Wipada Wipawin

Investment thesis

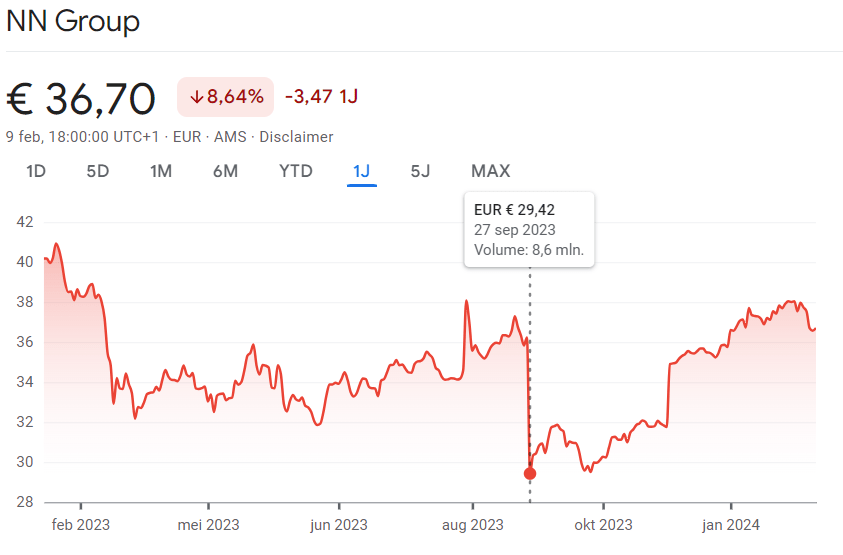

On the 3rd of September, I wrote my last article about NN Group (OTCPK:NNGPF). Since then, a lot has happened. On September 27, the share price plummeted -22% due to a huge increase in concerns about the unit-linked insurance products.

NN share price development (Google finance)

Hardly anyone saw the impact of the message coming, me included. At that time, it was also difficult to predict what the ultimate impact of this would be. This could vary from several hundred million to a few billion euros.

On this day, there was a lot of conversation on Seeking Alpha about NN and I wrote the following in the comments:

Unfortunately the stock price has fallen almost 19% today. Didn’t expected that to be honest. At the moment there is a lot of uncertainty, and the market clearly doesn’t like that. I really don’t like the fact that I can’t do the math at the moment. There are a lot of possible outcomes , with the possibility that it will be way higher than the previous estimates of 390 million.

The “woekerpolisaffaire” is a thing since 2006 and different dutch insurers already paid about 3 billion in claims and settlements since then.

However, not all policies have been registered with the advocates. Some policies have been sold and some holders have possibly died.

In addition, NN disagrees with interim judgment so the whole process isn’t done yet. It may take a long time before NN has to make payments.Maybe if they make a settlement NN is been able to spread out it’s payments.

This certainly impacts my investment thesis. In my opinion NN went from a low risk high reward investment to an investment with a higher risk profile. I still think NN has strong fundamentals and decent future prospects, they have strong capital generation of 1.8 billion and a solvency ratio of +200%, so they definitely can handle some headwinds.

Personally, I am not planning to sell my shares of NN, but I hope NN can provide us with some useful information and I will probably rewrite my thesis including these risks.

In these situations, it is good to take a step back and certainly not make emotional decisions. At that time, the investment thesis was definitely changed to a more risky investment profile. It was possible to buy shares of NN between €29-€32 euro per share, but there was way more risk involved. However, the strong fundamentals of the company made me hold my shares. Personally, I didn’t “buy the dip”, because of the extra investment risk involved, and I was willing to wait for NN to give some additional information about the unit-linked insurance policies.

Things were very unclear until the 29th of November, when ASR (ASRNL.AS), another Dutch insurance company that was also involved in the case, reached a final settlement. NN shares reacted very well on the news and the share price jumped about 10% during the day.

NN share price recovery (Google Finance)

On the 9th of January, NN also agreed a final settlement with different interest groups on unit-linked insurance products. This involved a total amount of €360 million. This total amount was on the lower end of the spectrum and since the announcement the share price is moving in an upward trend again.

Is it too late to invest in NN? I don’t think so because the company still has a lot to offer for income-oriented and dividend growth investors.

After rain comes sunshine

Now that we have looked back on the past, let’s look at the future again. So, what makes NN an interesting stock to own?

