Sergio Mendoza Hochmann/Moment via Getty Images

Performance Assessment

In my last coverage of Palantir (NYSE:PLTR), I had initially rated the stock a ‘Neutral/Hold’. On 25 January 2024 in a pinned comment, I revised my rating to a ‘Sell’ before earnings as I had doubts on the quality of backlog growth as measured by remaining performance obligations (RPO). This view has not played out as Q4 FY23 results went the exact opposite of what I was expecting. As a result, the stock has surged +48.88% since my ‘Sell’ view, compared to the S&P500’s (SPY) (SPX) +2.26% over the same period, implying a negative alpha of 46.62%.

Thesis

I believe my ‘Sell’ rating update was too early. And although the market proved my thesis wrong, I am retaining my ‘Sell’ view as I believe the operating momentum – as strong as it may be – is ticking below the lofty expectations demanded of the stock given current valuations. Here’s how I’m viewing the key drivers of Palantir:

- Deal flow validation of AIP and bootcamps is compelling

- Palantir is de-risking revenues and steadily upgrading margins

- Management’s guidance is falling short of expectations

- Valuations are near historical peak levels

Deal flow validation of AIP and bootcamps is compelling

Palantir talked about having bootcamps with commercial enterprises showcasing their artificial intelligence platform (AIP) in Q3 FY23. The commentary was optimistic from management, however, I noticed that despite the bullish talk, Palantir’s backlog of work as measured by remaining performance obligations were not seeing any material tick up. This led me to believe that there was still some top-line risk as RPOs are a leading indicator of future revenues.

However, this has dramatically changed in Q4 FY23. The numbers match the bullish narratives:

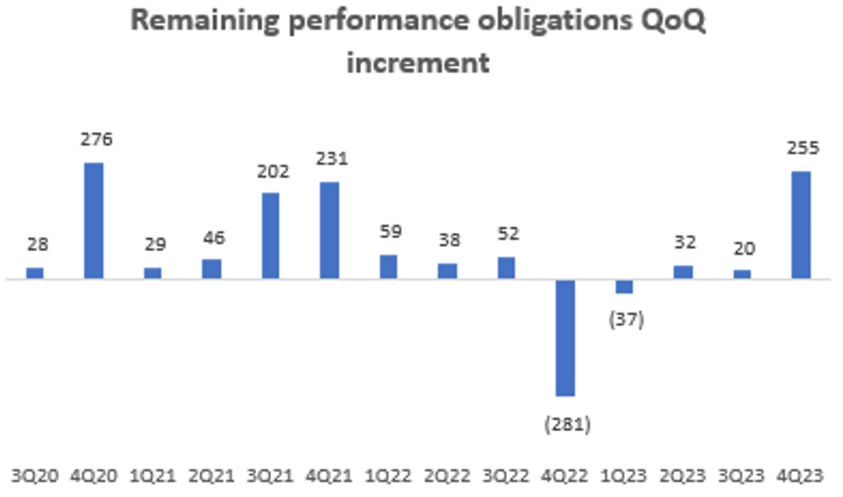

Remaining Performance Obligations QoQ Increment (USD mn) (Company Filings, Hunting Alpha Analysis)

Q4 FY23 saw a massive $255 million QoQ tick up in RPOs, reversing the cumulative fall over the 4 quarters prior. Importantly, a good chunk (67%) of this increase is attributed to longer-dated RPOs recognized over more than a 12-month period:

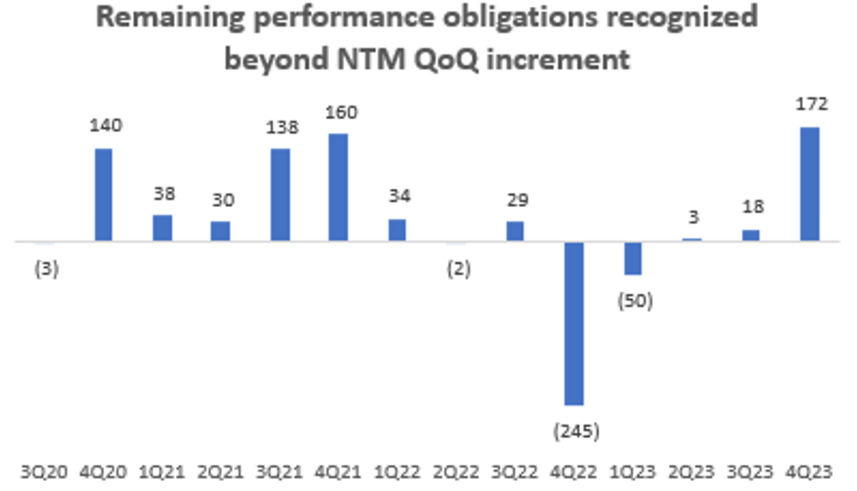

Remaining performance obligations recognized beyond NTM QoQ Increment (USD mn) (Company Filings, Hunting Alpha Analysis)

