PATRICK T. FALLON/AFP via Getty Images![]()

As a value investor, growth investing can be a scary concept. Paying a high price, a price that is higher than justified based on current fundamentals, with the hope that future growth will not only make up that gap but also allow you to achieve a robust return does not exactly come across as sound investment advice. Having said that, when growth investing is done right, the results can be phenomenal. For much of last year, I was rather bearish on one of the most popular growth stocks of the last few years. That is none other than Palantir Technologies (NYSE:PLTR). Rapid growth, combined with hype centered around AI, ended up sending shares of the business up rather meaningfully.

After re-evaluating the picture, looking at the market opportunity, and factoring in what the continued expansion of the company, even under fairly conservative assumptions, would mean for the business, I ended up biting the bullet and upgrading the firm from a ‘sell’ to a ‘hold’ in November of last year. Since then, the stock has continued to outperform the market. Shares are up 21.3% since that article was published. That’s almost double the 11.3% seen by the S&P 500 over the same window of time.

Given this sizable move higher over such a short window, you might expect that I have changed my attitude again and that a downgrade would be in store. But I’m not there yet. It is true that shares are looking very expensive. And I also believe that much of the hype regarding AI will not have a massive, rapid impact on firms like this in the near term. But according to recent guidance, the picture does not look bad at all. And when you factor in how healthy the company is and what the end result will likely mean for its cash on hand, I think that a ‘hold’ is still appropriate. But of course, everything has its limits. And if shares rise much more than what we have seen already, a more bearish assessment might ultimately be needed.

A great way to start off a year

One of the great things about many companies, including Palantir Technologies, is the fact that management provides some sort of insight into what the current fiscal year might end up looking like. The latest such example involving Palantir Technologies was announced on February 5th when the company put out its financial results covering the final quarter of the 2023 fiscal year. Given how much time has passed, I don’t think there is much value in going over those results and how the business fared compared to expectations. I do think it’s noteworthy that the company achieved its 5th consecutive quarter of profitability. But outside of that, the most important takeaway is what management is forecasting when it comes to 2024.

