PM Images/DigitalVision via Getty Images

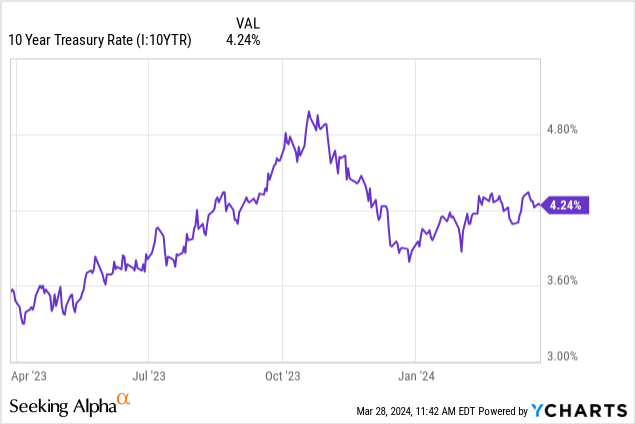

Over the past six months, income producing assets have staged a rally, bouncing from their October bottoms. Speculation around news from the Federal Reserve points towards rate cuts sooner rather than later, sparking enthusiasm. Positive economic indicators such as easing inflation have shifted sentiment around both a hard landing and a higher for longer scenario. As a result, the ten year treasury yield rapidly declined and has since rebounded slightly.

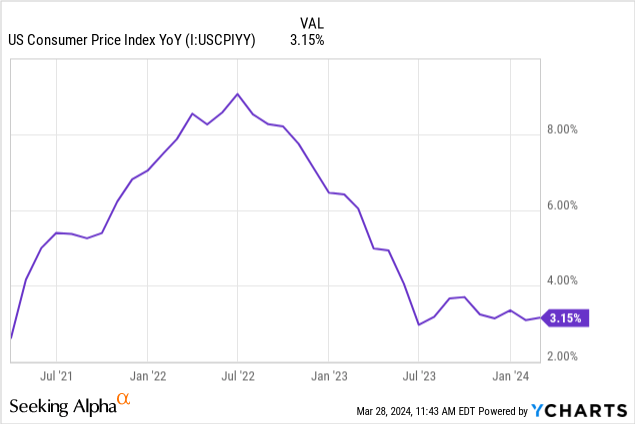

Inflation has been a primary factor in determining the direction of monetary policy. Jerome Powell has prioritized inflation over other economic markers in setting the course of interest rate policy. Recently, several markers have shown promise that inflation is slowing.

Following the March meeting, Jerome Powell made several confident remarks. As the economy continues to move towards the Federal Reserve’s long term inflation goal of 2%, Powell has been careful to try and thread the needle by keeping the economy moving, but not cutting rates too soon.

The story is really essentially the same of inflation coming down gradually to 2% on a sometimes bumpy path…we’re not going to overreact…to the two months of data. Nor are we going to ignore them.

Should the economy keep moving in the right direction, there is a chance rate cuts could begin before the end of the year. Today, we are going to dive into PIMCO’s newest closed end fund, the PIMCO Access Income Fund (NYSE:PAXS).

PIMCO is one of the largest and most esteemed fixed income managers. A core piece of PIMCO’s lineup is their closed end funds. These high yielding, complex vehicles have impressive histories of beating fixed income benchmarks, despite elevated volatility. As one of the largest fixed income managers, PIMCO is dialed into the economy, constantly polishing their crystal ball. PIMCO recently published an article with a clear view on near term rate movements.

U.S. Federal Reserve Chair Jerome Powell’s confident press conference following the March meeting coupled with revised Fed projections suggest Fed officials are determined to cut interest rates this year – most likely starting in June. Fed officials signaled that it would take a dramatic turn of events to knock them off this course. The median interest rate forecast for 2024 did not change from three 25-basis-point (BP) rate cuts by the end of 2024, despite upward revisions to the inflation forecasts.

