Jonathan Kitchen

Written by Nick Ackerman, co-produced by Stanford Chemist.

Nuveen Core Plus Impact Fund (NYSE:NPCT) provides investors with exposure to a diversified portfolio of mostly fixed-income investments. Since launching in 2021, the closed-end fund has been trading at a substantial discount to its net asset value per share.

That isn’t too unheard of for CEFs or for new funds either. The current discount level is about where it has been trading for the last couple of years now. With that being said, it is another target for the activist firm Saba Capital Management.

NPCT Basics

- 1-Year Z-score: 0.64

- Discount: -13.53%

- Distribution Yield: 11.01%

- Expense Ratio: 1.75%

- Leverage: 35.67%

- Managed Assets: $536.4 million

- Structure: Term (anticipated liquidation date of May 2, 2033)

NPCT seeks “total return through high current income and capital appreciation, investing primarily in fixed income investments while giving special considerations to certain impact and environment, social and governance (“ESG”) criteria.”

The ESG tilt is one offsetting factor for this fund compared to other fixed-income options. I’ve never been personally concerned with investing with this as a consideration, but it is something others value. Having the option out there helps those investors, and it doesn’t hurt.

With that said, they also provide that the fund “may invest up to 50% of Managed Assets in below investment-grade investments, but no more than 10% investments rated CCC or lower at the time of investment.” They also provide that there is no limit on investments in international markets outside of the U.S., but do have a stipulation that “no more than 30% of Managed Assets in investments of foreign issuers located in emerging market countries.”

Limited Term Structure

This fund was also launched after 2018, and like most publicly traded closed-end funds doing so during this time, it comes with a term structure. In this case, it was a 12-year term, but they also left the door open for potentially going perpetual or seeing this extended. This is also a common feature with CEF 2.0s, but this is the first time I’m covering this fund, so I try to lay out further details.

The specifics for this fund are that the Board can extend it for “up to two one-year periods.”

Going perpetual would be done after conducting a tender offer to investors. This would be done 18 months preceding the termination date and is in high likelihood, should the fund survive for 12 years, go through this process. Nuveen has generally proposed these tender offers with their other limited-term CEFs, which is understandable as they are managing fee-generating assets.

The tender offer would be for 100% of outstanding shares at 100% of the NAV at the time of the expiration of the tender offer. If a minimum level of net assets is left over after the eligible tender offer is reached, the fund could choose to change the structure to a perpetual one.

Most funds had previously listed a specific net asset value threshold, such as $100 million or $200 million. NPCT has left flexibility in determining what it believes would provide for “continued viability,” which would be determined by “prevailing market conditions at the time.”

In other term funds, we’ve also seen them ask shareholders to approve going perpetual before conducting any tender offer. That was the case with Western Asset Mortgage Opportunity Fund (DMO) and much more recently with XAI Octagon Floating Rate & Alternative Income Trust (XFLT). So, that seems to remain an option as well, but a major difference was that those funds sported premium for a considerable period of time. At least, DMO, at one point, had traded at a persistent premium for a period of time before removing the term structure and now trades at a discount regularly.

Activist Pressure And Discounts

Similar to our very recent discussion on BlackRock Capital Allocation Term Trust (BCAT), Saba is looking to get representation on the Board of NPCT. Also, Nuveen, similar to BlackRock, is trying to provide key highlights on why investors should disregard Saba’s proxy and vote on their proxy instead. The primary selling point appears to be that the three independent Board members already with the fund have decades of “public company experience.”