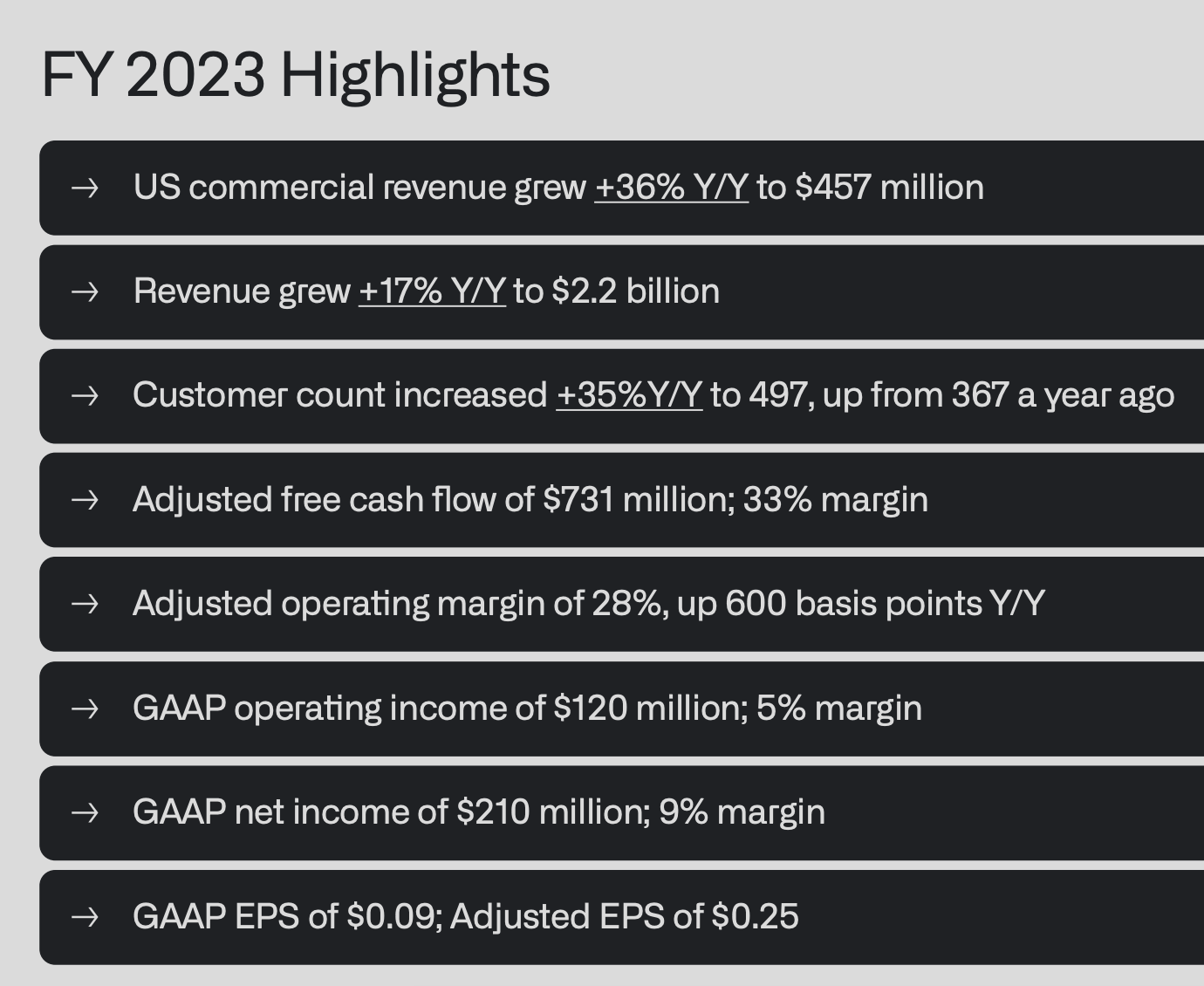

In 2023, Palantir Technologies generated revenue of $2.23 billion. That was about 17% higher than what the business achieved one year earlier. While this is fantastic growth for a company of its size, that kind of upside paled in comparison to what the business achieved in prior years. From 2021 to 2022, for instance, the company saw revenue climb 23.6% year over year. And from 2020 to 2021, growth was an astounding 41.1%. Clearly, there is a deceleration when it comes to growth. Or I guess it would be more appropriate to say that there was.

