Ryan Fletcher

With final stage in the breakup of General Electric finalized earlier this month as GE Aerospace (GE) and the energy business GE Vernova (GEV) started to trade separately, the Wall Street Journal ran a nice photographic retrospective of General Electric. The once towering conglomerate is no longer, but its legacy will undoubtedly persist for at least another generation. Though I don’t have any direct financial interest personally in any of that legacy at the moment, I’ve encountered it in my little rural corner of the world where I’ve encountered a co-worker who used to work for GE whose retirements were seemingly ruined when the company was tottering, and I even have a neighbor who works for the new energy division. Although I do not have a direct interest in GE per se, I do follow it with interest, as its LEAP jet engines are a major driver of the fortunes of a company I am invested in.

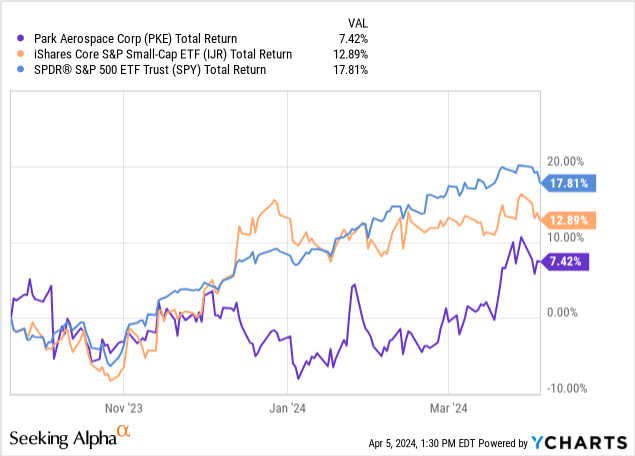

Park Aerospace (NYSE:PKE) is a fairly small American company sitting in the middle of the supply chain for some big programs, especially for the engines that carry the Airbus (OTCPK:EADSY) A320 family of jets around the world, but rounded out with supplying to defense contracts and business aircraft business as well. I last updated my view on Park Aerospace in September 2023, rating it a buy at that time. Since then, shares have been mostly range-bound between $14 and $16, though intermittently pushing past the $16 level recently. An investment in September would have resulted in a fairly flat total return and lagging other small caps broadly as well as the S&P 500 index, anyone buying at the $14 level and holding might be relatively pleased today.

Although the shares have little to show in terms of value creation, I continue to like the long-term trajectory of the business and at the current valuation, I still consider them a solid long investment.

Financial Review

The company operates on a fiscal year that runs from March to February, so fiscal 2024 full-year results are not yet available, but I expect to see them released in the first half of May. Third-quarter results released in January are for the period ended November 26, 2023.

For the quarter, sales were $11.6 million, with a gross margin of 27%, versus $13.9 million in sales in the prior year’s third quarter, with gross margins then of 32%, obviously not trends one wants to see off the bat. The main reasons, as explained by management, were a combination of the sales mix for the quarter, compounded by $0.56 million in missed shipments due to international freight backlogs on top of higher shipping rates for the orders that did go out. The well-known delays from avoidance of the Suez Canal due to armed conflict in the region, and low-water levels for the Panama Canal are taking their natural toll, and now we can add the tragedy of the Baltimore bridge accident to the list of things that will not help to relieve pressure on shipping options, at least in the short-term. For Park Aerospace, the compressed margins and lower sales delivered EPS of $0.06 for the quarter, and a total of $0.24 for the year-to-date, definitely trailing the previous year’s results of $0.11 (Q3 of fiscal 2023) and $0.29 (cumulative through Q3 fiscal 2023) respectively.

The YTD earnings convert into a cash loss from operations of $0.89 million, mostly from working capital changes that were detrimental to the tune of $7.5 million. Overall, the balance sheet remains in fair shape, with Park Aerospace being debt-free for many years, though the cash and marketable securities have been coming down to return cash to shareholders. There was a special $1.00 dividend paid in March of 2023 at the start of the fiscal year, along with implementing a raise to the regular quarterly dividend, from $0.10 to $0.125, as well as a share repurchase agreement authorizing the purchase of up to 1.5 million shares. Only a small sliver of that authorization has been used, with the company reporting the retiring of 221 thousand shares at an average price of $13.09.