Business position

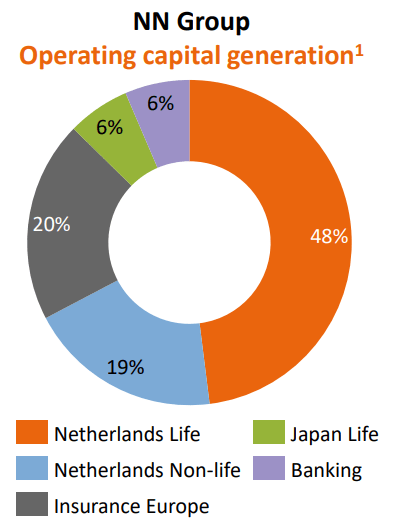

NN has international exposure, and they’re mainly active in Europe and Japan. However, the Netherlands is by far their biggest cash generator.

Geographic distribution capital generation (NN group investor presentation)

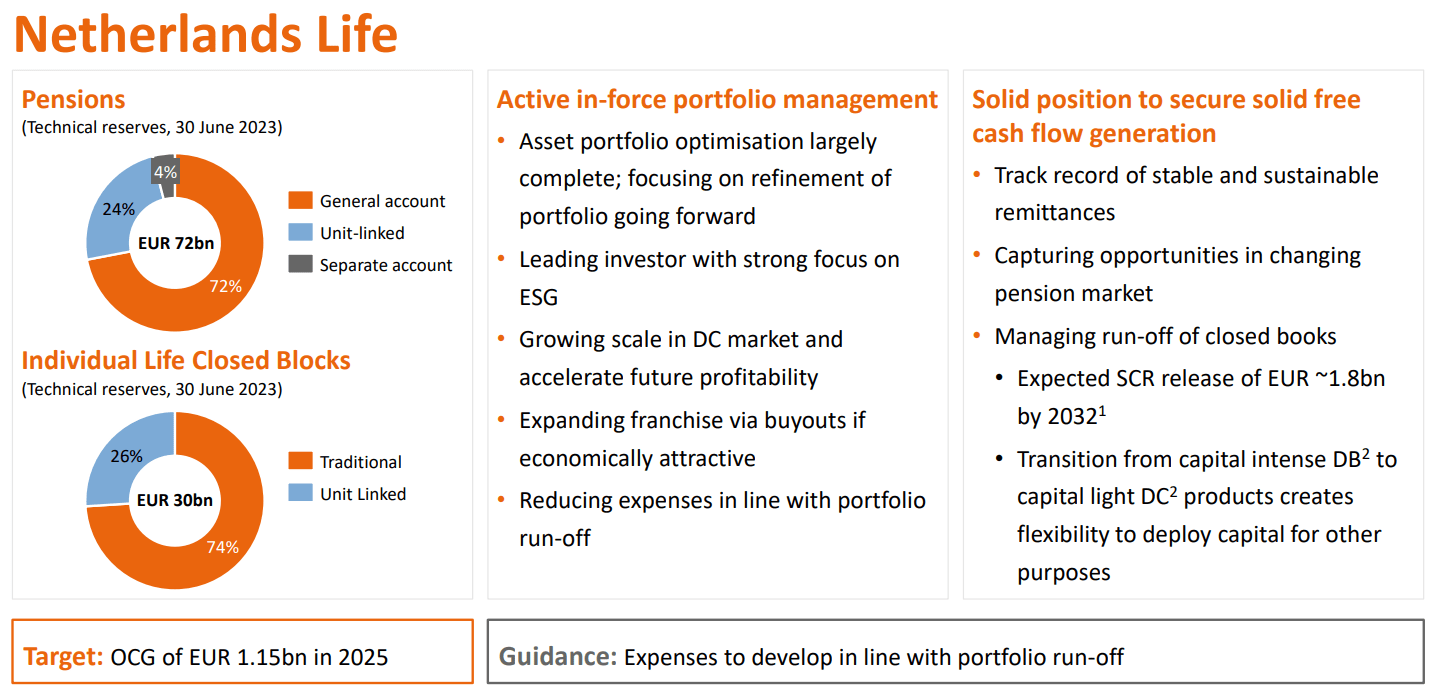

In the Netherlands, the company is a leader in life and non-life insurance. Don’t expect spectacular growth in the Netherlands, since the market is quite saturated. However, the cash flow generation is strong and there are several long-term opportunities where NN can benefit from.

