Jiojio/Moment via Getty Images

The thesis

NRG Energy (NYSE:NRG) looks well-positioned to continue to benefit from the record-breaking temperature in its core Texas market in peak seasons particularly, which is a key driver for energy demand. The contribution from the new Vivint business should also play a key role in NRG’s future growth with its leading technology platforms and innovative products which serve a large customer base across the country.

The company’s stock valuation is at a discount to historical level. The margins are also growing and should continue to grow with continuous operational improvement and mid-term goals of achieving cost savings across the business. I believe the company is at a decent valuation to consider investing in this for a longer term, which makes it a good buy.

Business overview

NRG Energy is a power company based in the U.S. that generates and sells energy and related products and services across North America. NRG primarily sells electricity and natural gas to residential, Commercial & Industrial, and wholesale customers under segments with a geographical focus. These segments are Texas, East, and West. The company has also acquired an additional category business, Vivint, a smart home platform company, which includes products and services like lighting, solar, security, protection plans, and energy management. NRG plays a pivotal role in the energy industry, providing retail and wholesale services, and is actively involved in innovation, technology, and customer-centric solutions to meet energy needs.

Last quarter performance

The company’s topline continues to decline for the straight third quarter. This was primarily due to lower revenue in the East and the West segment, which includes all activities related to customer plant and market operations in these regions. However, 17.4% YoY growth in the Texas segment, driven by record demand in the core Texas market, and additional revenue from the new Vivint Smart Home business partially offset the impact of the weak East and West segment, resulting in an overall topline contraction of 6.6% to $7.95 billion versus the prior-year quarter.

The margin on the other hand experienced exceptional growth and more than doubled versus the prior year quarter. The company reported an adjusted EBITDA margin of 12.2%, up from just 5.6% in Q3 2022. This margin expansion was primarily driven by strong operational performance and the addition of Vivint. Additionally, lower supply costs and improved plant performance on the Texas side were also the key drivers of margin expansion during the third quarter of 2023, which more than offset the negative impacts from lower margins, primarily in the west segment mainly due to lower spark spreads, a difference between the cost of natural gas and the price of the electricity generated from it.

Increased profits during the quarter also resulted in NRG’s free cash flow growth of $355 million for the quarter reaching a total of $983 million year to date, which has helped the company in making significant progress towards its target debt reduction of $1.4 billion, with $800 million achieved by end of Q3 2023.

Record demand in the core market

The energy industry is a cyclical business that generally tends to benefit from locations with extreme weather conditions, either summer or winter. The revenue of companies in this industry is primarily driven by the weather conditions in the region in which it operates and tends to be highest during extreme conditions, such as high demand and prices for electricity when there is extreme heat, and similar is the case for natural gas but generally in the winter season.

NRG is among the largest competitive energy retailers across the U.S. with recurring electricity and natural gas revenue across 24 U.S. states. The interesting part is that the company’s retail brands, collectively have the largest share of residential electric customers in the NRG’s core Texas market, which is also among the hottest regions in the U.S., making this region among the ones with the highest power demand.

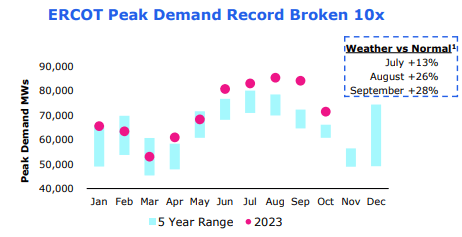

The company experienced the hottest summer on record in this region breaking the previous peak demand record 10 times, which is a positive factor for the company’s power sales in the coming years. Also, the average retail customer count has increased notably in the core Texas market to 2.96 million as of year-end 2022, which is approximately 21.8% higher than what it was in year-end 2020.

Peak demand in MWh (NRG presentation)

In my opinion, as long as the company is able to handle peaking energy requirements during the extreme seasons, either through self-generation or via external plants, the demand should remain healthy for the company resulting in topline expansion in the years ahead.

