Dilok Klaisataporn

Introduction

On Holding (NYSE:ONON), often referred to as On Clouds due to its product line-up, is an appealing brand offering premium footwear and sports apparel products that have been gaining in popularity in the past few years. The absolute size of the company compared to its industry peers including Nike (NKE) and Lululemon (LULU) is far smaller, yet I believe a potential investment in On Holdings is attractive. On Holdings is not only an extremely fast-growing company with a strong and growing brand power, but the company’s bottom line is expanding along with the growth and expansion of the company creating a unique and appealing buying opportunity for investors. Further, the company has a reasonable valuation with a strong balance sheet along with the potential macroeconomic tailwind with strong consumer spending during the holiday season. Therefore, due to the strong growth of the company and the brand power, I believe On Holding is a buy.

Growth Momentum

On Holding has a strong growth momentum behind the company, which is reflected by the historical trend in revenue growth. As the chart below shows, On Holdings has been reporting strong revenue growth fairly persistently for the past several quarters.

Seeking Alpha

[Chart created by authoring using source]

As showcased during the 2023Q3 earnings report, the management team and the company’s revenue data also portray strong momentum. In the first nine months ending in September 2023, the company’s net sales increased 46.5% or 58% in constant currency year-over-year to 1.345 billion CHF. Further, the management team said that “the third quarter has not only been the seventh consecutive record top-line quarter but also our most successful quarter in history across numerous measures.” Further, the company is also expecting this momentum to continue as the company has raised the full-year 2023 outlook during this earnings report in November. Therefore, the company has a strong growth momentum.

I believe the implication of having a strong growth momentum is monumental as it likely implies two things. One, On Holding’s fast growth and success, are likely not a fad. Second, it is likely that the brand power and recognition are getting stronger along with the continued demand for the company’s products.

Oftentimes, for relatively newer companies, initial fast growth is later determined as a fad. Consumers are likely interested in the new popular thing resulting in a temporary interest; however, in the case of On Holdings, because the company has been experiencing a strong growth momentum for multiple years with an expectation for continued strong growth in the near term, I believe it is reasonable to argue that the demand for the company’s products are not a fad.

Strong brands are lucrative. A company can leverage the brand for strong demands and higher margin products. This is likely the case for On Holdings. Along with the strong momentum in revenue growth, the company’s brand power has also strengthened. During the 2023Q3 earnings report, the company said that the “growth in the three months was driven by On’s direct-to-consumer (“DTC”) channel, recording a growth of 54.6%” before saying that the company’s DTC channel will outgrow its wholesale channels as a result of “the strength of On’s existing own channels.” In other words, due to On’s brand power and its appeal, the company can grow higher margin DTC channels since the consumers are willing to seek out On’s own channel over wholesalers.

Overall, On Holdings is experiencing a strong growth momentum. On the surface, the revenue growth is strong, but within the surface, it implies that the current growth is not a fad as it is a process of creating a strong and appealing brand for sustainable future growth.

Earnings Momentum and Balance Sheet

On Holding’s strong top-line growth is also accompanied by an expanding bottom line. Unlike some relatively younger and fast-growing companies reporting continuous losses during the early years of operations, On Holding is expecting a strong margin and bottom-line expansion.

During the 2023Q3 quarter, the company’s gross profit increased 53.5% year-over-year to 287.7 million CHF from 187.4 million CHF. Further, the gross profit margin increased to 59.9% from 57.1% with an expectation for a 59% gross margin for the full year 2023. Finally, regarding the future outlook, the company said “The higher DTC share, alongside On’s premium positioning and ongoing high full-price share will further support the achievement of higher gross profit margins in the future.” Therefore, the company’s earnings momentum is also strong with a continued expectation for this trend to continue as the top line continues growth and the brand power grows along with it.

On Holding also boasts a strong balance sheet health. The company has about $471.9 million in cash with a total assets of $1.86 billion. On the other hand, the company’s total debt of $227 million with a total liability of $668.5 million bringing the total liabilities to asset ratio at only about 35.94%. Therefore, the company’s balance sheet is healthy and will likely allow On Holding to sustain any unforeseen events of a reasonable magnitude.

