Hispanolistic

Here at the Lab, given our investment in Aegon, we usually check the Benelux insurers, and we believe the sector is inexpensive. In aggregate, the companies trade on >6x 2024 estimated P/E, and we believe they are set to outperform in an environment of declining bond yields, attractive balance sheets given solid Solvency II capital position, strong capital return, and limited sensitivity to low asset risk and yields. Last week, NN Group N.V. (OTCPK:NNGPF) (OTCPK:NNGRY) released an update on the settlement with the collective groups related to the unit-linked mis-selling claims. This removed a significant overhang for the company. It is positive on the dividend, and we believe the company’s re-rating is set to continue. On our estimates, NN Group trades at a lower valuation than its peers at 5.8x P/E.

Before you comment on the 2024 expectation, it is essential to look at the latest communication. After the market closed on 9 January, the company settled legal cases with interest groups concerning the mis-selling of life unit-linked policies, which took place 20 years ago. The company’s pre-tax total cost is set at €300 million with an extra provision for hardship cases of €60 million. Although we still have to wait for the formal approval of the policyholders, we believe this communication has almost lifted the liability uncertainty. In our previous estimates, we anticipated a negative one-off of more than +€500 million. The press release shows that NN Group had already injected €1 billion into NN Life to cover the provision. That said, the company has fully recovered since the court ruling back in September. Despite that, we believe investors might now focus on what’s next.

Why are we positive?

- (Further enhance capital distribution). With the final settlement announcement, NN Group also stated that it has a cash capital position at the end of December 2023 of approximately €1 billion. As a result, the company plans to increase its dividend per share by a double-digit percentage from its 2022 payment. In our estimates, we increase our dividend projection by 10%. This represents a DPS of €3.07 and is a new base for the NN dividend growth story. In addition, the company also confirmed its capital management with an annual buyback of €250 million. In the case of M&A opportunities, these additional excess capital returns might be used for value-creating opportunities. Here at the Lab, we now believe that NN Group is a dividend player with good visibility going forward. We forecast a DPS CAGR of 8% by 2025, and this will lead to a continued re-rating of the share;

- (Higher ROE asset optionalities). We believe the company’s €1 billion capital injection into NN Life will help fund future growth. The above pre-tax settlement cost offsets this, but there are now options. Although we forecast a dilution to the solvency due to wider mortgage spreads, we anticipate NN to reinvest most of this capital in a higher return on equity assets growth, and we might have space for positive cash flow surplus;