This tells me that commercial enterprises are committing to longer-term projects; a good sign of future revenue stability.

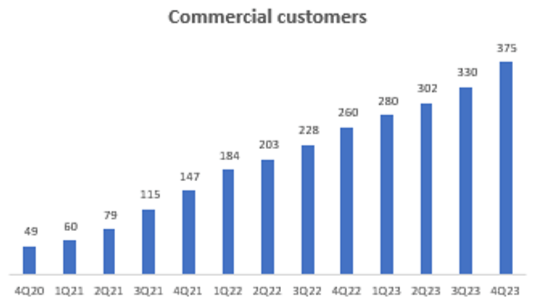

In Q4 FY23, much of the increased traction came from new commercial customers, which saw the largest QoQ increase of 45 customers in the company’s publicly-listed history:

Commercial Customers Count (Company Filings, Hunting Alpha Analysis)

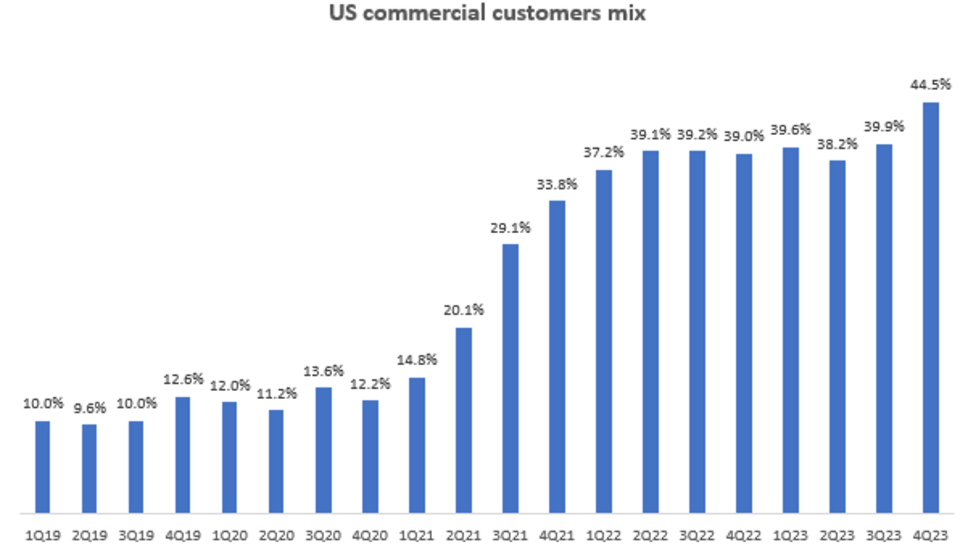

Commercial customer counts make up 75.5% of the overall customers mix (between commercial and government customers). Digging into this a bit deeper, we see that the US commercial enterprises are leading most of the increased traction here as the mix of US commercial customers jumped from 39.9% to 44.5%:

US Commercial Customers Mix (Company Filings, Hunting Alpha Analysis)

These numbers align with a key narrative shift from the company, revealing new insights about Palantir’s growth path ahead. In the past, Palantir’s management had often said their biggest competition is enterprises’ own internal IT departments. However, now they say “that’s certainly not the case anymore”:

You go to these meetings and they’ll often be the IT person telling a CEO, like, “Look, we have no choice. We need to install this quickly.” And so there’s a cultural shift in the U.S. I don’t think outside the U.S. it’s the case. But inside the U.S., people and IT are responsible for business value.

– CEO Alexander Karp in the Q4 FY23 earnings call, Hunting Alpha’s bolded highlight

What’s happening is these bootcamps are showing enterprises in a short amount of time (10 hours) that Palantir can build useful AI to aid in business decision making that their own internal companies and other IT service vendors cannot. Hence, the new insight I glean from this is that competitive intensity is actually decreasing for Palantir.

