Michael Burrell/iStock via Getty Images

Investment thesis:

Perdoceo Education (NASDAQ:PRDO) sports an attractive valuation at just 8.4x forward P/E versus the sector median of 15.4x and has posted solid financial performance including expanding operating margins and a healthy balance sheet. However, the for-profit education industry faces intensifying scrutiny under the Biden administration over issues like gainful employment and 90/10 rule changes, and Perdoceo itself is under investigation by the Departments of Education and Justice. Recent insider stock sales by executives along with the surprise resignation of the company’s CEO in less than two years also raise some caution flags. I believe the stock deserves a hold rating due to mounting regulatory headwinds, at least until there’s further clarity.

Company Overview

Perdoceo operates three primarily online for-profit universities – Colorado Technical University and American InterContinental University. Perdoceo operates exclusively online, with over 97% of its ~39,000 students enrolled in online degree programs across business, IT, healthcare, and other fields as of the last 10k filing. Enrollments as of the most recent quarterly release are at 36,400, declining consistently year-over-year. The student body is also largely non-traditional, with 76% enrolled in business programs and 68% aged over 30. TTM revenue is $730 million.

Regulatory Troubles Mounting

The for-profit education industry has faced growing scrutiny in recent years from regulators and policymakers. Efforts by the Department of Education to limit eligibility and federal aid for poor-performing programs or schools could significantly impact players like Perdoceo.

Specific areas of focus include the 90/10 rule, which caps the share of revenue that for-profit colleges can receive from federal student aid sources. An even more restrictive version has taken effect in 2023 which has made compliance more challenging. Breaching the 90/10 limit for two straight years would threaten accreditation and federal aid eligibility.

There is also a push to bring back “gainful employment” regulations that were rescinded in 2019. These rules can revoke federal aid eligibility for programs whose graduates have excessive debt burdens compared to earnings. The Department has signaled plans to introduce new gainful employment rules in 2023.

Perdoceo faces not only stricter legislation but greater enforcement as well. Both the Department of Education and the Department of Justice have sent information requests regarding the company’s student recruiting, marketing, and financial aid practices. This has affected student enrollments over the last few years, which are down from 42,700 in 2020 to 36,400 as of the last reported quarter.

CEO Departure & Insider Sales

In November 2023, Perdoceo announced the surprise resignation of CEO Andrew Hurst after less than two years on the job. The company reinstalled former chairman and CEO Todd Nelson to the top post.

While the reasons for Hurst’s exit are unclear, the abrupt change raises questions about the company’s leadership stability and strategic direction. Nelson himself brings controversy – he is being sued over the alleged wrongful death of his daughter-in-law, although he has vehemently denied the allegations through his lawyer.

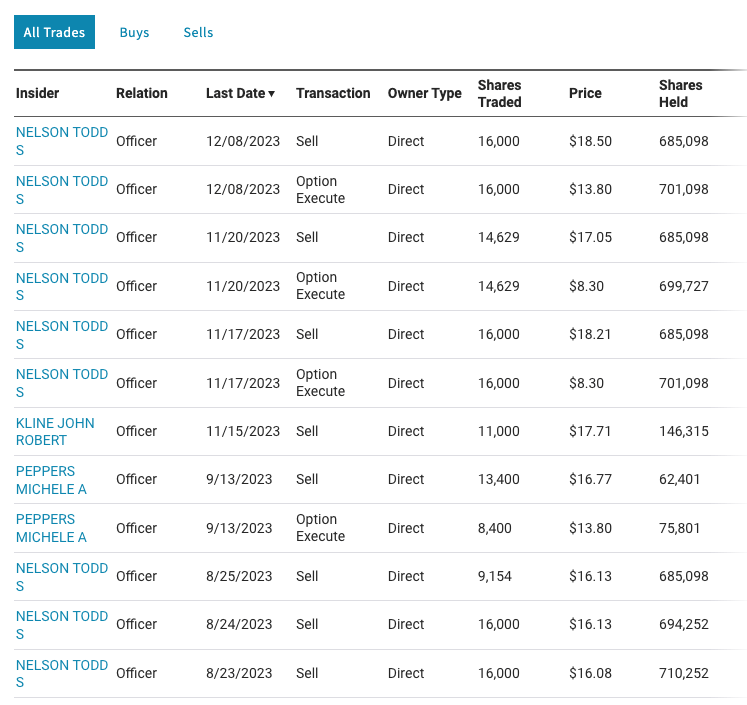

Additionally, Nelson has executed significant sales of Perdoceo stock over the last couple of months. Other executives also offloaded shares last fall. The insider selling hints that leadership may see further downside ahead.