We believe the very modest upward adjustment in the expected path of interest rates past 2024, despite a strong U.S. economy and recent stickier inflation readings, suggests that the Fed views the competing risks (recession versus persistent inflation) as reasonably balanced now. So if core PCE inflation (personal consumption expenditures, the Fed’s preferred measure) remains within the “2-point-something” zone – not far above the 2% target – when Fed officials meet in June, we expect they will cut.

Should the ball keep rolling, rate cuts could appear as soon as three months from now. As previous rate cut cycles have shown, fixed income investments of all shapes and sized stand to benefit from rates coming down. Let’s dive into PAXS and see how it stacks up against other funds from PIMCO.

Fund Overview

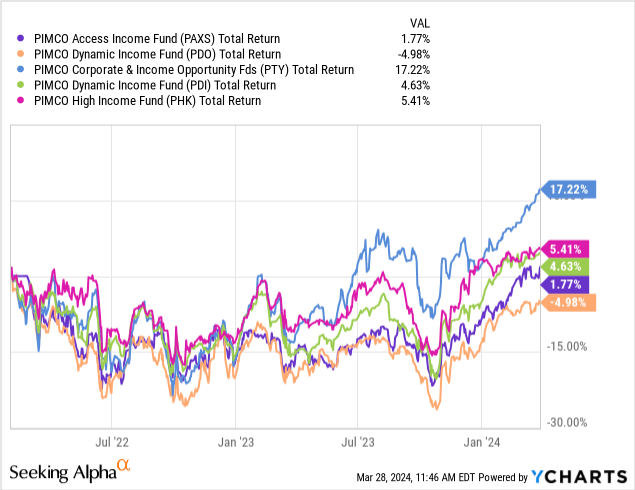

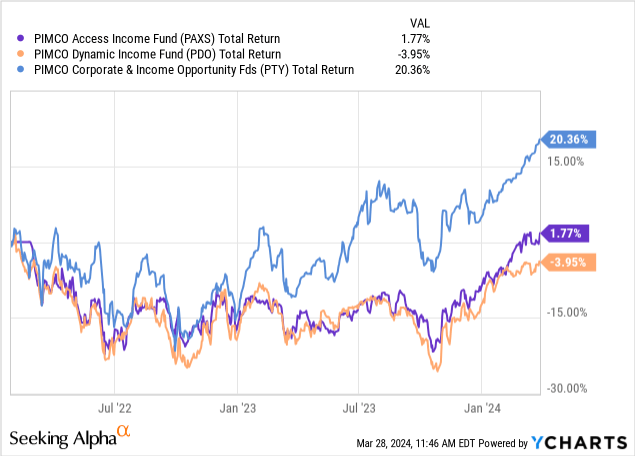

PAXS launched in 2022 and is the newest fund in the PIMCO CEF lineup. The fund has performed well against other members of the crew, outperforming the struggling PIMCO Dynamic Income Opportunities Fund (PDO) but trailing the legendary PIMCO Corporate and Income Opportunity Fund (PTY) since inception.

PAXS is also considerably smaller than other funds in the lineup with $664 million in common assets under management. As a point of reference, PAXS holds around one tenth of the assets of the PIMCO Dynamic Income Fund (PDI). Despite having similar names, we quickly see that each fund from PIMCO is unique in performance and structure. Let’s explore PAXS in greater depth and see what sets the fund apart.

In managing the fund, PIMCO will employ an active approach to allocation among multiple fixed income sectors based on, among other things, market conditions, valuation assessments, economic outlook, credit market trends and other economic factors. With PIMCO’s macroeconomic analysis as the basis for top-down investment decisions, including geographic and credit sector emphasis, PIMCO will manage the fund with a focus on seeking income generating investment ideas across fixed income sectors, including opportunities in developed and multiple emerging global credit markets. PIMCO may choose to focus on particular countries/regions, asset classes, industries and sectors to the exclusion of others at any time and from time to time based on market conditions and other factors. The relative value assessment within fixed income sectors will draw on PIMCO’s regional and sector specialist insights.