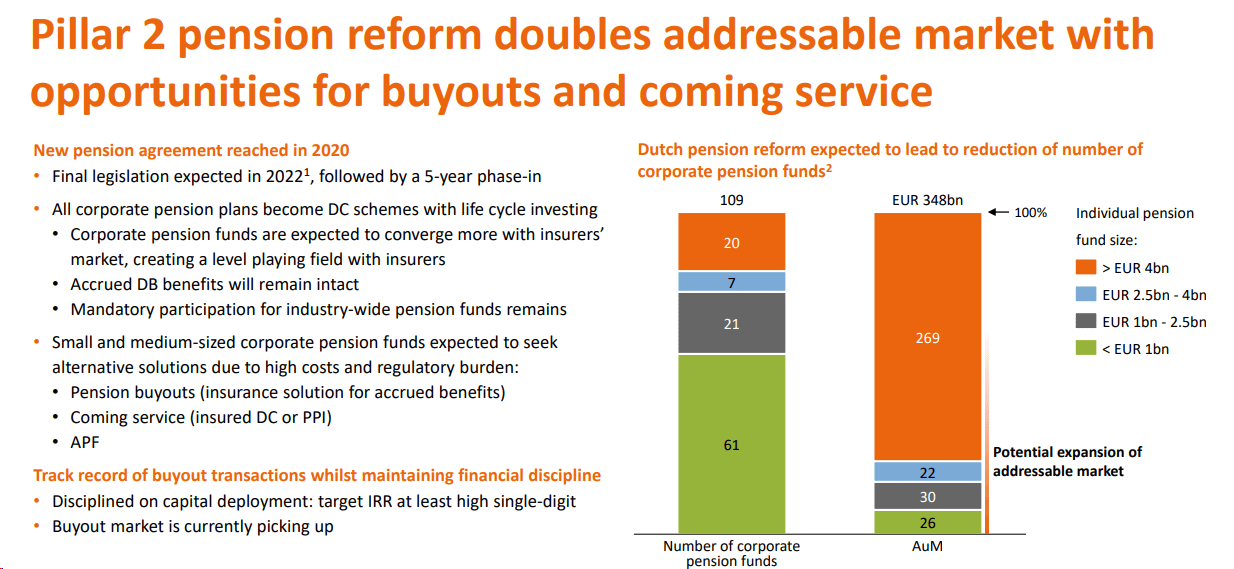

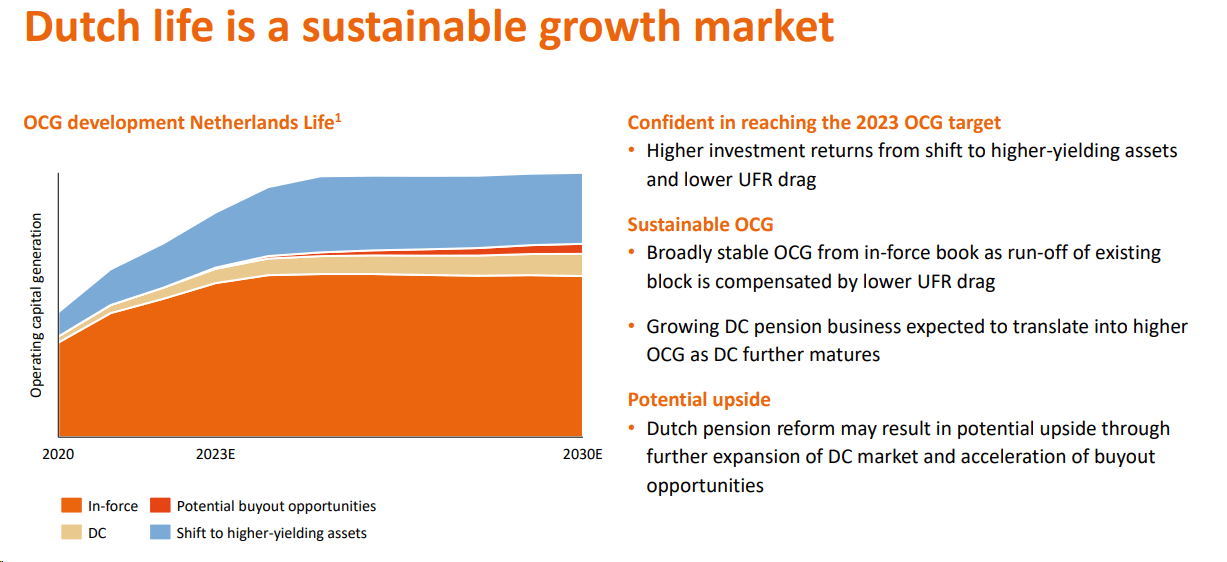

- (Attractive opportunity in the Dutch pension reform). We see the company as a beneficiary of the Dutch pension reform (Fig 1). In particular, this might lead to a significant transfer to NN Group solution from smaller pension funds. This might accelerate NN Group’s addressable market and smaller buyouts (Fig 2). As a reminder, the Dutch Senate adopted the new Pension Act, enacted in July 2023. That said, continuing to apply NN Group market share could mean a potential upside of approximately €10 billion in pension liabilities, equal to €200 million in organic capital generation. However, this growth might increase the solvency of own funds by almost €900 million;

- (Still above the regulatory requirements). After the negative one-off and following the two longevity transactions in mid-December, we believe the NN Group’s solvency ratio will be broadly higher by year-end. Trying to reverse engineer, we anticipate a Solvency II ratio of 192%. This is based on a 2023 operating profit of €2.5 billion. This also aligns with our previous publication called Financial Flexibility And A Solid Balance Sheet.

Dutch Pension Reform

Source: Investor & analyst deep-dive webinar (November 2021) – Fig 1

Dutch life growth market upside

Fig 2

Conclusion and Valuation

We have a DPS CAGR of 8% by 2025, with the company expected to grow its total dividend payment in line with free cash flow. In addition, there is a buyback optionality. NN Group is the most inexpensive compared to its peers and trades at 5.8x P/E (Aegon and Ageas trade at 6.5x and 6.6x P/E, respectively). In addition, the company is below its five-year average at 8.2x. With the significant overhang removed and a solid organic growth contribution, based on our forecast operating income, we arrive at an EPS of €6.5. Continuing to value the company with a target P/E of 8x, we increased our valuation from €44.8 to €52 per share. Downside risks in our target price include a low-interest rates environment, higher defaults in Dutch mortgages, new regulatory change, higher claims costs, and higher corporate expenses.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")