The pension system in the Netherlands will undergo several changes. There will be a transition from Defined Benefit to Defined Contribution. The new pension act will be gradually introduced before the end of 2027. Defined Contribution offers the employee more flexibility since there are more options to choose from. This makes the new system more “custom-made”.

In the new system, scale is very important. It is possible that small to medium-sized pension funds will experience pressure due to new laws and regulations and will be bought out in the long term. From all the insurance companies in the Netherlands, it is likely that NN will benefit the most from it, since they have a 40% total market share. Since NN is in a good financial shape, it could take action at such times to expand its position.

NN Netherlands life segment (NN investor presentation august 2023)

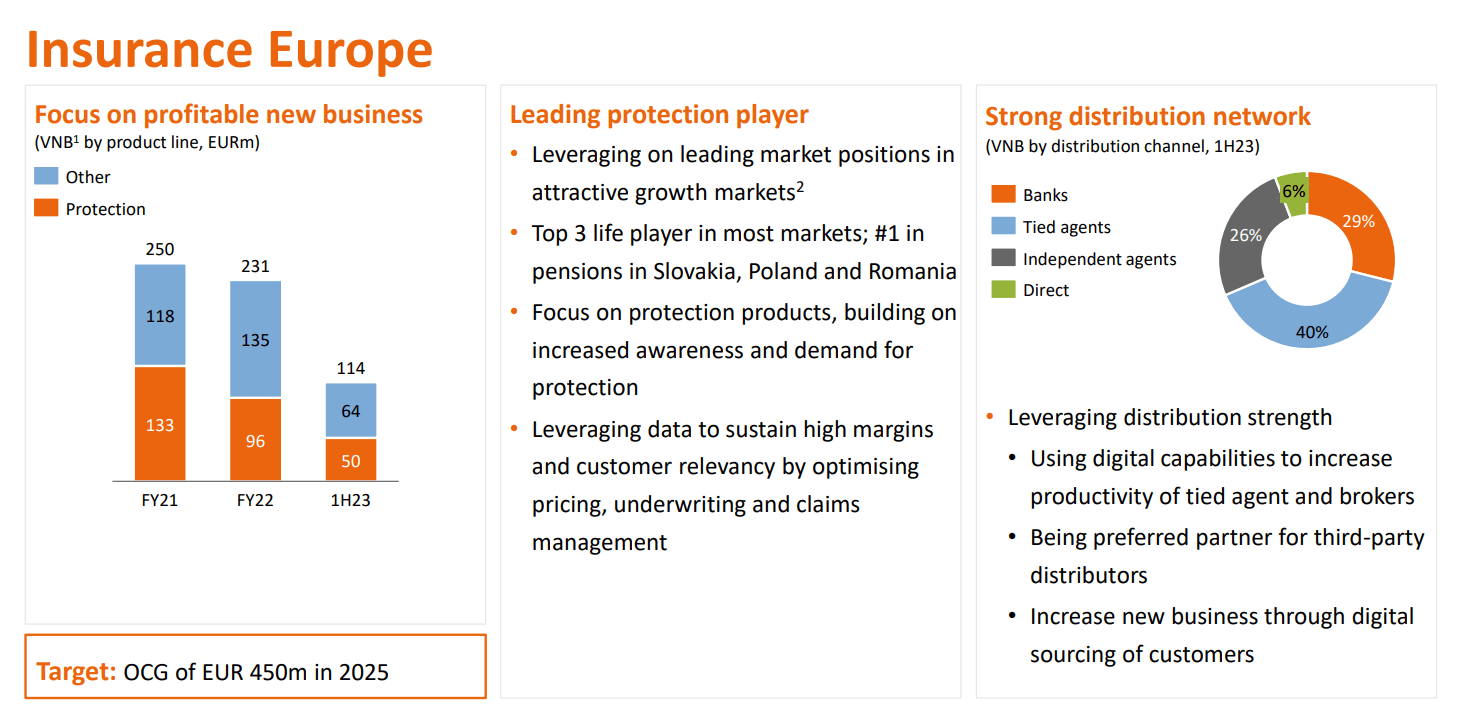

Insurance Europe is, in my opinion, one of the most important growth divers for NN Group. Compared to the Dutch insurance market in central and Southern Europe the markets aren’t fully penetrated. There is a shift towards protection products in this region and the company benefits from this.