The Fund seeks to achieve its investment objectives by utilizing a dynamic asset allocation strategy among multiple sectors in the global public and private credit markets, including corporate debt, mortgage-related and other asset-backed instruments, government and sovereign debt, taxable municipal bonds and other fixed-, variable- and floating-rate income-producing securities of U.S. and foreign issuers, including emerging market issuers and real estate-related investments (“real estate investments”).The Fund may invest without limitation in investment grade debt securities and below investment grade debt securities (commonly referred to as “high yield” securities or “junk bonds”), including securities of stressed, distressed or defaulted issuers.

PIMCO provides a comprehensive overview of the fund’s strategy and operations on the main page. On the surface, we’ll see that PAXS is like other PIMCO funds in terms of targeting a diversified portfolio of debt investments. Additionally, PAXS has the right to invest in bankruptcies and other special situations where PIMCO has historically shined.

PIMCO

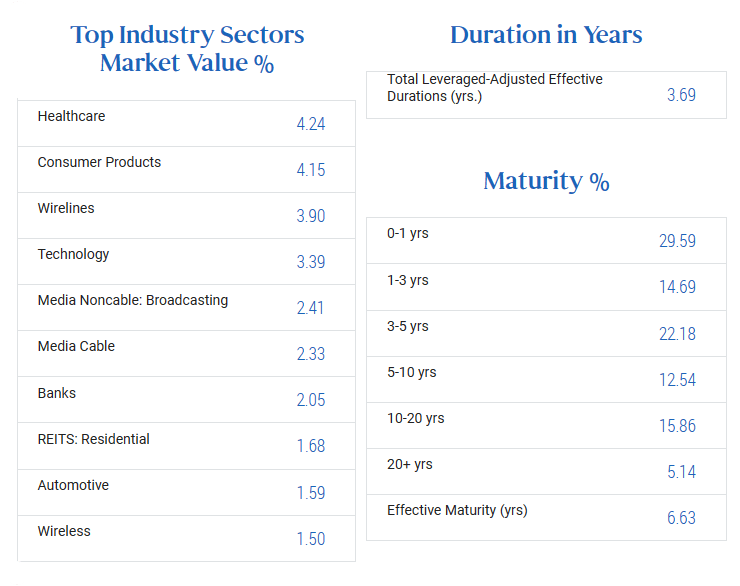

PAXS is diversified across industries with no single sector accounting for more than 5% of the portfolio. Similarly, positions are invested across maturities. Most of the fund matures within five years, but some positions extend beyond 20 years. In theory, the near term maturities give PAXS an opportunity to reinvest maturing positions at higher rates. Over 90% of the fund is invested in the United States.

We mentioned that PAXS is smaller than competing funds with only $664 million in common assets. As with other funds from PIMCO, PAXS is internally leveraged at a rate of around 40%. Accounting for the fund’s leverage, there is $1.1 billion in managed assets. PIMCO defines “managed assets” as:

Total Managed Assets include Net Assets Applicable to Common Shareholders (“Common Net Assets”) + Preferred Shares + Reverse Repurchase Agreements + Credit Default Swaps + Floating Rate Notes Issued in Tender Option Bond (“TOB”) transactions, as applicable. In TOB transactions, a fund sells a fixed rate municipal bond to a broker who places that bond in a Special Purpose Trust from which Floating Rate Notes and Inverse Floaters are issued.

Why Is PAXS Different?

A major performance differentiator for PAXS was the timing of the fund’s launch. PIMCO has been launching closed end funds over the course of decades. PTY has been trading for over 20 years, while PAXS is just over two years old. While the funds are similar in goal and composition, the timing is critical. PAXS launched when the federal funds rate was bottomed. In fact, PAXS was formed almost immediately before the Federal Reserve began the most aggressive rate hike cycle in decades.

