Michael Vi/iStock Editorial via Getty Images

Overview

I’ve been an investor in Palantir (NYSE:PLTR) since its IPO three years ago, purchasing shares at $18 and $7. The journey has indeed been a roller coaster. My enthusiasm for the company extends beyond its stock price fluctuations; I’ve been a fan for years, ever since reading a Fortune article that portrayed Palantir as an organization with a strong culture that developed a disruptive product for data analytics within the Army.

In the past five days, the stock has surged by 40%, generating considerable excitement around the company. However, this hype can obscure our judgment, making it crucial to remain rational when making any recommendations about the stock.

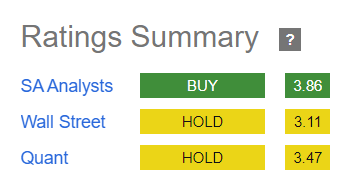

Figure 1: Seeking Alpha

We are outlining a recommendation on the company, focusing on three main aspects. Fundamentally, I admire the company’s products and how effectively they’ve capitalized on AI opportunities in the commercial sector. I believe their government business is robust, although, the Q4 results have been disappointing. However, my main concern lies in the insufficient progress in expanding their commercial business internationally.

Figure 2: Seeking Alpha

Seeking Alpha analysts are bullish about the stock, in contrast to Wall Street analysts and Seeking Alpha Quant. Let’s find out which is my recommendation as a long-term investor in the stock

What I like about Palantir: its products, their commercial business AI strategy and its potential inclusion in the S&P 500

Over the past 20 years, Palantir has dedicated itself to developing the operating system for businesses (Foundry) and government (Gotham). Rather than simply creating individual software applications like CRM or ERP systems, Palantir aims to build comprehensive platforms. These platforms serve as operating systems that can be tailored to reflect the unique operations of a business, establishing the appropriate data structures and integrations to facilitate decision-making. This approach carries significant business implications, as an operating system exhibits substantial network effects and has the potential to dominate the market. These network effects arise from the platform’s ability to bring together developers, operations specialists, and business managers, integrating various software solutions. As more users engage with the platforms, they generate increasing value for others within the ecosystem. For instance, if managers adopt the software, operators are compelled to use it, and managers may instruct developers to build upon the platform. This interconnected ecosystem reinforces the platform’s value proposition and fosters its growth.

Figure 3: Palantir website. Foundry

In the history of operating systems, dominance has traditionally been tied to a specific hardware platform, such as Windows with Intel processors or Android with smartphones. Palantir is aiming to break away from this paradigm by decoupling its platforms/operating systems from any specific hardware infrastructure. This strategy enables them to potentially dominate the B2B market without being reliant on the evolution of hardware. To achieve this goal, they have launched Apollo. The ambitions of this relatively small company are lofty, and it remains to be seen whether they can successfully execute their vision. We need concrete evidence indicating that they are progressing in the right direction.

They have cracked the commercial business leveraged by AI

Its software is exceptionally well-built, evident in how rapidly they integrated Large Language Models (LLMs) and developed a new platform, AIP, from scratch. This product or platform capability has enabled Palantir to swiftly capitalize on the GenAI opportunity. Not only have they created a robust product, but they have also devised an effective go-to-market strategy with Bootcamps. Bootcamps serve as workshops where the Palantir team collaborates with developers, analysts, and managers from potential clients. During these workshops, they strive to implement use cases using the Foundry Platform alongside the potential client’s systems or cloud solutions. For example, a client recently developed a use case ready for immediate implementation, resulting in significant savings of $10 million. In October, Palantir set an ambitious target to conduct 500 AIP bootcamps within a year, a goal they have substantially surpassed, completing over 560 bootcamps for 465 organizations to date, as stated in its earnings call.

This strategy has proven effective. The number of commercial customers increased by 44% year-over-year to 375 clients in the last quarter, according to the latest 4Q2023 earnings release. Furthermore, in the fourth quarter, the company achieved a significant milestone by attaining a commercial Total Contract Value (TCV) of $699 million, marking its highest quarterly figure to date. This remarkable outcome underscores a substantial year-over-year growth of 156%.

Growth among existing clients has also been robust. Revenue in the US commercial business has surged by 70% year-over-year, accompanied by a 55% increase in client count. Moreover, the average revenue of the top 20 customers has risen by 11%, climbing from $49 million to $55 million.

