Ivan Bajic

Introduction

Nu Skin (NYSE:NUS), a beauty multilevel marketing company, faces falling sales and margins. Their products are expensive, and the multilevel marketing model is risky. Like Avon, Nu Skin might struggle. Their focus on expanding the multilevel marketing model ignores the decline of this business model. Despite a potential bright spot in manufacturing (Rhyz), the core business is expected to shrink in 2024. Overall, I recommend selling Nu Skin stock due to a bleak outlook and a less promising future in multilevel marketing.

Current Situation

Nu Skin is a company that develops and sells beauty and wellness products through direct selling, mainly person-to-person (multilevel marketing), and using social media in the beauty retailing and manufacturing industries. They operate globally, with the US representing about 26% of their revenue. In addition to their core business, they invest in related areas through Rhyz Inc. (mainly manufacturing capacities), contributing 11% of their revenue in 2023 and 13% in 4Q23.

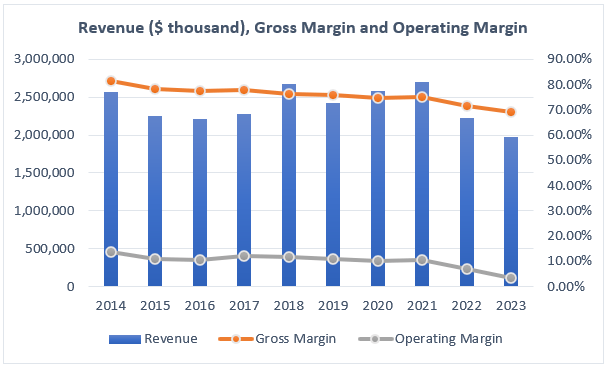

The company experienced flat sales between 2014 and 2021, but in 2022 and 2023, its revenue fell by -17.4% and -11.5%, respectively. Moreover, even if revenue remained flat most of the time, its margin didn’t. The gross margin fell from 81.4% in 2014 to 68.9% in 2023; the operating margin fell from 13.7% in 2014 to 3.5% in 2023, losing 1000 bps in less than ten years.

Author’s Elaboration with data from QuickFS

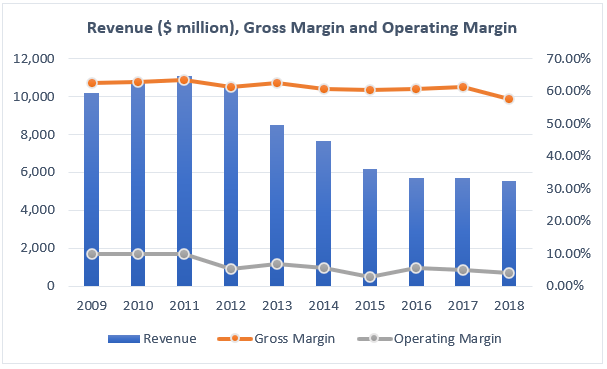

Nu Skin’s situation resembles the situation of many other multilevel marketing companies, such as Herbalife (HLF), Avon, Tupperware (TUP), and Medifast (MED). The most similar company was Avon, which was forced to sell its US business for $170 to Cerberus in 2015, and subsequently, the whole company was acquired by Natura Co. in 2020. Analyzing the last years of Avon as a public company, we find a similar pattern in its revenue and margins.

Author’s Elaboration with data from QuickFS

Furthermore, Herbalife has also been struggling to make its revenue grow constantly, while its margins have been contracting in the previous four years.

Author’s Elaboration with data from QuickFS

The reasons behind the failure of most multilevel marketing companies are uncompetitive cost structure compared to large retailers, higher legal risk, and low-quality products compared to their prices.

First, Avon failed in the US because of the rapid growth of beauty retailers with affordable luxury brands, such as Ulta Beauty (ULTA) and Sephora, alongside non-specialty retailers incorporating beauty products to their shelves, according to Fortune. Furthermore, analyzing a comparison between Nu Skin’s cost structure and Ulta Beauty’s cost structure, made by Fernando Batista on Seeking Alpha, gives us a clear picture of how Ulta Beauty can generate, on average, more operating income per revenue than Nu Skin. Consequently, I think the disadvantage in the cost structure could explain why the margins started falling sharply in the previous three years, as consumers’ wallets were squeezed by the high inflation, generating a more conscious consumer; thus, from my point of view, Nu Skin is especially vulnerable to business cycles.

