onurdongel

Nucor (NYSE:NUE) experienced a mixed FY23 when compared to the previous year, generating a substantial amount of free cash flow on softer revenue. Despite the headwinds to growth, management remains optimistic about eFY24 as building construction and infrastructure projects pick up steam as a result of the IRA and CHIPS Act. As management anticipates a strong year ahead of them, operations at their new Brandenberg steel plant facility are expected to pick up in eFY24 and reach breakeven by mid-2024. In addition to commodity pricing risk, there are a number of macroeconomic challenges that Nucor faces in eFY24 and eFY25 that may create a challenging market for the steelmaker. I provide NUE shares a SELL recommendation with a price target of $145.55/share.

Operations

On their FY23 earnings call, management discerned rightsizing their balance sheet as the firm has pooled cash in anticipation of a merger deal with US Steel (X). As a result, the firm ended the year with just over $7b in cash and $6.8b in debt on the balance sheet. Going into eFY24, management anticipates putting this cash to use as they ramp up their capital investment program in bringing new facilities online through 2026.

Lourenco Goncalves, CEO of Cleveland-Cliffs (CLF) was very suggestive post-FY23 earnings that the Nippon and US Steel deal will not go through the antitrust process and that a deal may still be on the table, albeit at a reduced premium. Nucor management cited that they will not overpay for an acquisition and appeared to have moved on from the US Steel deal. Though this is purely speculation, I believe that if the Nippon & US Steel deal were to falter and Cleveland-Cliffs come back with a lower purchasing premium, Nucor may find interest in rekindling the acquisition process at the lower bidding premium as management mentioned that M&A elsewhere is in their outlook.

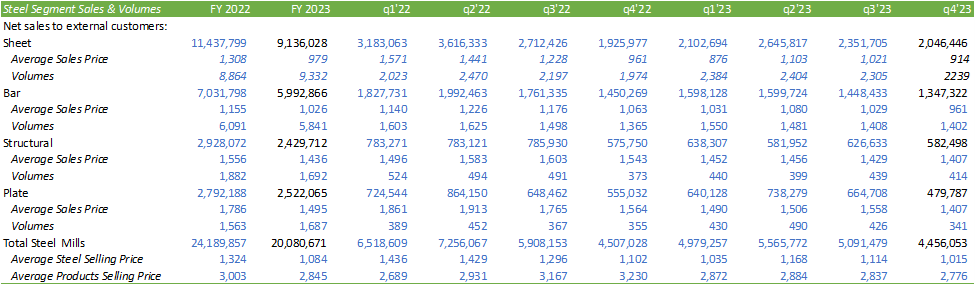

FY23 experienced challenging comps as average earnings per ton fell nearly -40% from $401/ton to $245/ton as sales per ton fell by 15% from $1,626/ton to $1,377/ton. Nucor’s steel segment faced significantly challenging prices across all steelmaking products that resulted in a decline in revenue. (note, the chart that follows may not be 1-for-1 as FY23 and q4’23 are using average sales prices and volumes as reported and not total figures).

Corporate Reports

Though Nucor experienced a 2% increase in steel volumes, product volumes, and raw materials experienced a decline of -10% and -6%, respectively.

Corporate Reports

This has led to a -34% decline in earnings before tax.