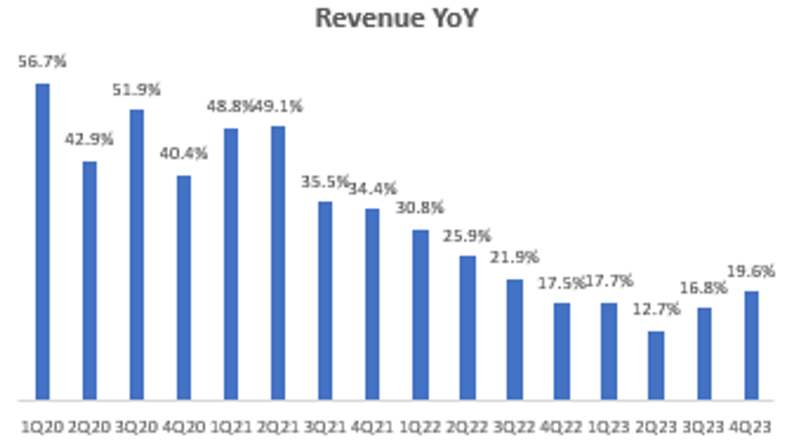

Revenue YoY (Company Filings, Hunting Alpha Analysis)

Overall, I expect these deal signings and onboarding of new customers to materialize in higher revenue growth. The company’s FY24 guidance of $2.66 billion at the midpoint of the range implies 20% growth YoY.

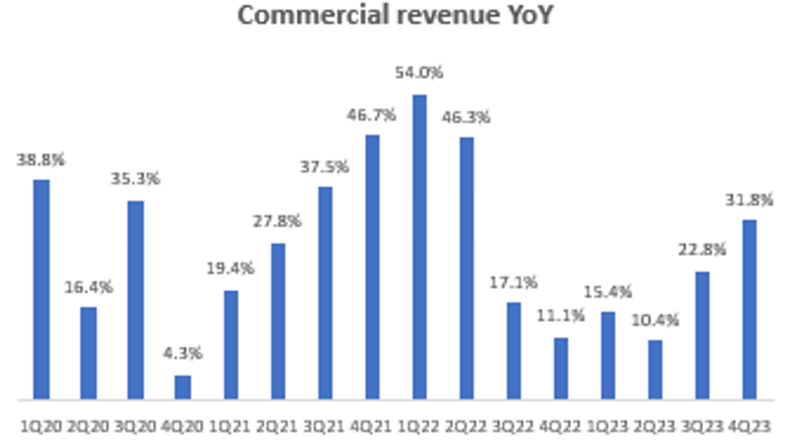

Most of this growth is expected to come from the US Commercial Segment, which currently makes up 21.5% of overall revenues. In FY24, US Commercial revenues are expected to be more than $640 million, implying an impressive acceleration of an already strong growth track to at least 40% YoY:

Commercial Revenue YoY (Company Filings, Hunting Alpha Analysis)

Palantir is de-risking revenues and steadily upgrading margins

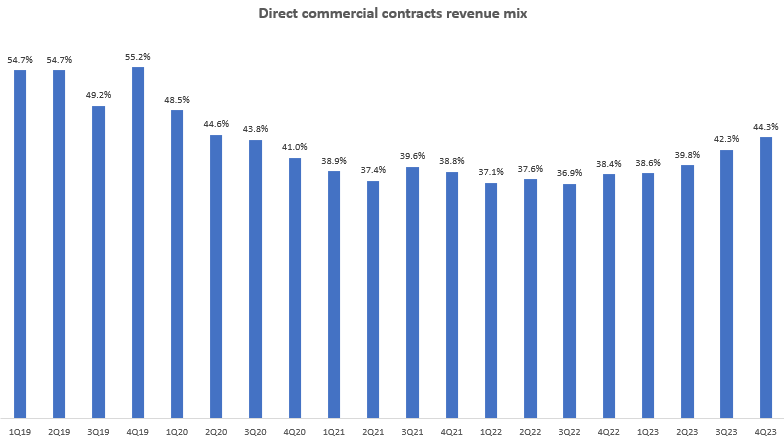

As Palantir benefits from broader product adoption, it also de-risks its revenue stream. I believe Direct Commercial contracts are the best source of business for Palantir since selling to other enterprises may lead to more favorable pricing and working capital terms (something that may not work to Palantir’s favor in government contracts). I anticipate this mix to climb up back toward 50% and higher in future:

