4FR

Investment Thesis

Norfolk Southern (NYSE:NSC) had a tough start to FY24 with their most recent Q1 results seeing the railroad generate lacklustre returns from their operations.

While significant one-off costs associated with the mediation for a derailment that occurred in 2023 placed a real damper on net income, Norfolk also struggled to control operating costs all the while revenues contracted slightly YoY.

This has degraded the value proposition of the railroad’s stock with shares currently trading at essentially a fair valuation according to my intrinsic value calculation.

Still, I believe the company is well positioned to generate great long-term returns for shareholders thanks to their moaty business and focus on operational excellence.

I therefore rate NSC stock a Hold at present time and cannot present a stronger buy-oriented thesis without a larger margin of safety with regards to the share price.

I continue to hold my significant position in the stock.

Company Background

Norfolk Southern is one of six Class I railroad operators in the U.S. Over the last couple decades, the railroad has emerged as one of the few industry leaders alongside the likes of Warren Buffett’s BNSF, Union Pacific (UNP) and CSX (CSX).

The railroad hauls a variety of cargo including intermodal freight, coal, automobiles, chemicals along with forestry and agricultural products – just to name a few commodities.

Furthermore, the inherent nature of owning over 20,000 route miles of track servicing essentially every corner of the eastern United States generates significant moatiness for Norfolk’s business operations.

While competition with the likes of Union Pacific and BNSF is fierce, rail transport still enjoys tangible cost advantages over road or air-based alternatives, at least at present time.

When combined with their massive network of rails and absolute importance to the daily functioning of the U.S. economy, I still believe Norfolk enjoys a wide economic moat rating.

I recommend reading my previous deep dive article, “Norfolk Southern: All Aboard This Buy-And-Hold Freight Train”, to gain a more in-depth analysis into Norfolk Southern’s business and economic moat.

Fiscal Profile – Q1 FY24 Analysis

The most recent first quarter of 2024 saw Norfolk present a less than stellar set of fiscal results with a worsened revenue mix and little improvement in adjusted operating ratios.

NSC FY24 Q1 10-Q

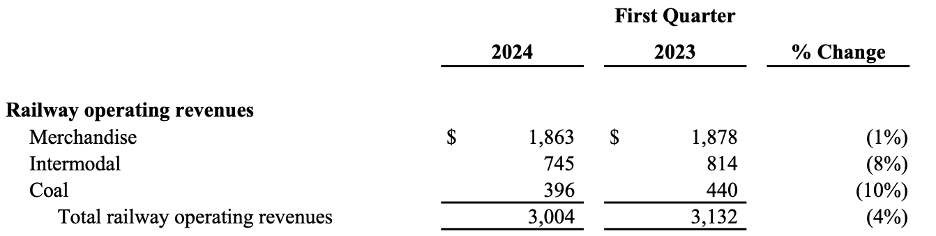

Headline railroad operating revenues of $3.0 billion represent a 4% contraction YoY. These flat line revenues came as a result of a macro shift in demand for railroad transport which skewed Norfolk’s revenue mix towards lower-margin traffic.

Coal and Intermodal revenues fell 8% and 10% respectively as a result of a softer demand environment with a surprising resilience in merchandise demand limiting the segments revenue contraction to just 1%.