Vivint contribution

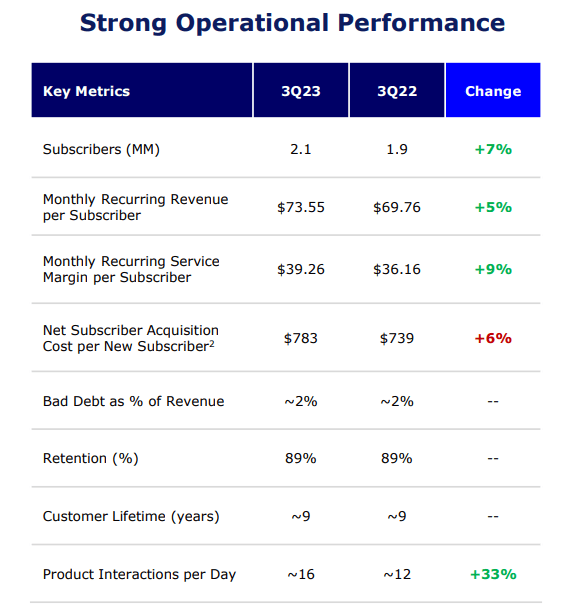

Acquired in 2022, NRG’s new segment, Vivint smart homers, has already started contributing significantly to NRG’s business reaching 6% of the company’s total revenue in Q3 2023. Also, the additional margin contribution by this new category was also significant, with $225 million in EBITDA in Q3 2023, which is about a quarter, or to be precise, 23.1% of NRG’s total EBITDA in the third quarter of 2023.

Vivint’s attractive home business, which includes products and services like lighting, solar, security, protection plans, and energy management, has been able to achieve a customer retention level near 89% so far, through its industry-leading brand loyalty, which indicates towards segment’s market strength strengthening the market position for future growth.

Vivint operational performance (NRG investor presentation)

The segment has launched its new indoor camera and smart indoor lighting solutions. Also, the company continues to focus on the advancement of its technology platforms by launching new innovative products with a goal of increasing product per share while decreasing the cost to serve. The Smart home segment has a total accessible market of $35 billion, which also provides a big room for growth opportunities for this segment as it continues to execute on strategy of product innovation to acquire new customers, benefiting the company’s revenue in the longer term. Additionally, the company’s leading technology platforms, high customer engagement, large coverage across the U.S., and complementary sales channels should act as key drivers in the company’s journey of gaining market share in this large market in the coming years. Overall, I am very optimistic about the segment’s future growth prospects and its contribution to NRG.

Margin expansion

Considering the strong position of NRG in the core Texas market and new fast-growing high-margin business, Vivint Smart Home, the company’s guidance for total EBITDA for FY23 has been revised to the north. The company is seeing the EBITDA for FY 2023 in the range of $3.15B – $3.3B, which looks quite achievable to me as the company’s diversified supply strategy and solid plant performance continue to provide predictable supply costs through volatile load and price conditions in Texas.

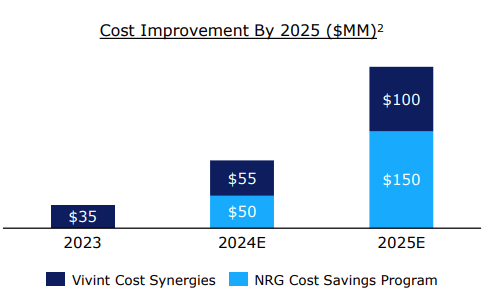

Additionally, the company also continues to execute its portfolio optimization efforts, as part of which NRG has already retired Joliet power station and also sold Gregory and its interest in STP. The company is also targeting $250 million in cost savings by 2025, $100 million in Vivint as part of overhead and operational efficiencies, and $250 million in the core NRG business, which should further support the company’s margin expansion in the coming years

Cost savings target (NRG company presentation)

Valuation

Currently, the NTR’s stock is trading at a forward P/E ratio of 7.76 times its 2024 EPS estimates of $6.92, which is at a discount to its five-year average of 8.87. While compared to its sector median, the stock looks even more attractive, at a discount of approximately 50% from 16.06 times.

The top line is expected to be on the lower side in the near term due to the non-peak season, however, the company’s long-term prospects remain favorable, and the revenue should grow in the coming years, particularly with the help of NRG’s leading position in Texas and contribution from Vivint in the longer term. I am also expecting margin expansion in the coming years which should lead to an even more reasonable valuation in the coming years.

Risk

The company’s overall margin has been in the mid-single digits throughout 2022. However, since the addition of Vivint Smart Homes, the company’s overall profitability has improved notably. But, the margins of the East/West segment combined still appear to be struggling when compared with the prior year quarters.

My thesis is built upon the consideration that the company’s overall margin should continue to get support from strong Texas core market as well as additional margin from the Vivint category. However, the only thing that concerns me is, that if the Vivint acquisition does not end up delivering as per expectation, the company’s profitability might be negatively impacted which can potentially impact the stock’s valuation.

Conclusion

As discussed earlier, the company’s stock is at a discounted valuation based on 2024 estimates when compared to its historical levels. In my opinion, the company should benefit from its leading position in certain markets. Also, the contribution from the new Vivint acquisition in terms of new innovative products and amazing customer retention should help the company in gaining market share in the future. The margin of the company profile also looks promising. Due to these reasons, I am optimistic about the company’s future prospects, which makes me recommend a buy rating on the stock.

Q2 2024 Earnings Call Transcript")