gilaxia

PetIQ (NASDAQ:PETQ) is undergoing a much-needed cost-cutting program as the company continues to support its strong cash-generating product segment while closing inefficient clinics in the services segment. This can put the company on a spiral of higher revenues, higher EBITDA margin, and eventually higher FCF. All these milestones together would support a valuation re-rate in terms of EBITDA multiples, and we see an upside potential of around 30%.

Margins expansion and revenue growth expected ahead

In our last coverage of PETQ, in January 2022 we spoke about the great opportunity that pet care centers operated by the company represented. However, years later we find out that we were wrong. The true opportunity was indeed embedded in their product segment, and the services division is still struggling with poor margins. We think this is also the reason that is keeping the stock from trading at more generous multiples, as a company trading at this magnitude and generating this much cash deserves.

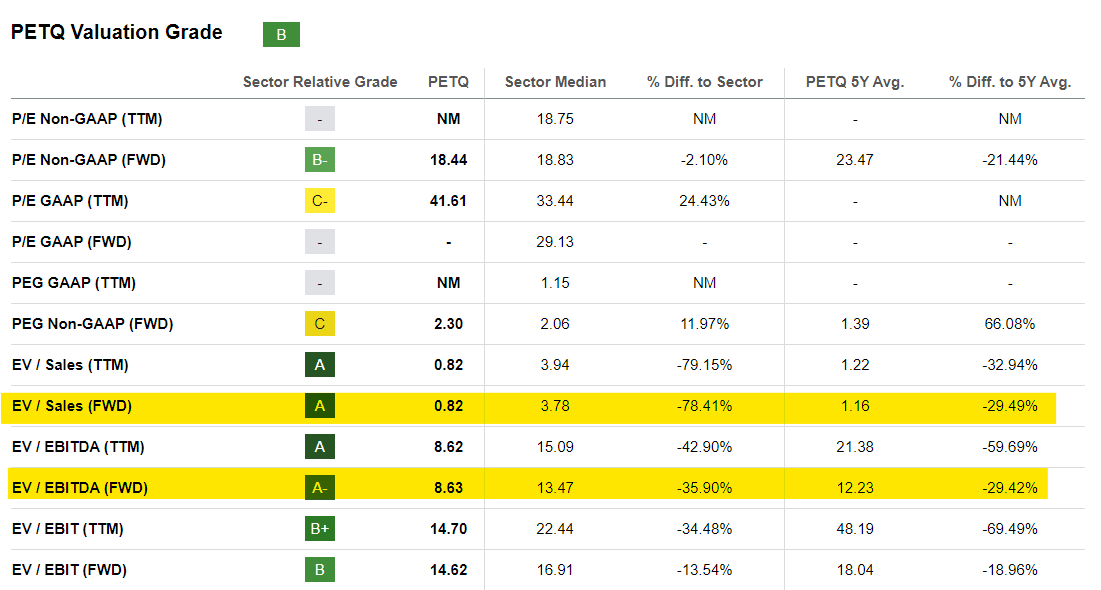

PETQ – Valuation Multiples (Seeking Alpha)

There is indeed a substantial discount on both EV/EBITDA and EV/Sales both compared to its peers, and its 5-year average. But this is in clear contrast with the cash generation and topline growth that the company is experiencing in the last few years.

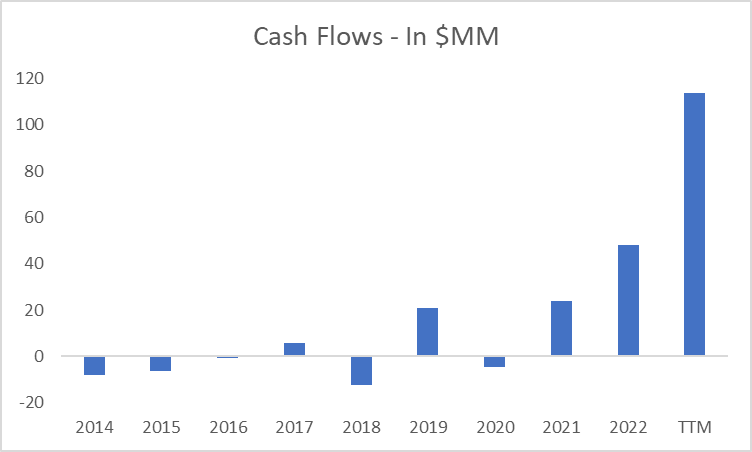

PETQ – Cash Flows (Seeking Alpha)