Second, multilevel marketing has been and probably will continue to be exposed to lawsuits, fines, and prohibitions in several world regions. For instance, due to restrictions, Nu Skin changed its business model from multilevel marketing to retail selling in China, after it paid $47 million. Additionally, in the US, we find several lawsuits against multilevel companies; for example, in 2019, many companies with the same business model were involved in legal problems; one of those companies was AdvoCare, which was banned from multilevel marketing and fined $150 million by the Federal Trade Commission. Furthermore, the FTC’s focus on policing inappropriate earnings claims and problematic compensation structures and ensuring consumer protection could easily translate into legal action against Nu Skin if its practices are deemed to violate evolving interpretations of direct selling and anti-pyramid laws. Examples abound: the FTC’s aggressive 2015 action against a multilevel marketing company and the 2019 case where a company was barred from using multilevel marketing model altogether highlight the potential consequences. Even seemingly minor infractions, like the FTC’s 2020-2022 warnings against COVID-19 product claims or misleading income opportunities, demonstrate the agency’s vigilance. The 2021 notice to Nu Skin and over 1,100 other companies, outlining specific practices deemed deceptive, further underscores the potential for significant civil penalties if FTC standards aren’t met. The 2022 ANPR indicating a potential rule on earnings claims and the 2023 successful lawsuit against illegal multi-level marketing programs solidify the FTC’s proactive stance.

Third, analyzing reviews from customers and dermatologists, Nu skin products don’t rank well compared to other competitors. In the case of dermatologists, the reviews on The Derm Review were negative, obtaining 3.3 out of 5 stars as Nu Skin products were significantly overpriced compared to competitors’ products with similar components. In the case of customers, I found mixed reviews, on Amazon, most of the products have more than 4 out of 5 stars, but on Consumer Affairs, the products only get 3.4 out of 5 stars, with a mode of 2 stars. Furthermore, on Trustpilot, they only get 3.1 out of 5 stars. I found on Consumer Affairs, Trustpilot, and Quora allegations about review manipulation by the company and those who sell the products; even if this information cannot be confirmed, the incentives are there; if a seller depends on selling Nu Skin products, she probably won’t give a bad review. Finally, many reviews I read complained about Nu Skin products being overpriced and low–quality.

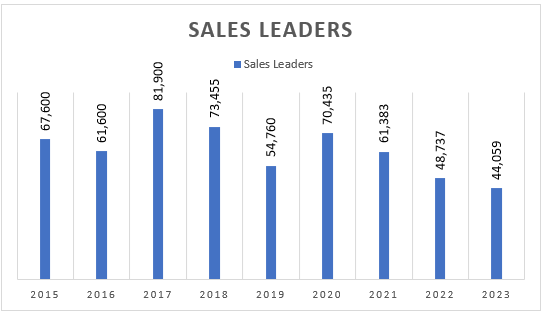

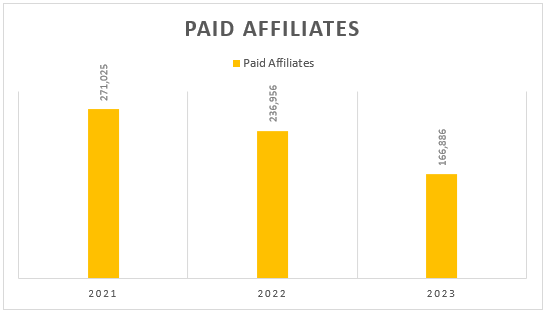

Following the disadvantages of multilevel marketing businesses, expecting a fall in this business model is plausible. Nu Skin has experienced fewer Sales Leaders and Paid Affiliates in previous years. Having fewer distributors will have a negative effect in the coming years.