Cash used for dividends then YTD, including the special, was $28.1 million, and the shares repurchased would be around $2.9 million, for a total use of cash returned to shareholders of about $31.0 million, which correlates pretty much to the net sale of marketable securities of $32.3 million. This has brought the combined total of cash and marketable securities down to $74 million. There is still a tax installment payment due of $9.3 million, but no debt, so net cash at the end of Q3 is essentially ~$64.7 million after backing out the tax payment.

Opportunities, Capital Allocation, and Valuation

As a supplier dependent on the volume expectations of other manufacturers, Park Aerospace is somewhat at the mercy of its largest program, especially the GE Aerospace LEAP jet engine program for Airbus. Fortunately, that program is massive and growing, especially as the share of engines done by the GE program (operated as the joint venture Safran (OTCPK:SAFRY)) is taking market share from the Pratt & Whitney (RTX) option, due at least in part to the well publicized technical problem on the Pratt engines that is grounding planes for repairs. The Safran LEAP-1A engines now have essentially two-thirds of the Airbus A320 family market share, up from 60%. With Airbus having a staggering backlog of deliveries, it has long been pushing its suppliers to ramp up production to strive for 75 deliveries per month, which translates to ~1,200 units per year for Park Aerospace based on having 65% of the market, for years to come.

While cash is now flowing back to shareholders, there are still some growth opportunities out there aligned with Park’s ability to fund them without taking on debt. Management has previously floated possibilities that failed to materialize, however on the earnings call in January, CEO Brian Shore spoke to one such opportunity with a higher level of confidence. To quote him directly, he shared (edited for length and clarity):

[A] major new manufacturing project initiated for Park [was] requested by a highly motivated long-term large customer. We believe the project has a high degree of likelihood to proceed. Why is that? Because there’s a motivated customer that wants it to proceed. . . But just to give you a perspective, in order to do this, we need to build a new or purchase a new factory for the project. . . probably closer to 50,000 square feet. Capital estimated $6 million to $10 million. . . Now we’re looking seriously at automation to reduce the size of the workforce, but that would increase the capital spending automation. [The] preliminary estimate of revenues for the project, $20 million to $30 million per year range. . . We’re not talking speculation about the revenue opportunity. There’s lots and lots and lots of detail behind that. And it’s probably more than 10 years, probably life of program. Again, whatever, 20 years, 25 years. So it’s a big thing for Park. High priority, potentially very important project for Park and our customer.

What is different here, in my opinion, than previous projects that management has talked up as possibilities, is that an existing client came to Park and asked for this, so the demand for it is real and not hypothetical. With around $65 million in cash (net after the tax payment), if this new project were to move forward and require $15 million (50% more than the higher estimate of $10 million), that still leaves ~$50 million in cash available as cushion while operating cash flows might be lumpy.

As a reminder, the regular dividend will work out to ~$10.2 million per year at the current share count. Not being able to fund the normal dividend from operating cash is less than ideal, as was the case in Q3. However, with the continued demand growth from Airbus A320 program and other existing programs, I expect to see revenue and margin improvements in the coming quarters improve as Park’s updated pricing terms come into greater effect, and in turn, that should support earnings and operating cash flow. In other words, I anticipate operating cash flow to fully cover the dividend over time.

So how does all this filter down to assessing the valuation? In my view, Park Aerospace has held a generally attractive profile for investors for a while, although it has taken longer to deliver value than I had hoped. But that profile, which blends a strong growth outlook from the existing mix of commercial and defense programs the company is already supplying with being debt-free points to a well-managed business, even if at times tends to be somewhat cautious and conservative. With a fairly recent turn towards more directly returning cash to shareholders, such a business strikes me as highly investable at the right valuation, and here Park Aerospace continues to be appealing.

Specifically, for fiscal 2024, adjusted EBITDA is expected to be fairly in line with the prior year, around $11.8 million (compared to $11.5 million for fiscal ’23), but then the incremental growth will start to kick into high gear.

First of all, the GE engine program and select defense programs are expected to pick up significantly, expanding the top line by ~$50 million or more just by themselves. To be clear, this does not require winning new projects, just based on the growth trends from their customers on existing programs for Park. This would essentially double the sales relative to the baseline fiscal 2023, and lead to an adjusted EBITDA of about $36 million.