Corporate Reports

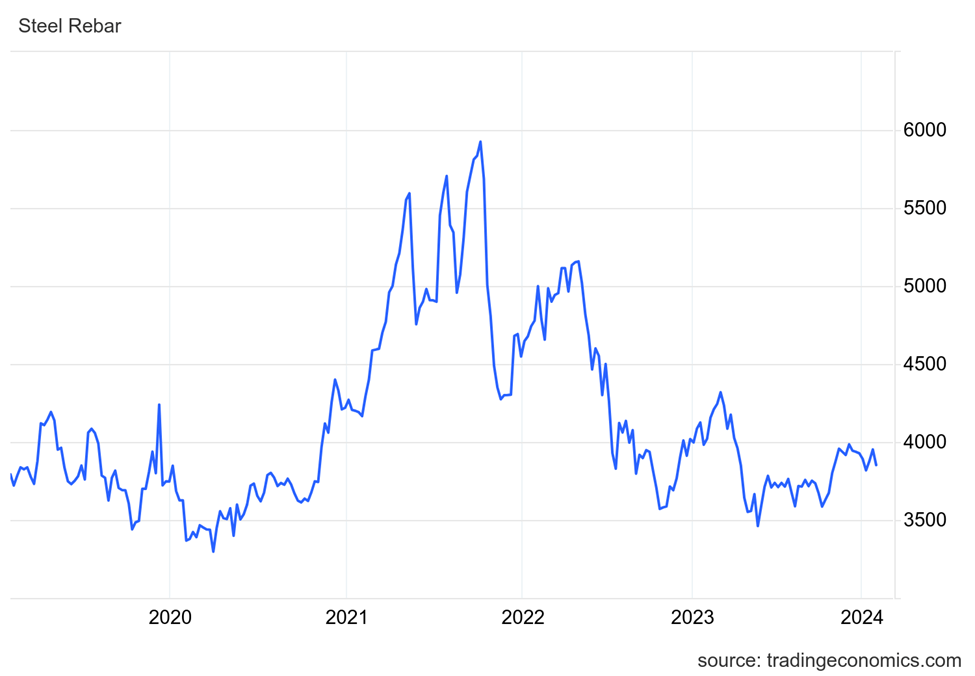

Comparing aggregate FY23 to FY22 steel prices sheds some light on the commodity and why Nucor’s top line suffered in the fiscal year.

TradingEconomics

Despite the headwinds, Nucor managed their cash well, generating $4,898mm in free cash flow for a 14% flow through. Though FY23 FCF is about -40% below FY22’s free cash generation, free cash flow appears to have become more normalized when compared to FY21 as steel prices leveled out from their high in FY22.

Looking ahead to eFY24, I anticipate some growth challenges net of volumes from new facilities being brought online. As Nucor’s steel is relatively commoditized, their revenue is largely driven by market price + hedges. The challenges I anticipate derive more from a macroeconomic perspective as opposed to an operational perspective. I do believe that Nucor will experience volumetric growth as they bring their Brandenburg and Gallatin facilities up to a profitable run rate further into eFY24.

For the Steel Mills segment, we expect quarterly earnings to increase due to higher realized pricing and higher volumes, in particular, from our sheet mills. In the Steel Products segment, we expect lower realized pricing compared with the prior quarter.

Steve Laxton, EVP & CFO

Nucor deployed $2.2b in capital investments in FY23 and anticipates deploying $3.5b in eFY24 with 7 of their largest growth projects representing 2/3rd of the total investment. As far as positive macro catalysts are concerned, I anticipate many of the cited areas of growth to either be slower than expected, smaller than expected, or pushed back to a later date.

Macroeconomics

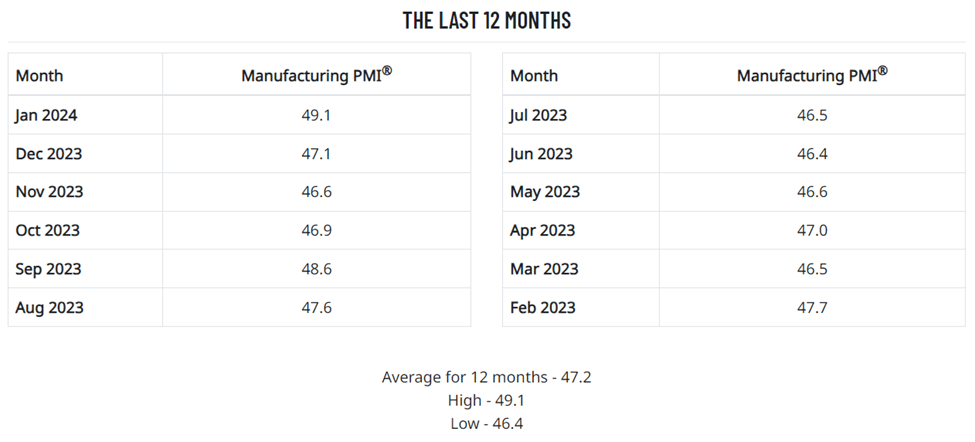

At a high level, the January Manufacturing PMI remained in contractionary territory at 49.1% in aggregate. The report suggested that inventories increased by 2.3% to 46.2% but still remained in a highly contractionary state, while backlog orders remained in a strong contractionary state at 44.7%. As customers’ inventories, differentiated from inventories, fell back to 43.7%, there may be some tailwinds for Nucor if inventories require replenishment.

ISM Manufacturing PMI

Good start to the year. We had budgeted a 3.5-percent increase over 2023. We expect it to be a challenging year. Currently, orders are positive in our automotive OEM and automotive aftermarket business. Our industrial business sector is looking weak at the moment. Still, expect to achieve budget forecasts through the first quarter. We feel January is running high for automotive because at the end of December, many OEMs cancelled the last few weeks of orders to reduce inventory levels.

