A background of $100 U.S. banknotes. OlyaSolodenko

Those who have followed me on Seeking Alpha know that my most favored and predominant investing strategy is dividend growth investing. This is because I am a big believer in the keep-it-simple stupid mantra of Berkshire Hathaway’s (BRK.A) (BRK.B) long-time Chairman and CEO, Warren Buffett.

Dividend growth investing helps me to focus my attention on the fundamentals of my investment holdings. Rather than being distracted by the day-to-day market noise, this helps me to focus on the long-term profits and dividends that my portfolio generates and distributes to me. That makes it much easier for me to hold onto/add to my winners over time and let the market do the heavy lifting for me via compounding.

The Power of Dividends – Hartford Funds

The other factor that I like about dividend growth investing is that it has historically worked. Now, there are no guarantees in investing.

But for my money, building wealth with quality dividend stocks is the closest thing possible to a guarantee in this uncertain world. What is my basis for this argument?

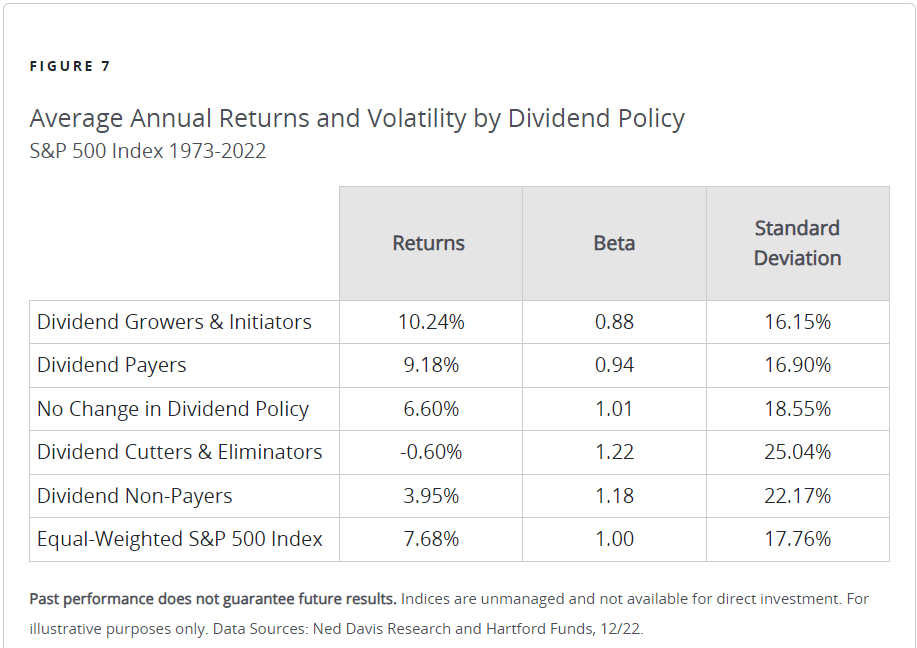

As the Hartford Funds’ The Power of Dividends illustration shows, dividend growers and initiators within the S&P 500 index (SP500) radically outperformed all other dividend policy classes from 1973 to 2022. A $10,000 investment in 1973 in dividend growers and initiators would have grown to over $1.3 million to end 2022 with dividends reinvested. That’s head and shoulders better than the $404,000 that the same amount invested in an equal-weighted S&P 500 index would have been worth at the end of 2022.

Dividend growth investing is one of the most proven investing strategies to build sustainable wealth over the long run and the proof is in the pudding.

Today, I will be focusing on a company that initiated a dividend in 2023. As the article unfolds, I will be explaining why I believe the human capital management company, Paycom Software (NYSE:PAYC), could be the next exceptional dividend grower.

Dividend Kings Zen Research Terminal

Paycom’s 0.8% dividend yield won’t come across as enticing to more income-focused investors. But for me, this is more of a story of the company’s dividend growth potential than its immediate income.