Direct Commercial Contracts Revenue Mix (Company Filings, Hunting Alpha Analysis)

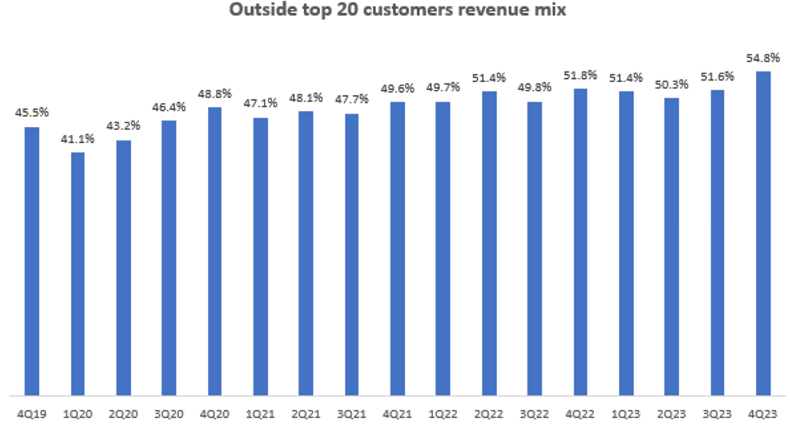

Another benefit is that Palantir’s historically high customer concentration is expected to reduce as the company signs on a more diverse set of enterprise customers. I believe a 220bps QoQ jump in the concentration of outside top 20 tail-end customers from 51.6% to 54.8% is an initial sign of further revenue concentration de-risking ahead:

Outside Top 20 Customers Mix (Company Filings, Hunting Alpha Analysis)

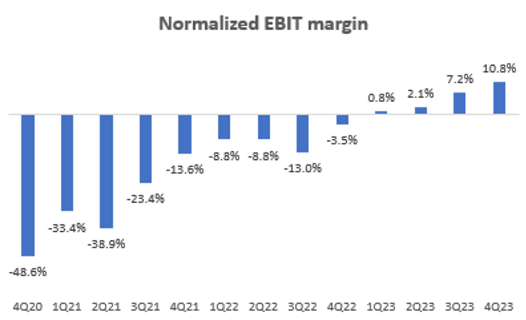

PLTR is also building upon its transition to profitability and increasing margins steadily:

Normalized EBIT Margin (Company Filings, Hunting Alpha Analysis)

Steady-state profitability is nowhere close to being hit just yet reached as the incremental YoY normalized EBIT margins have been north of 80% for the last 3 quarters and north of 50% for the last 6 quarters.

