ryasick

Oaktree Specialty Lending (NASDAQ:OCSL) suffered weakness in its dividend coverage metrics for the quarter ending March. While the decline in the dividend coverage was not great, the BDC announced that it was lowering its management fee which is set to improve Oaktree Specialty Lending’s dividend coverage. As a result, I don’t expect the BDC to lower its dividend as the estimated impact of the management fee reduction is set to improve Oaktree Specialty Lending’s dividend coverage metrics. The company is also seeing solid origination growth and the portfolio remained well-diversified in the last quarter. With shares currently trading at only a small premium to net asset value, I believe investors, despite a deterioration in dividend coverage, should remain invested here!

Previous rating

I rated shares of Oaktree Specialty Lending a strong buy in February — Fear Creates 11%-Yielding Buying Opportunity (Rating Upgrade) — after the BDC reported Q4’23 results that also showed a slight deterioration in the company’s dividend coverage. The change in the fee structure that management announced is a positive for shareholders and is set to improve the BDC’s coverage metrics, however.

Robust new originations, well-diversified investment portfolio

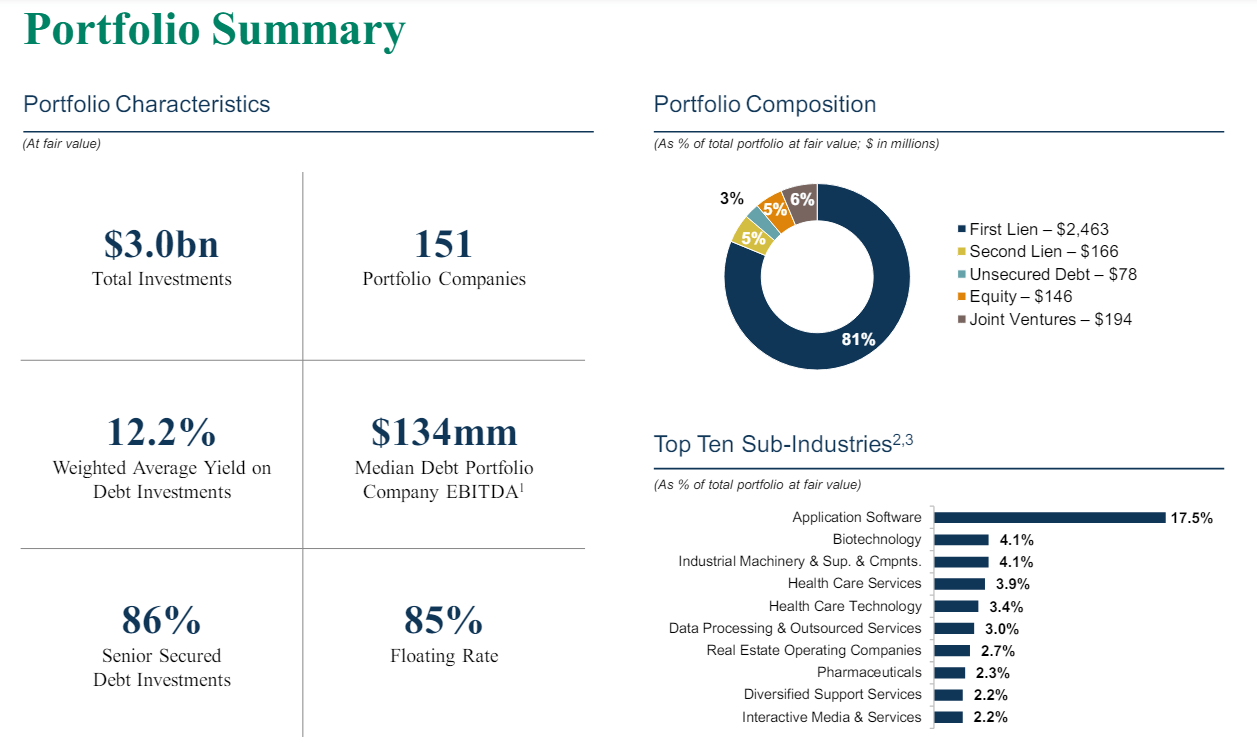

Oaktree Specialty Lending offers dividend investors a first lien-focused investment strategy that it complemented by other investments in second liens, unsecured debt, joint venture and equity. By far the most important investment position are first liens, which represented 81% of Oaktree Specialty Lending’s portfolio structure in the March quarter. All investments combined had a value of $3.0B. Of those investments, Oaktree Specialty Lending retained an 85% variable rate investment percentage.