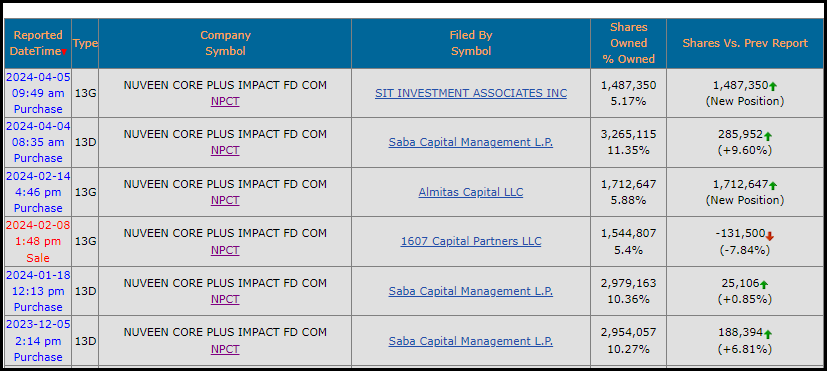

Saba owns 11.35% of the fund. That ownership is a smaller position compared to the position they hold in BCAT, but another activist also recently took a position in the fund. SIT Investment Associates has started a position at just over 5% of the outstanding shares that would likely vote in favor of any Saba proposal.

NPCT Fund Ownership (SecForm4)

If Saba gets representation on the Board of the fund, it can make it easier to ‘negotiate’ in ways to reduce the fund’s discount.

That could be by conducting a tender offer, conversion to an open-ended fund or liquidation. In any of those moves, the fund’s investors would be able to realize a portion or the entire discount of the CEF.

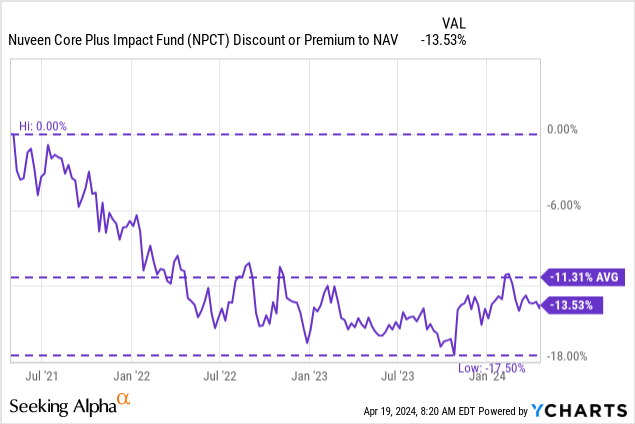

The fund began trading at a wider discount nearly immediately, and that isn’t all that unusual for new CEFs. Since then, it has fluctuated between -17% and roughly -10 %.

We are currently at a level where there is plenty of opportunity for discounts to be realized, but it would require a potential catalyst. Outside of that, the current discount level looks fairly appealing, but not a screaming ‘Buy’ here.

YCharts

Distribution Looking Stretched

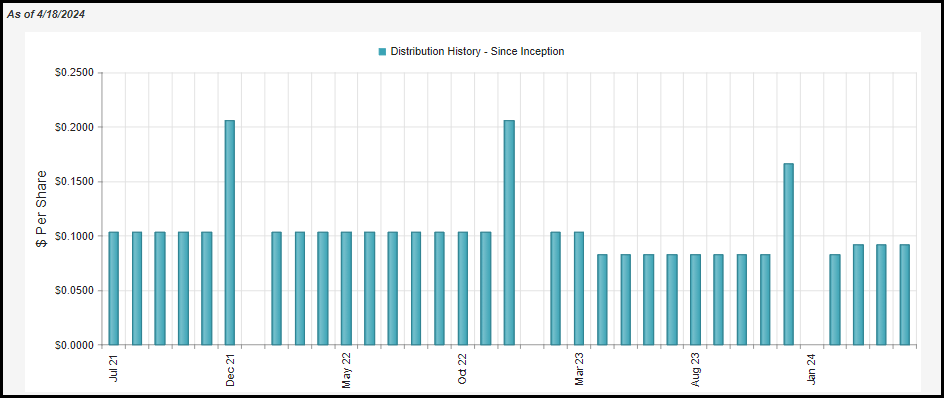

Another one of those ways to potentially reduce the fund’s discount would be to increase the distribution even further than they had already bumped it up heading into 2024. That said, this was a reduction from the distribution the fund was paying at launch.

NPCT Distribution History (CEFConnect)

With an NAV distribution rate of around 9.5% already, we are most likely looking at an elevated yield here. The chances of the fund earning this, as well as covering its operating expenses, are fairly low.