NSC FY24 Q1 10-Q

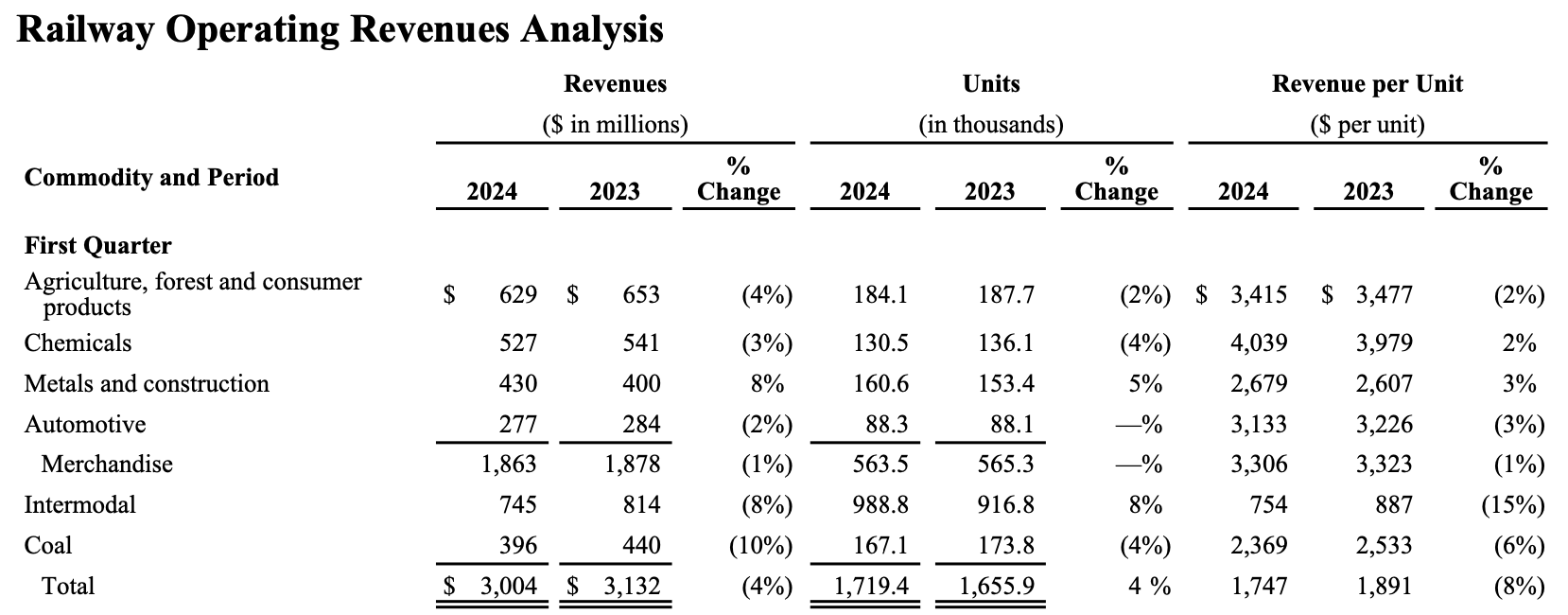

The skew towards a less favourable mix of revenues occurred specifically as a result of decreased transport of agricultural, forest and consumer products along with a similar contraction in chemicals transport. These two commodity groups tend to produce the largest unit revenues for the firm.

While these figures are disappointing, I am not alarmed. The U.S. economy has shown remarkable resilience over the past two years despite a higher interest rate environment. I believe that the consequences of an increasing stagflationary macro backdrop appear to finally be biting the supply side economy.

NSC FY24 Q1 10-Q

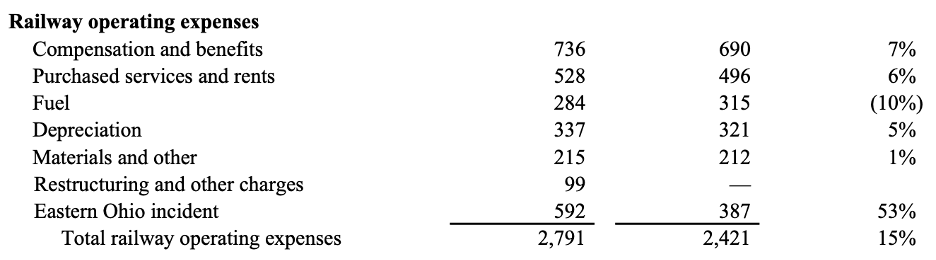

Norfolk also had a tricky quarter from a cost perspective, particularly as a result of supply side inflation pressures and ongoing costs related to the East Palestine derailment.

Total operating expenses increased 15% YoY on a GAAP basis primarily because of the $592 million in costs associated with the management of their derailment back in 2023.

Wage expenses grew 7% while purchased services and rent costs increased 6% YoY, highlighting the challenges supply side inflationary pressures present Norfolk Southern.