ISM PMI Fabricated Metal Products respondent

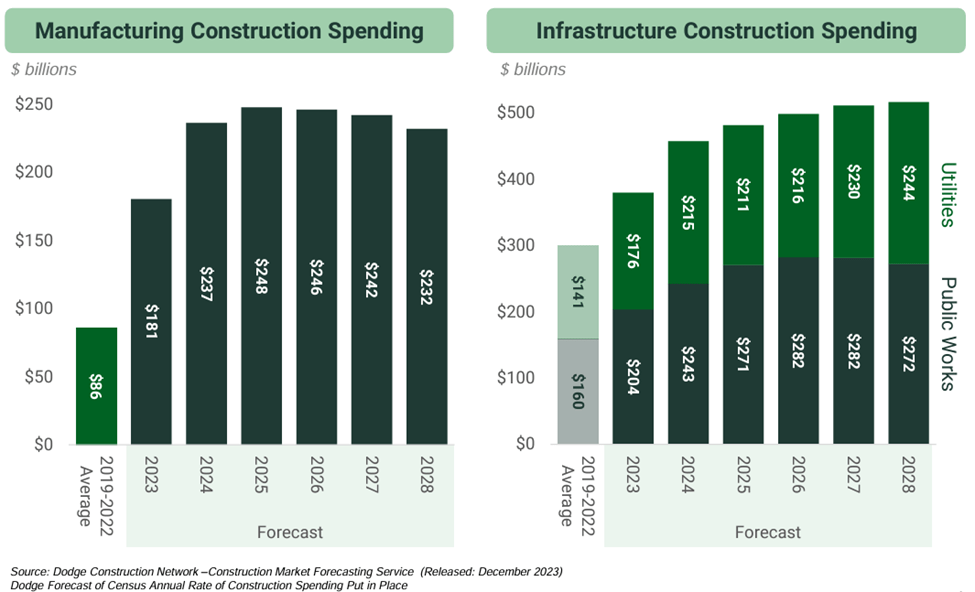

Nucor management anticipates a strong year for infrastructure and construction spending as the big legislature is anticipated to begin taking shape. Between the IRA, Infrastructure Bill, and the CIPS Act, management expects a significant amount of projects to commence in eFY24 through the end of the decade as manufacturing comes onshore or nearshore.

Corporate Reports

Accordingly, McKinsey & Co. expects chip manufacturers to invest between $223-260b in developing new foundries through 2030 with $54b in grants under consideration under the CHIPS Act. This should be a huge opportunity for Nucor to provide steel to construct these massive facilities.

In addition to this, there has been $5b announced for major transportation projects in the US with federal funding. This includes $1b to replace the Blatnik Bridge, additional construction on the I-5 Bridge over the Columbia River, a 10-mile stretch of I-10 in Indiana and Arizona, improvements to I-376 in Pittsburgh, and the Cross Bronx Expressway in New York. According to Reuters, more than $400b in projects has been announced, spanning across 40,000 projects under the Infrastructure Bill.

I believe looking at the firms that will be sourcing and constructing these projects is a good start for building a case. Below are the backlogs of a few of the EPC companies, presenting strong growth in power transmission and renewables.

Taken from their q3’23 10-q from October 2023, MYR Group (MYRG), a US-based EPC company that specializes in power transmission, experienced a significant decline in backlog.

MYR Group Backlog

On the contrary, Quanta Services (PWR) experienced a significant rise in their backlog with projects across all areas of expertise, from electrical power to renewables.

Quanta Services Backlog

MasTec (MTZ) experienced strong backlog growth as well for renewables infrastructure, communications, and O&G-related with a slight pullback on power delivery.

MasTec Backlog

On the renewables side, NextEra Energy anticipates to significantly (NEE) grow their renewables capacity through 2026. The firm expects to add 6,502MW of wind, 5,136MW of battery storage, and 8,206MW of solar through 2026, opening the door for massive steel contracts for Nucor to bid on.

Remaining on the renewables front, the DOE announced $7b in grants for developing hydrogen hubs, which can open the door for further investment in the hydrocarbon space. Hydrogen is utilized for manufacturing petrochemicals, transportation fuels, and many other industrial applications. I believe that this funding will begin a cascading effect for the space and allow for more companies to invest in hydrogen-based infrastructure and utilization.