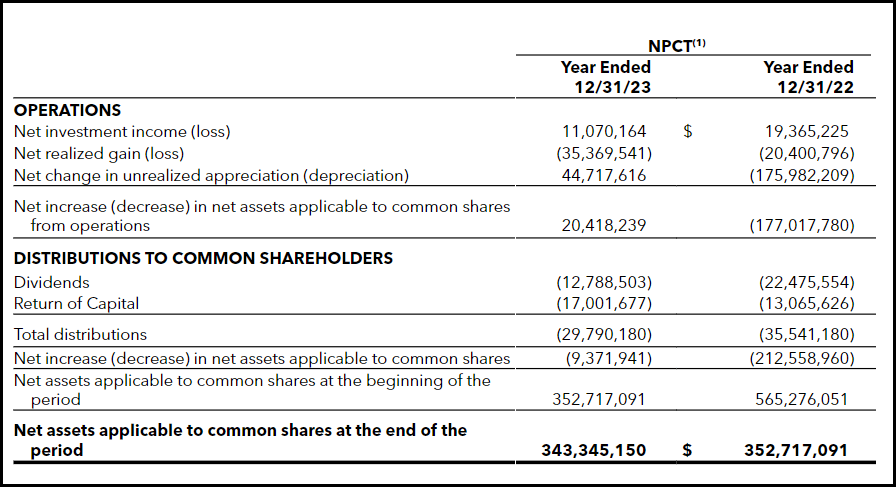

Of course, that doesn’t mean that the fund can’t provide a decent total return in the future, but I expect that it is likely to see the NAV erode over time. As we can see in the prior annual report for 2023, the fund’s NII coverage came to about 37%.

NPCT Annual Report (Nuveen)

For a primarily fixed-income focused fund, we’d like to see this at closer to 100% and ideally over 100%. On a brighter note, thanks to the fund’s large discount, the distribution yield on the share price is more elevated at ~11%.

Given the increased distribution for this year, the NII coverage is likely to head lower for 2024 as well. One thing this fund would certainly benefit from would be a reduction in the Fed’s target rate, but as that gets pushed back further and further, the higher rate headwinds the fund faces continue.

The fund listed interest rate swaps that are helping to protect the fund’s leverage costs to some degree. However, at the end of 2023, the average notional amount of swap contracts outstanding was $36.453 million. Those helped to appreciate through 2023 with a net unrealized appreciation of $3.18 million.

That’s good news, but one problem is that the fund has much heftier borrowings, on which it is currently paying over 6% rates.

NPCT Leverage Stats (Nuveen)

The above is a consolidated view of all their leverage, but they actually utilize borrowings, reverse repos and variable-rate preferred. All of these are negatively impacted by higher short-term rates, leading to higher borrowing costs for the fund.

To put this in another perspective, the fund’s interest expense for 2022 came to $5.601 million, while it ballooned to $12.766 million this year. That’s why we saw the fund’s total expense ratio go from 2.95% to 5.50% by the end of 2023.

With that, the fund is definitely positioned for a lower-rate environment, and that doesn’t appear to be happening, at least in the near term. When it does, NPCT could be in a much better position with any decrease in short-term rates easing up pressures on its borrowings. It would also likely see some appreciation in its underlying portfolio, which could further help support the distribution.

For tax purposes, we see quite a bit of return of capital, which isn’t surprising given the coverage discussion we just outlined. For 2022, this would be an entirely destructive ROC. While 2023 saw a significant improvement in total NAV returns, there was still some destructive ROC there, too.

NPCT Distribution Tax Classification (Nuveen (highlights from author))