Palantir Technologies

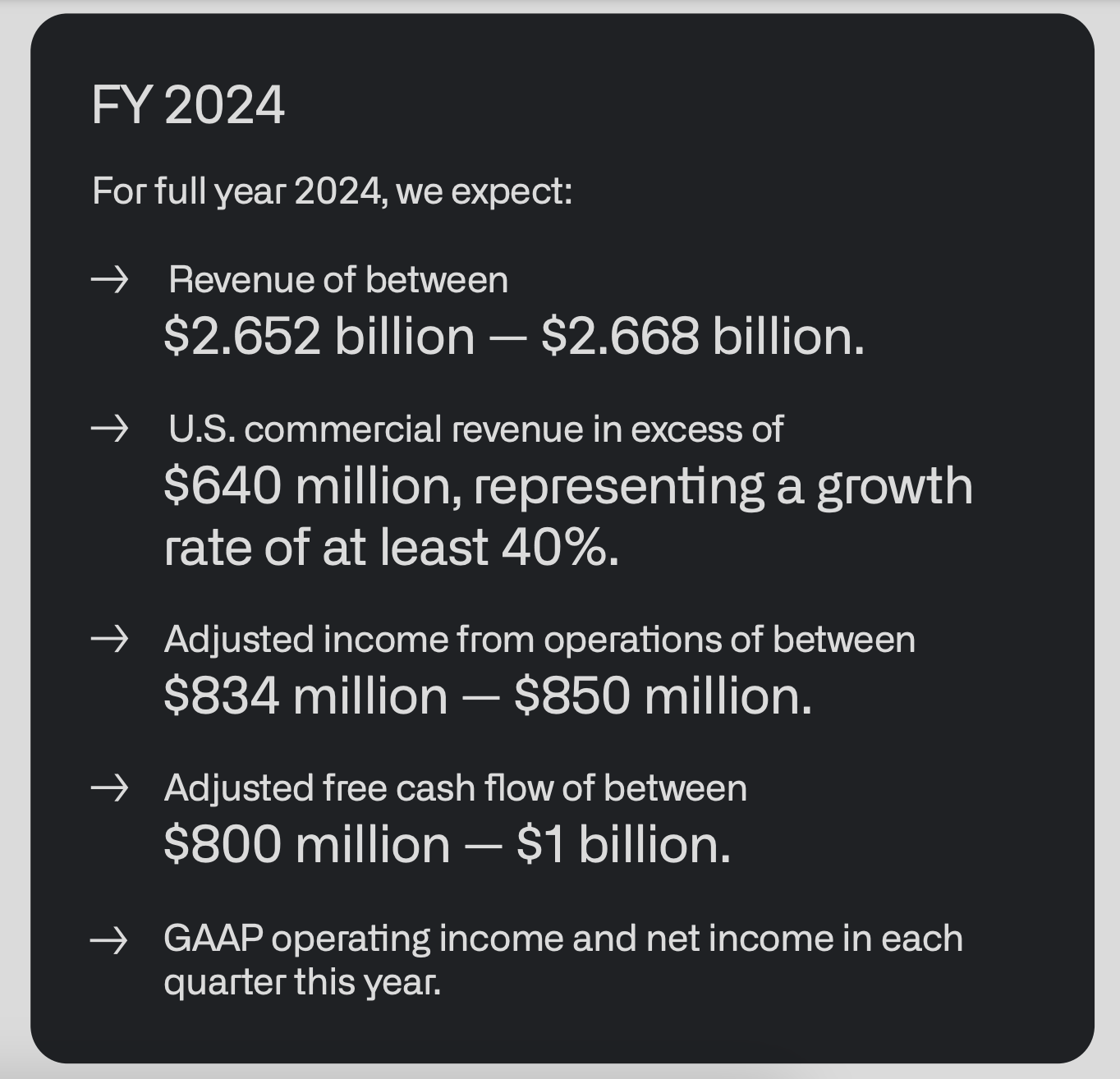

You see, according to management, revenue this year should be between $2.65 billion and $2.67 billion. At the midpoint, we are looking at about $2.66 billion. That’s 19.6% above what the company achieved last year. No, it’s not a rapid improvement. But it is an improvement all the same.

Originally, Palantir Technologies started off as a company that catered to the US government. It still generates a large portion of its revenue from those types of activities. Over the past couple of years now, however, the firm has been putting a great deal of emphasis on catering to the commercial space. These days, that’s where much of its growth is coming from. In 2023, government revenue grew by only 14%. But commercial revenue grew by 20%. US commercial revenue was particularly strong, shooting up 36% year over year. Much of this was weighted in the final quarter of the year, with revenue skyrocketing 70% year over year as the US commercial customer count jumped by 55%.

Palantir Technologies

If you’re reading this article now, you have probably read multiple times the different ways in which AI will prove bullish for the business and, in turn, its shareholders. It’s highly likely that much of the recent commercial growth has been because of the rise of AI. Data is mixed on the matter. But according to one source, 92% of companies in the Fortune 500 are currently using AI in some parts of their operations. However, the case has been made that AI is not as omnipresent as many think it is. One article, citing a study conducted by the Census Bureau that conducted a survey in November of last year, indicated that while around half of S&P 500 earnings calls late last year featured discussions of AI, only about 4.4% of businesses nationally are using it in order to produce goods or services.

This data can be interpreted in both positive and negative ways. On the positive side, it could mean that there is significantly more revenue potential that could come Palantir Technologies’ way as more companies become wedded to the use of AI. On the other hand, there’s also the possibility that, like other technological improvements that led to more hype than substance (like blockchain), AI could just be the exciting new toy that companies are playing around with and promoting in the hopes of boosting their share prices.

Of course, nobody knows at this point in time which case will prove to be accurate. However, it’s clear that management at Palantir Technologies has a reason to be optimistic about this year at a minimum. And it’s worth noting that the projections made by management are not just wishful thinking. The firm actually has companies putting their money where their mouths are. Last year, the firm had its own AIP boot camps, which are hands-on keyboard sessions that allow new and existing customers to build whatever it is they are building alongside the company’s engineers. No fewer than 465 such organizations participated in those boot camps since their launch. In terms of contracts for business, the firm landed 103 deals that were valued at $1 million or more just in the final quarter of 2023. 37 of those were worth at least $5 million, while 21 of them were worth at least $10 million.