Cash flows from operations almost skyrocketed to a new high above $100 million in the last twelve months, putting an end to a period of negative cash flows and consolidating 3 years of consistently positive numbers.

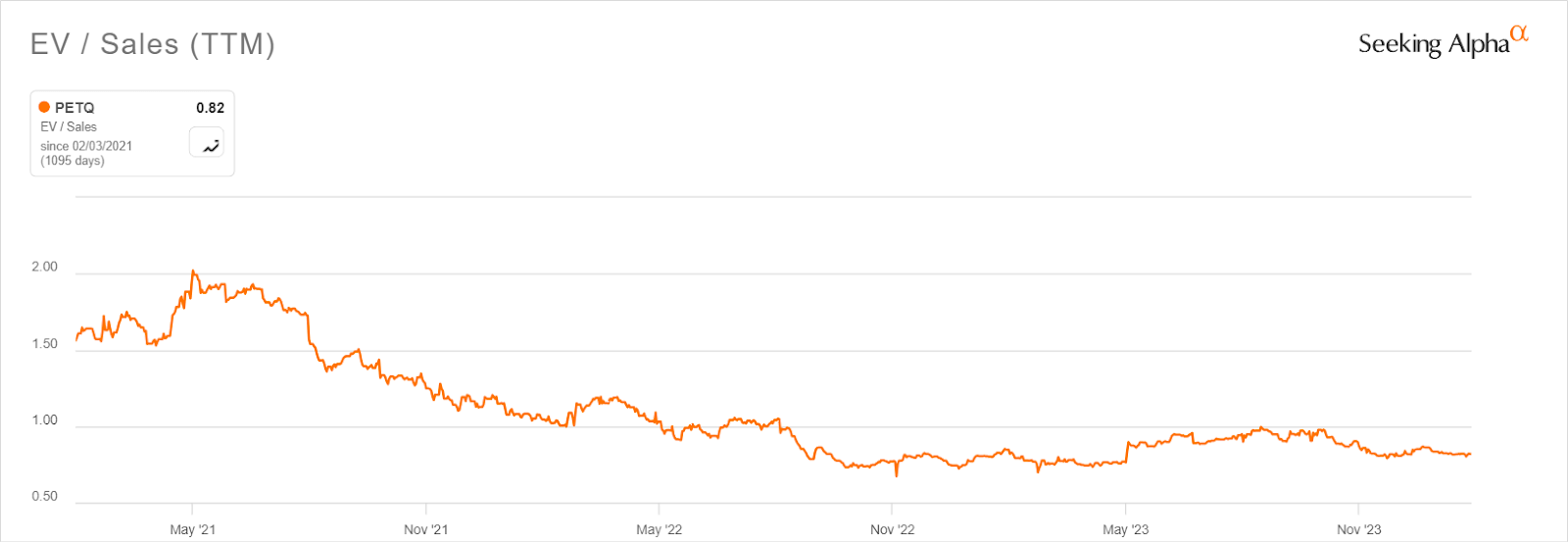

But instead of cheering for the new successes, the market remained very skeptical and lowered the multiples it attached to the business, as shown by a staggering decline in the EV/Sales ratio. This may be also driven by some seasonality that affects their business model. Indeed, Q3 earnings came 10% lower than Q2, but still some 30% higher YoY. This is mainly driven by a usually weaker business activity during the summer, as also in 2022 we saw an 8-10% decline between Q2 and Q3. Nevertheless, this was likely taken as a negative sentiment sign by the market which continued to lower the multiples.