This means PAXS faced an extraordinary set of headwinds as the fund began to ramp up. The timing was much better than PDO, which was doomed to start and suffer in a low rate world. However, this still meant that PAXS has underperformed competitors such as PTY and PDI due to the inferior securities in the portfolio. Older funds could be more selective with their investments as they made fewer investment decisions in a low rate world. At the fund level, this protected net asset value and the distribution.

The Rally

As the introduction covered, speculation around near term interest rate cuts has been a major contributor to the strong performance of fixed income over the past six months. For PAXS, this speculation provided much needed relief from the burden of rising rates since the fund’s inception.

The market is pricing in multiple near term rate cuts as we see the ten year yield begin to compress against inflation. What would happen if we were wrong? What if inflation reignites from another unforeseen geopolitical disruptor?

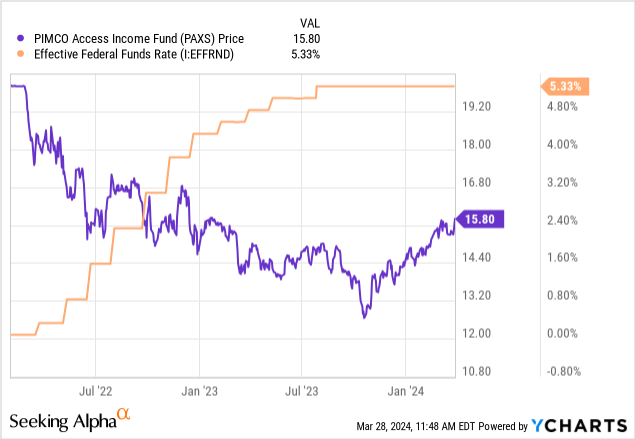

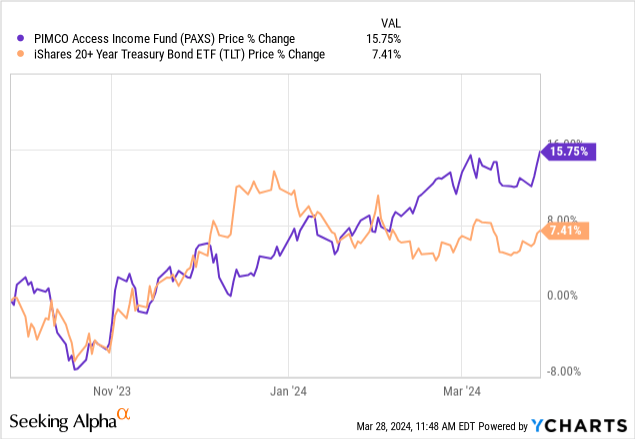

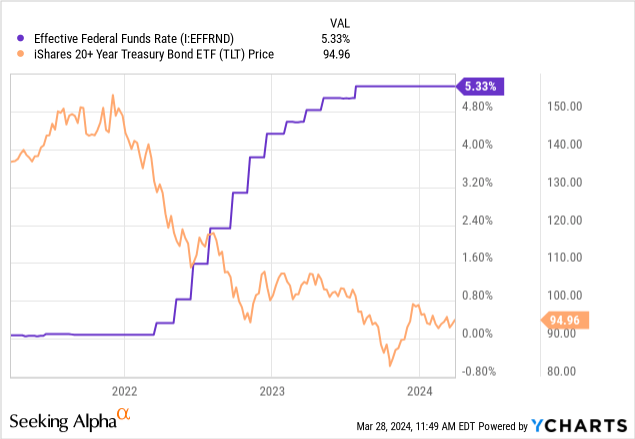

During the previous rate hike cycle, PAXS’s net asset value began to erode as rising rates hurt valuations. If the Federal Reserve begins to increase the federal funds rate once again, it could continue to negatively impact the fund. TLT provides a longer term illustration of this effect, before PAXS launched.

From a contrarian approach, a higher for longer scenario could benefit PAXS over a longer time horizon. The opportunity to reinvest maturing securities into higher coupons will provide resilience for net asset value and additional income to cover the fund’s distribution.