Insurance Europe (NN investor presentation august 2023)

NN is expecting mid to high single-digit growth in operating capital generation from FY 2021 to FY 2025. The CEO, David Knibbe, is saying that they are already ahead of schedule when it comes to their target of €450 million in 2025.

Capital return policy

This is the core of my personal investment thesis. The company offers an attractive total shareholder return in the form of a growing dividend and share buybacks.

The most important part of their capital return policy is the dividend. NN intends to pay an interim and final dividend, and there is an option to choose between cash- or stock dividend. For all the USA-based readers that are interested, dividend tax is withheld at the rate of 15% from gross dividends distributed.

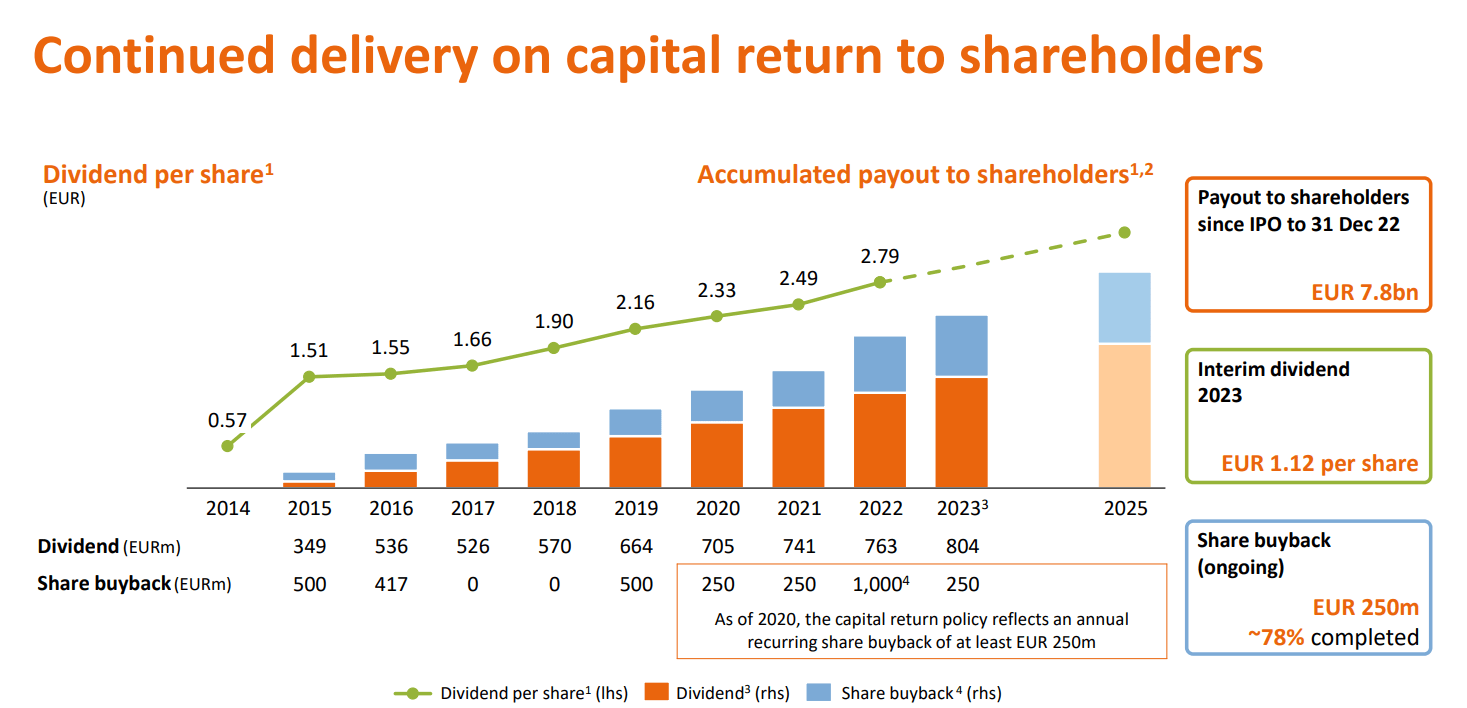

When it comes to the dividend metrics, the company ticks all the boxes. At the moment, NN has a dividend yield of 7.93%, which can be considered high. In a 5Y time frame (2018-2022) the dividend grew from €1.90 to €2.79, which implies a CAGR of 7.98%.