Management’s guidance is falling short of expectations

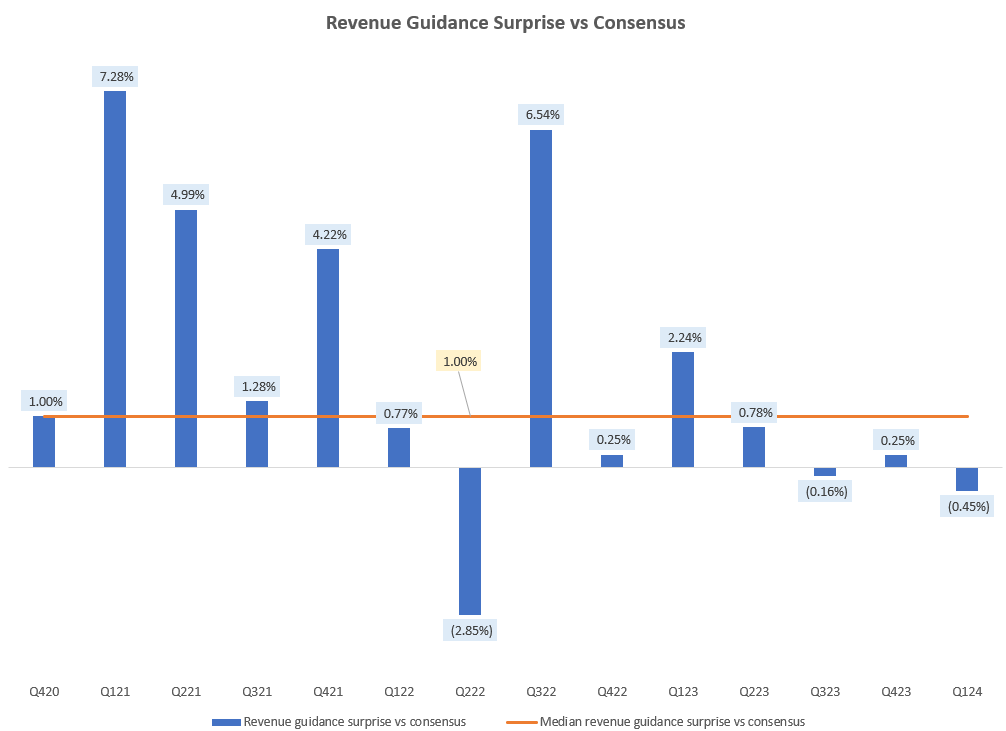

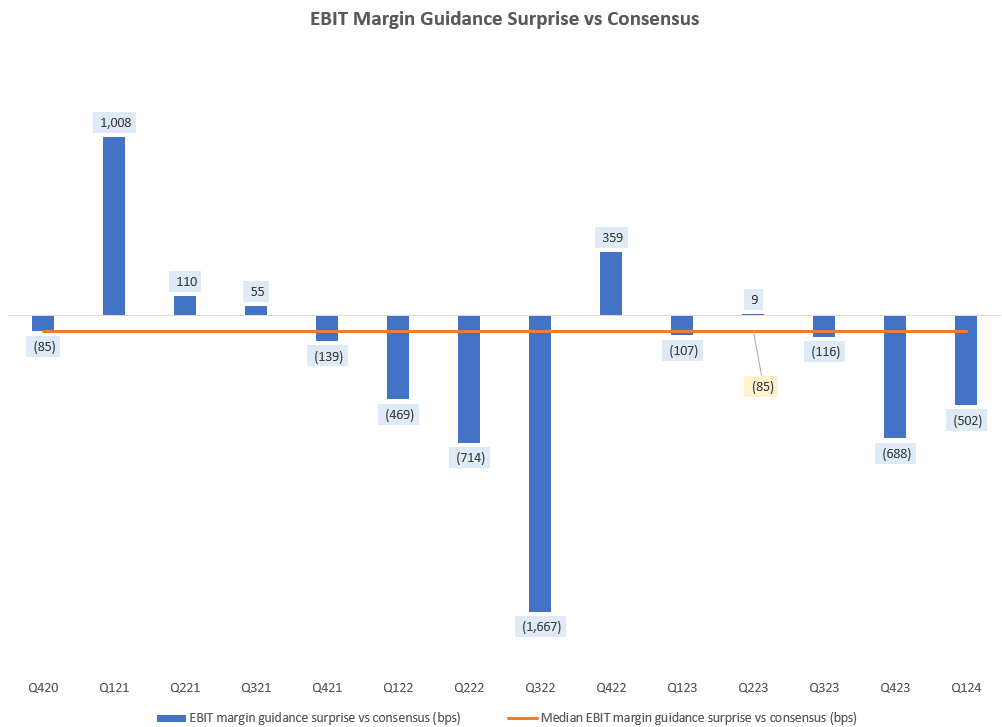

Clearly, Palantir’s operating momentum is sky high. However, it seems the market’s expectations are higher still. Q1 FY24 guidance stood at $617 million revenues and an implied 22.64% EBIT margin. However, both these numbers fell short of what Wall St consensus was expecting, as evidenced by the negative surprises:

Revenue Guidance Surprise vs Consensus (Capital IQ, Hunting Alpha Analysis) EBIT Margin Guidance Surprise vs Consensus (bps) (Capital IQ, Hunting Alpha Analysis)

This indicates that as bullish as Palantir’s progress may be, much of the optimism is already priced in, especially when one considers the fact that:

Valuations are near historical peak levels

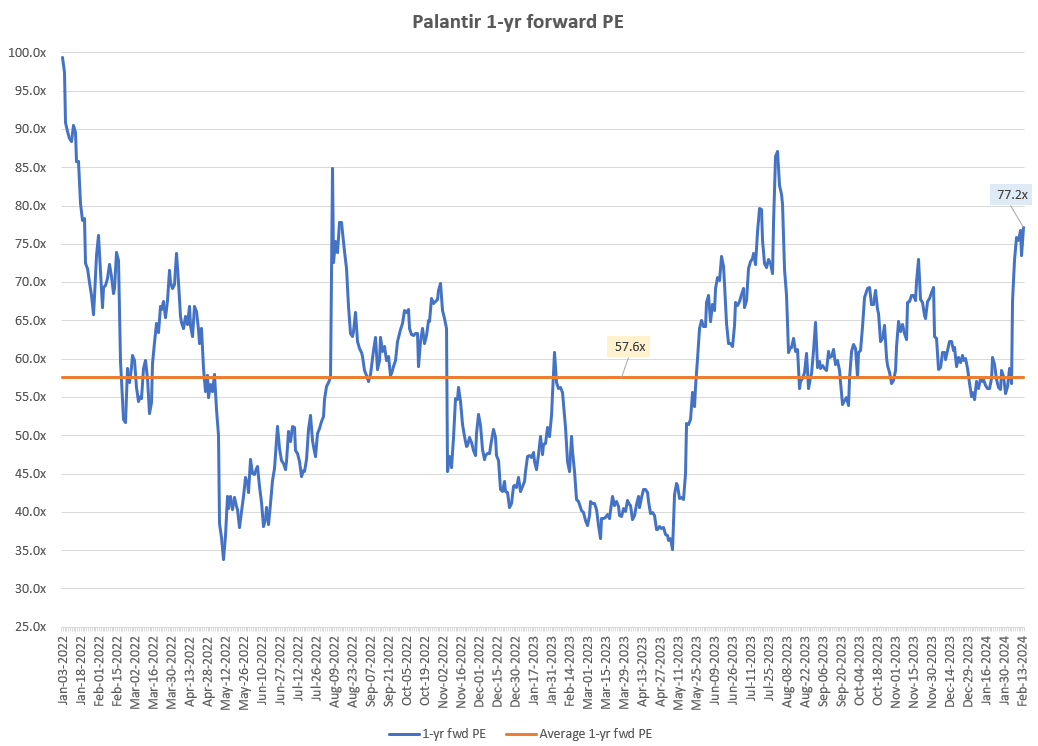

Palantir 1-yr fwd PE (Capital IQ, Hunting Alpha Analysis)

Palantir’s 1-yr fwd PE stands at 77.2x. The average 1-yr fwd PE over the last 2 years has been 57.6x; near the middle of the range marked by ~80x peak valuations and ~40x trough valuations. So with Palantir trading near historical peak valuations, at almost a 35% premium to the average or median (58.7x) band, I believe there is limited margin of safety for buys, even when considering the strong growth track.

Technical Analysis

If this is your first time reading a Hunting Alpha article using Technical Analysis, you may want to read this post, which explains how and why I read the charts the way I do, utilizing principles of Flow, Location and Trap.

