AzmanJaka/iStock via Getty Images

Thesis

The Invesco High Yield Equity Dividend Achievers ETF (NASDAQ:PEY) is positioned precariously at the hard-to-execute intersection of high-dividend payments and following an index-based strategy. While the ETF’s strategy of mirroring the Nasdaq US Dividend Achievers 50 Index offers an attractive proposition through its portfolio of high-yield dividend stocks with a record of growth, this approach is not without its drawbacks.

The fund’s largest holding, Walgreens Boots Alliance (WBA), exemplifies the risks involved. WBA’s recent struggles, including a stock price decline and index removals, illustrate the potential volatility PEY faces due to its lack of management flexibility in holding selection.

Moreover, the ETF’s performance has not kept pace with its peers, as indicated by the lag in momentum and heightened risk. This underperformance is exacerbated by PEY’s management fee, which is above average for its category, thereby diminishing its value proposition when returns are already compressed.

Taking these factors into account, my recommendation for PEY is a hold. Investors should exhibit caution, considering the fund’s rigidity in strategy, current vulnerability due to its WBA exposure, and the fees that cut into the overall returns.

Strategy

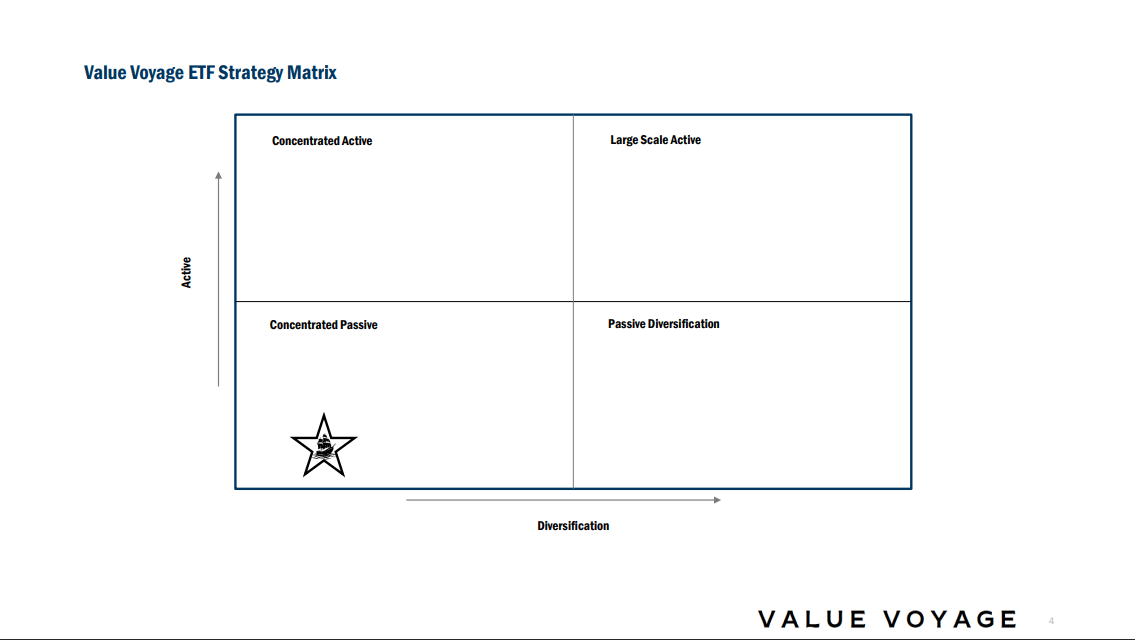

Value Voyage ETF Strategy Matrix (Author’s Calculations)

PEY is designed for investors seeking high dividend yield combined with dividend growth. It follows the Nasdaq US Dividend Achievers 50 Index, focusing on U.S. equities with high dividend yields and a history of increasing dividends. This strategic choice ensures that PEY invests in financially healthy companies capable of sustaining and growing their dividends over time (10-year increase in dividend increases), offering a blend of income generation and potential capital appreciation.

PEY’s investment strategy emphasizes diversification across various sectors, reducing the risk associated with individual stocks or specific market sectors. PEY targets companies with strong business models and financial stability by selecting companies that have consistently increased their dividends. This approach mitigates potential volatility and risk, aiming to provide a steady income stream to investors through dividends, which are attractive during various market conditions.

Overall, we rate place this ETF in the “Concentrated Passive” quadrant within our ETF strategy matrix, as this fund has around 50 holdings and actively changes the portfolio with movements in the overall market.