NN capital return policy (NN investor presentation august 2023)

There is even an acceleration in dividend growth, since NN has increased its latest interim dividend with 12% (€1.00 in FY 2022 to €1.12 in FY 2023). As a result of the settlement, NN group is planning a total double-digit percentage step-up of the dividend per share vs 2022.

analyst consensus final dividend (NN investor relations)

I expect the dividend increase to be in line with the 12% of the interim dividend, which should lead to a final dividend of €2.00 per share. In the long term, I expect the dividend growth will be more in line with its operating capital generation, which will be more in the mid-single digit range.

In my opinion, the dividend is relatively safe. The payout ratio in FY 2022 was 54.8% (€2.79 divided by €5.09 earnings per share). This gives the company enough room to increase the dividend in a sustainable manner and to make other investments if necessary.

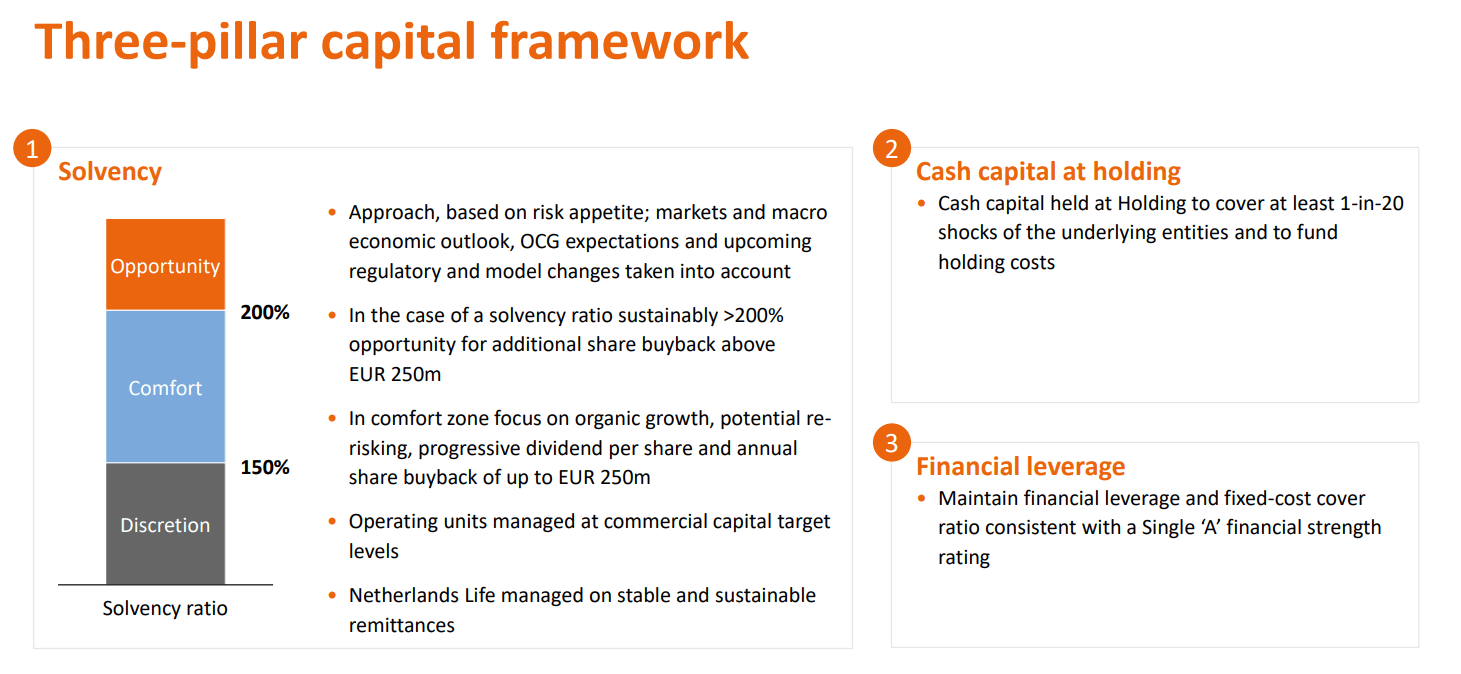

On top of this, they are planning a share buyback program of €250 million each year. If the solvency ratio is +200% it is likely that they will increase their share buybacks even more.