Oaktree Specialty Lending

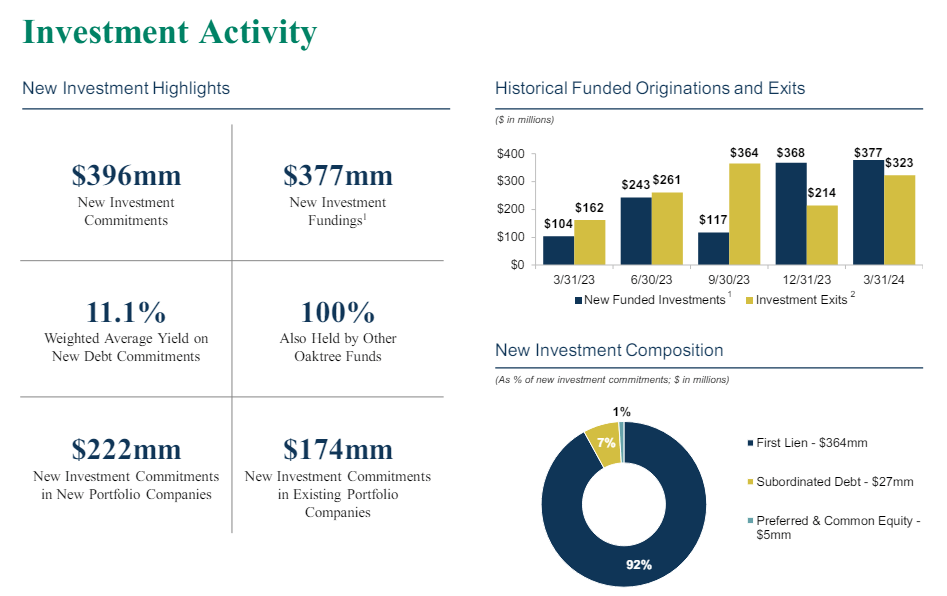

Oaktree Specialty Lending did $377M in new investment fundings in the March quarter which was about on the same level as in the prior quarter. I see a catalyst for further growth in new investment fundings under the condition that the Federal Reserve lowers the federal fund rate in the second half of the year.

Oaktree Specialty Lending

Oaktree Specialty Lending’s non-accrual percentage, which quantifies the risk of potential loan write-offs, decreased to 2.4% at the end of the March quarter, showing a 1.8% PP sequential decline. In this particular sense, Oaktree Specialty Lending’s asset quality improved Q/Q.

Turning to Oaktree Specialty Lending’s dividend coverage.

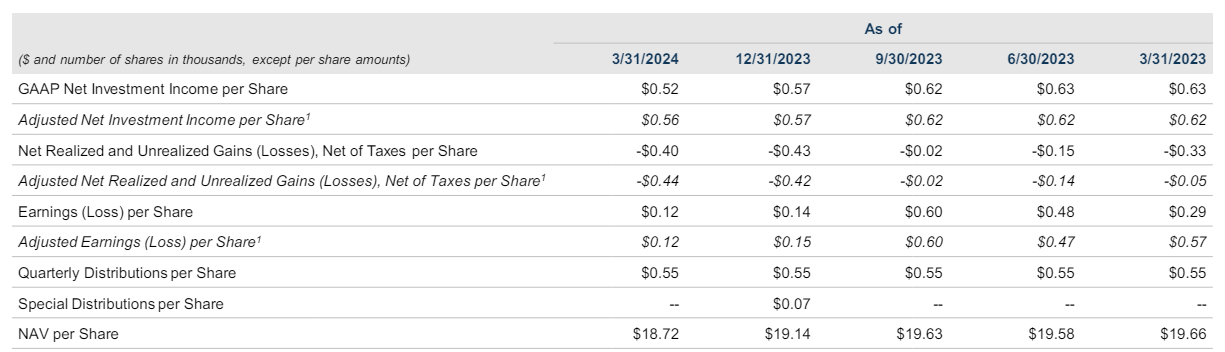

The BDC earned $0.56 per-share in (adj.) net investment income in the last quarter, showing a decline of 10% year over year. The decline was chiefly due to lower interest income from its loan portfolio. With $0.56 per-share in NII and a dividend of $0.55 per-share, the BDC’s dividend coverage ratio in FQ2’24 was just 1.02X. In FQ1’24, the previous quarter, Oaktree Specialty Lending’s investments generated net investment income, on an adjusted basis, of 1.04X.