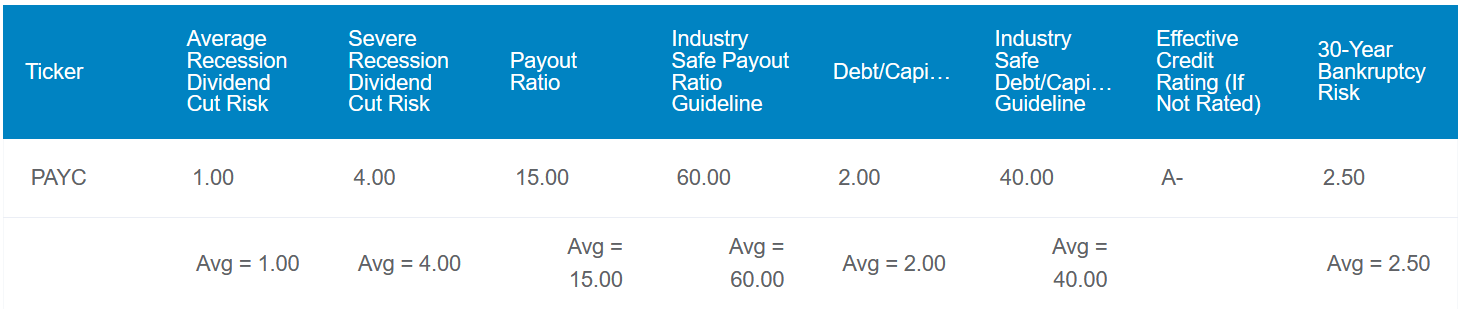

That’s because Paycom’s EPS payout ratio is 15%. This registers at just one-quarter of the 60% that rating agencies desire from the human capital management industry. Earnings growth prospects aside, Paycom has the flexibility to substantially boost this payout ratio as the years progress.

The company’s balance sheet is also pristine, with a 2% debt-to-capital ratio. That’s comfortably below the 40% that rating agencies like to see from the industry.