That is clearly pretty aggressive forecasting, and perhaps too generous in its assumptions, but even if it is only half-right and adjusted EBITDA goes from its current ~$11 million to ~$18 million (half of the $36 million shared in the presentation), that is still more than 60% EBITDA growth. I’ll use that $18 million adjusted EBITDA figure on a forward basis to keep myself more conservative than the forecast. For Park Aerospace’s enterprise value, assuming the cash balance is adjusted down to $50 million (after the tax payment and assuming $15 million for a new project), the EV would come out to around $275 million. On these assumptions, the forward EV / adj EBITDA multiple is ~15.25x, in line relatively for the overall industrial sector multiple, which sits around 13.3x.

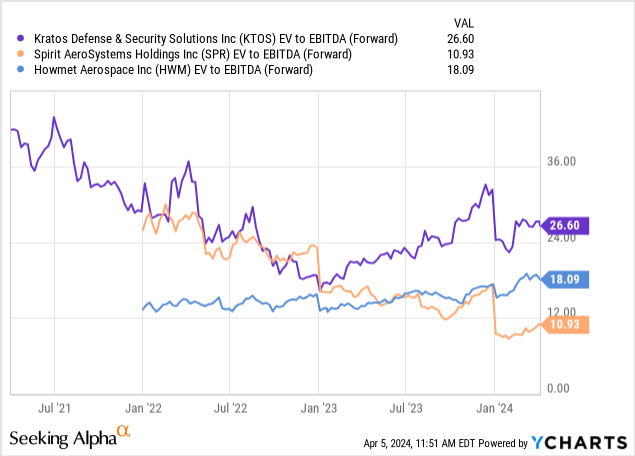

Compared to some of its customers and peers, this looks to be fairly valued. For example, Spirit AeroSystems (SPR) is 11x, Howmet Aerospace (HWM) is 18x, and Kratos Defense & Security Solutions (KTOS) has 27x.

What starts to get an investor’s attention is if the EBITDA actually creeps higher towards the forecast.

Park Aerospace – Enterprise Value / Adj EBITA (FWD) (Author’s spreadsheet)

Bear in mind as well that this is assuming a higher EV due to using some cash to build out a factory for the new project, while not assuming any benefit to EBITDA from that same project. Should the EBITDA start approaching the $20 million – $25 million range, which is still well below management’s forecasts, then I would classify Park Aerospace as undervalued.

Risks

Multiple risks could sink this thesis, both those within and outside of Park’s ability to control. For starters, if the production pace that Airbus wants to hit cannot be reached and sustained, then Park’s volumes and revenue growth projections will be off the mark. This outcome is not necessarily farfetched, as it could be impacted by the ability of other suppliers in the LEAP engine to keep pace, as well as the delays in international freight mentioned earlier. Alternatively, if Airbus were to run into any scenario remotely like Boeing’s recent trail of safety problems, resulting in its A320 family of aircraft getting grounded for a time, it would trickle down and negatively impact Park. Additionally, though I consider it a low-risk, political delays in approving defense budgets both in the United States and other Western governments could be bad for Park’s defense industry programs.

The risk that is more internal would be the pursuit of the new production opportunity outlined by management. This project is expected to require a fairly substantial capital investment, and should Park make the investment but fail to hit expected returns, it could be detrimental to value creation for shareholders.

Concluding Thoughts

I started building a small position in Park Aerospace in January of 2020 when shares were trading around the same $16 level as they are today, and that initial tranche is the personal peak valuation I ever went for, buying here and there over the last 4 years at prices ranging from just under $11 up to just under $15. With reinvested dividends, my position has gained ~44%, and I find I do have to watch my bias for anchoring.

What helps free me up from that distortion is the genuine runway for growth that is stretching out in front of Park Aerospace, simply as a result of industry conditions in general, plus the benefit of being paired to the Airbus A320 platform and avoiding the unfortunate problems at rival Boeing (BA). It has certainly not happened overnight, nor I do not expect rapid gains from here for shareholders, but over the longer term, I do anticipate more good things for patient Park Aerospace over the next 18 to 36 months as the actual growth scenario starts to bear fruit.

Q2 2024 Earnings Call Transcript")