NPCT’s Portfolio

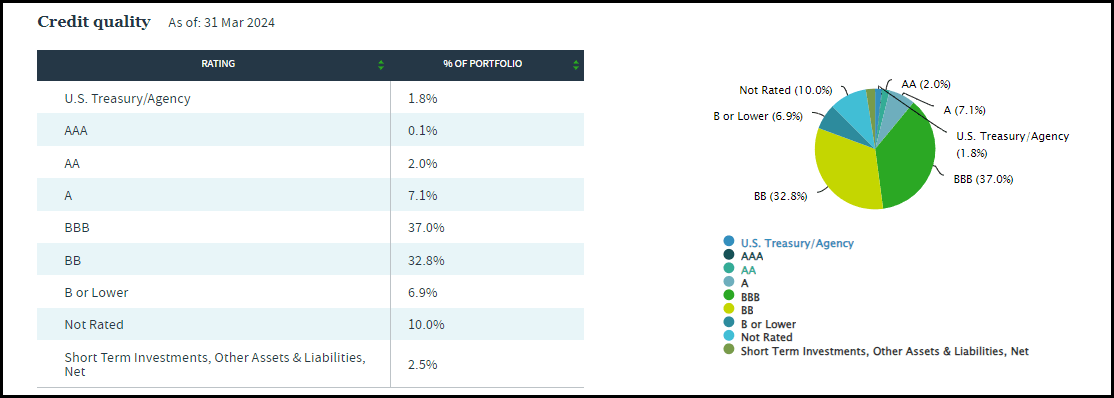

In looking at the fund’s portfolio, they list 134 total holdings with an average leverage-adjusted effective duration of 9.85 years. That is quite high and tells us that NPCT’s portfolio is quite interest rate-sensitive. This is in large part due to the higher quality portfolio tilt that it comes with. A meaningful 48% of the fund is invested in investment-grade debt of BBB or higher.

NPCT Portfolio Credit Quality (Nuveen)

That said, that duration is even higher than the Western Asset Investment Grade Income Fund (PAI), which is almost entirely investment-grade rated holdings and carries an effective duration of 7.14 years. Of course, PAI is also not a leveraged fund, and NPCT’s metric specifically provides the “leverage-adjusted” stat.

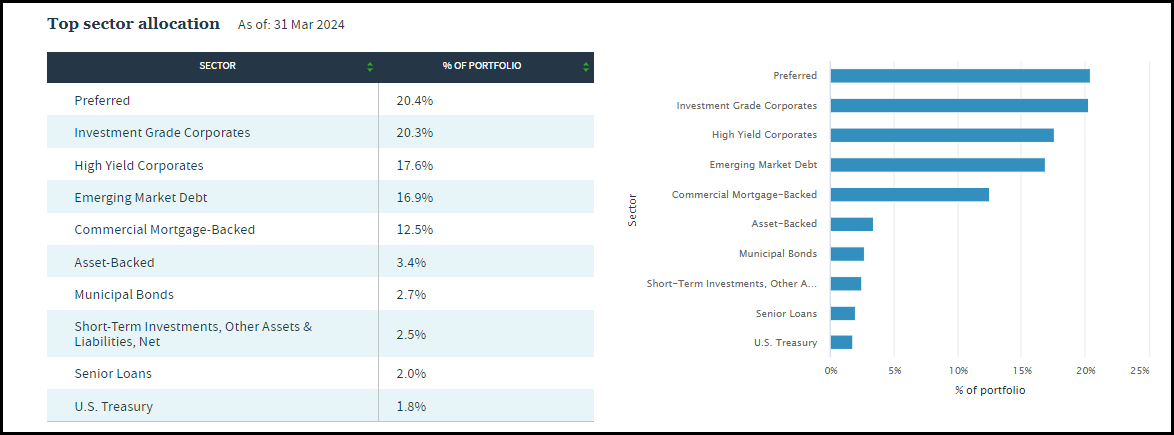

Diving into the portfolio further, we can see that preferreds hold the highest allocation but that only slightly edges out the investment-grade corporate sector sleeve.

NPCT Asset Breakdown (Nuveen)

We then have the high-yield corporates, emerging market debt and commercial MBS sector allocations, which are the spicier parts of the portfolio where the fund gets a yield lift.