Valuation

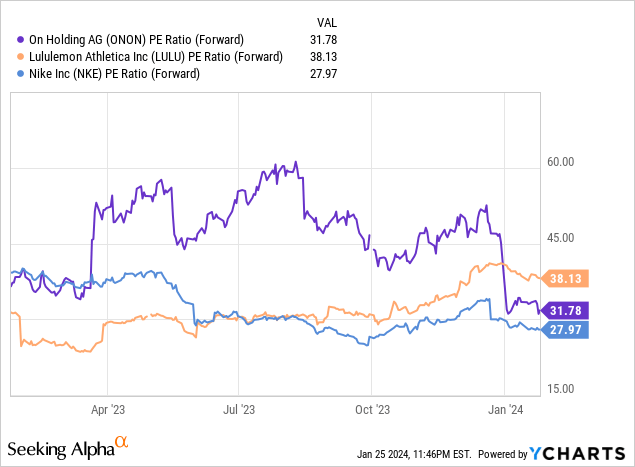

On Holdings has an attractive valuation multiple. The company has a 2024 forward price-to-earnings ratio of 31.26. Compared to the company’s industry peers, Nike, and Lululemon, On Holding’s valuation, multiple sits between these two companies as Nike and Lululemon have a forward pe ratio of about 27.97 and 38.13, respectively, as the chart below shows.

[Chart created by author using YCharts]

The valuation multiple compared to these peers may not seem cheap nor attractive; however, when taking into account the growth rate of all the companies, both top and bottom-line, On Holding becomes much more attractive.

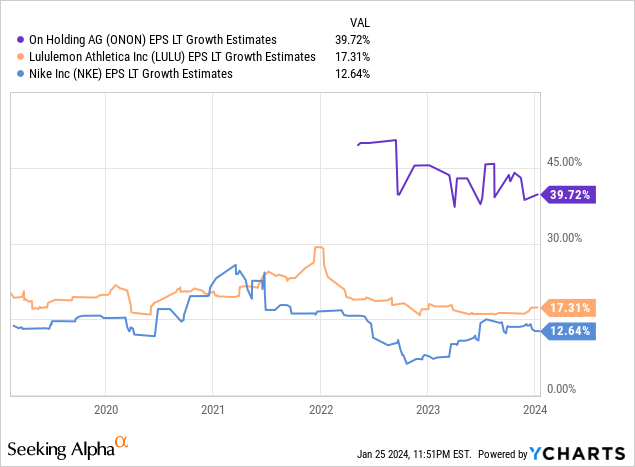

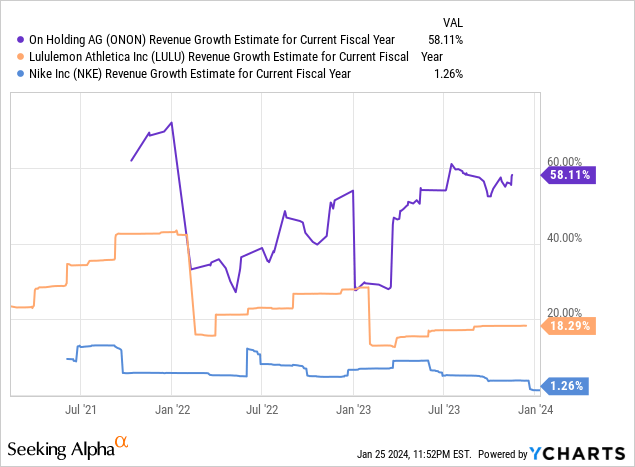

The chart directly below compares the three companies’ long-term EPS growth estimate, and as it is clearly shown, On Holdings is expected to show significantly stronger growth than both Lululemon and Nike. Further, the second chart below compares the three companies’ revenue growth estimates for this fiscal year. Again, it is clear that On Holdings is expected to report the strongest growth.

[Charts created by author using YCharts]

Therefore, considering that On Holdings is expected to report stronger top and bottom-line growth relative to its peers, I believe On Holding’s valuation multiple, which is in line with the industry peers, is attractive.

Risks

Looking at On Holding’s balance sheet, it shows that the company’s inventory grew far faster than the revenue from 2022Q3 to 2023Q3 period. At the end of 2023Q3, the company’s inventory levels stood at $463.7 million, which was about 74.32% increase from the previous year. Compared to the revenue growth of 46.5% year-over-year, the inventory levels grew at a far faster rate. The inventory level’s faster growth, while it is likely a result of the holiday season, could expose the company to some risks as it could be a drag on the company if any unforeseen events hinder the company’s growth rates.

Summary

On Holding is attractive. The company is experiencing a fast top and bottom line growth. This implies that the company is not only building a strong, attractive, and potentially lasting brand, but it also implies that the company is not sacrificing profits for growth. Further, On Holdings has an attractive valuation multiples along with a strong balance sheet. Therefore, I believe On Holdings is a buy.

Q2 2024 Earnings Call Transcript")