Author – SEC EDGAR Data

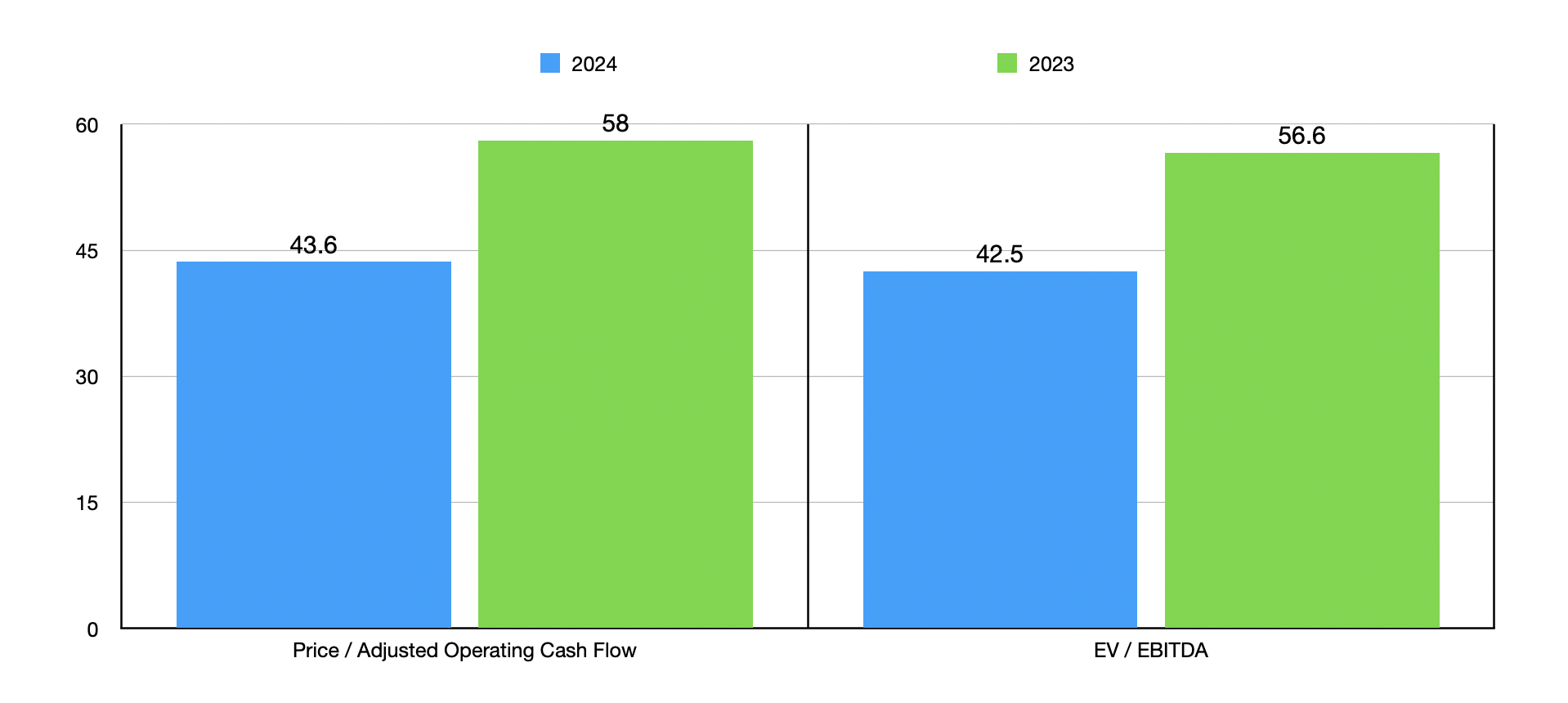

This growth in revenue should result in adjusted operating income of between $834 million and $850 million for the year. If we assume that other profitability metrics, such as operating cash flow and EBITDA, should rise by the same rate, then we would expect readings of $947.6 million and $886.3 million, respectively, for 2024. In the chart above, you can see how shares are priced on a forward basis and how they are priced relative to the data from 2023. On an absolute basis, these are very high multiples. But again, the idea behind growth investing is to capture something that can achieve further upside from here.