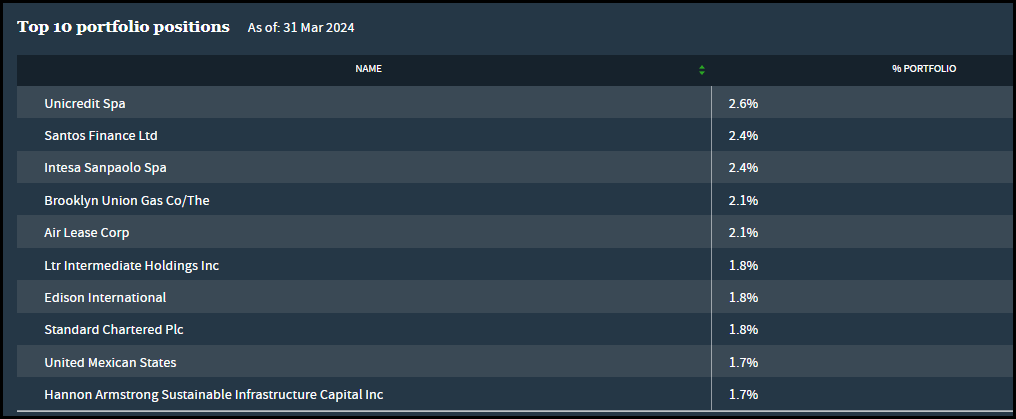

Turning toward the top 10 positions in the fund, we can see that none command an overly large allocation to the fund. That gives us better diversification in terms of not allowing just a handful of positions to really move this fund negatively.

NPCT Top Ten Holdings (Nuveen)

Of course, the reverse is also true; more diversification also means that any significantly positive performance in one position is also drowned out. Since we are primarily looking at fixed-income investments, the upside would generally be more limited compared to equities. One is merely making a bet that the company won’t default or go into bankruptcy. Even if that happens, there is generally some recovery from such events anyway, so it isn’t a complete wipeout.

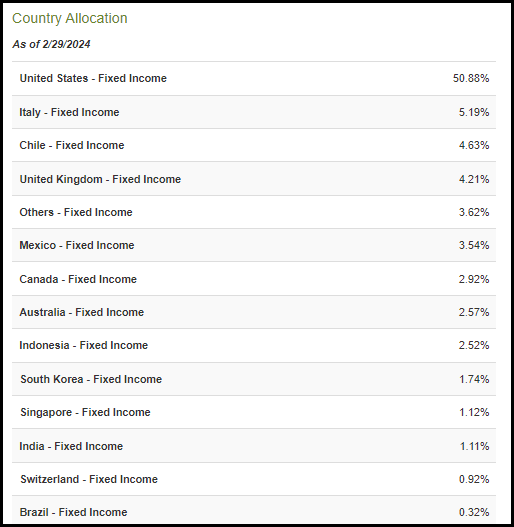

In looking at this fund, Nuveen doesn’t appear to have provided a geographic or “top countries” exposure list like they often provide for a number of their other funds. That said, it could be a fair amount because most of the top holdings aren’t headquartered in the U.S. – only Air Lease Corp (AL), Edison International (EIX) and Hannon Armstrong Sustainable Infrastructure Capital, Inc. (HASI) are U.S.-headquartered. There is also LTR Intermediate Holdings Inc., but that isn’t a publicly traded company.

Brooklyn Union Gas Co. also operates in the U.S., but it’s like a Russian doll with several layers. The parent company is National Grid USA, whose parent company is National Grid North America Inc., and whose parent company is National Grid (NGG), which is based out of England.

Given this sampling is just the tip of the iceberg and, therefore, possibly misleading, it seems to suggest that a significant portion of this fund is invested globally outside of the U.S. For holding information, I generally avoid looking at CEFConnect data as it is usually inaccurate. However, in this case, it also seems to tilt toward suggesting the fund has a heavy allocation to geographic regions outside of the U.S., with only about 50% listed as U.S. fixed-income.

NPCT Country Allocation (CEFConnect)

Conclusion

NPCT provides investors with a diversified pool of fixed-income exposure. It comes with an elevated leverage-adjusted duration, which means it is highly susceptible to interest rates and the direction in which yields move. Given the relatively limited hedging in place based on the effective leverage the fund is utilizing, they also stand to benefit from lower rates from the Fed in that way, too. If one believes that rates will eventually come down and if risk-free yields also follow lower, and they are expected to at some point, this could be one to play a significant rebound.

At the same time, the fund is under activist pressure from Saba, which is a potential main catalyst and one that could have a meaningful impact if they get representation on the Board of this fund. Given the current discount, the fund appears to be a ‘Hold,’ but this activist push certainly could make it a more exciting proposition.

Q2 2024 Earnings Call Transcript")