Because of the decline in dividend coverage, Oaktree Specialty Lending announced a permanent reduction in the company’s base management fee. This fee reduction will boost the BDC’s net investment income by an estimated $0.03-0.04 per-share quarterly. If the base management fee reduction were in place in the last quarter already, Oaktree Specialty Lending’s dividend coverage ratio would have been 1.07-1.09X. As a result, I don’t believe Oaktree Specialty Lending will reduce its dividend, but I come to this conclusion only because of the BDC’s permanent base management fee reduction.

Oaktree Specialty Lending

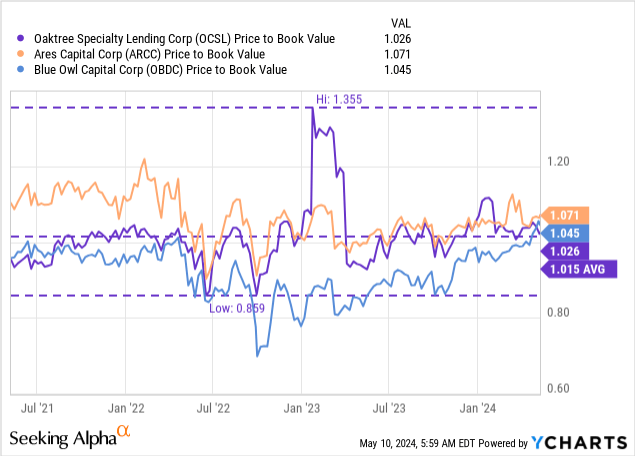

Oaktree Specialty Lending’s valuation

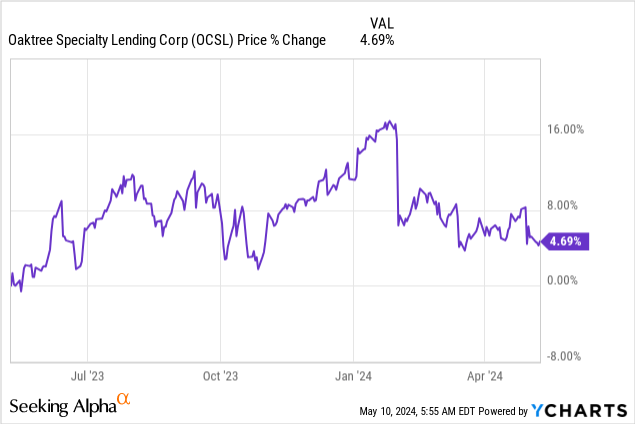

The BDC suffered trading weakness after the company reported earnings for Q1’24, with shares declining after earnings. Shares of Oaktree Specialty Lending are currently trading at 1.03X P/NAV which is slightly above the 3-year average P/NAV ratio of 1.02X. However, Oaktree Specialty Lending traded at a higher net asset value multiplier in the last year when its credit quality was looking better. If Oaktree Specialty Lending returns to better asset quality, through work-outs, as an example, I believe the BDC could achieve a higher valuation, especially if it avoids a dividend cut. My fair value estimate for Oaktree Specialty Lending is $18.74, which equals the company’s net asset value for the March quarter, after payment of the $0.55 per-share quarterly distribution.

Risks with Oaktree Specialty Lending

The most important metric to track here is the dividend coverage ratio as it is the primary indicator that signals a potential change in the safety of the dividend. Additionally, I consider the NII trend to be something worth watching, especially because Oaktree Specialty Lending has 85% of investments in loans that carry variable rates. If the Federal Reserve starts to cut the federal fund rate in the second half of the year, Oaktree Specialty Lending is potentially set to see a decline in its interest income and net investment income.

Final thoughts

Oaktree Specialty Lending is set to make a change to its fee structure which will take some pressure off of the BDC’s dividend coverage ratio. The BDC’s loan quality, judged by the company’s non-accrual percentage, however, has improved in the last quarter which is why I maintain my strong buy rating. With shares currently trading slightly above net asset value, I believe shares remain a strong buy here for dividend investors. I don’t expect Oaktree Specialty Lending to reduce its dividend at the current time, largely because of the estimated outlook for future net investment income related to its base management fee change!

Q2 2024 Earnings Call Transcript")