Author’s Elaboration with data from Nu Skin’s 10K Reports Author’s Elaboration with data from Nu Skin’s 2023 10K Report

What to expect

Nu Skin has cut its dividend to $0.06 quarterly recently, and at the moment of writing this article, it has a forward dividend yield of 1.92% and a dividend payout ratio (based on 2023 free cash flow) of 19.72%. The reasons behind the cut are the management plan to attain the Nu Vision 2025 objectives, expand Rhyz business, and expand to India and the brain health market (according to its last earnings call). Nonetheless, except for Rhyz’s manufacturing capacities (which will produce other brands), all the other initiatives are related to the multilevel marketing strategy that is currently failing. From my perspective, the future doesn’t seem promising as the strategic plan doesn’t address the disadvantages of multilevel marketing and the price issues related to its products.

This capital allocation differs from other multilevel marketing companies, such as Herbalife and Tupperware. Herbalife has focused on being a cannibal in the last ten years, reducing its outstanding shares from 181.6 million shares to 100 million shares. Tupperware paid dividends and made stock repurchases before experiencing difficulties in 2019 and so on. Hence, it seems like Nu Skin is looking for opportunities that may not exist for multilevel marketing companies anymore instead of focusing on returning capital to its shareholders through share buybacks and dividends. However, expanding to a large market like India could keep the revenue from falling, as India’s growth offset the harmful effects of other markets. Furthermore, even if expanding to the brain health market could bring higher revenue, I doubt the success of these new products based on the bad reviews of the current products; therefore, I think they will have a low probability of success.

Nevertheless, I think the Rhyz bet in the manufacturing industry could save the company from a declining business model; however, it doesn’t mean that the company will begin to earn high returns if it shifts to a pure manufacturing player because it keeps being a highly competitive industry with low pricing power and significant capital investment. Nonetheless, the management expects Rhyz to be around 20-25% of sales by 2025. Therefore, Nu Skin will keep relying on a multilevel marketing strategy.

In this sense, the management expects a decrease in sales in 2024 of approximately 8.59% if we take the middle point of the guidance ($ 1.8 billion), which is also the analysts’ estimate. The decrease in revenue is expected even when the Rhyz business continues to show strong growth, with 41% growth in the whole year and 100% in 4Q23. Furthermore, the management expects Rhyz to grow at a double-digit rate in the following years. Consequently, the management is expected a decline in the revenue of its core business even if macroeconomic conditions are already improving.

On the other hand, the EPS in 2024 will be around $0.75 and $1.15, according to the guidance, while analysts expect it to be around $1; therefore, Nu Skin is trading at a FWD P/E of approximately 12.64, which I believe is a little demanding given the dire outlook the company is facing and the significant competitive disadvantages it has. Nevertheless, comparing it to its historical valuations, the company offers a discount, as the last five years’ median P/E has been 17.63; however, the financial performance of the company has deteriorated in the previous year, and it doesn’t seem to improve soon, so it may be too optimistic to think that the company will trade again at those multiples. Moreover, comparing Nu Skin with some competitors in the industry and some companies with the same business model, we find that companies like Ulta Beauty, L’Oreal (OTCPK:LRLCF), and Estee Lauder (EL) trade at high FWD P/E multiples of 20.58, 34.13, and 35.34, respectively. However, I don’t think this means that Nu Skin has a considerable discount, as the company also has significant competitive disadvantages that will impair its growth opportunities. Moreover, Nu Skin is trading at a premium compared to other multilevel marketing companies, as the FWD P/E of Herbalife and Tupperware are 3.8 and 6.56, respectively, and the P/E of Medifast is 4.44.

Lastly, I think the Rhyz business could save the company from the slow death of the multilevel marketing business, but the transition will be slow, according to management estimates.

Conclusion

From my perspective, Nu Skin is a ‘Sell.’ The company has severe competitive disadvantages that will probably impair its growth opportunities. The lack of competitive products, the non-competitive cost structure, and the high probability of lawsuits make Nu Skin stay behind the competition. Moreover, multilevel marketing seems to be declining, as companies like Herbalife, Medifast, Tupperware, and Nu Skin struggle to remain competitive in the market, while Avon already failed. Nevertheless, I think the Rhyz bet could move the company to another business model where it could earn better returns and keep growing. However, the transition will be slow to an already competitive market will be slow, so the returns may not be high and will take too much time to be significant. Finally, expanding to India and the brain health market could bring back revenue growth and improve the outlook when implemented.

Editor’s Note: This article covers one or more microcap stocks. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")