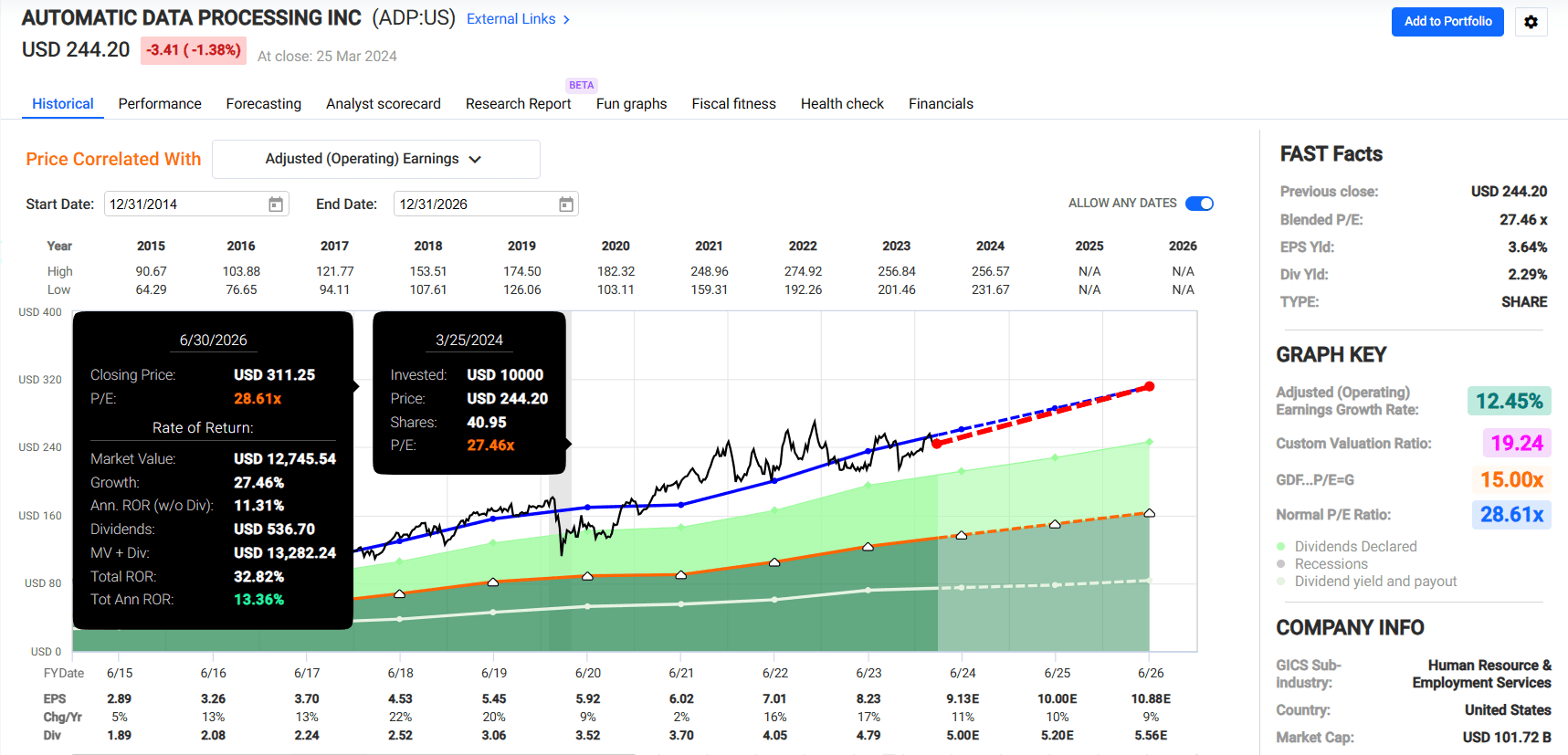

Paycom doesn’t formally have a credit rating from S&P. However, the Zen Research Terminal estimates that its fundamentals would meet the requirements to possess an A- credit rating. For context, that’s better than Paychex’s (PAYX) BBB+ credit rating equivalent and below Automatic Data Processing’s (ADP) AA- credit rating from S&P on a stable outlook. This A- credit rating equivalent implies the risk of Paycom going bankrupt in the next 30 years is 2.5%.

Due to these factors, the Zen Research Terminal projects that the probability of a dividend cut from the company in the next average recession is 1%. If the next recession turns out to be severe, the likelihood of a dividend cut would rise to 4%. These are each respectively double the 0.5% and 2% minimums within the Zen Research Terminal. It’s worth noting, though, that as Paycom demonstrates its commitment to shareholders with payout hikes on its new dividend, its dividend cut chances could improve further.

Dividend Kings Zen Research Terminal

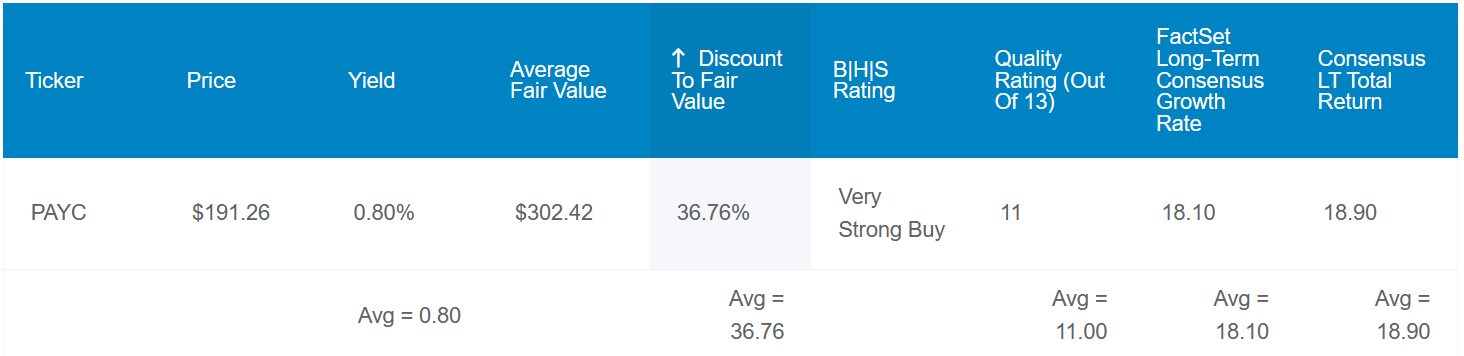

Paycom’s valuation could position it as an appealing buy. Applying a 37.5 P/E ratio to the stock (given its growth prospects and debt-free status), shares could be worth an average of $302 apiece per the Zen Research Terminal. Markets tend to be forward-looking. So, this valuation assumes a weighting of 75% of this year’s FAST Graphs analyst consensus of $7.76 (what’s remaining in this year) and 25% of next year’s $8.85 consensus.

