has got that on the back of the biggest easing in financial conditions.

Bank Of America

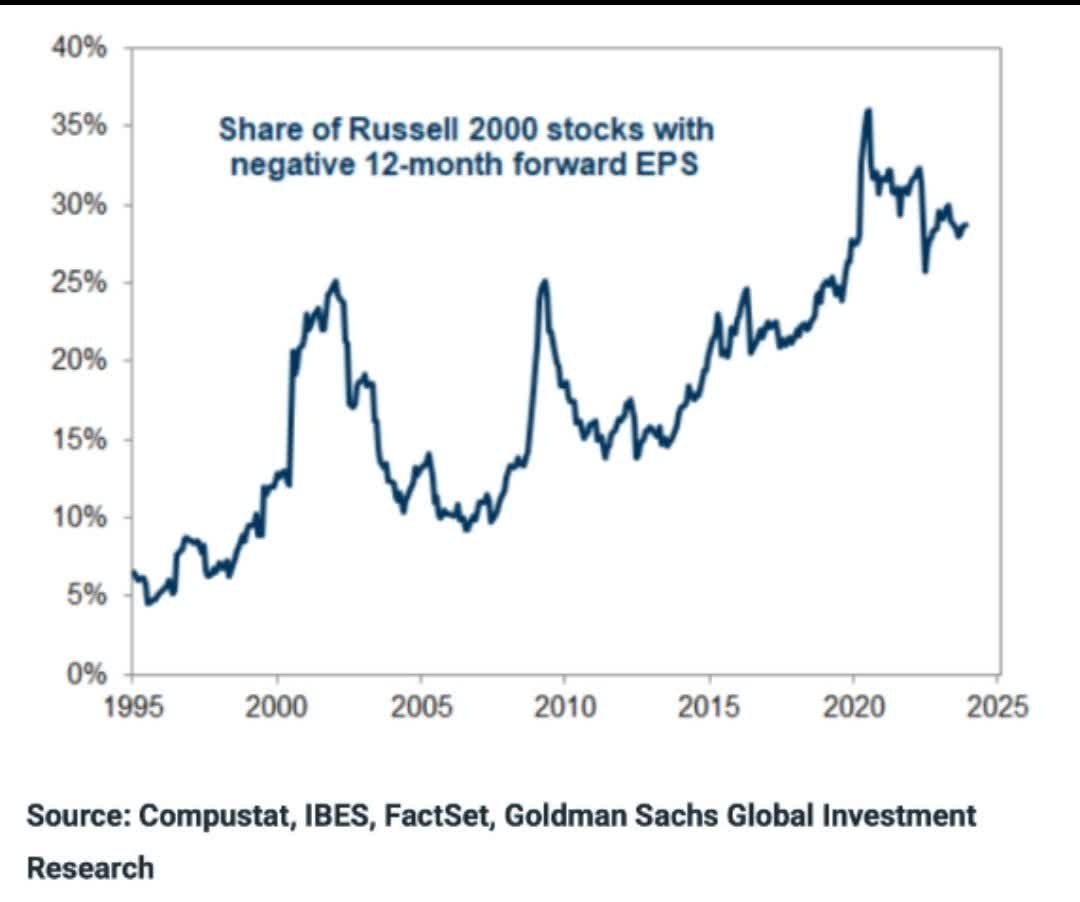

Going forward, we think the soft-landing forecast has to work perfectly for PFF to hold this level of NAV. Otherwise, it will follow what happens to IWM, which in turn is setup about as bad it can be for a recession.