The third pillar of this model revolves around operating leverage: as the business expands, it becomes more profitable, achieving a free cash flow margin of 50% compared to 15% in the fourth quarter of 2022. Adjusted EBITDA, akin to the operating margin, has surged from 24% to 36% due to increased business capture from existing and new clients, primarily driven by the same software infrastructure. While software improvements and new functionality are ongoing, the effort required is not proportionate to the revenue capture. Additionally, net working capital and CAPEX have been managed effectively, even amidst such rapid growth rates.

Figure 4: Author

Tailwinds in corporate events could further boost the stock price: inclusion in the S&P 500 index

Palantir has achieved five consecutive quarters of GAAP profitability, with $100 million in net income. I anticipate this trend to continue throughout 2024. Alex Karp has been striving for this, and the CEO of Palantir has talked about the inclusion in the S&P 500 as a strength for the company:

My interest in profitability is for obvious reasons, but it’s also, I think we’ll just be in a much stronger position as we — it becomes clear that we are — we qualify for participation in S&P, and a lot of people look as a fresh, new and we’ll begin to look closer at our strengths.”

This is why stock-based compensation is being reduced as a percentage of revenue. I estimate that the stock price could increase by more than 15% upon news or speculation of inclusion in the index, similar to what happened with Uber (UBER) recently. I don’t think this event is factored into the current stock price, the main driver behind the stock’s rise is its AI commercial business, as we’ve discussed.

Figure 5: The Wall Street Journal

… but there are some concerns: government and international businesses

Government revenue increased by 11% year-over-year to $324 million, which may not seem impressive initially. However, management believes that the current business is solid, despite not securing much new business this quarter. They expressed optimism in the 2Q2024 earnings call, citing several reasons. Palantir expects to win a contract for the next phase of TITAN from the Army in Q2 2024. They’re actively involved in major conflicts worldwide, although specifics are limited. Initiatives like Mission Manager and the First Breakfast are related to large programs for Joint All-Domain Command and Control (JADC2). Palantir also extended its partnership with the Army to enhance the Army Vantage platform. They noted that the Army’s allocation of only 0.015% of its budget to command and control software in fiscal year ’24 is commendable, with expectations for increased investment in the future.

Another worry is the performance of the commercial international business, which grew by 11% year-over-year to $154 million. Alex Karp mentioned in the earnings call that European companies are not embracing the AI revolution. Although they discussed new distribution methods with Fujitsu and saw growth in Asia, the renewal of contracts with Novartis and Swiss Re, it’s clear in my opinion that this segment isn’t performing well. This suggests that Palantir hasn’t figured out the right approach to succeed with these companies.

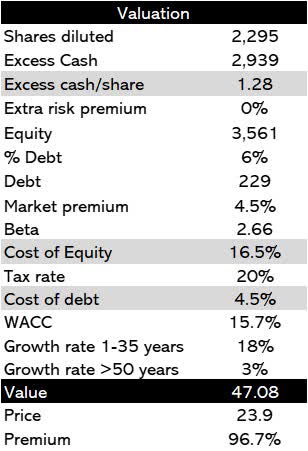

Palantir’s Valuation

I believe Palantir is a powerful company aiming to dominate business operating systems. Their top-notch software and strong performance show they’re on track to lead this important sector. To value Palantir, I’ll use a method I introduced in my ARM article, the Dominance Company Valuation. With $1.28/share in excess cash, I’ll assume an 18% growth rate in free cash flow for the next 35 years.

Figure 6: Author

Nobody can predict the future, not even if Palantir will succeed in the market. I can’t predict what will happen either, but I see Palantir as a great company. Growing at 18% for 35 years seems very feasible to me, as other successful companies have achieved similar growth rates.

Conclusion

4Q2024 was a standout quarter for Palantir. Their top-notch software has successfully seized the AI opportunity, starting with ChatGPT and making waves globally. Palantir has cracked the US commercial market with a model centered around their software platform, Foundry, complemented by a go-to-market strategy based on Bootcamps. They learn from real-world cases, making slight software improvements that lead to better profitability. However, there are challenges in the government and international commercial sectors. I believe they still have much to do and learn.

To me, Palantir is an inspiring company that has revolutionized the Army, emerged as an AI leader, and is poised to dominate business operating systems. While its valuation is high, I see the potential for the stock price to rise significantly higher.

Q2 2024 Earnings Call Transcript")