I also arrive at a fair value of approximately $302 a share by plugging the following inputs into the discounted cash flows model: $7.75 in 2023 non-GAAP net income per share, a 9% annual earnings growth rate for the next five years, a 7% annual growth rate thereafter, and a 10% discount rate.

I believe a 9% compound annual earnings growth rate for the next five years is realistic. That’s because when extrapolating the current FAST Graphs analyst consensus of $10.60 for 2026, this is an 11% compound annual growth rate for 2023 through 2026. This provides a roughly 20% buffer with the current analyst growth consensus, which I would argue provides an adequate margin of safety. Additionally, the 7% annual growth rate into perpetuity is well below the long-term consensus potential growth rate.

Combining these fair value estimates, Paycom’s shares could be worth $302 each. That would represent a 37% discount to fair value from the current $191 share price (as of March 26, 2024).

If Paycom can grow as anticipated and return to fair value, here are the total returns that it could produce over the coming 10 years:

- 0.8% yield + 18.1% FactSet Research annual growth consensus + a 4.7% annual valuation multiple upside = 23.6% annual total return potential or a 732% 10-year cumulative total return versus the 9.8% annual total return potential of the S&P or a 155% 10-year cumulative total return

Growth Will Be Muted In 2024 But The Long-Term Story Is Intact

Boasting an $11 billion market capitalization, Paycom is a large-cap player in the human capital management industry. The company’s software products were used in a variety of functions, such as talent acquisition, human resources, and payroll by almost 37,000 clients as of Dec. 31, 2023.

This client base was also well-diversified, with no client comprising more than a half percent of Paycom’s revenue in 2023. The company’s business continued to be almost entirely derived from recurring revenue. This made up 98.3% of Paycom’s revenue in 2023 (info sourced from pages 6 and 60 of 103 of Paycom’s 10-K filing).

Paycom Q4 2023 Earnings Press Release

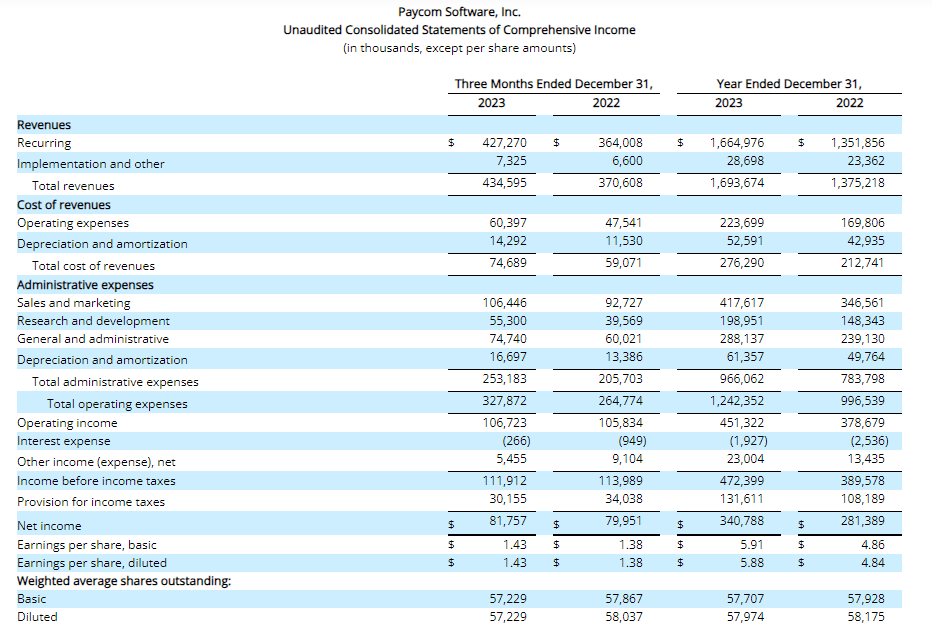

Paycom’s revenue surged 23.2% higher year-over-year to $1.69 billion during 2023. What was behind this topline growth for the year?

As more clients worked to further streamline their operations and outsource functions to Paycom’s software, the Oklahoma-based company benefited from new business wins. Paycom’s responsiveness to client needs also helped its annual revenue retention rate to hold at 90% in 2023, which was down versus the 91% figure recorded for 2022. According to President and Co-CEO Chad Richison’s remarks during the Q4 2023 Earnings Call, this was due to the macro environment of higher interest rates and inflation hurting smaller clients.