Goldman Sachs

3) Much Better Yields If You Do The Work

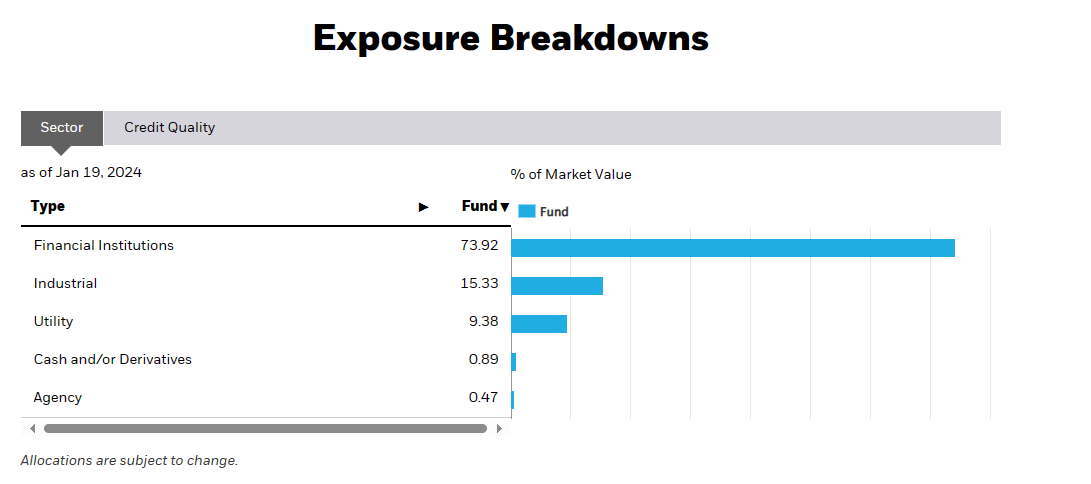

With PFF you are relegated to the index and that index is essentially a bet on the banks.

PFF

But there are far better yields available if you do the work. For example, we highlighted Brookfield Infrastructure Partners L.P. 5.125 CL A PFD13 (BIP.PR.A), which holds a very solid BBB- rating, when it was yielding 7.8%. If you like a higher yield with a lower risk profile, there are many that come into play. Yes, you have to wait for them and you cannot buy them all on the first day of making such a goal. But you can definitely do better than PFF on this front.

4) Rebalancing Tends To Lose Cash

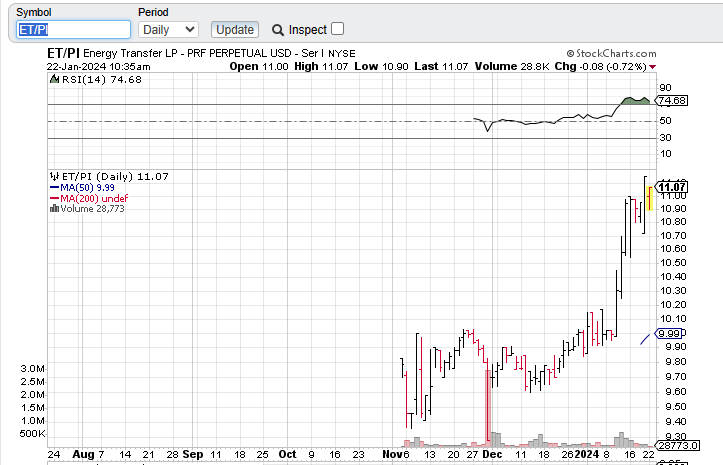

Anyone who has observed what happens to preferred shares on the last business day of the month has seen this madness in action. There is some rather unbridled dumping and bidding up, regardless of fundamentals as PFF rebalances. Here is one example. Note the price action in Energy Transfer LP 9.250% FXD PFD I (ET.PR.I) on the last business day of December 2023.

Stock Charts

It was mercilessly dumped by some fund and it is our experience that is almost always the PFF rebalance effect. ET.PR.I dropped from $9.80 to as low as $9.30. Guess who is paying for selling those that low today?