Risks

There are a variety of risk factors that face PAXS and all closed end funds. PAXS and other funds from PIMCO are extraordinarily complex. In fact, it’s impossible to have a complete handle on the fund’s operations at any one time due to the active management and periodic reporting requirements. This makes assessing PAXS’s risk factors difficult, if not impossible. At the end of the day, a significant portion of our investment is trust in PIMCO and their track record. This is a critical risk factor on its own.

A more surface level risk factor is the sustainability of the fund’s dividend. PAXS offers a distribution yield around 12%, meaning incoming shareholders will receive approximately 1% of their investment back in monthly income. To make this distribution sustainable, PIMCO must invest the portfolio in a manner which exceeds this leakage rate. Doing so will result in NAV appreciation. Failing to accomplish this will result in NAV falling over the long term.

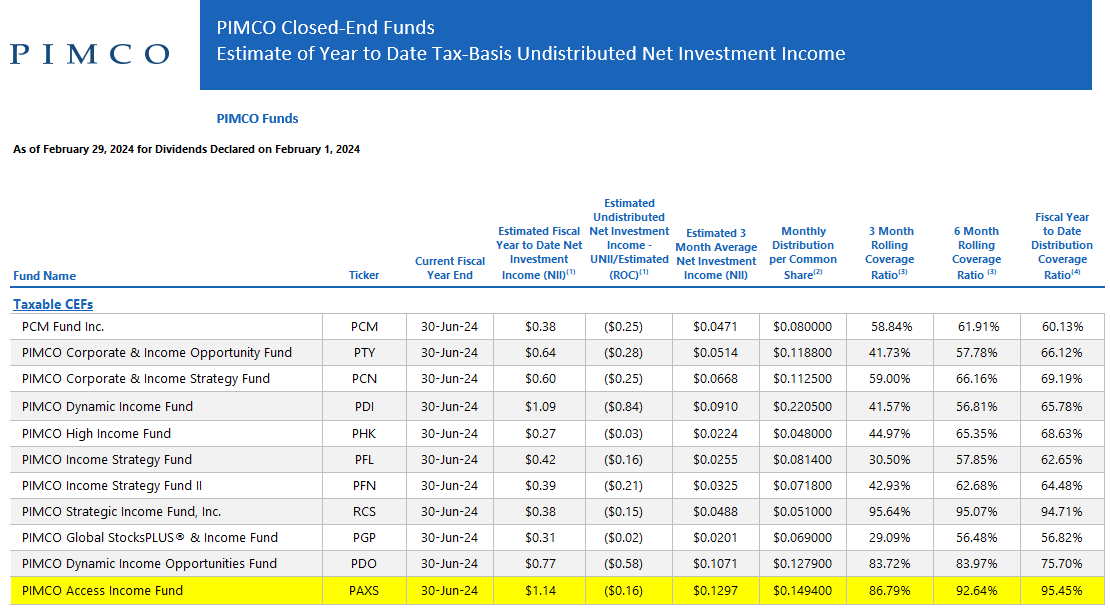

PIMCO

PIMCO publishes a monthly report outlining coverage of each fund’s distribution based on undistributed net investment income. Year to date, PAXS has the highest coverage ratio of the lineup at 95.45%. PAXS comes in second on a six month rolling basis, covering 92.64% of the distribution in UNII.

These coverage ratios should be taken with a grain of salt as there is opacity in the calculation of UNII. Despite UNII coverage being low, PIMCO has been able to sustain the distributions across the lineup except for several rare cuts.

Conclusion

PAXS continues to establish itself amidst a challenging backdrop. On one hand, the fund has been a strong performer against fixed income benchmarks, but it still trails other funds from the lineup. Near term rate cuts will be a critical piece of the fund’s near term success. However, PAXS may also thrive under a higher for longer scenario. For the time being, there may still be better options from the lineup. We know that past performance is not indicative of future returns, but PTY and PDI continue to outperform meaningfully.

Q2 2024 Earnings Call Transcript")