PETQ – Historical EV/Sales (Seeking Alpha)

We believe there is an opportunity for PETQ to drive a valuation re-rate if (1) management is able to implement the cost savings on the services segment, and (2) put in place stronger remuneration for shareholders. In the last earnings call a savings plan was announced as the company planned to shut down several underperforming clinics and save at least $6 million per year. From the call:

As we announced in today’s earnings release, late in the third quarter, we initiated a Services segment optimization to close 149 wellness centers in an effort to improve future profitability. We expect to generate approximately 6.3 of net cost savings over the next 12 months, all of which we anticipate reinvesting into our future growth, focusing primarily on the growth of our mobile community clinics and sales and marketing initiatives for our manufacture brands.

We think this is great news as it shows that management is aware of the damage that running a sub-optimal segment does to the overall valuation. The shift towards mobile clinics should lower SG&A expenses and Capex, thus inflating EBITDA and FCF. Also, it will redirect the attention of the market towards the valuable product segment, as management plans to re-invest these savings into marketing for their strongest manufacturing brands.

The franchising opportunity: the way to extraordinary multiples

We also think that the services segment is probably run in a structurally inefficient way. Owning clinics, opening new ones and closing the underperforming ones, hiring staff, running complex analyses to find the best markets, well, it’s expensive. There is a simple reason why McDonald’s is so successful: franchising. We did not find mentions of this strategy on the calls or the filings, but we believe that the most successful strategy for the company would be to franchise all its clinics and create an integrated network for marketing spending and product distribution. PETQ will collect both royalties on sales and be able to create a nationwide platform to physically sell their high-value proprietary products at a fraction of their current cost base.

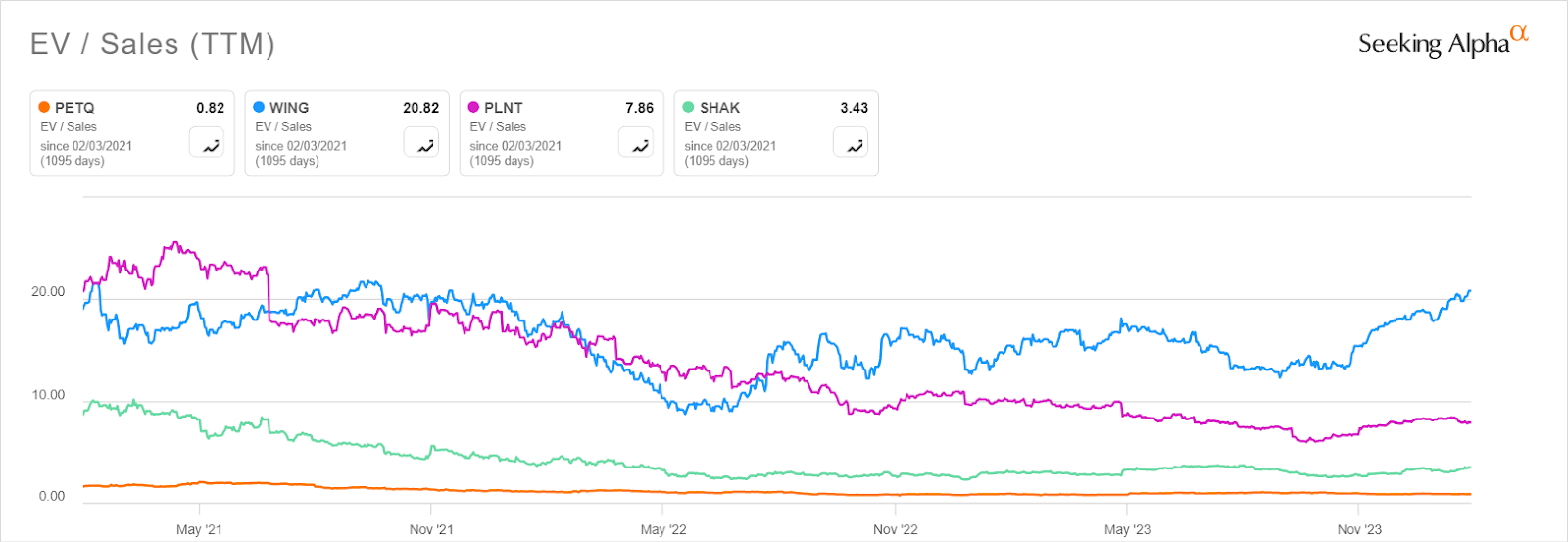

For comparison, we see the EV/Sales multiples attached to fast-growing franchise businesses, and it is simply a staggering difference to PETQ:

PETQ – EV/Sales Comparison (Seeking Alpha)

The least expensive one, SHAK, trades at 3.4x times sales, almost 4 times higher than PETQ’s 0.8x multiple. This would create an enormous re-rate opportunity as it would set the company on track to reach record EBITDA margins and slash Capex. We hope that soon enough management will recognize this strategy, or an activist shareholder will step up to point it out, as it would be company-changing.

Risks: consumer spending and competition

We believe there are two main risks out there for a company growing at the pace of PETQ: a slowdown in consumer spending as fiscal deficits go away, and increased competition as the high margins attract new products. The first one is a systemic risk affecting virtually every company, but we need to consider it in our thesis as it may impact revenues and cash flows. GDP growth has been strong this year, but there is uncertainty in 2024 with elections coming up and thus lack of visibility on fiscal spending, which is a key driver of consumer demand.

The second risk is more specific to PETQ. The company has been running record cash flows and profits selling its proprietary products, and we are worried that this may attract unwanted competition. We feel that they still benefit from first-mover advantage and the scale of their clinics’ presence surely helps with brand and product awareness. However, it is still a tangible risk to consider as we move forward and it could materialize in 3-4 years from now.

Valuation: finding the right multiple in the midst of changes

Our main takeaway is that the stock will eventually face a valuation re-rate with the expansion of multiples favored by higher margins. This will likely occur as the market recognizes the improvements during FY 2024.

To find a proper fair price per share, we will use a scenario-based analysis where we compare the associated EBITDA margin gains reached over the next 12 months and the subsequent multiple that the market will likely attach. Of course, the re-rate is not driven by the actual improvements alone, but rather by expectations of subsequent improvements in 2025, 2026, and beyond. For the last 12 months, the EBITDA margin stands at 9.5%. In each scenario we compute (1) Revenues, (2) EBITDA, and (3) the attached multiple which is taken considering comparables. The sector median EV/EBITDA stands at 13x, and we base incremental multiple improvements that go towards that level.

Our scenarios are the following:

-

Bear case: competition and slowing demand will impact topline growth and margins as discounts will affect selling prices. We believe that the combined effect on EBITDA would be a decline to 9%, which combined with the topline decrease of around 5% means actual EBITDA of $90 million. Coped with a multiple of 7.5x this means a fair price of $13 per share.

-

Base case: modest improvements by closing inefficient clinics translates into an EBITDA margin of 10%, with topline growth similar to historical levels at 10%, we end up with an EBITDA of $117 million. By applying a multiple expansion of just 0.5x times, to 9x times, we end up with a fair value per share of $26.

-

Bull case: significant cost savings and possible conversion to a franchise model in the next few years would significantly boost the valuation multiple. We assume the same gains in EBITDA in the short term as of the base case, but a multiple expansion to 11x times EBITDA. This translates into a fair price per share of $34.

We also assume these probabilities for each scenario, respectively: 20%, 70%, and 10%. We are apparently skewed towards our bearish case, but this is to remain conservative in our estimates. This also better reflects the execution risk embedded in the plans. The overall fair price per share is then $24, with an upside potential of around 30% from the current levels.

Conclusion

PetIQ is an outstanding pet wellness company that is implementing a modest but potentially effective cost-cutting program in its services segment. This, coped with deeper fundamental changes (i.e. franchising), and the natural growth historically experienced, suggests that a valuation re-rate is possible. We estimate a fair value per share that is 30% above the current price.

Q2 2024 Earnings Call Transcript")