One of the areas that I anticipate lagging growth is in the EV space. Tesla warned in their FY23 earnings report that production will be significantly reduced from FY23 numbers as the firm transitions to its next-gen factory. Both GM (GM) and Ford (F) have curtailed EV production expectations for eFY24. In addition to this, I anticipate significant headwinds in the public charging space as two of the largest pureplays, EVgo (EVGO) and ChargePoint (CHPT) have undergone recent restructurings and leadership changes as a result of stalling growth. I believe that one of the biggest challenges these firms face, with Nucor providing a part of the solution, is that the grid wasn’t designed for this level of load and that much of the infrastructure, as I have outlined in my thesis covering EVgo, must be modernized to support public vehicle charging loads.

The commercial vehicle market appears to be retracting a bit in 2024 compared to last year. Forecast sales have decreased slightly in most product segments, with only limited growth related to customers’ competitive sourcing and moves to new technology.

ISM PMI, Transportation Equipment respondent

Looking ahead, consensus estimates Nucor to have some market headwinds and generate $32.92b and $32.61b for eFY24 and eFY25, respectively, falling in line with the macro effects as presented above. I believe much of Nucor’s challenges will be due to soft steel commodity pricing as they continue to bring new EAFs online. Assuming the constant shares outstanding, consensus expects net margins to contract to 10% for both periods, generating $3.4b and 3.17b for eFY24 and eFY25, respectively. As management alluded to in their FY23 earnings call, I believe EBITDA margins may face some tailwinds as the firm focuses on higher margin value-add products; however, I do believe these headwinds may be offset by pricing as more volumes are expected to hit the market of soft inventory builds. If inventories were to reverse course, I believe that this factor could significantly change. I do believe that it would be dangerous to assume that inventories would reverse course because they’ve pulled back so much. My expectations would be such that inventories would remain at lower levels as more available volumes hit the market. If the US were to undergo a recession in eFY24, I believe that further growth challenges would be presented followed by influential government spending as 2024 is an election year. There are a lot of variables at play that can push or pull growth for Nucor, and I believe taking a more conservative approach to growth would be prudent with this level of uncertainty.

Valuation & Shareholder Value

Corporate Reports

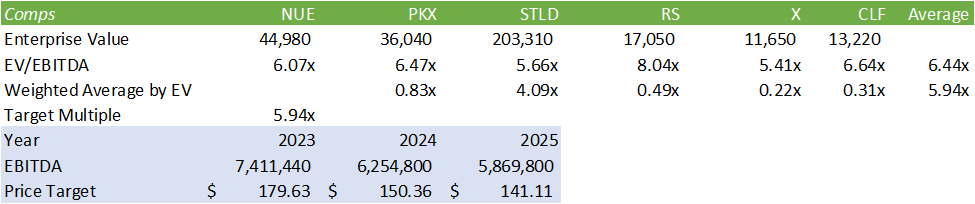

Management recently increased the dividend rate by 5.90% to $0.54/share for an annualized yield of 1.1%. NUE currently trades at 6x EV/EBITDA, in range with the rest of the industry. Using an enterprise value-weighted average approach to valuation, NUE shares can be seen as overvalued at their current multiple.

Corporate Reports

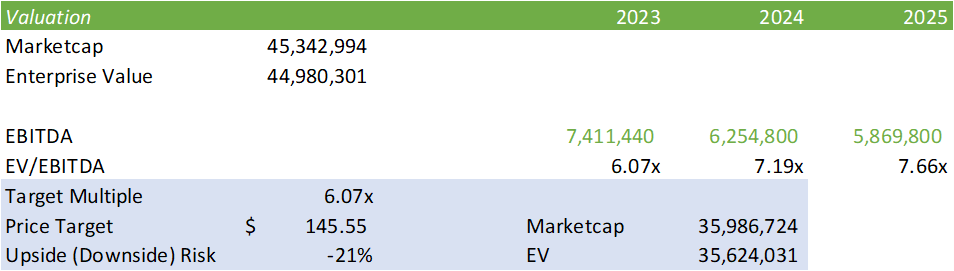

Considering my forecasted challenges on EBITDA growth, I anticipate some share decline going into eFY24 & eFY25. Though the macroeconomic landscape may change between now and then, I believe that the risk of a further economic slump, despite the government-funded projects, will result in a challenging market for Nucor. I provide NUE shares a SELL recommendation with a price target of $145.55/share.

Corporate Reports

Q2 2024 Earnings Call Transcript")