Insider Activity (Nasdaq)

Financial Performance Solid, Valuation Discounts Regulatory Risk

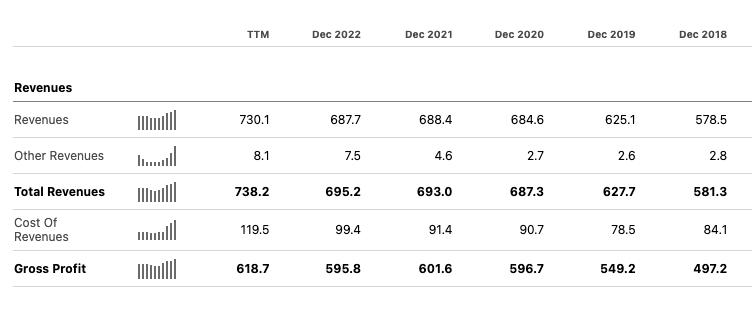

Perdoceo has posted impressive financial results throughout. Despite some hiccups, revenues grew healthily over the last five years, up from $578m to $730m in the last twelve months. Results have been aided by higher student retention and lower general & administrative costs as a percentage of revenue.

Seeking Alpha

The company also carries a solid balance sheet, with ~$600 million in cash against negligible debt. This provides flexibility for organic investments and acquisitions – Perdoceo recently made purchases to expand its offerings in healthcare, IT, and cybersecurity training.

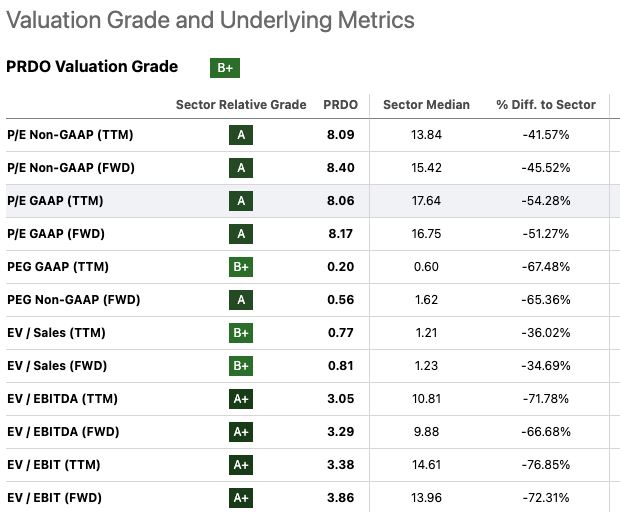

The stock trades at just 8.4x forward P/E compared to over 15x for its closest publicly traded for-profit education peers. A lot of the regulatory risk has already been discounted in the price.

Valuation Scores (Seeking Alpha)

Bulls will point to the potential for continued margin expansion, organic growth opportunities in areas like healthcare training, and upside from recent acquisitions. Execution of the company’s strategy could also make it an attractive takeover candidate.

But ultimately, the regulatory storm clouds make it difficult to get too constructive, especially given the departure of the CEO and insider sales. While the risk/reward calculus seems favorable for value and contrarian investors, I prefer to remain on the sidelines for now.

Upside Catalysts

- Margin expansion if retention remains high and enrollment trends improve

- Accretive acquisitions that expand presence in growing areas like healthcare training

- Regulatory reversals following an administration change

- Settlement of Department of Education investigation without penalties

- Successful integration of recent Coding Dojo and CalSouthern acquisitions

- Stock repurchases supported by large cash balance

Downside Catalysts

- Stricter “gainful employment” rules lead to loss of federal aid eligibility for certain programs

- Failure to comply with new 90/10 rule caps and required audit processes

- Penalties, fines or operational restrictions resulting from DoE investigation

- Reputational damage from controversies hurting enrollment and retention

- Insider sales and CEO change indicative of concern over coming results

- Recession reduces demand for discretionary education spending

- Acquisitions fail to drive growth and require significant investment

Conclusion

Perdoceo Education presents an intriguing risk/reward profile, with solid financial trends and a discounted valuation that may offer a significant margin of safety. However, the elevated regulatory uncertainties, recent senior leadership changes, and insider selling keep me neutral on the stock until there’s more clarity. Value investors can stay opportunistic if any unexpected positive catalysts emerge.

Q2 2024 Earnings Call Transcript")