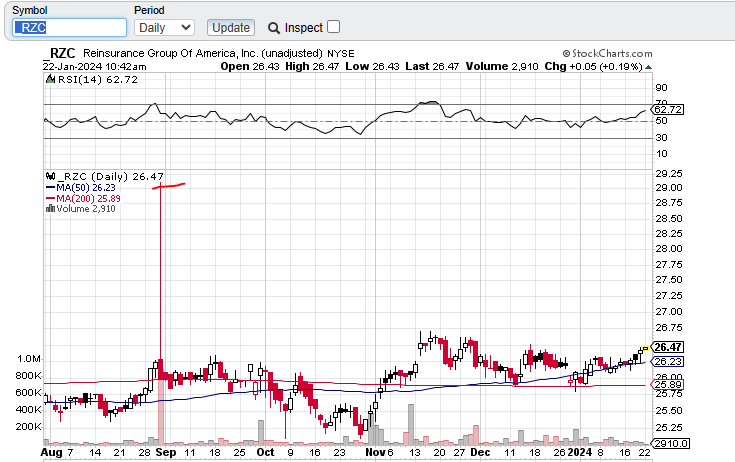

Here is another example, but in the opposite direction. Reinsurance Group of America, Incorporated NT CAL 52 (RZC), the baby bonds of Reinsurance Group of America (RGA), are actually held within PFF. These are not preferred shares, but they make it into PFF. That’s fine. What is not fine is this bidding on the last business day of August 2023. These traded over $29.00 at one point.

Seeking Alpha

Who do you think bought these?

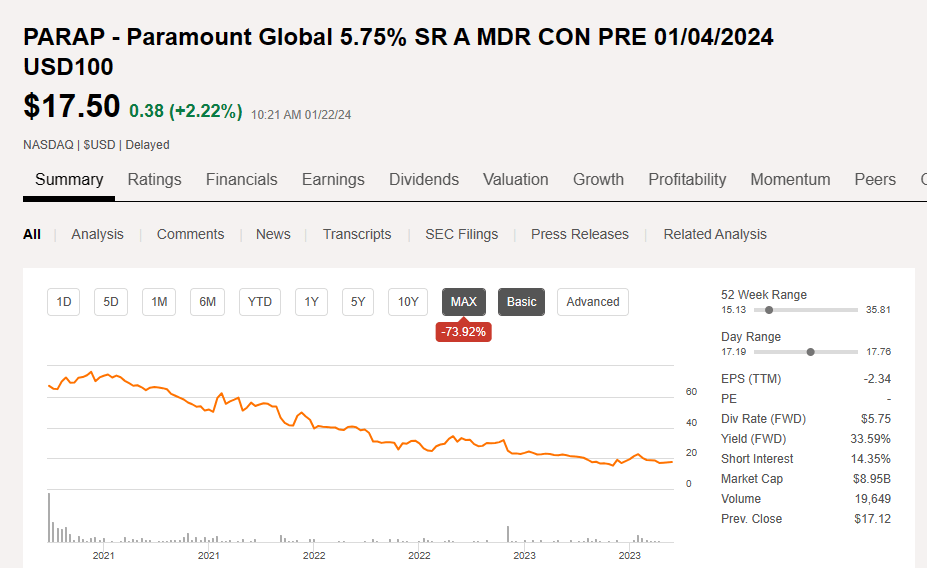

PFF has also held Paramount Global 5.75% SR A MDR CON PRE 01/04/2024 (PARAP) pretty much since these started trading publicly. As we have previously shown these mandatory convertibles were horribly priced and guaranteed to have the worst outcome. That has come to pass.

Seeking Alpha

So this passive ETF has some big drawbacks and that is one of the reasons why your returns have been subpar for years.

Verdict

PFF is a hard one to get behind today with the current credit spreads. That alone should be reason enough for you to look elsewhere. Passive methodology might be a big success for the S&P 500 (SPY), but within the preferred space, active management pays off big time. You are getting better yields if you just look hard and exercise a modicum of patience. This applies to preferred shares and to bonds, both baby and regular. As the credit landscape changes, we think opportunities should multiply and give you a lot of good risk-reward setups. PFF is not one of them.

Please note that this is not financial advice. It may seem like it, sound like it, but surprisingly, it is not. Investors are expected to do their own due diligence and consult with a professional who knows their objectives and constraints.

Q2 2024 Earnings Call Transcript")