Fuel associated costs decreased sharply YoY by 10% as a result of positive commodity price changes with the average purchased price per gallon of diesel decreasing from $3.088 to just $2.724.

Still, as a result of the significant increase in railroading expenses, Norfolk’s income from operations decreased a whopping 70% with net income falling an even greater 89% YoY as a result of increased interest expenses on debt.

The railroad’s operating ratio accordingly expanded to a very poor 92.9% against a wonderful Q1 FY23 ratio of just 64.9%.

On a non-GAAP adjusted basis (primarily removing the one-off nature of derailment related costs), Norfolk’s Q1 looks a little more positive with an operating ratio of 69.9% yielding net income of $565 million (down 25% YoY).

While the GAAP standards certainly do no favours for Norfolk’s Q1 results, I think it is important to remember that the costs incurred by the firm are real. Nevertheless, the non-GAAP figures suggest that the underlying business at Norfolk remains undamaged with the current headwinds being transitory in nature.

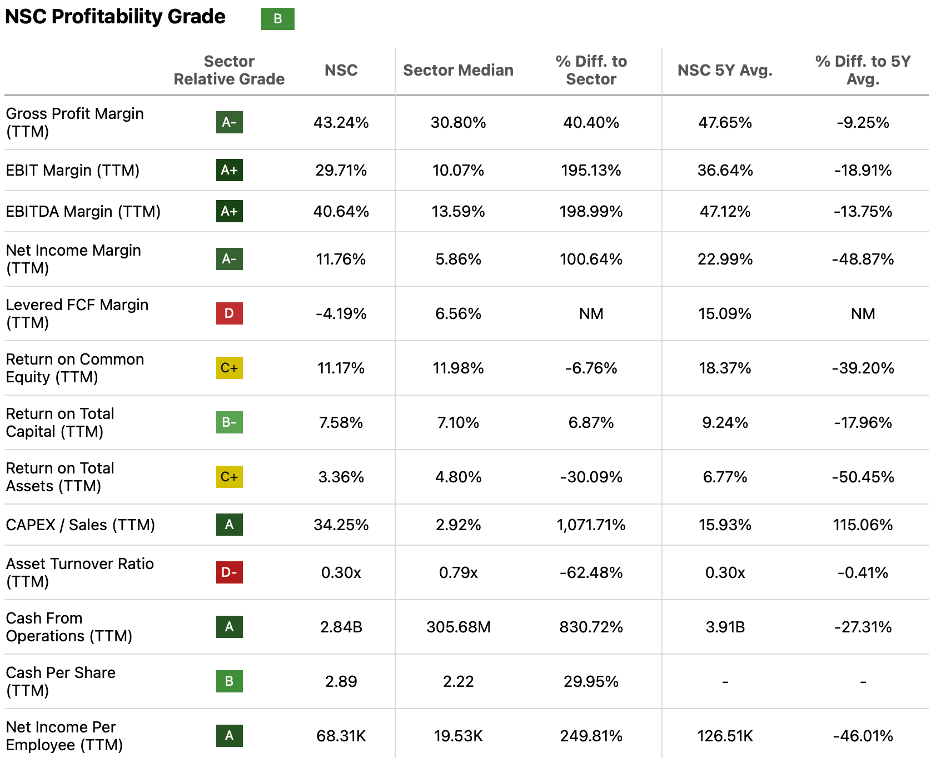

Seeking Alpha | NSC | Profitability

Seeking Alpha’s Quant had downgraded Norfolk’s profitability rating from an “A” back in November 2023 to a “B” at the present time. While I do not think the firm’s underlying profitability has suffered any irreparable damage, Norfolk is certainly facing some real challenges at the present time.

From an asset allocation perspective, Norfolk Southern remains well capitalised with a relatively strong balance sheet. Total current assets have decreased to just $2.36 billion as a result of a sharp drop in cash required in the financing of the derailment costs.

Current liabilities of $3.45 billion leave the firm with a worsened short-term liquidity outlook, with Norfolk sporting a quick ratio of 0.54x and a current ratio of 0.70x.

While these are much lower than in November 2023, they are still largely in line with my expectations for Class I railroads.