Yet, Paycom’s revenue growth was in line with the 23% compound annual growth rate that was logged between 2020 and 2023 (page 42 of 103 of Paycom’s 10-K filing).

Moving to the bottom line, the company’s non-GAAP diluted EPS soared 26.2% over the year-ago period to $7.75 during 2023. Disciplined cost management is what led Paycom’s non-GAAP net profit margin to expand by nearly 60 basis points to 26.5% for the year. That’s how the company’s non-GAAP diluted EPS growth rate outpaced revenue growth in 2023.

Looking at 2024, Paycom anticipates revenue to come in at a midpoint of $1.87 billion ($1.86 billion to $1.885 billion) – – in line with the analyst consensus per Seeking Alpha. This would be equivalent to an 11% growth rate over 2023.

The analyst consensus is for $7.76 in non-GAAP diluted EPS in 2024 according to FAST Graphs. That would be a 0.1% growth rate over 2023.

The company’s growth should pick up in 2025 and beyond. That is because as the employee-driven payroll system, Beti, gains traction with customers, retention rates should improve. Richison noted that a third-party survey found the use of Beti reduced payroll errors by over 80% and payroll processing time by 90%. For competitive reasons, Richison wouldn’t give an exact breakdown of Beti’s impact on client retention. However, he did indicate that attrition was much lower with businesses that use Beti versus those that don’t.

An eventual improvement in macroeconomic conditions will also help growth to reaccelerate. That’s why the FAST Graphs analyst consensus is for 14% growth in non-GAAP diluted EPS to $8.85 in 2025 and 19.8% growth to $10.60 in 2026.

Turning to the balance sheet, Paycom is unquestionably a financially robust business. The company had no long-term debt as of Dec. 31, 2023, compared to $294 million in cash and cash equivalents (unless otherwise sourced or hyperlinked, all details were according to Paycom’s Q4 2023 Earnings Press Release and Paycom’s Q4 2023 Earnings Call).

Free Cash Flow Can Support Generous Dividend Growth

Paycom’s quarterly dividend per share of $0.375 was initiated last May, so there’s no dividend growth record as of yet. However, I believe that will soon be changing.

The company generated $292.6 million in free cash flow during 2023. Against the $64.8 million in dividends paid during the year, that equates to a 22.2% free cash flow payout ratio. The company generated so much in free cash flow that it also covered the bulk of the $286.6 million in share repurchases that it executed in 2023 (page 62 of 103 of Paycom’s 10-K filing).

Couple that with a nice cash position and Paycom has the means to reward shareholders with huge dividend growth. My hunch is that the desire to do so is also there, but only time will tell if that’s correct.

Risks To Consider

Paycom’s underlying business is great, but there are risks with an investment in it like any other stock.

According to ADP’s February 2024 Investor Presentation, the human capital management industry is already worth $150 billion and counting. This is all while growing by 5% to 6% annually. Needless to say, there is plenty of competition to Paycom. That means the company will need to continue executing well to deliver additional growth to shareholders. If Paycom can’t meet the evolving demands of its clients, it could lose market share to competitors.

Another similar risk is employee attraction and retention. Attracting and keeping the best and brightest minds in the industry is part of the secret sauce behind Paycom’s immense success. The company anticipates that it will be doling out 8.5% of revenue in 2024 via stock-based compensation to employees per CFO Craig Boelte. This shows a sustained commitment to doing right by both clients and employees. But if Paycom ever forgets how it became a major industry player, it could end up losing key personnel to rivals. This could deal a big blow to the company’s fundamentals.