Investing in companies with very high dividends can be attractive due to the potential for substantial income. However, it carries risks, such as the sustainability of high dividends if they exceed earnings over time, which might indicate financial instability. High dividends could also suggest a lack of better investment opportunities within the company, limiting growth potential. Moreover, a focus on high-dividend yields might expose investors to sector concentration risks, as certain industries are more prone to offer high dividends.

Holdings and Recent Transactions

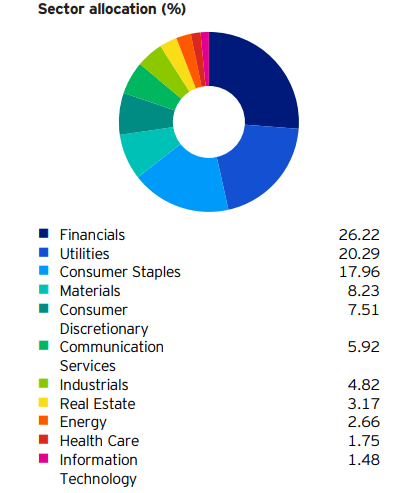

PEY Sector Allocation (PEY Factsheet)

As of the latest report, PEY presents a diversified portfolio emphasizing stability and income through high-dividend-yielding stocks. The top five holdings in the fund are Walgreens Boots Alliance, constituting 3.94% of the portfolio, followed by Nu Skin Enterprises Cl A at 3.63% (NUS), Altria Group Com at 3.14% (MO), Lincoln National (LNC) at 3.09%, and Kennedy-Wilson Holdings at 2.78% (KW). These companies, spanning various sectors such as healthcare, consumer goods, and financial services, underscore PEY’s strategy to leverage sectors with a reputation for reliable dividend payouts, reflecting the fund’s objective to provide investors with a steady income stream alongside potential capital appreciation.

In the recent half-year period, PEY has made portfolio adjustments. The largest buys included Nu Skin Enterprises Inc Cl A, Walgreens Boots Alliance, Scotts Miracle-Gro Cl A (SMG), Kennedy-Wilson Holdings, and Leggett & Platt Com (LEG). Conversely, the fund executed significant sales during the period, parting ways with positions in Telephone & Data Systems (TDS), V.F. Corp. Com (VFC), HNI Corp. Com (HNI), KeyCorp (KEY), and Phillips 66 (PSX).

The actions look to be nothing more than basic rebalancing to ensure the tracking of their Benchmark, although I will discuss one large holding in the next section.

Walgreens Exposure

When reviewing PEY’s holdings, one firm stands out as a clear problem child with the overall portfolio: Walgreens Boots Alliance. Not only does this firm have a significant stock price decline over the last year, but has since been removed from S&P 500 Dividend Aristocrats, and will likely be removed from the Dow Jones Industrial Index soon.

This is often why the lack of flexibility is a headwind for many ETFs that track an underlying index; there is often little room for the managers of the ETF to actively remove a firm that has near-term headwinds and will likely drag performance. Notably, there’s a prevailing expectation that WBA may reduce its dividend in the foreseeable future. Such a move would likely result in Walgreens Boots Alliance being removed from the underlying index that PEY tracks, given the ETF’s focus on high-dividend-yielding companies. Despite this anticipation, it’s important to recognize that, in the near term, PEY continues to have substantial exposure to Walgreens, which adds significantly to our hold rating.

It’s also fair to say that at 3%, it doesn’t represent a significant downside risk to the fund, which is true. I contend that this exposure represents a significant comparative risk to PEY versus their counterparts, which are much more diversified and don’t have the largest of the fund’s exposure to WBA:

PEY Peer Concentration (Seeking Alpha)