NN capital framework (NN investor presentation august 2023)

I like the fact that NN is doing share buybacks because I think the company is trading at attractive valuations. Currently, NN has a market cap of €10.36 billion. So, if the company is buying back at least 250 million in shares, we can add up another 2.4% to the total shareholder yield. Personally, I wouldn’t be surprised if NN is going to announce an increase in share buybacks during the 2H2023 results.

Financial health

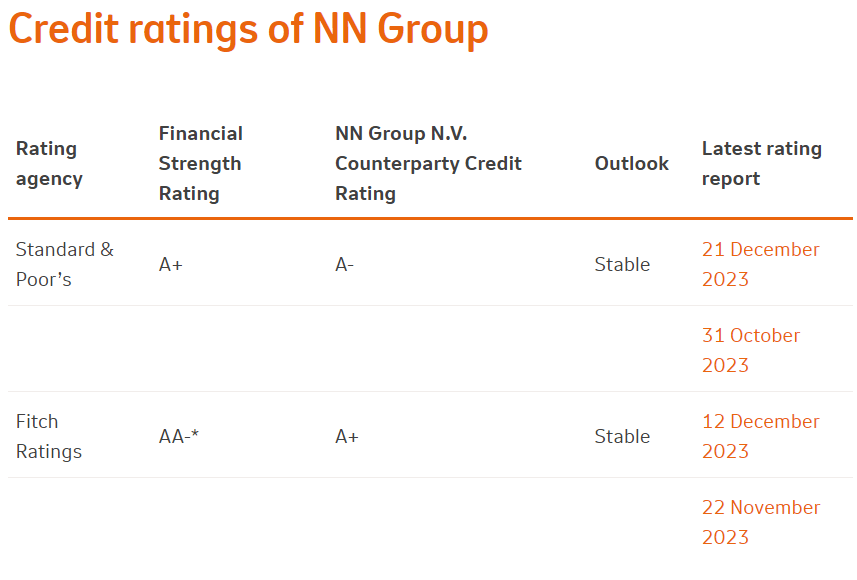

NN’s financial health is improving as well. The company has a strong solvency ratio of 201%, which enables them to return cash to shareholders, while maintaining a strong financial position. This has led to a positive upgrade from S&P Global. On December 21st, S&P global raised the credit rating of NN from A to A+.

NN group credit ratings (Investor relations)

Valuation

NN group is trading at a TTM price-to-book ratio of 0.48, which is significantly lower than the sector median of 1.08.

To calculate the fair value of NN Group, the dividend discount model was used. This model fits the company very well, and I am convinced that NN can grow its dividend at a constant rate.

I estimate that the total FY 2023 dividend will be €3.12 per share (€1.12 interim dividend + €2 final dividend). I used a rate of return of 12.5% because this is my personal rate of return on my investment. For the calculations, a relatively conservative dividend growth rate of 6% was used. This percentage is a bit below the 5 year CAGR of 7.98% and more in line with its growth in operating capital generation.

If we do the math, this comes to a fair value of €48 per share. Compared to the current share price of €36.70, NN Group is 30% undervalued.

Conclusion

After the settlement, the risk/reward profile for NN has improved drastically. NN is a company that has a lot to offer for income- and dividend (growth) investors. The company is a strong player in its operating segments, has a nicely diversified business mix and a strong solvency. NN clearly knows how to generate capital, which they return in large quantities to the shareholders in the form of growing dividends and share buybacks. In addition to this, share price appreciation can also be expected, since I think shares are undervalued.

Of course, there are also risks associated with investing in NN. Inflation is still higher than average. Persistent inflation can have a negative impact on claim costs, solvability, and labor costs. Weather conditions can also influence profitability. This actually turned out positively in the last half-year results, but this may be different in the future. In a world of rapid technological change, disruption can always occur from other companies like Big Tech or “InsurTech“.

Nonetheless, NN is one of my larger positions and I wouldn’t mind adding more at current levels. Even if the share price stays flat, you can still enjoy a total shareholder yield of +10%!

With all this in mind, I give NN a “BUY” rating. I am really looking forward to the 2H2023 results to see what they have in store for us.

PS: Shares of NN Group are listed on Euronext Amsterdam (NN.AS) and their ADRs trade on the OTC markets (OTCPK:NNGPF). I would encourage you to buy the shares from Euronext Amsterdam for liquidity reasons.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")