Summary: Paycom Is A Steal Right Now

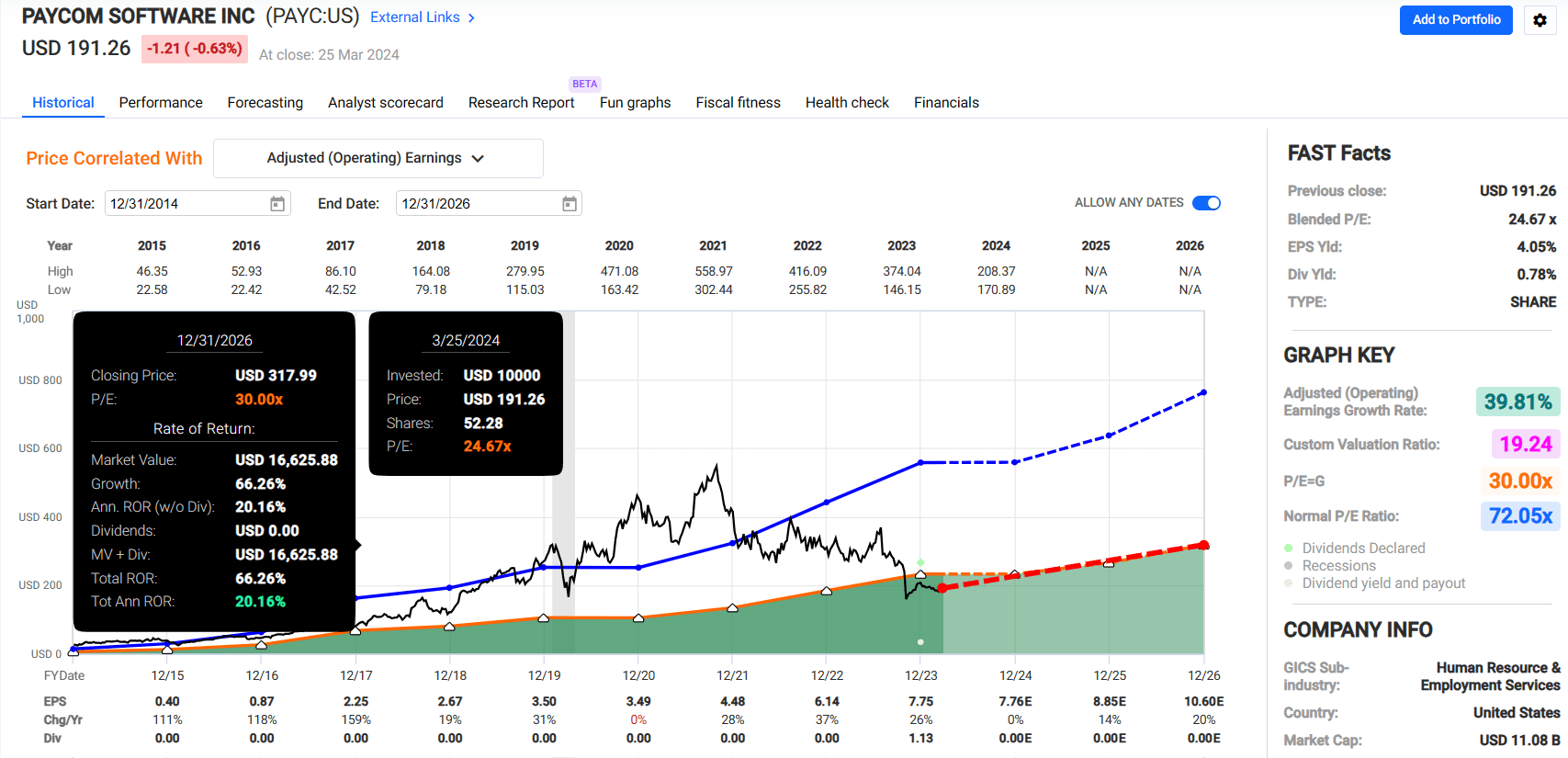

FAST Graphs, FactSet FAST Graphs, FactSet

Paycom’s 24.7 blended P/E ratio is far below its normal P/E ratio of 72.1 according to FAST Graphs. The company’s blended P/E ratio is even meaningfully cheaper than ADP’s blended P/E ratio of 27.5.

In the years to come, I think Paycom could conservatively command a valuation multiple of 30. Sure, it lacks the dividend growth record that ADP has for now. However, it has double-digit annual earnings growth potential, no long-term debt on the balance sheet, and loads of room for future dividend growth to make up for that fact.

This is why even with a blended P/E ratio of 30, Paycom could generate 20% annual total returns between now and 2026, if it can match current growth estimates. That would be much higher than the 13% annual total returns that could be expected from ADP in a similar period. This is why I’m starting coverage for Paycom with a buy.

Q2 2024 Earnings Call Transcript")