Norfolk Southern continues to operate with a financial leverage ratio around 3x, with the most recent quarter suggesting 3.3x leverage. I find this to be an acceptable level, although I would appreciate a drop back towards the 2.5x region in the coming decade.

Moody’s continues to provide an LT issuer credit rating of “Baa1” for Norfolk Southern, along with an unchanged “Baa1” rating for their unsecured domestic notes. The outlook remains stable. Ratings defined as “Baa1” are considered to be of “medium investment grade”.

Overall, the Q1 FY24 results illustrate the struggles Norfolk is currently facing with regards to their operations. While the lack of revenue growth is mostly explained by external factors, it is undeniable that the costs associated with the derailment remediation are taking a toll on overall profitability.

I continue to be realistic about the situation and while I consider the short-term headwinds to be a real challenge, I still like the overall fiscal profile present at Norfolk Southern.

Accordingly, I am forecasting a 6-10% long-term (5-20 year) revenue growth per annum rate at Norfolk Southern and base this estimate in line with their historic 20-year average. This is supported by analyst expectations on Seeking Alpha’s earnings estimates tab for NSC.

Valuation

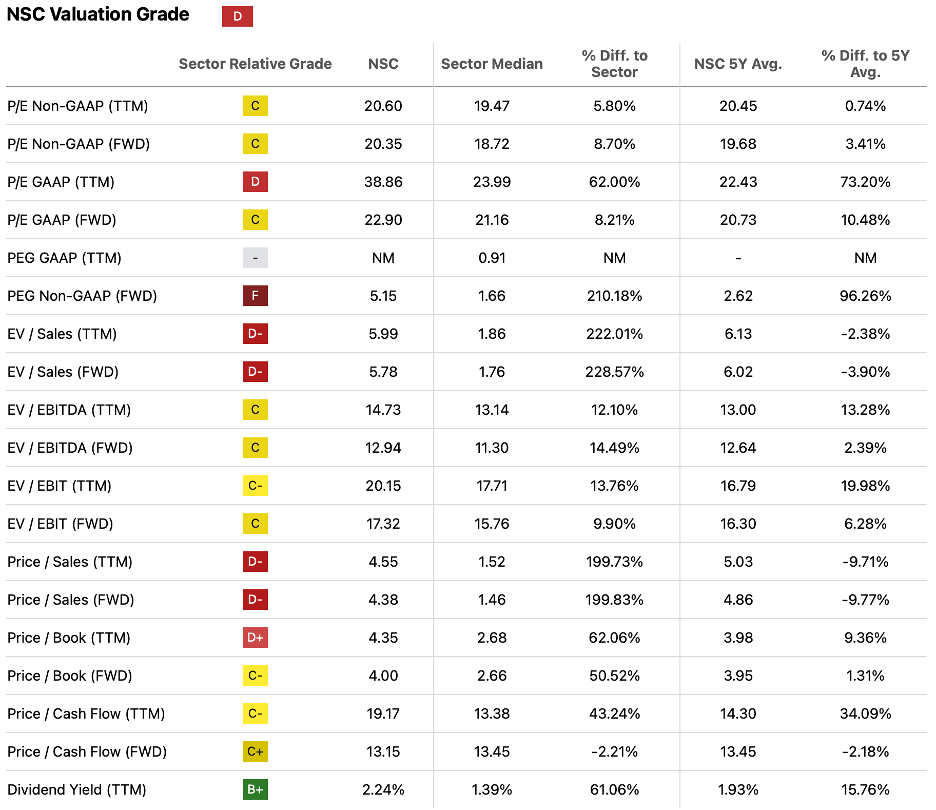

Seeking Alpha | NSC | Valuation

Seeking Alpha’s Quant continues to assign a “D” valuation rating for NSC shares. I consider this letter grade to be a slightly pessimistic illustration of the value present in the railroad’s stock, as it suggests shares may be materially overvalued. I believe shares are fairly valued at the present time.

Looking at the individual metrics, the current GAAP P/E FWD of 22.90x is reasonable for the railroad and has been appreciated in recent times due to the decrease in profitability present at Norfolk Southern.