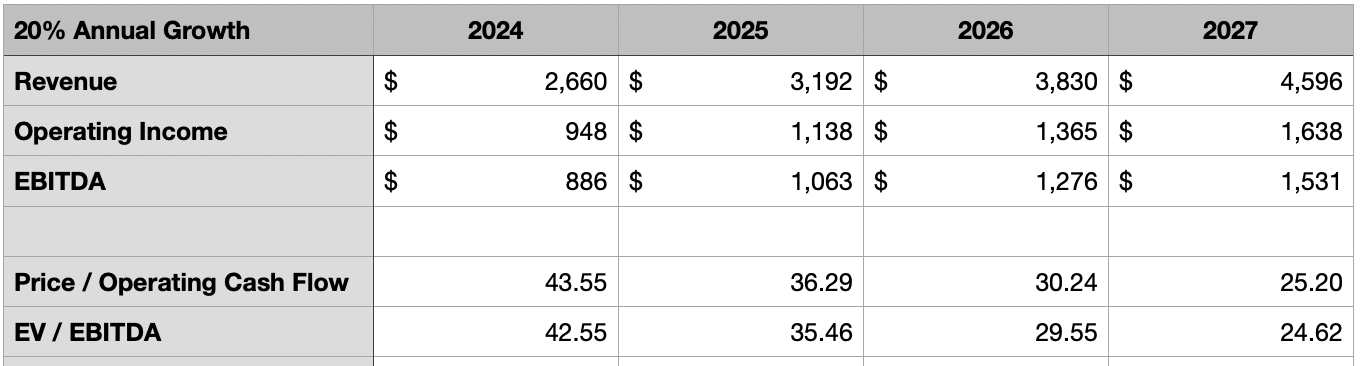

If we take management’s word for it for the 2024 fiscal year, we can project out from that point with the future might look like. If AI truly is some remarkable opportunity that’s worthy of rapid growth, then it shouldn’t be difficult for the company to continue growing at a rate of about 20% per annum. I say this because, according to one source at least, it’s believed that the AI market will grow at a 21.6% annualized rate from 2023 through 2030. And if Palantir Technologies truly is going to be one of the great beneficiaries of this paradigm shift, you would expect its growth to perhaps exceed that rate.

Author – SEC EDGAR Data

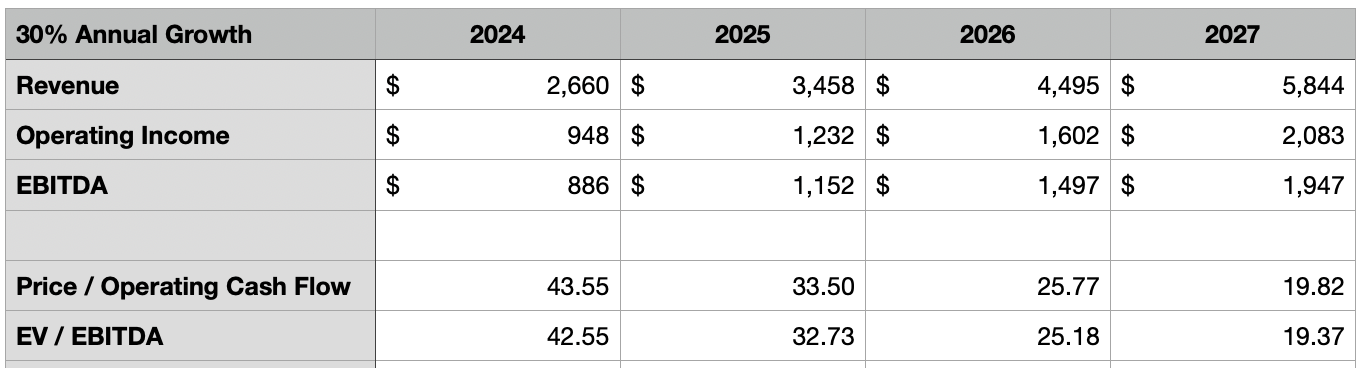

Regardless, in the table above, you can see what revenue, operating cash flow, and EBITDA would look like for the company in each year from 2024 through 2027. You can also see how shares are priced on a price to operating cash flow basis and on an EV to EBITDA basis. If growth does come in greater than that, such as at a rate of 30% per annum, you can see the results below. Naturally, the stock does get cheaper as time goes on. But at no point would I call shares cheap? If anything, they are still quite pricey.