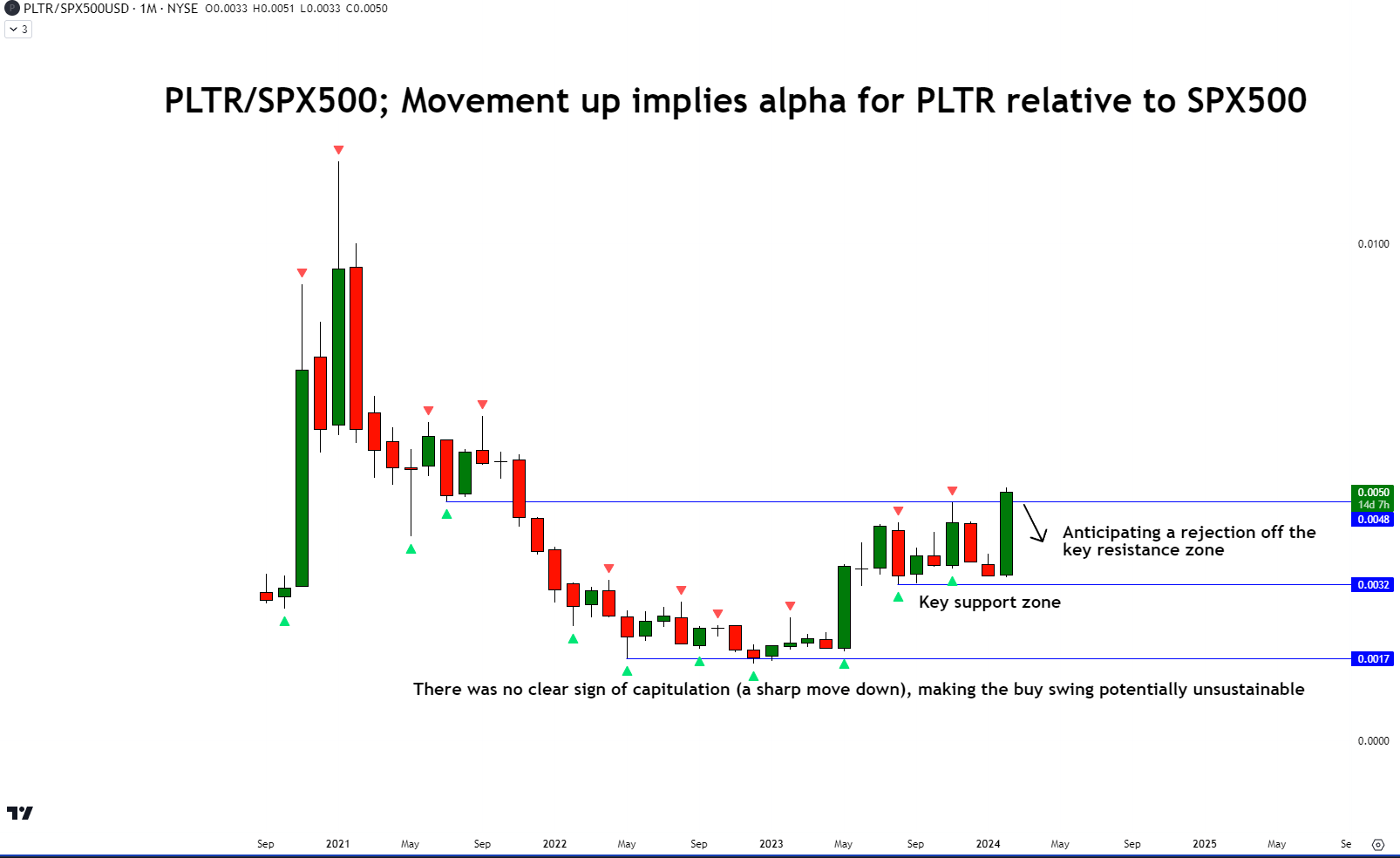

Technical Analysis of PLTR vs S&P500 (TradingView, Hunting Alpha Analysis)

In the monthly relative chart of PLTR vs the S&P500, I notice that the ratio prices are near a key resistance zone. I anticipate sellers to post a rejection off this area. Another thing I observe is that in this overall buy-swing (alpha-generating swing) that began in May 2023, there was no clear sign of seller capitulation via a sharp move down preceding the buys. I believe this lack of a V-shaped recovery increases the chances of a less sustainable and buyer led move that has the ability to continue and match record highs.

Takeaway and Risk Mitigation

Admittedly, my relative bearish view on Palantir vs the S&P500 is mostly based on a belief of overextended valuations and a couple of negative surprises on company guidance. This view is at odds with some very impressing operating momentum metrics, including very healthy backlog (RPO) growth.

Typically, I’ve learnt that it is generally risky to go against the trend of red-hot operating momentum. Hence, my risk mitigation plan is simple; if the relative chart of PLTR vs the S&P500 shows a sustained break above the key monthly resistance level, then I will throw in the towel, accept defeat and revise my view. Because if this scenario plays out, then my main argument for being bearish the stock would be based on valuations alone. And how long can that go for? What if the stock continues to outperform? Holding on to the ‘Sell’ view with the excuse of high valuations would be irresponsible in my view because the market can defy valuation-only arguments very easily.

Hence, I rate the stock a ‘Sell’, but with a flexible readiness to change my mind if need be.

How to interpret Hunting Alpha’s ratings:

Strong Buy: Expect the company to outperform the S&P500 on a total shareholder return basis, with higher than usual confidence

Buy: Expect the company to outperform the S&P500 on a total shareholder return basis

Neutral/hold: Expect the company to perform in-line with the S&P500 on a total shareholder return basis

Sell: Expect the company to underperform the S&P500 on a total shareholder return basis

Strong Sell: Expect the company to underperform the S&P500 on a total shareholder return basis, with higher than usual confidence

The typical time-horizon for my views is multiple quarters to around a year. It is not set in stone. However, I will share updates on my changes in stance in a pinned comment to this article and may also publish a new article discussing the reasons for the change in view.

Q2 2024 Earnings Call Transcript")