The price/sales TTM of 4.55x is also quite reasonable in my opinion, given how stable and predictable revenues traditionally are for class I railroads.

While price/cash flow FWD is quite elevated at 13.15x for my liking, I do believe this ratio should improve as Norfolk regains their stride and continues growing both top and bottom-line results.

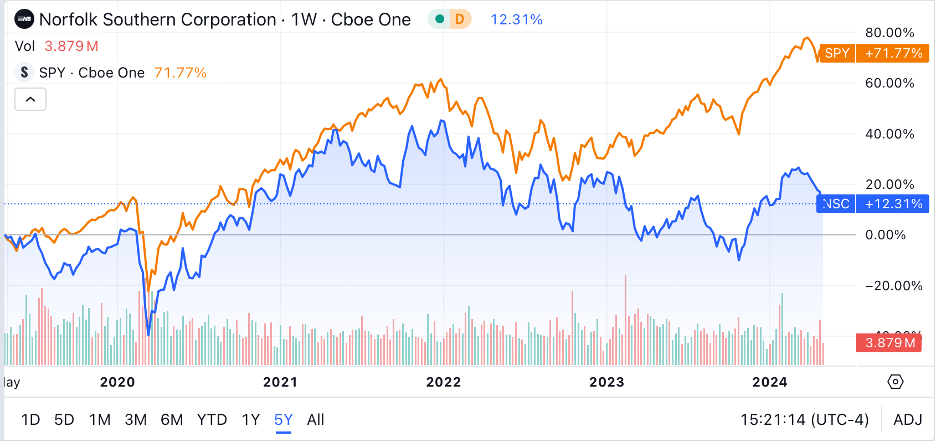

Seeking Alpha | NSC | 5Y Advanced Chart

The last five years have seen quite a bumpy ride for NSC stock. Since a post-2020 COVID boom, shares have largely traded sideways, with some downwards momentum arising a result of correcting market forces reducing the firm’s excessive peak valuation.

It is important to note that NSC stock has been outperformed by almost 60% over the last five years by the popular S&P 500 tracking SPY (SPY) index fund.

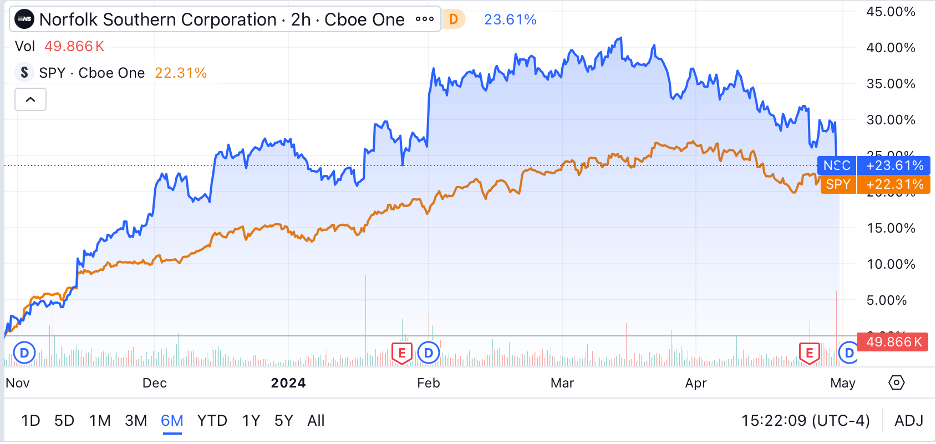

Seeking Alpha | NSC | 6M Advanced Chart

The last six months show a very different story for NSC stock. A strong rebound after a slump caused by the East Ohio derailment in 2023 has seen shares largely outperform the S&P 500 index, with a recent selloff resulting in a huge 23% appreciation.

Still, the stock has proven to be quite volatile with a beta ratio of 1.29x, which to me suggests investors hold some uncertainty over the future direction of shares.

The Value Corner

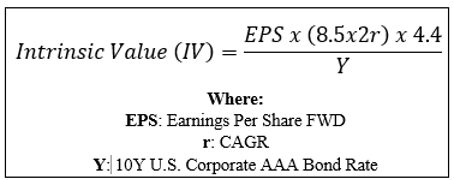

The Value Corner’s Intrinsic Valuation Calculation can allow us to better understand what value exists in the stock from a quantitative perspective.