Author – SEC EDGAR Data

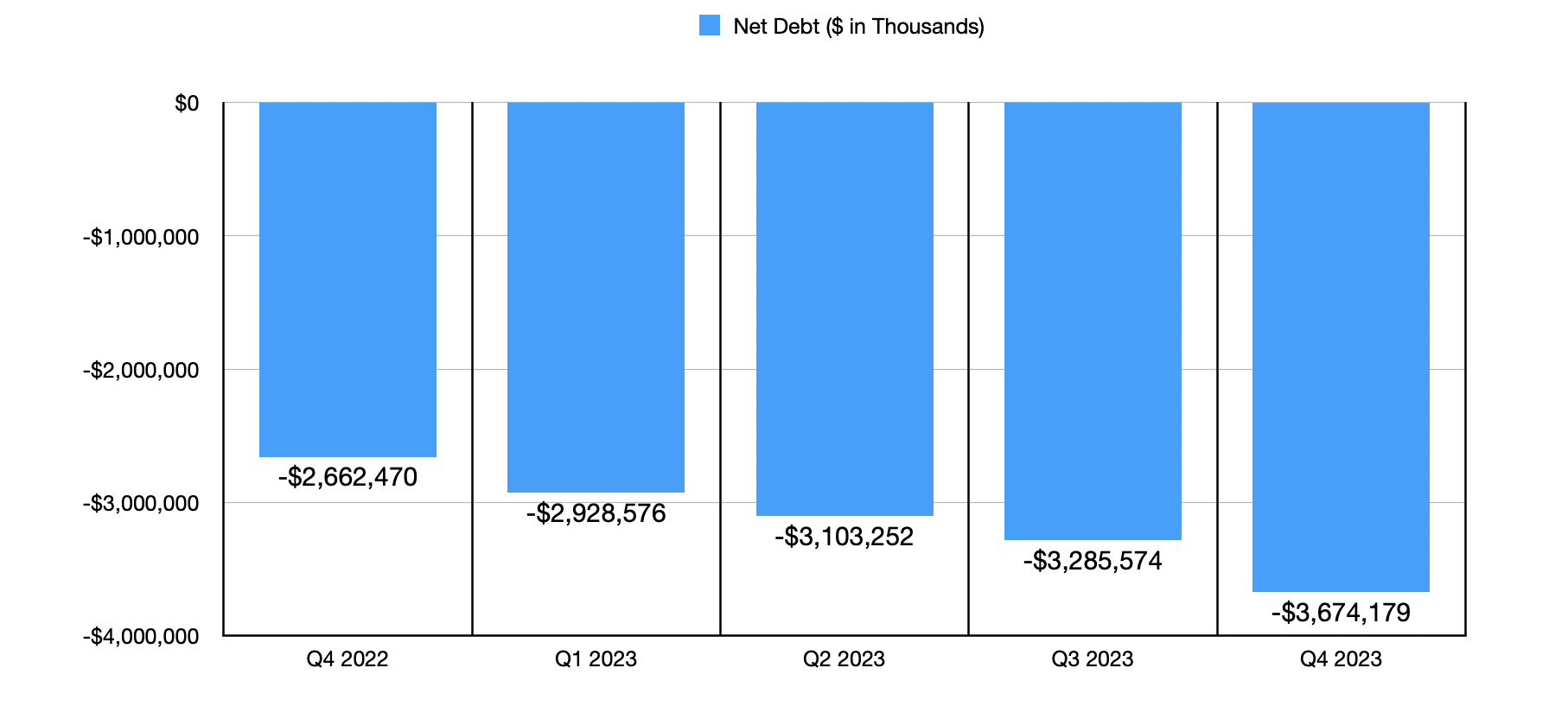

Another topic that should be discussed here involves the firm’s balance sheet. Many companies, including those that are growing rapidly, have large amounts of debt on their books. Debt is used to fuel growth. However, Palantir Technologies is an exception to that. The company has no debt at this time, and it enjoys $3.67 billion of cash and cash equivalents on its books. Furthermore, this is substantially higher than the $2.63 billion in cash that the firm had at the end of 2022. With the company growing while generating positive cash flows, it’s likely that cash balances will continue to expand unless management does something with that capital. But the important thing is that this provides safety, and it provides flexibility for the firm to grow more rapidly or to deploy the capital in interesting ways. The other advantage that shareholders have is that the high trading price of units means that management can always issue additional stock in order to bolster cash further. That’s the beautiful thing about growth prospects. Issuing stock is like issuing overly inflated currency. But it gives the company in question more buying power that it can use for whatever it wants.

Author – SEC EDGAR Data

Takeaway

At this point in time, I’m remaining open-minded when it comes to Palantir Technologies. It’s clear that the company is growing at a rapid pace, and profitability has become a big selling point for investors. I would not go so far as to say that I have become bullish on the firm. Although operationally I am, there is no denying that the stock is very pricey. In the event that management can achieve rapid growth for the next few years, the end result might be positive for shareholders. But I also think that, given how pricey units are, further upside without any corresponding revision in profitability could risk a justifiable downgrade.

Q2 2024 Earnings Call Transcript")