Comparable Tickets and Performance

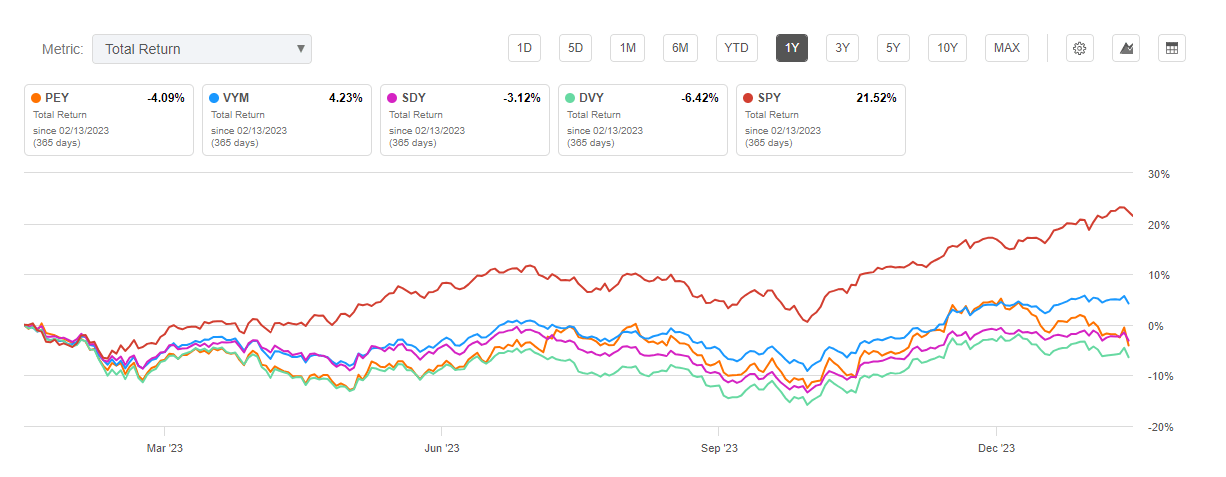

PEY Returns (Seeking Alpha)

PEY lags its peer and overall market performance considerably over the one-year timeframe, and this performance has been consistent throughout its inception. While some readers may note that the comparison here is not to the benchmark as a whole but instead the SPY and overall market, I pose the question of why would the individual investor ever invest in anything that does not generate alpha over the broad market index, given the considerable ease of which an investor can access this.

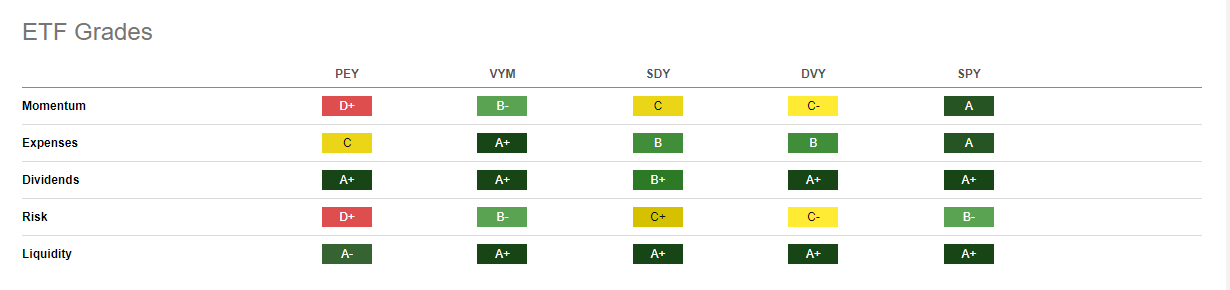

ETF Grades (Seeking Alpha)

When compared with its counterparts such as (VYM), (SDY), (DVY), and the broader market indicator (SPY), PEY’s momentum and risk grades, as reflected in the ETF Grades chart, fall short, receiving a D+ and D- respectively. This suggests that PEY has not capitalized on market movements as effectively as others and may carry a higher risk profile.

A particular point of concern for investors may be PEY’s management fee, which is significantly higher than those of its peers:

PEY Fee Comparison Versus Peers (Seeking Alpha)

While PEY offers an attractive dividend yield, as noted by its A grade in dividends, the combination of lower momentum, higher risk, and elevated expenses could contribute to its underperformance relative to peers.

Investors may also weigh the liquidity of the fund, which stands with an A grade, indicating ease of entry and exit in the market. However, this benefit is somewhat overshadowed by the fund’s performance metrics when compared to similar investment vehicles. The underperformance, coupled with a higher fee structure, suggests that investors in PEY are paying more for management while potentially receiving less in terms of total return, a consideration that could prompt a reevaluation of the fund’s position within an investment portfolio.

Recommendation

Based on my analysis, I issue a hold recommendation for PEY.

My reasons for this rating are straightforward. First, the lack of flexibility inherent in PEY’s index-based strategy has been highlighted as a significant limitation, particularly as it pertains to the ETF’s largest holding, WBA. Furthermore, PEY’s performance has been consistently lagging behind its peers and the broader market, as evidenced by the one-year timeframe returns and the ETF’s grades in momentum and risk. This underperformance is not justified by the higher management fee PEY charges, which stands above the average for its category, further diminishing the fund’s appeal. Finally, while PEY’s high dividend yield and liquidity are positive aspects, they do not fully compensate for the fund’s shortcomings in performance and cost efficiency.

Q2 2024 Earnings Call Transcript")