Using the firm’s current share price of $229.63, an analyst average estimated 2024 EPS of $11.95, a realistic “r” value of 0.07 (7%) and the current Moody’s Seasoned AAA Corporate Bond Yield ratio of 5.01x, I derive a base-case IV of $236.10. This essentially represents a fair valuation at the present time.

A more pessimistic CAGR value for r of 0.05 (5%) can be used to model a more pessimistic recessionary scenario where U.S. business activity falls tangibly. In such an outcome, shares are still valued at around $194.20 representing an 18% overvaluation relative to present prices.

The spread between my base and bear case outcome illustrates just how much growth is still being incorporated into the current valuation. While this is traditionally the case for stable income producing businesses such as railroads, the recent shortfall in profitability at Norfolk exacerbates the potential for investor concern regarding the valuation.

This means that in the short-term (1-12 months), essentially anything could happen to the stock price. Recent underperformance in the latest Q1 results may indeed place some downward pressure on shares as some investors could lose confidence in the railroad.

In the long-term (2-10 years), I still believe Norfolk is well positioned to continue benefitting from their fundamentally moaty business operations. The railroad remains fundamentally solid, with a focus on efficiency and operational excellence at the forefront of their strategy.

Norfolk Southern Risk Profile

Norfolk faces some real risks with market cyclicality, operational safety issues and competitive pressures being the key threats.

Given that Norfolk has become an essential element of the U.S. economy, it goes without saying that the firm’s overall profitability and revenue growth trajectory relies on a strong and prospering domestic economy.

A recessionary environment present perhaps the gravest cyclical threat to Norfolk, as the slowdown in business activity in the U.S. economy would almost certainly reduce the demand for rail freight transport.

A continuation of the troubles Norfolk has for safety with regards to railroading safety could also present a real challenge for the firm. The East Palestine derailment illustrated just how costly the remediation of such an event can be, with some real damage being done to the Norfolk name as a result.

I believe Norfolk must focus relentlessly on improving the safety of their operations so as to safeguard against any future incidents which could do irreparable reputational damage, not to mention the significant fiscal costs of such an event.

Finally, Norfolk faces an acute competitive threat from the other Class I railroads as well as road transport solutions. Recent strides made in profitability by both Union Pacific, CSX and BNSF have only amplified the relative weakness present at Norfolk Southern.

Furthermore, governance changes with regards to crewing of locomotives could result in two drivers being required instead of one.

This may erode some of the advantage railroads have over the trucking industry, which could slightly impact overall growth estimates for the sector.

From an ESG perspective, Norfolk Southern faces some social and environmental threats at present time. The derailment has resulted in the railroad facing some backlash over the incident, particularly with regards to the toxic spillage that occurred as a result of the incident.

Nevertheless, I find these ESG risks to be of an acute nature rather than a systemic long-term set of threats.

Overall, I rate Norfolk as currently having a medium risk profile, with some uncertainty arising from the ongoing mediation of the derailment. Without these concerns, I would happily rate the railroad as having a low risk profile, given the predominant cyclical and competitive pressures.

Matters of risk analysis and evaluation are inherently subjective, and I therefore strongly suggest you carry out your own research into these matters should they be of any concern to you.

Summary

It is undeniable that Norfolk Southern is facing some real headwinds at the present time which require their immediate and complete attention.

Nevertheless, I still think the company is both metaphorically and hopefully literally on the right tracks, with operational excellence still at the forefront of their strategy.

The current valuation is fair in my opinion, which leaves little room for a value-oriented investor to get involved at the present time due to the lack of a margin of safety. The potential for an overvaluation in shares is also real should a recessionary market environment materialise in the U.S. economy.

I therefore rate Norfolk Southern shares a Hold at present time. I continue to hold my NSC shares and opportunistically look for around a 15% undervaluation as an opportunity to potentially evaluate expanding my position further.

Q2 2024 Earnings Call Transcript")